Sample Category Title

Yen and Franc Broadly Lower on Risk Appetite, Non-Farm Payrolls, Canadian Job and Eurozone CPI Eyed

Japanese Yen and Swiss Franc are trading as the weakest major currencies for the week on strong global risk appetite. Nikkei is extending recent rally in Asian session, after hitting 26 year high yesterday. DOW, S&P 500 and NASDAQ also closed at record highs again overnight, following the record high in FTSE. Commodity currencies and Euro are the main beneficiary in the current market sentiments. Dollar, on the other hand, stays generally weak except versus Yen and Franc. Non-farm payroll report, in particular wage data, will be key to whether the greenback can stage a turnaround. In addition, Canadian job data and Eurozone CPI will also be closely watched.

Wage growth is the key in NFP

Economists are expecting non-farm payrolls report to show 189k growth in December, unemployment rate to stay at 4.1%. Other employment related data released were solid. ADP reported showed stellar 250k growth in private sector jobs. Employment component of ISM manufacturing dropped from 59.7 to 57.0, but that's a healthy level. Meanwhile, the four week moving average of initial jobless claims was at 241.75k last week. It's more likely than not that NFP will show healthy job growth in December. The main question remains on wages. Average hourly earnings are expected to rise 0.3% mom, which leaves some room for downside surprise.

ISM services, factory orders and trade balance will also be released in the US.

Canadian job data also a focus

Canadian job data will also be clearly watched. Markets are expecting 0k job growth in December, after the surprisingly strong 79.5k growth in November. Unemployment rate is expected to climb back by 0.1% to 6.0%. Canadian Dollar has been notably strong in recent weeks as economic data revived speculations of another BoC rate hike in January. Also, recent surge in oil price also helped the Loonie. WTI crude oil extended recent bullish run and surges through 62 handle overnight. We'd probably get another up-leg in the Loonie should job data surprises on the upside today.

Trade balance and Ivey PMI will also be released from Canada.

Eurozone CPI as highlight of European session

Eurozone inflation data will be another key event to watch. Headline CPI is expected to slow by 0.1% to 1.4% yoy in December. Core CPI, on the other hand, is expected to accelerate 0.1% to 1.0% yoy. PPI is expected to be unchanged at 2.5% yoy. Eurozone will release retail PMI and German retail sales. Swiss Foreign currency reserves is also featured in European session.

Elsewhere

From Australia, trade balance unexpectedly turn into AUD -0.63b deficit in November, much worse than expectation of AUD 0.55b surplus. Japan monetary base rose 11.2% yoy in December. UK BRC shop price index dropped -0.6% yoy in December.

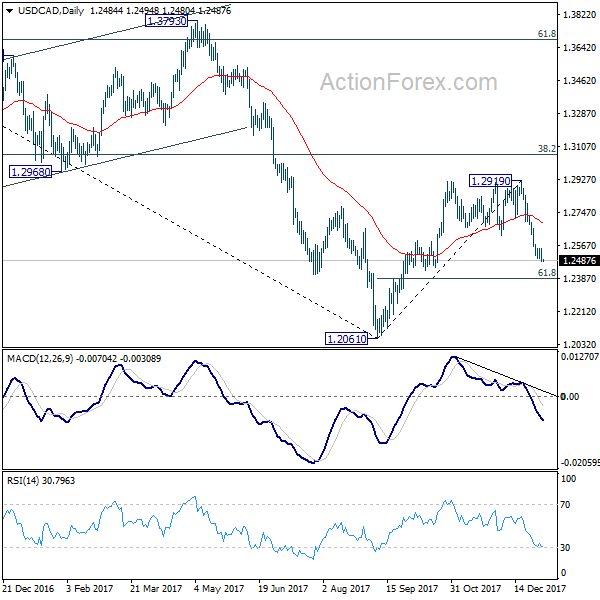

USD/CAD Daily Outlook

Daily Pivots: (S1) 1.2462; (P) 1.2508; (R1) 1.2534; More....

USD/CAD's decline resumed after brief consolidation and reaches as low as 1.2480 so far. Intraday bias is back on the downside. Current fall from 1.2919 should target 61.8% retracement of 1.2061 to 1.2919 at 1.2389. We'll look for bottoming signal below there. On the upside, break of 1.2554 resistance is needed to indicate short term bottoming. Otherwise, outlook will remain bearish in case of recovery.

In the bigger picture, we're still favoring the case that USD/CAD has defended 50% retracement of 0.9406 (2011 low) to 1.4689 (2016 high) at 1.2048. And with 1.2048 intact, we'd favor the case that fall from 1.4689 is a correction. With that in mind, fall from 1.2919 is viewed as a correction. Hence, we're not anticipating a break of 1.2061 low. In the long run, USD/CAD should have another medium term rise to take on 38.2% retracement of 1.4689 to 1.2061 at 1.3065.

Economic Indicators Update

| GMT | Ccy | Events | Actual | Forecast | Previous | Revised |

|---|---|---|---|---|---|---|

| 23:50 | JPY | Monetary Base Y/Y Dec | 11.20% | 13.20% | ||

| 00:01 | GBP | BRC Shop Price Index Y/Y Dec | -0.60% | -0.10% | ||

| 00:30 | AUD | Trade Balance (AUD) Nov | -0.63B | 0.55B | 0.11B | -0.30B |

| 07:00 | EUR | German Retail Sales M/M Nov | 1.00% | -1.20% | ||

| 08:00 | CHF | Foreign Currency Reserves (CHF) Dec | 738B | |||

| 09:10 | EUR | Eurozone Retail PMI Dec | 52.4 | |||

| 10:00 | EUR | Eurozone PPI M/M Nov | 0.30% | 0.40% | ||

| 10:00 | EUR | Eurozone PPI Y/Y Nov | 2.50% | 2.50% | ||

| 10:00 | EUR | Eurozone CPI Core Y/Y Dec A | 1.00% | 0.90% | ||

| 10:00 | EUR | Eurozone CPI Estimate Y/Y Dec | 1.40% | 1.50% | ||

| 13:30 | CAD | International Merchandise Trade (CAD) Nov | -1.3B | -1.5B | ||

| 13:30 | CAD | Net Change in Employment Dec | 0.0K | 79.5K | ||

| 13:30 | CAD | Unemployment Rate Dec | 6.00% | 5.90% | ||

| 13:30 | USD | Change in Non-farm Payrolls Dec | 189K | 228K | ||

| 13:30 | USD | Unemployment Rate Dec | 4.10% | 4.10% | ||

| 13:30 | USD | Average Hourly Earnings M/M Dec | 0.30% | 0.20% | ||

| 13:30 | USD | Trade Balance Nov | -48.1B | -48.7B | ||

| 15:00 | CAD | Ivey PMI Dec | 62.2 | 63 | ||

| 15:00 | USD | ISM Non-Manufacturing/Services Composite Dec | 57.6 | 57.4 | ||

| 15:00 | USD | Factory Orders Nov | 1.40% | -0.10% |

Market Morning Briefing: The Pound Trades Higher

STOCKS

Dow (25075.13, +0.61%) is trading just below weekly resistance at 25000 while the daily and the 3day candles show some more scope on the upside. While below 25000, the index could trade sideways for a few sessions before trying to move up towards 25400 levels.

Dax (13167.89, +1.46%) continues to trade within the 13200-12800 region. It may test the immediate resistance at 13200 in the next few sessions and attempt another fall towards 12800. Note that 12800 is a long term support and is likely to hold in the longer term eventually taking the index above 13200 in the coming weeks.

The sharp surge in Nikkei (23547.78, +0.18%) has come in much later than our expectations as indicated by the Dollar Yen (112.824) and the US-Japan 10Yr yield (2.41%) spread during mid of Dec'17. However while the yield spread heads towards 2.4% or higher and the Dollar Yen moves up to test 113 or higher, Nikkei could move higher towards 23600-23800 in the medium term with some interim dips.

Shanghai (3387.79, +0.07%) is looking strong just now and is likely to move up towards resistance at 3500 in the coming sessions.

Nifty (10504.80, +0.59%) and Sensex (33969.64, +0.52%) will have to break and sustain above 10550 and 34200 levels respectively to turn more bullish just now. A sharp surge on the upside looks unlikely and the indices may remain ranged in the near term. Immediate supports near 10400 and 33600 is holding well for now.

COMMODITIES

Gold (1321.89) has moved up sharply from levels near 1308. While the US Dollar Index moves down towards 91, Gold is likely to test 1350 on the upside before coming off from there to levels near 1300 and lower in the medium term. Near term looks bullish.

Brent (67.96) and WTI (61.94) are trading at crucial resistance levels and if that holds, a corrective dip is possible in the coming sessions; else the prices could keep moving upwards to test fresh highs in the current rally breaking above near term resistances. WTI has indicated a break above the weekly resistance near 59-60 levels and while that sustains, it could well move up towards 64. Brent has almost moved up towards 68 as expected in our earlier predictions but will now have to move up beyond 68 to record fresh highs.

Copper (3.2680) may get some support near 3.20 which if holds could take the metal to levels near 3.35-3.40 in the medium term. 3.40 could thereafter act as an important long term resistance. For now Copper looks sideways to bullish for the coming sessions.

FOREX

Euro (1.2077) held above the 1.1997 Support yesterday and may move up to 1.2150 while above 1.20. Break below 1.20 sets up test of stronger Support at 1.19, delaying but not negating rise to 1.2150.

Dollar-Yen (112.82) did not break below 112 yesterday and may try to weakly test the 113.00-50, as the bounce could fizzle out. The Euro-Yen (136.22) has risen past the resistance at 135.70 mentioned yesterday. This opens up chances of a rise towards 1.38, after the multi-month sideways consolidation between 132-134.

The Pound (1.3562) trades higher and may well rise past 1.36 as well. The Aussie (0.7852) seems to be breaking above the 200-week Moving Average mentioned yesterday and may rise further towards 0.80.

Dollar-Rupee should have Resistance in the 63.60-80 region and can test 63.30-10 along with Euro strength.

US Dollar Weak Ahead of US Jobs Report

Inflation data in Europe and US to guide Market

The USD fell on Thursday despite a strong private jobs report released in the morning. The ADP showed that 250,000 jobs were added in December beating a forecast of 190,000 positions. Bears continue to pressure the greenback as the U.S. Federal Reserve is losing its status as the lone central bank tightening monetary policy. The EUR is near three year highs as economic growth has put the European Central Bank (ECB) in a position to start removing stimulus on its way to higher rates. Rising political risk in the US has led the growth and monetary policy stories from having less impact ahead of this year's primaries.

- NFP expected to show 190,000 jobs gain in December

- Canadian Jobs expected with slight gain after massive November numbers

- European flash inflation could cool euro pace

The U.S. non farm payrolls (NFP) will be released by the Bureau of Labor Statistics on Friday, January 5 at 8:30 am EST. The forecast calls for more than 190,000 jobs to have been added in December but more importantly the average hourly wages to have gained 0.3 percent. The Fed is torn between members who want to wait for more signs of inflation before committing to higher rate hikes and those who want to hike sooner rather than later.

The EUR/USD rose 0.46 percent on Thursday. The single pair is trading at 1.2070 after the release of various Service PMI reports published in the morning. The sense that European indicators continue to improve was enough to keep the USD from gaining after a strong ADP report. This is something that could play out again tomorrow when the inflation estimates for Europe are leased on Friday, January 5 at 5:00 am EST. Inflation has not recovered evenly in the EU, with Germany at a five year high, but countries such as Italy still stuck in negative price pressures. The European Central Bank (ECB) has signalled that is ready to start tapering its QE program, but it awaits more clarity on inflation. A strong preliminary inflation report could end up hurting the dollar, even if the NFP report beats expectations.

The U.S. Federal Reserve raised rates three times in 2017, but the path of monetary policy is unclear in 2018 as Fed Chair Janet Yellen is soon to step back with Jerome Powell taking her place at the head of the central bank. A US interest rate hike in January is unlikely with the CME FedWatch tool showing market participants expect the Fed to stand pat at 99.5 percent probability. The rhetoric from other central banks has moved closer to ending lower rates which has put pressure on the US dollar as investors seek better yields.

The USD/CAD has lost 0.73 percent during the week. The currency pair is trading at 1.2488 as once again the loonie has managed to trade under 1.25. The surge in the price of oil has supported the Canadian currency as the correlation has gotten stronger. The geopolitical risk driving the commodity and the NAFTA risk as the treaty is under review could turn negative for the CAD. Canadian employment data will be published on Friday. Canada is expected to have added 1,800 jobs in December a far cry form the close to 80,000 positions created in November. The unemployment rate is forecasted to rise to 6.0 percent.

Economic indicators improved in the first half of 2017, prompting the Bank of Canada (BoC) to raise rates twice to put the benchmark rate at 1.00 percent. This is the same rate from 2015 before the BoC cut pro actively to avoid the drop in oil prices. While the gap between Canadian and American interest rates is expected to grow in 2018 the BoC Governor Stephen Poloz will not make a proactive move like the two rate cuts in 2015. that monetary policy decision was the result of an anticipated drop in oil prices. With the price of West Texas Intermediate above $60 the BoC can afford to wait. Mr. Poloz has said that that current interest rates were still too low and would hike although he was in no rush to do so.

Next in the Canadian economic calendar will be the release of employment data on Friday, January 5 at 8:30 am EST. Statistics Canada reported a gain of 79,500 positions in November, and the forecast calls for a loss of 2,500 in December with an unemployment rate of 6 percent. US jobs data will also be released at the same time with the U.S. non farm payrolls (NFP) expected to show a gain of 190,000 positions. The wage component will be closely scrutinized for signs of inflation with an expected 0.3 percent in hourly earnings. The USD could start a rally if the NFP report shows a definite improvement in wage growth but if it misses it will continue to be a disappointing start for the greenback in 2018.

Market events to watch this week:

Friday, January 5

- 5:00am EUR CPI Flash Estimate y/y

- 8:30am CAD Employment Change

- 8:30amCAD Trade Balance

- 8:30am USD Average Hourly Earnings m/m

- 8:30am USD Non-Farm Employment Change

- 10:00am USD ISM Non-Manufacturing PMI

*All times EDT

Market Trends to Watch for in 2018

Capital Market trends investors will be looking at for 2018

Crypto-currencies: Bitcoin – the rise of regulators

U.S corporate tax cuts: What's the 'real' potential?

Interest rate differentials: Central banks tapering – since 2008, G10 central banks have been employing expansionary monetary policies to stimulate their economies. With growth around the globe now looking healthier, the trend has started to reverse. How far can G10 yields back up? Will the BoJ be the exception?

Brexit negotiations: Will Theresa May remain Prime Minister in 2018? Hard Brexit vs. soft Brexit depends on the flexibility from both sides (U.K and E.U).

Growth prospects in Emerging Market: India and China performed especially well in 2017. Can the trend continue?

New Fed head in February: Is the market "underpricing Federal Reserve hikes and U.S. tax reform impact?

Fallout of MiFiD

Russian inquiry: Will impeachments proceedings begin against President Trump?

Global re-ordering: The potential for a U.S/China trade war

U.S Midterm's: Will the U.S democrats take back a majority in the November midterm elections in the U.S House of Representatives?

OPEC: Will crude prices finish 2018 above $70? How much of a threat to oil prices is U.S shale production?

2018 Geo-political Calendar Events:

January

U.S President Donald Trump delivers his first State of the Union address

February

Winter Olympics in South Korea

Raúl Castro set to step down as Cuba's president

U.S Federal Reserve chair Janet Yellen to step down

March

UK hopes to agree to a Brexit transition deal

Vladimir Putin expected to win Russia's presidential elections.

Italian general election, with the Eurosceptic Five Star Movement leading the polls

Venezuela voting could be held, with Nicolás Maduro having a good chance of re-election

May

Iraq elections

June

World Cup held in Russia

G7 summit in La Malbaie, Canada

July

Mexico general elections

September

Sweden general elections

October

Brexit deal signature expected (tentative)

Brazil general elections

November

U.S midterm elections

December

G20 summit in Buenos Aires

Gold Gains Ground on Mixed US Employment Data

Gold has rebounded on Thursday, posting considerable gains. In North American trade, the spot price for an ounce of gold is $1381.81, up 0.41% on the day. On the release front, ADP Payrolls report jumped to 250 thousand, crushing the estimate of 191 thousand. However, unemployment claims rose to 250 thousand, higher than the forecast of 241 thousand. The focus remains on job data on Friday, with the release of Average Hourly Earnings and Nonfarm Payrolls. Traders should be prepared for some movement in gold prices in Friday's North American session.

The highly-anticipated Federal Reserve minutes were released on Wednesday. The minutes provided details of the December policy meeting, where the Fed raised interest rates for a third time in 2018. The minutes were positive in tone, reflecting a robust US economy. Policymakers noted that economic activity was expanding at a "solid pace", buoyed by improved consumer and business spending, as well as a stronger global economy. FOMC members revised upwards their projection for GDP in 2018, from 2.1% to 2.5%. The minutes noted that new tax reform is expected to raise economic growth, but the Fed is unsure on the impact of the new law in areas such as the labor market. As for inflation, Fed officials remain concerned that inflation levels are well below the target of 2%, and this trend could continue.

US employment numbers were a mixed bag on Thursday, which weighed broadly on the US dollar. Will we see a repeat on Friday? The markets are expecting wage growth to improve to 0.3%, but are braced for a slowdown from Nonfarm Payrolls. Investors will be keeping a keen eye on these December releases, as will the Federal Reserve. Currently, the odds of a January rate hike are at 99.5%, according to the CME. However, a poor showing by Nonfarm Payrolls could lower these odds and send the US dollar to lower ground.

Canadian Dollar Inches Lower, Markets Eye US, Canadian Job Numbers

The Canadian dollar has ticked lower in the Wednesday session. Currently, the pair is trading at 1.2520, down 0.12%. On the release front, US employment numbers were a mixed bag. The ADP Payrolls report jumped to 250 thousand, crushing the estimate of 191 thousand. However, unemployment claims rose to 250 thousand, higher than the forecast of 241 thousand. In Canada, RMPI jumped 5.5%, compared to 3.8% a month earlier. On Friday, there are key events on both sides of the border, led by US Nonfarm Payrolls, wage growth and Canadian Employment Change. Traders should be prepared for some movement from USD/CAD during Friday's North American session.

As expected, the Federal Reserve minutes from December were positive in tone. At that meeting, the Fed raised interest rates for a third time in 2017. Policymakers noted in the minutes that economic activity was expanding at a "solid pace", buoyed by improved consumer and business spending, as well as a stronger global economy. FOMC members revised upwards their projection for GDP in 2018, from 2.1% to 2.5%. The minutes noted that new tax reform is expected to raise economic growth, but the Fed is unsure on the impact of the new law in areas such as the labor market. As for inflation, Fed officials remain concerned that inflation levels are well below the target of 2%, and this trend could continue.

The Canadian dollar started the New Year on a positive note, as USD/CAD briefly broke below the 1.25 line for the first time since mid-October. The currency enjoyed a respectable 2017, posting gains of 6.6% against its US cousin. Will the positive trend continue in January? With the US economy booming, the Federal Reserve raised rates in December, and another move is expected this month. This will put strong pressure on the Bank of Canada to match with a rate hike, or risk seeing the Canadian dollar lose ground as investors move to a more attractive US dollar.

DAX Jumps as Services PMIs Climb

The DAX has posted strong gains in the Thursday session. In North American trade, the index is at 13,185.50, up 1.57% on the day. The index is currently at a 2-week high. On the release front, German Final Services PMI improved to 55.8, matching the forecast. Eurozone Final Services PMI followed suit, climbing to 56.6, which edged above the estimate of 56.5 points. Friday will be busy, as the Germany releases retail sales, and the eurozone publishes CPI Flash Estimate.

Germany's economy continues to impress, as fourth quarter numbers point upwards. Manufacturing and services PMIs gained ground in December, and inflation accelerated to 0.6%, edging above the forecast of 0.5%. The strong gain matched the February reading, equaling the strongest gain recorded in 2017. Unemployment rolls continue to fall, as the labor market continues to remain tight in a robust economy. The numbers are all the more impressive as the political landscape remains uncertain, following inconclusive elections in September. President Angela Merkel is now eyeing the Social Democrats as a coalition partner, but negotiations are moving at a slow pace.

European stock markets have posted strong gains on Thursday, buoyed by sharp German and eurozone Services PMIs. These releases come on the heels of strong Manufacturing PMIs in Germany and the eurozone. With the manufacturing and services sectors continuing to expand, investors like what they see in Europe, and the euro and the DAX have pushed higher on Thursday. German Retail Sales are expected to rebound in December, with an estimate of 1.0%. If the indicator meets or beats expectations, the DAX rally could continue.

Eurozone Inflation: Will it Determine the Euro’s Short-Term Bias?

Eurozone's preliminary inflation figures for December are due out on Friday at 10:00 GMT, and forecasts project both the headline and the core CPI rates to tick down. With inflation likely to continue undershooting the ECB's target over the coming years, will the Bank maintain its current degree of stimulus beyond September?

Inflation in the euro area has been subdued in recent years – and it's expected to remain so for a while longer. According to the European Central Bank's (ECB) latest projections, core inflation (excluding food and energy) is not anticipated to meet its target of "below, but close to 2%" until 2020. This is probably the main driver behind the ECB's willingness to continue buying massive amounts of assets under its QE program; if it stops too early, inflation may take even longer to reach the target.

Does that mean the ECB is locked in? Under its current forward guidance, the Bank has pledged to continue QE until "September 2018, or beyond, if necessary, and in any case until the Governing Council sees a sustained adjustment in the path of inflation". If one relies solely on this guidance in the context of low inflation, then a strong argument can be made that the Bank could extend QE beyond September.

Alas, guidance can change. Following the October gathering – where the ECB announced its QE extension – several key policymakers including Jens Weidmann hinted at the possibility of decoupling the Bank's forward guidance on QE from requiring a sustained pickup in inflation. Such a change would pave the way for the Bank to reduce (or end) its purchases even while inflation remains below-target. This prospect has appeared even more likely lately, after ECB officials Benoit Coeure and Ewald Nowotny suggested the Bank could end its QE program in 2018 provided growth remains solid and inflation doesn't disappoint.

This brings us to this week's release of inflation data. The consensus is for both the headline and the core CPI rates to decline marginally, to 1.4% and 1.0% respectively on a yearly basis. However, such prints will hardly be a shocker for the ECB. The Bank's own forecasts already project the headline CPI to end the year at 1.5% and the core at 1.0%. Thus, if the forecasts are simply met, these data are likely to have little impact on ECB decisions and by extent, on the euro.

That said, a potential upside surprise in these rates – and particularly in the core – could amplify further the case for the Bank to end its QE program this year. Something like that could encourage euro/dollar bulls to take the reins and perhaps aim for another test of the 1.2080 zone, where a clear break could open the way for the 1.2130 area, marked by the lows of August 2012. On the other hand, a larger-than-expected decline in the CPI rates could heighten speculation that the Bank may extend QE again. In this scenario, the bears could drive the pair lower, aiming initially for the psychological territory of 1.2000. A decisive break below that level could set the stage for more bearish extensions, towards 1.1960. Lastly, it is paramount to note that much of the pair's forthcoming direction will also be decided by the US employment data for December, due out a few hours after Eurozone's CPIs.

Euro Gains on Strong German, Eurozone Services Reports

The euro has posted gains in the Thursday session, erasing the losses seen on Wednesday. Currently, EUR/USD is trading at 1.2079, up 0.53% on the day. On the release front, German Final Services PMI improved to 55.8, matching the forecast. Eurozone Final Services PMI followed suit, climbing to 56.6, which edged above the estimate of 56.5 points. In the US, employment numbers were a mixed bag. The ADP Payrolls report jumped to 250 thousand, crushing the estimate of 191 thousand. However, unemployment claims rose to 250 thousand, higher than the forecast of 241 thousand. Friday will be busy, as the Germany releases retail sales, and the eurozone publishes CPI Flash Estimate. In the US, the focus remains on job data, with the release of Average Hourly Earnings and Nonfarm Payrolls.

The Federal Reserve minutes were positive in tone, but not overly hawkish. As a result, the US dollar remains under pressure as the euro has risen on Thursday. Policymakers noted that economic activity was expanding at a "solid pace", buoyed by improved consumer and business spending, as well as a stronger global economy. FOMC members revised upwards their projection for GDP in 2018, from 2.1% to 2.5%. The minutes noted that new tax reform is expected to raise economic growth, but the Fed is unsure on the impact of the new law in areas such as the labor market. As for inflation, Fed officials remain concerned that inflation levels are well below the target of 2%, and this trend could continue.

German numbers continue to look sharp. Manufacturing and services PMIs gained ground in December, and inflation accelerated to 0.6%, edging above the forecast of 0.5%. The strong gain matched the February reading, equaling the strongest gain recorded in 2017. Unemployment rolls continue to fall, as the labor market continues to remain tight in a robust economy. The numbers are all the more impressive as the political landscape remains uncertain, following inconclusive elections in September. President Angela Merkel is now eyeing the Social Democrats as a coalition partner, but negotiations are moving at a slow pace.

EURCHF Continues to Strengthen; Next Level to Watch 1.2095

EURCHF has been trading within an ascending move since August 2017 and during last week's session, it posted an almost three-year high of 1.1775. Thursday could be the third green day in a row and a rise above the aforementioned level should drive the pair up to the 1.2095 resistance level, near the previous' three years peg level, and the high of December 2014.

Short to medium-term trend indicators on the daily chart (50, 100 and 100-period simple moving averages) are moving to the upside, showing some signals for further gains.

The market became more positive following last week's peak as was indicated by the RSI's strong bullish movement, while it is ready to touch the 70 overbought level and there is no subsequent retracement for the pair to the downside today. In addition, the MACD oscillator is rising in the positive territory, slightly above the trigger line.

On the downside, a clear break below the ascending trend line could indicate the market a clear bearish correction until the 1.1600 significant psychological level or moreover until the 38.2% Fibonacci mark with the low at 1.1260 and the high at 1.1775, near 1.1576.