Sample Category Title

Euro Shines on Upbeat Data, Dollar Recovery Fails Again

The pattern continues today with Dollar trying to recovery but fails. Economic data from US are solid but that gives little support to the greenback. Instead, Euro shines today as PMI data confirmed a "stellar" end to 2017, as the best year for over a decade. Released from US, ADP report showed 250k growth in private sector jobs in December, above expectation of 190k. Initial claims rose 5k to 250k in the week ended December. Challenger report showed -3.6% yoy fall in planned layoffs in December. From Canada, IPPI rose 1.4% mom in November. RMPI rose 5.5% mom.

Eurozone economy had best year for a decade in 2017

Eurozone PMI services was revised up by 0.1 to 56.6 in December. Germany PMI services was unrevised at 55.8. France PMI services was revised lower by 0.3 to 59.1. Italy PMI services dropped 0.1 to 54.6 in December. Markit noted that "a stellar end to 2017 for the euro zone rounded off the best year for over a decade, continuing to confound widely held fears that rising political uncertainty would curb economic growth." Also, "based on past experience, the extent to which demand appears to be outstripping supply for many goods and services suggests that inflationary pressures could continue to build in the coming months."

UK services PMI beat expectation

UK PMI services rose to 54.2 in December, up from 53.8 and beat expectation of 54.0. After disappointment from manufacturing and construction PMIs, there's finally a better than consensus piece of data. Markit noted that the set of PMI data suggests 0.4-0.5% growth in UK GDP in Q4. But Markit chief economist Chris Williamson also cautioned that "as has been increasingly the case in recent months, the good news comes with a health warning about the sustainability of the upturn." He added "digging into the details behind the resilient strength signaled by the headline numbers, the survey data reveal an economy that is beset with uncertainty about the outlook, which is in turn dampening business spending and investment."

Also from UK, Nationwide house price rose 0.6% mom in December. Mortgage approvals rose to 65.1k in November, M4 rose 0.1% mom.

Released earlier today, Japan PMI manufacturing was revised down to 54 in December. China Caixin PMI services rose to 53.9 in December, up from 51.9, above expectation of 51.8.

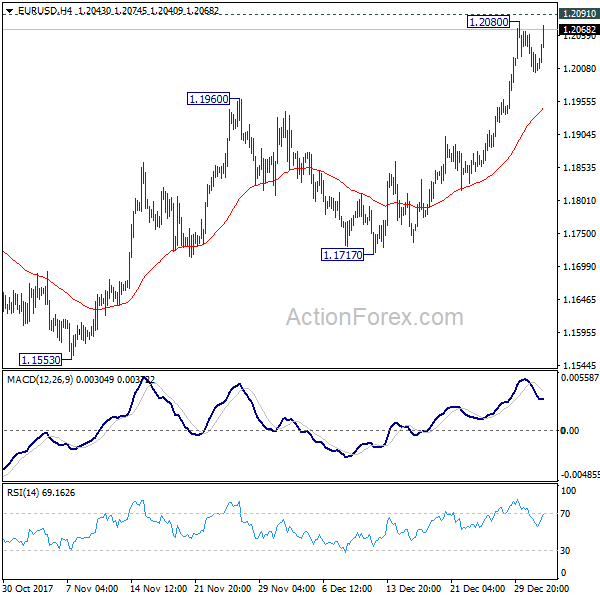

EUR/USD Mid-Day Outlook

Daily Pivots: (S1) 1.1987; (P) 1.2026 (R1) 1.2052; More....

EUR/USD rebounds strongly today but stays below 1.2091 resistance. Intraday bias remains neutral first. Further rise is expected as long as 4 hour 55 EMA (now at 1.1946) holds. Firm break of 1.2091 will confirm medium term rally resumption and target next key fibonacci level at 1.2494/2516. However, sustained break of 4 hour 55 EMA will extend the consolidation pattern from 1.2091 with with another decline through 1.1717 support.

In the bigger picture, rise from 1.0339 medium term bottom is seen as a corrective move for the moment. Therefore, in case of another rally, we'd be expect 38.2% retracement of 1.6039 (2008 high) to 1.0339 (2017 low) at 1.2516 to limit upside and bring reversal. That is also close to 61.8% projection of 1.0569 to 1.2091 from 1.1553 at 1.2494.

Economic Indicators Update

| GMT | Ccy | Events | Actual | Forecast | Previous | Revised |

|---|---|---|---|---|---|---|

| 00:30 | JPY | PMI Manufacturing Dec F | 54 | 54.2 | 54.2 | |

| 01:45 | CNY | Caixin PMI Services Dec | 53.9 | 51.8 | 51.9 | |

| 07:00 | GBP | Nationwide House Price M/M Dec | 0.60% | 0.10% | 0.10% | |

| 08:45 | EUR | Italy Services PMI Dec | 54.6 | 54.7 | 54.7 | |

| 08:50 | EUR | France Services PMI Dec F | 59.1 | 59.4 | 59.4 | |

| 08:55 | EUR | Germany Services PMI Dec F | 55.8 | 55.8 | 55.8 | |

| 09:00 | EUR | Eurozone Services PMI Dec F | 56.6 | 56.5 | 56.5 | |

| 09:30 | GBP | Mortgage Approvals Nov | 65.1k | 64.1k | 64.6k | 64.9k |

| 09:30 | GBP | Money Supply M4 M/M Nov | 0.10% | 0.40% | 0.60% | |

| 09:30 | GBP | Services PMI Dec | 54.2 | 54 | 53.8 | |

| 12:30 | USD | Challenger Job Cuts Y/Y Dec | -3.60% | 30.10% | ||

| 13:15 | USD | ADP Employment Change Dec | 250K | 190k | 190k | 185K |

| 13:30 | CAD | Industrial Product Price M/M Nov | 1.40% | 0.80% | 1.00% | 1.10% |

| 13:30 | CAD | Raw Materials Price Index M/M Nov | 5.50% | 4.00% | 3.80% | |

| 13:30 | USD | Initial Jobless Claims (DEC 30) | 250K | 244K | 245K | |

| 14:45 | USD | US Services PMI Dec F | 52.4 | 52.4 | ||

| 15:30 | USD | Natural Gas Storage | -221B | -112B | ||

| 16:00 | USD | Crude Oil Inventories | -5.2M | -4.6M |

Dollar Depressed ahead of ADP Report

This is certainly shaping up to be another painful trading week for the Dollar. Bulls were nowhere to be found during Thursday's trading session, despite the release of yesterday's somewhat hawkish Federal Reserve minutes. While policymakers expressed optimism over the US labour markets, and believe that tax cuts could stimulate consumer spending, concerns over low levels of inflation lingered throughout the meeting minutes.

Today's main risk event for a tired Dollar will be the US ADP private sector jobs data, which is expected to have risen by 191k during December. Technical traders will continue to closely observe how the Dollar Index behaves before and after the ADP report this afternoon. Sustained weakness below 92.00 could open a path lower towards 91.60.

Currency spotlight - GBPUSD

Sterling appreciated against the Dollar on Thursday morning after Britain's service sector grew at a faster rate than expected in December. UK Services PMI increased to 54.2 in December, up from 53.8 in November, fuelling optimism that the UK economy accelerated in the final quarter of 2017.

While the current optimism may spark further upsides for Sterling in the short-term, the currency still remains at the mercy of Brexit developments. With Dollar weakness one of the key players behind the GBPUSD's impressive appreciation, it will be interesting to see how much higher the currency pair trades before bulls lose stamina.

Taking a look at the technical picture, the GBPUSD is bullish on the daily charts with the breakout above 1.3520 opening a path towards 1.3600. A failure of prices to keep above 1.3520 may result in a decline back to 1.3440.

Commodity spotlight - Oil

WTI Oil started the New Year on an incredibly bullish note with the commodity currently hovering around its highest level in two and a half years, in part due to ongoing tensions in Iran.

It seems that the combination of geopolitical risk and optimism over OPEC's supply cut rebalancing the markets, have turned sentiment bullish towards oil. While the current momentum suggests that further upside is on the cards, it must be kept in mind that US Shale remains a threat to higher oil prices.

From a technical standpoint, WTI Crude is approaching the psychological $62.00 resistance level. A decisive breakout above $62.00 has the ability to trigger an incline higher towards $63.80.

Eurozone Data Push Euro and Stocks Higher; ADP Employment Report in Focus

Here are the latest developments in global markets:

FOREX: Upbeat data on December's composite PMI for the Eurozone published on Thursday lifted euro/dollar towards 1.2052 (+0.32%), reversing most of yesterday's losses as the figures suggested a faster Q4 growth for the region. Pound/dollar also gained from better-than-expected survey data, rising to 1.3554 (+0.24%). The dollar, on the other hand, was in the backfoot against six major currencies at 91.95 (-0.23%) unable to gain further from Wednesday's economic numbers and Fed meeting minutes. Dollar/yen was flat at 112.60 and dollar/loonie inched down to 1.2517 (-0.12%). The kiwi was the best performer as stronger global commodity demand and a weaker dollar underpinned the currency, with kiwi/dollar surging to 0.7124 (+0.48%).

STOCKS: European stocks gained momentum after the release of the Eurozone data underlined the economic strength of the block, following their Asian counterparts which reached fresh highs overnight. The benchmark STOXX 600 and the blue chips STOXX 50 were up by 0.50% and 0.44% respectively at 1100 GMT. The German DAX 30 jumped by 0.94% driven by gains in industrial and financial sectors, while the British FTSE 100 touched an all-time high thanks to a rally in oil shares. However, the index latest steadied as losses in retail sectors offset part of the gains. US stock futures were pointing to a positive open.

COMMODITIES: Oil prices were mixed after reaching more than two-year highs earlier on Thursday on the back of anti-government protests in Iran (OPEC's third largest producer). WTI crude increased by 0.21% to $61.76 per barrel but Brent was weaker by 0.16% at $67.75. Gold was trading flat on the day at $1,313.50 per ounce.

Day ahead: ADP nonfarm employment report attracts attention

Traders will keep a close eye on the dollar as several economic releases are expected to move the currency during the European trading hours.

At 1315 GMT, the ADP nonfarm payrolls report which tracks changes in the US private sector employment is expected to show that the number of workers increased by 190,000 in December, as in November. The report is considered as a good predictor of the all-important nonfarm payrolls due on Friday which indicates employment trends in both the private and public sectors. A few minutes later, the US Department of Labor will publish figures on initial jobless claims for the week ending December 29.

Meanwhile in Canada, producer prices are anticipated to rise by 0.8% m/m in November after touching the highest growth in a year of 1.0% in the previous month.

In terms of public appearances, St. Louis Fed President, James Bullard (a non-voting FOMC member) is scheduled to give a presentation on the US economy and monetary policy at 1830 GMT.

At 1600 GMT, the EIA report which measures weekly changes in US oil inventories is projected to bring some volatility to oil prices. Forecasts are for crude oil inventories to fall by a larger amount of 5.148 million barrels compared to a reduction of 4.609 million barrels in the preceding week. That would be the seventh week of declines for the US crude stocks.

New Highs Eyed Ahead of US Data

- US Indices Target More Record Highs on the Open;

- USD Under Pressure Again After Dead Cat Bounce;

- EUR and GBP Buoyed By PMI Data.

US equity markets are currently on course to open at record highs again on Thursday, continuing the positive start to the year and coming on the back of strong gains in Asia and Europe.

With tax reform now over the line, attention will likely turn to earnings season as companies start reporting on the fourth quarter over the next week. Investors appear quite optimistic about earnings after another strong showing in the third quarter and will likely be keen to know what impact the new tax reform measures will have on the bottom line. Prior to this, we have plenty of economic data to focus on with ADP non-farm employment data, services PMI, jobless claims and crude inventories all due today, ahead of tomorrow's December jobs report.

The US dollar is once again coming under pressure on Thursday following its brief recovery a day earlier, with the FOMC minutes providing an additional short-lived boost before the decline resumed. The minutes themselves in reality provided little new insight, with the acknowledgement that tax reform could provide an economic boost which contributed to raised forecasts, likely spurring the move higher in the dollar though.

Overall the minutes appeared quite neutral which may explain why the dollar is struggling to hold onto yesterday's gains. With the composition of the FOMC changing over the coming months, it's difficult to take too much of value away from the minutes. Particularly when members acknowledge that the economic benefit of the tax cuts is unknown, with a number of people outside the central bank arguing that it will be small and short-lived.

A slight improvement in PMIs across the eurozone and the UK this morning has also boosted the euro and pound, respectively, a little which is also likely weighing on the dollar. The eurozone composite PMI rose to 58.1, above expectations, signalling another quarter of strong growth for the region and good momentum heading into 2018. This was helped by a similar beat in the German composite PMI, which rose to 58.9, offsetting a slight decline in France, although across the board the numbers are very encouraging.

The PMI numbers coming from the UK this week have been a little weaker but the services sector did not disappoint which has given a leg up to the pound. The services sector - which is by far the biggest and most important, making up more than three quarters of the economy - saw a slight uptick in the PMI to 54.2 in December, which is still well below pre-Brexit referendum levels but comfortably in growth territory.

NZDUSD Stalls Recent Rally And Consolidates Around 0.71 Level, Short-Term Outlook Remains Bullish

NZDUSD stalled its recent rally and is hovering around the key 0.7100 level. The short-term outlook remains bullish. On the 4-hour chart, the 50 and 200-period moving averages are positively aligned and RSI is above 50.

While NZDUSD consolidates, immediate support is expected to be provided around the 0.7080 area. As long as this support holds, risk remains to the upside. But a break below the consolidation range would shift the bias to bearish and another leg lower would target the 0.7020 area which saw some congestion in the past and acted both as a support and resistance zone. A drop lower might imply the market is set to fall further to target 0.6900.

The short-term technical setup is still bullish and a sustained break above the January 2 peak of 0.7130 would confirm the start of another bullish phase, extending the recent uptrend. From here the market has scope to target 0.7200. But the longer time the pair trades sideways, the more the upside momentum will fade, risking more weakness in the market.

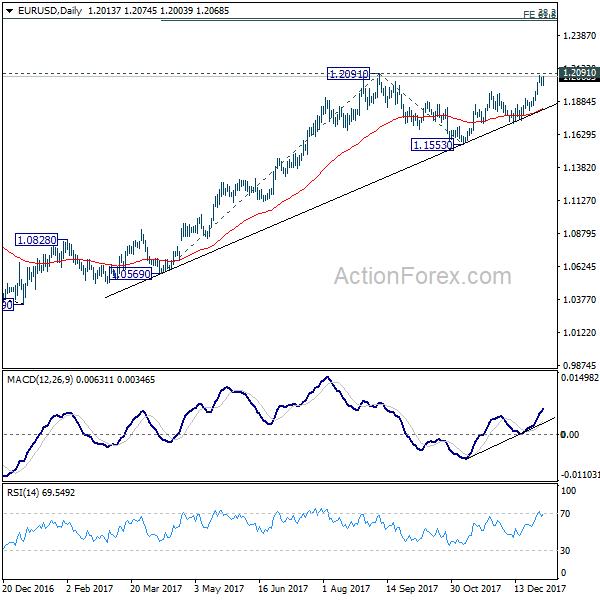

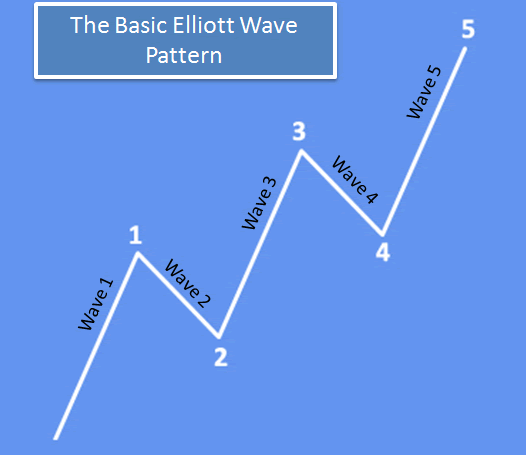

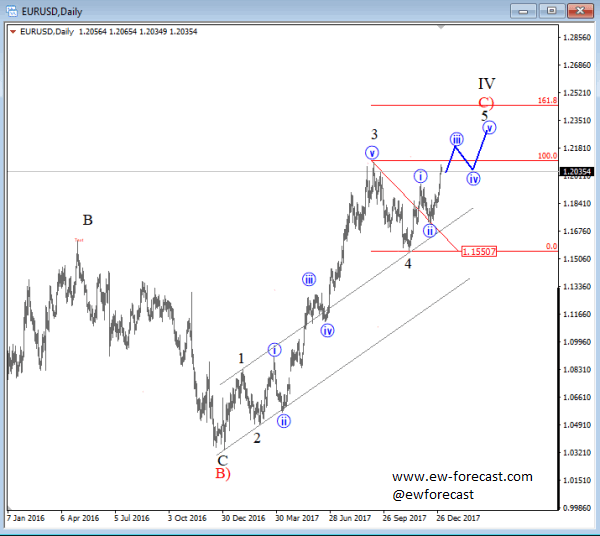

Elliott Wave Analysis: EURUSD Trading In A Bullish Impulse

On the mid-term time frame of EURUSD we see price rising for some time now and unfolding a bullish impulsive movement. Particularley we see price picking up from the low, away from end of Decemeber of 2016 and unfolding a five-wave bullish development with final black wave 5 leading the way. As you know an impulse in Elliott wave theory is a five-wave pattern, that moves in the direction of the trend, it is also quite sharp and has a clear structure with no significant overlaps between the waves.

Below we have an image of an impulse:

(There are no overlaps between the waves( only overlap that usually occures is between waves 1 and 4, but this happens in an Elliott wave ending diagonal)

Now if we add this look to the EURUSD, we can see that price may be trading within its final wave 5, as labeled on the chart. Well this wave 5 is also an impulse and may also unfold five minor waves within itself. At the moment we see only three waves unfolded, meaning more upside can still follow on the EURUSD, before a significant top, ideally at around 1.2400 may be locked in and then a change in trend from bearish to bullish can follow.

EURUSD, Daily

Once the top is locekd in, we would look for a minimum three wave reversal. A confirmation for a bearish reversal would later be a new minor five-wave drop from the high, and a break below the former swing low of 4 at 1.1551 level.

Market Update – European Session: European Zone PMI Services Data Shows Region Ended 2017 On A Strong Note

Notes/Observations

German pre-coalition talks between the CDU/CSU and the SPD turning out surprisingly promising

FOMC Minutes reinforce that was on course for its moderate course in pushing rates up

German and Euro Zone PMI Services confirm multi-year high readings

US East Coast weather prompts 2-hours opening delay in DC; thus no lock-up for economic releases

Asia:

Japan Dec Final PMI Manufacturing: 54.0 v 54.2 prelim (highest level since Feb 2014)

BOJ's Kuroda repeats vow to maintain ultra-easy policy

South Korea military: No imminent missile launch seen from North Korea

South Korea Fin Min Kim and BOK Gov Lee agree to closely monitor risk factors and take swift measures if needed

China Dec Caixin PMI Services registered its fastest rise since Aug 2014 (53.9 v 51.9 prior); PMI Composite: 53.0 v 51.6 prior

Europe:

German chancellor Merkel's conservatives and Social Democrats agree to hold exploratory talks on possible government from Jan 7th; parties say confidence has risen, are optimistic after discussions between parties' leaders

Americas:

FOMC Dec Minutes: Officials saw modest boost from tax reform; Generally agreed flatness of yield curve not unusual by historical standards; some expressed concern a possible future inversion could portend economic slowdown; Several Fed officials concerned by low inflation expectations

Energy:

Weekly API Oil Inventories: Crude: -5M v -6M prior

Economic Data:

(IN) India Dec PMI Services: 50.9 v 48.5 prior (moved back into expansion); PMI Composite: 53.0 v 50.3 prior

(IE) Ireland Dec Services PMI: 60.4 v 56.0 prior; Composite PMI: 60.2 v 57.7 prior

(UK) Dec Nationwide House Prices M/M: 0.6% v 0.1%e; Y/Y: 2.6% v 2.0%e

(ZA) South Africa Dec PMI (Whole economy): 48.4 v 48.8 prior

(SE) Sweden Dec PMI Services: 64.6 v 61.9 prior

(HU) Hungary Nov Unemployment Rate: 3.8% v 4.0%e

(ES) Spain Dec Services PMI: 54.6 v 54.6e (50th month of expansion); Composite PMI: 55.4e

(IT) Italy Dec Services PMI: 55.4 v 54.7e (19th month of expansion and the highest since July); Composite PMI: 56.5 v 56.0e

(NG) Nigeria Dec PMI: 56.8 v 55.2 prior

(FR) France Dec Final Services PMI: 59.1 v 59.4e (confirmed 18th month of expansion); Composite PMI: 59.6 v 60.0e

(DE) Germany Dec Final Services PMI: # v 55.8e (confirmed 54th month of expansion and highest since Dec 2015); Composite PMI: 58.9 v 58.7e

(EU) Euro Zone Dec Final Services PMI: 56.6 v 56.5e (confirmed 54th month of expansion and highest since Apr 2011); Composite PMI: 58.1 v 58.0e

(UK) Dec Services PMI: 54.2 v 54.0e (17th month of expansion); Composite PMI: 54.9 v 55.0e

(UK) Nov Net Consumer Credit: £1.4B v £1.5B; Net Lending: £3.5B v £3.4Be

(UK) Nov Mortgage Approvals: 65.1 K v 64.0Ke

(UK) Nov M4 Money Supply M/M: 0.1 v 0.6% prior; Y/Y: 3.7 v 4.1% prior; M4 Ex IOFCs 3M Annualized: 3.4% v 5.4% prior

Fixed Income Issuance:

(SI) Slovenia opened its books to sell EUR-denominated 10-year note; guidance seen +17bps to mid-swaps

(ES) Spain Debt Agency (Tesoro) sold total €3.84B vs. €3.0-4.0B indicated range in 2022, 2027 and 2046 bonds

Sold €960M in 0.45% Oct 2022 SPGB; Avg yield: 0.356% v 0.290% prior, Bid-to-cover: 2.5x v 1.87x prior

Sold €1.836BB in 1.45% Oct 2027 SPGB; Avg yield: 1.525% v 1.488% prior; Bid-to-cover: 1.8x v 1.95x prior

Sold €1.04Bin 2.90% Oct 2046 SPGB; Avg Yield: 2.836% v 2.874% prior; Bid-to-cover: 2.1x v 1.55x prior

(ES) Spain Debt Agency (Tesoro) sold €800M vs. €0.5-1.0B indicated range in 1.00% inflation-linked 2030 bonds; Real Yield:0.479 % v 0.858% prior; Bid-to-cover: 1.9x v 1.3x prior

(FR) France Debt Agency (AFT) sold total €8.11B vs. €8.0-9.0B indicated range in 2028, 2036 and 2048 Oats

Sold €5.211B in 0.75% May 2028 Oat; Avg Yield: 0.79% v 0.76% prior; Bid-to-cover: 1.44x v 1.57x prior

Sold €1.335B in 1.25% May 2036 Oat; Avg Yield 1.35% v 1.38% prior; Bid-to-cover: 1.90x v 1.76x prior

Sold €1.565B in 2.00% May 2048 Oat; Avg Yield: 1.75% v 1.74% prior, Bid-to-cover 2.00x v 1.42x prior

SPEAKERS/FIXED INCOME/FX/COMMODITIES/ERRATUM

Equities

Indices [Stoxx600 +0.5% at 392.0 , FTSE +0.1% at 7680 , DAX +1.0% at 13110, CAC-40 +1.0% at 5376 , IBEX-35 +1.0% at 10220, FTSE MIB 1.3% at 22188 , SMI -0.1% at 9471, S&P 500 Futures +0.2%]

Market Focal Points/Key Themes: European Indices trade higher once again continuing the positive momentum seen in 2018 following on from another record close in the US as well as a 25 year high in Japan. Both the Dax and CAC trade higher by ~1% while the FTSE under performs with Debenhams a notable decliner after its Christmas trading update which saw UK LFL sales fall 2.6%. The stabilizing Euro has helped mainland Europe Indices with European Auto names advancing following US Dec sales figures reported yesterday, with a big move in Fiat, which has hit an all time high helping the FTSE MIB outperform. In the US Costco once again posted strong Dec SSS of 8.8% helping lift shares in the post market. Looking ahead notable US earners include WBA, Monsanto and RPM.

Movers

Consumer Discretionary [Debenhams [DEB.UK] -18% (Christmas trading update), Whitbread [WTB.UK] +1% (Chairman retires)

Industrials [Michelin [ML.FR] +1% {JV with Sumitomo in NA)]

Healthcare [Vectura [VEC.UK] -3.5% (Trading update), Pixium Vision [PIX.FR] +7.9% (Receives FDA approval to begin human clinical study of its PRIMA sub-retinal implant in the US), Pixium Vision [PIX.FR] +7.9% (Receives FDA approval to begin human clinical study of its PRIMA sub-retinal implant in the US)]

Technology [Sopheon [SPE.UK] +24% (Trading update)

Energy [PGS [PGS.NO] +17% (Prelim Q4)]

Speakers

ECB's Smets (Belgium) CPI seen rising to 1.7% by 2020 (in-line with staff forecasts)

China said to send an envoy (to discuss North Korea) to South Korea between Jan 5th- 6th

Currencies

USD could hardly muster any support in the aftermath of Wed's release of FOMC Dec Minute despite that officials expressed growing confidence in the strength of the labor market and the economy

EUR/USD holding above the 1.20 level as German pre-coalition talks between the CDU/CSU and the SPD was turning out surprisingly promising. The economic data out of Europe also continued to confirm the ECB belief that the region's recovery was robust and broad-based as German and Euro Zone PMI Services confirmed multi-year high readings

GBP/USD continued to find resistance at the 1.36 area but was higher by 0.2% just ahead of the NY morning at 1.3545

USD/ZAR was at 2-year lows below 12.25 level aided by reports that South Africa Ruling ANC party was said to consider removing Zuma

Fixed Income

Bund Futures trade down 19 ticks at 161.36 as momentum fades and nears the 200-DMA. A continued move below 161.00 low targets 160.71 then 160.45, with a continued rebound targeting 161.86.

Gilt futures trade at 124.57 down 31 ticks off the session lows. Continued upside eyeing 124.75 then 125.25. Downside targets include 123.25 then 122.75.

Thursday's liquidity report showed Wednesday's excess liquidity rose to €1.823T from €1.789T prior. Use of the marginal lending facility fell to €53M from €317M prior.

Corporate issuance is taking off as the new year begins .

Looking Ahead

05:30 (PL) Poland to sell PLN3.0-5.0B in Bonds

06:00 (BR) Brazil Nov PPI Manufacturing M/M: No est v 1.5% prior; Y/Y: No est v 3.5% prior

06:00 (ZA) South Africa Nov Electricity Production Y/Y: No est v 1.3% prior; Electricity Consumption Y/Y: No est v 0.0% prior

06:00 (CZ) Czech Republic to sell bills - 06:45 (US) Daily Libor Fixing

07:00 (BR) Brazil Dec PMI Services: No est v 46.9 prior; PMI Composite: No est v 48.9 prior

07:30 (US) Dec Challenger Job Cuts Y/Y: No est v 30.1% prior

08:00 (RU) Russia Gold and Forex Reserve w/d Dec 29th: No est v $432.0B prior

08:05 (UK) Baltic Dry Bulk Index

08:15 (US) Dec ADP Employment Change: +190Ke v +190K prior

08:30 (US) Initial Jobless Claims: 241Ke v 245K prior; Continuing Claims: 1.93Me v 1.943M prior

08:30 (CA) Canada Nov Industrial Product Price M/M: 1.0%e v 1.0% prior; Raw Materials Price Index M/M: No est v 3.8% prior

09:45 (US) Dec Final Markit Services PMI: 52.5e v 52.4 prelim; Composite PMI: 53.0e v 53.0 prelim

10:30 (US) Weekly EIA Natural Gas Inventories

11:00 (US) Weekly DOE Crude Oil Inventories

13:30 (US) Fed's Bullard (non-voter, Dove)

Technical Outlook: WTI Oil Hit New 2 ½ Year High But Correction Signals Require Caution

WTI oil hit new high at $62.19 on Thursday (the highest since mid-May 2015) in extension of Wednesday's strong rally. Oil prices remain supported by OPEC-led production cut, with additional boost coming from recent tensions in Iran, one of key world oil producers. In addition, repeated draws in US oil stocks which brings inventories close to five-year average and freezing weather in the US and Canada which increased demand for oil products, keep oil prices supported. US API crude inventories report was released on Wednesday, showing a draw of nearly five million barrels, with EIA report due later today, being in focus (5.14 million barrels draw f/c vs -4.60 million barrels previous week). Oil price is holding with narrow range under new high on Thursday and looking for attack at key barrier at $62.71 (13 May 2015 high), break of which could spark fresh acceleration towards $66.72 (50% retracement of $107.40/$26.04 descend). Technical studies are in firm bullish setup and supportive for further advance, however, corrective action could be anticipated, as overbought conditions on daily and weekly charts warn of correction.

Res: 62.19, 62.71, 63.00, 63.50

Sup: 61.74, 61.24, 61.00, 60.28

Nonfarm Payroll Report: American Wage Growth Of Most Interest

The chief economist at Moody's Analytics Mark Zandi said that 'it is a good time to be an American worker' given that the economy has been creating two million jobs each year for the last six years. The US labor market remained resilient, with the unemployment rate falling to multi-year lows in 2017, even after devastating hurricanes slammed Texas and Florida, leading to a period of weaker hiring. However, employment numbers are not what analysts are paying most attention to but instead wage inflation is of greater concern as growth in average earnings remains subdued in an already tight labor environment. Hence, wage growth figures on Friday's nonfarm payrolls report would be of greater importance to the markets and may prove to be a source of volatility for the dollar.

According to forecasts, the government's NFP report due on Friday at 1330 GMT is expected to show that the number of job positions created in December increased by 188,000 compared to 228,000 seen in the month before. Regarding the unemployment rate, this is estimated to remain flat for the second consecutive month at a 17-year low of 4.1%, while the average hourly earnings are projected to inch up by 0.1 percentage points to 0.3% m/m. The latter could be a sign that a stronger labor market has started pushing wage growth to the upside, but looking at historical data someone could say that there is still great room for improvement. On a yearly basis, average hourly earnings rose by 2.5% in November and are projected to maintain this pace of growth in December, though at the current unemployment rate levels the annual expansion rate should have stood at least at 3.5% according to some analysts, a rate last seen before the financial crisis.

Rising wages would also be good news to the Fed's ears as policymakers wait for higher wage growth to push up inflation and therefore convince the central bank that remaining on a path of policy normalization is the right thing to do. Nevertheless, the Fed plans to get more aggressive in the upcoming years despite lackluster inflation as the 'economic expansion is increasingly broad-based across sectors' according to the Fed chair, Janet Yellen, and is the fastest over the last three years (Yellen is to be replaced by Jerome Powell in February). Currently, the FOMC predicts three rate hikes in 2018, while markets are currently pricing in two rate rises for the aforementioned period according to Fed fund rate futures prices; December's Fed fund futures are currently suggesting that short-term interest rates will climb towards 1.92% at the end of this year.

The easiest way to explain the weak momentum in wage growth is the aging population which potentially restricts the labor force participation rate from rising as older workers are less likely to participate in the workforce. Besides that, not only has the life expectancy increased but older adults are working longer, reducing human capital in the market. Turning back to previous economic recoveries, the share of people aged at least 55 was around 12-15% of household survey employment but in 2016 this percentage jumped to a record of 23%.

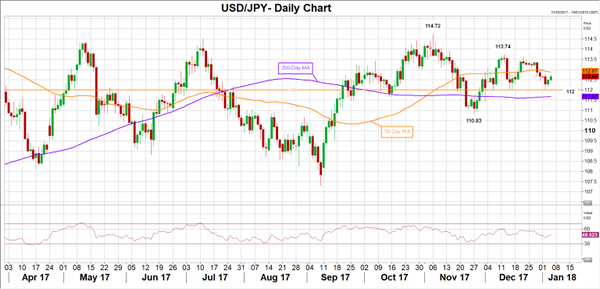

For now, though, hopes are for the labor market to continue strengthening, supporting households' pockets. In case the NFP report reveals better-than-expected readings, the dollar/yen could surpass the 50-day moving average at 112.87 and break back above the 113 key-level. However, only a break above the previous top of 113.74 is expected to more conclusively turn the bias from neutral to bullish. From here, the next target could be the nine-month high at 114.72.

On the flip side, discouraging numbers would likely pressure the pair, pushing it down to the 112 handle, while steeper decreases would bring the previous low at 110.83 into view.

OPEC Maintains Production | No Love For The Dollar | UK Data Under Focus

Chinese services data shows strength

FOMC shows gradual rate hike

OPEC maintains its production

Brexit and the banking sector is the key point

Broadly speaking it appears that the next move for the equity markets is still to the upside. Global equity markets have started the year on the front foot, and the US markets are printing “another record high” headlines. European and US futures are trading higher encouraged by the strong Chinese economic data reading. The gauge of services industries confirmed that the growth is robust and this has been enough for traders to push the Asian markets higher.

The dollar index failed to gain any momentum, as the FOMC minutes confirmed that the Fed is in no rush in adopting any aggressive methods with respect to their interest rate hike. Gradual interest hike was the primary message for the markets from the FOMC minutes yesterday and this made investors to push the treasury yields higher

From the minutes, it is evidently clear that the Fed is finding solidarity within the tax cuts, as it would comfort their inflation concerns but also support the growth equation too. Perhaps, it is the fiscal policies that would be able to fill the gap. Also Flattening yield is keeping many awake during the night, but this is untrue for the Fed, as minutes were released yesterday confirming the unified message “flattening yield is no longer an indication for any signs to worry”.

The banking industry is literally the heartbeat of London and London is the heart of the UK. If Theresa May does not create a good deal for the banking sector that helps banks to run efficiently, the chances of London remaining as the centre of attention will diminish further and it would also create more pain for the UK economy.

The ongoing game of bluff which Michael Barnier is playing (which says there will be no special deal for financial services) is not the way to kick start the negotiation process for the post Brexit ties with the European Union. Traders will be keeping a close eye on this development, and on the upcoming services and composite data. We expect these numbers to show some encouraging signals with the reading of 54 and 55 respectively.

While the protesting situation in Iran continues to accelerate, the latest figures are showing OPEC has kept its production steady at 32.47 million barrels a day. Lower Libyan oil production opened the room for Nigeria to fulfil the gap. The most important point to seize from this is the OPEC production number, the cartel has sent a strong signal to the oil market that they are committed to their production cut, and they are kick-starting the near year when the compliance sits at 121% which was at the same level as November. For brent, the near terms support is at 63.80 and the resistance is at 70.03.