Sample Category Title

Technical Outlook: GBPUSD – Bid Tone Above 1.3500, UK Data In Focus

Cable ticked higher in early European trading on Thursday after holding within tight range in Asia.

Wednesday's strong close in red after four consecutive bullish days was negative signal, but dips were so far limited at 1.3493 (Fibo 38.2% of 1.3301/1.3612 upleg) which marks pivotal support.

North-heading daily MA's maintain bullish structure and offset negative signals from descending momentum and slow stochastic.

Renewed attempts above 1.3600 barrier could be expected while 1.3493 support holds, however, the pair may stay in extended consolidation before bulls resume.

Retest of Wednesday's high at 1.3612 would open way towards key barrier at 1.3655 (2017 high).

Alternatively, deeper correction could be anticipated on break below 1.3493 pivot, with extended dips to focus daily Tenkan-sen (1.3472) and rising 10SMA (1.3447). Release of UK Service PMI for December is in focus, with fresh bullish acceleration expected on better than expected figure.

Res: 1.3549, 1.3600, 1.3612, 1.3655

Sup: 1.3505, 1.3493, 1.3472, 1.3447

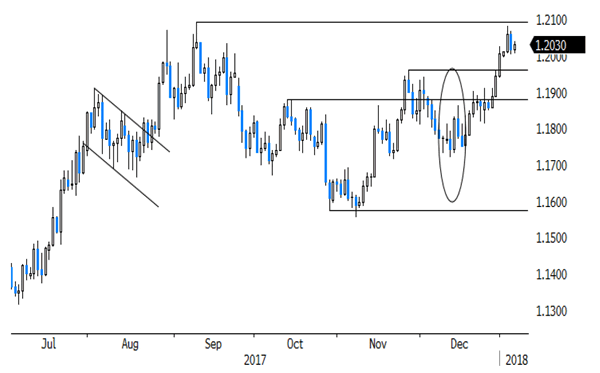

Technical Outlook: EURUSD Trades In Extended Consolidation Above 1.2000 But Deeper Pullback Not Ruled Out

The Euro holds positive sentiment and bounced to 1.2038 on Thursday, after limited impact from encouraging Fed minutes, released late Wednesday.

Fed policymakers backed continued gradual rate hikes, in expectations for faster inflation from tax cut. However, concerns of failure of inflation to reach 2% projection exist and may slow rate hike process.

Initial support at 1.2000 holds for the third day, after Wednesday's close in red, keeping immediate focus at the upside, as underlying bull-trend remains intact. However, deeper correction cannot be ruled out as slow stochastic is reversing from overbought territory.

Break below 1.2000 handle would expose next strong supports at 1.1961/50 (former top of 27 Nov/Fibo 38.2% of 1.1737/1.2081 upleg, reinforced by rising 10SMA) which is expected to hold extended dips.

Friday's releases from EU (CPI) and US (NFP) are in near-term focus for fresh signals.

Res: 1.2038, 1.2066, 1.2092, 1.2166

Sup: 1.2000, 1.1961, 1.1950, 1.1900

Greenback Regains Some Composure While US Stock Indices Close At Records, US ADP Employment Due

Here are the latest developments in global markets:

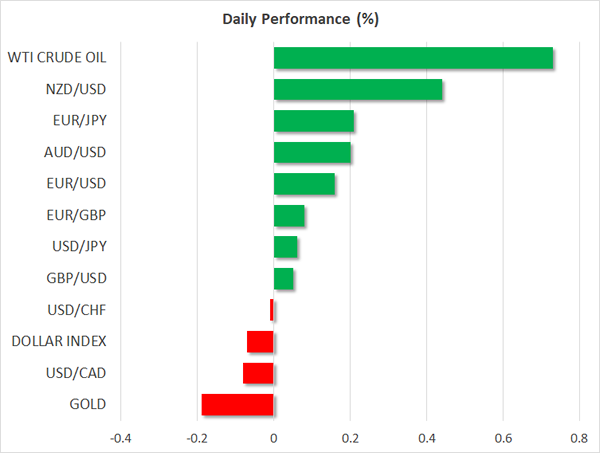

FOREX: The US dollar traded 0.1% lower against a basket of major currencies during the Asian trading session Thursday, after posting gains on Wednesday.

STOCKS: All three major US equity indices (Dow Jones, S&P 500, Nasdaq Composite) closed at fresh record highs yesterday, buoyed by optimism around the US economy following strong data releases and a cheerful tone in the FOMC minutes. Futures tracking the Dow, S&P and Nasdaq 100 are currently in the green as well. In Asia, Hong Kong’s Hang Seng was up 0.5%, while Japan’s Nikkei 225 and Topix indices finished higher by 3.2% and 2.6% respectively, both closing at multi-decade high levels.

COMMODITIES: Gold fell, trading 0.2% lower as the Asian session was coming to a halt, after trading lower yesterday as well. Meanwhile, WTI and Brent crude oil were up 0.7% and 0.5% respectively, as the continued political instability in Iran lead to concerns that the nation’s oil production may be disrupted in the future.

Major movers: Dollar recovers as FOMC minutes reaffirm steady path; gold declines

The US dollar regained some of its lost glamour on Wednesday, after the ISM manufacturing PMI for December surprisingly rose, beating expectations that projected it to tick down, and indicating that the sector finished 2017 on a very strong footing. The greenback recovered further a few hours later, after the FOMC minutes from the December meeting reaffirmed the central bank remains committed to continue its normalization cycle in 2018, even despite below-target inflation.

The only worried remarks came from a “couple of participants”, which were probably Neel Kashkari and Charles Evans, both of which dissented from the decision to raise rates. The absence of any other signals suggesting that we could see a pause in rate hikes next year if inflation continues to undershoot likely came as a relief to dollar bulls. Gold traded lower after the minutes, possibly due to the gains in the US currency, as gold is denominated in dollars.

However, the dollar did not hold on to its gains, trading slightly lower during the Asian session Thursday. Euro/dollar was up nearly 0.2%, while sterling/dollar was marginally higher as well. The commodity-linked currencies outperformed the greenback once again with kiwi/dollar leading the charge, trading 0.4% higher. Meanwhile, aussie/dollar was up 0.2%.

Day ahead: ADP jobs data out of the US and UK services PMI on the agenda

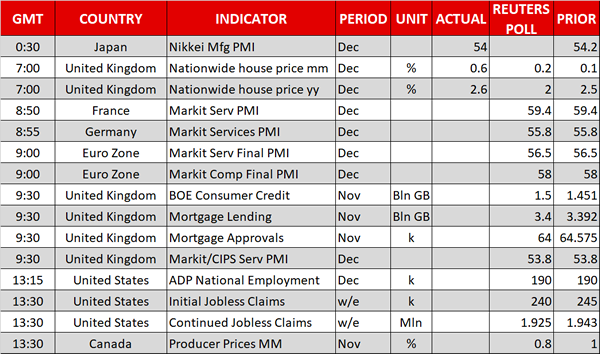

The eurozone will see the release of the readings on December services PMI as well as composite PMI – the measure that blends the manufacturing & services sectors – at 0900 GMT. However, the data will pertain to the final release and are unlikely to spur much positioning by markets. A little before that, Germany and France, the eurozone’s two largest economies, will see the release of their respective readings.

Earlier in the week, the UK was on the receiving end of weaker than expected manufacturing and construction PMIs. The December reading for the all-important for the UK economy services sector is due today at 0930 GMT. Further disappointment is anticipated to push sterling lower. Data on UK consumer credit and mortgage lending/approvals are scheduled for release at the same time.

In the US and having the capacity to spur dollar positioning is the December ADP report on positions added to the economy by the private sector. The release is viewed by some analysts as a preview to the much-awaited nonfarm payrolls report which includes data on both the private and public sector and is due on Friday. The ADP national employment report will go public at 1315 GMT and is projecting the addition of 190k private positions to the economy, the same number as in November. A little after (at 1330 GMT) weekly data on US initial and continued jobless claims will be released.

Data on Canadian producer prices for the month of November are due at 1330 GMT.

St. Louis Fed President James Bullard (a non-voting FOMC member) is scheduled to give a presentation on the US economy and monetary policy at 1830 GMT.

The EIA weekly report, that includes information on US crude oil and gasoline inventories, will be made public at 1600 GMT. Crude stockpiles are expected to decline by around 5.1 million barrels in the week that preceded. The report tends to cause volatility in oil prices.

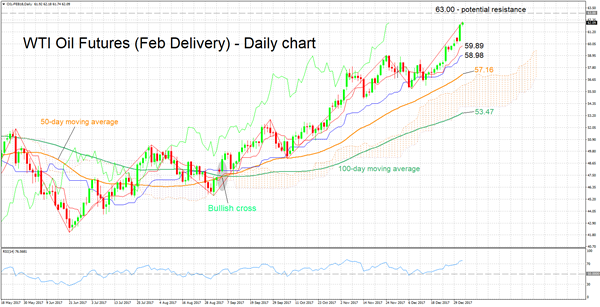

Technical Analysis: WTI oil futures hit fresh 2½-year high; bullish in short-term though RSI overbought

WTI oil futures for February delivery recorded a fresh 2½-year high of 62.18 during today’s trading.

The Tenkan-sen line being above the Kijun-sen line is a positive alignment pointing to bullish momentum in the short-term. The RSI is supporting this view as it continues rising, though notice that it has crossed into overbought territory above 70.

A bigger-than-anticipated drawdown in crude stockpiles out of today’s EIA report could lend further support to prices. In such an event, the area around the 63.00 handle could act as a barrier to the upside. This is a potential psychological level that has also served as a peak back in mid-2015 (as well as an area of congestion).

On the contrary, a smaller-than-projected drawdown could weaken prices. In this case, the range around the Kijun-sen at 59.89 might provide support. The area around this level encapsulates a peak from the recent past, as well as the 60.00 mark, another potential psychological level.

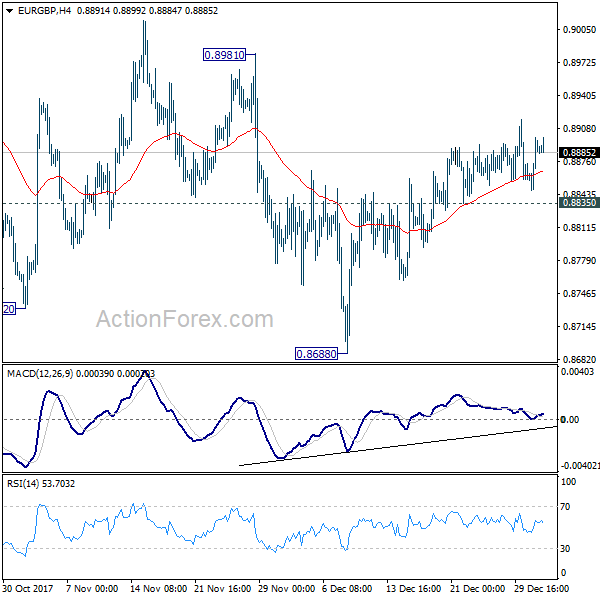

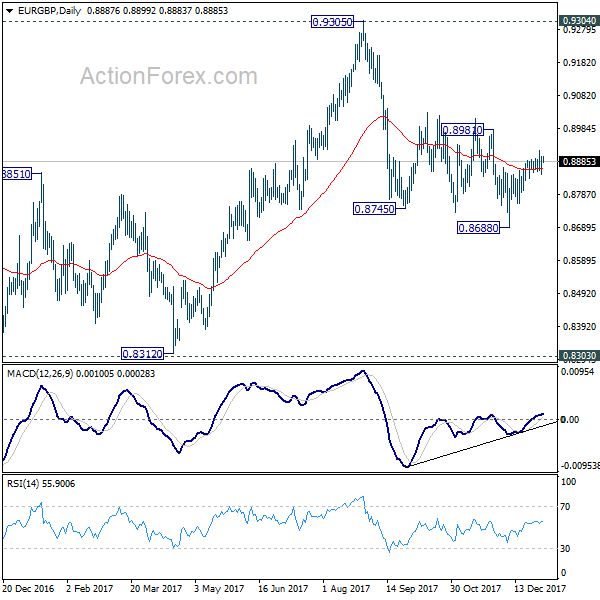

EUR/GBP Daily Outlook

Daily Pivots: (S1) 0.8857; (P) 0.8878; (R1) 0.8908; More...

Further rise is still mildly in favor in EUR/GBP for 0.8981 resistance. Sustained break there will indicate that whole decline from 0.9305 has completed. In such case, EUR/GBP will target a test on 0.9304/5 key resistance. On the downside, below 0.8835 minor support will turn bias back to the downside for 0.8668 instead.

In the bigger picture, there are various ways to interpret price actions from 0.9304 high. But after all, firm break of 0.9304/5 is needed to confirm up trend resumption. Otherwise, range trading will continue with risk of deeper fall. And in that case, EUR/GBP could have a retest on 0.8303. But we'd expect strong support from 0.8116 cluster support (50% retracement of 0.6935 to 0.9304 at 0.8120) to contain downside.

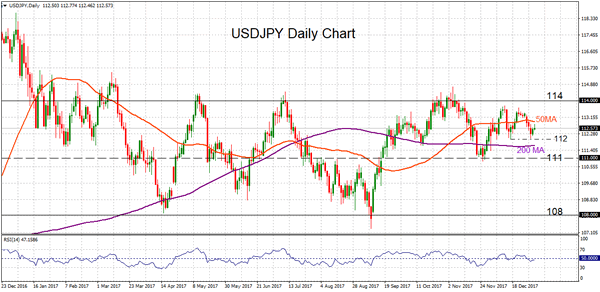

USDJPY Maintains Neutral Bias, Pivoting 50-Day Moving Average

USDJPY has been neutral both in the short and medium term. Since late September the pair has been trading in the upper half of the 9-month range between 111 and 114. The market does not have any clear direction and this lack of trend is indicated by the horizontal 50-day and 200-day moving averages.

Near-term risk has moved to the downside after prices fell back below the 50-day MA earlier this week. However, further downside may be limited as long as support is being provided by the 200-day MA at 111.65. Below this, the 111 level is expected to provide support as well.

A daily close below 111 would suggest the start of a bearish phase to target the bottom of the medium-term range at 108. This scenario seems unlikely if USDJPY can move and stay above 112 in the next few sessions.

The market needs to cross back above the 50-day MA to find momentum to target the top of the range at 114. In the meantime, the neutral bias is expected to remain in the near term.

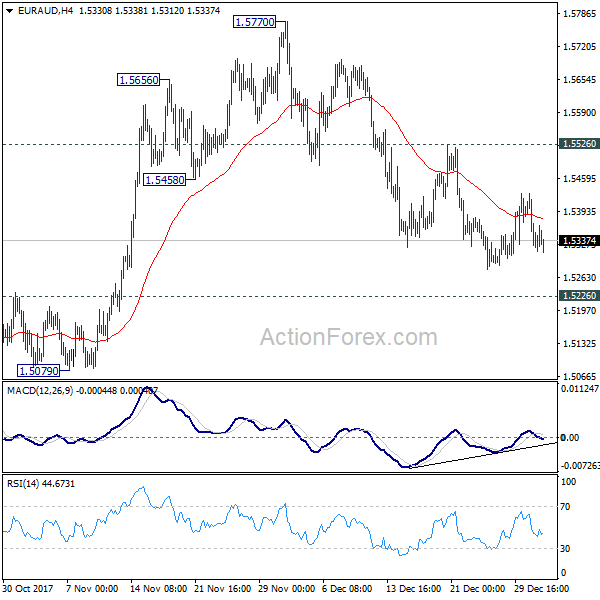

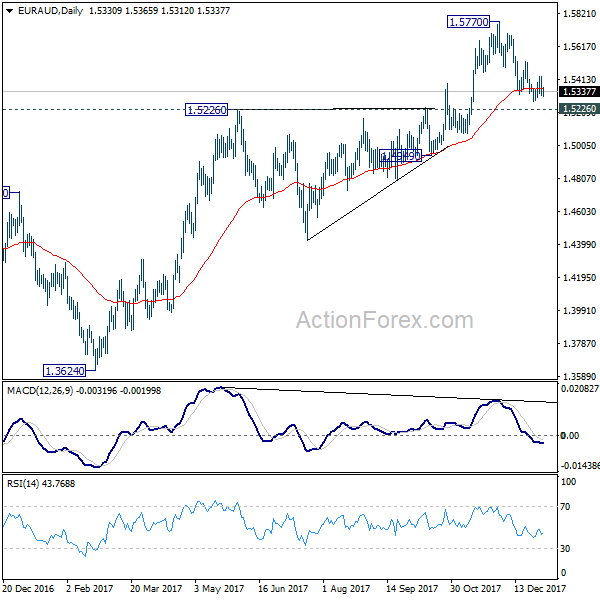

EUR/AUD Daily Outlook

Daily Pivots: (S1) 1.5289; (P) 1.5360; (R1) 1.5403; More....

Intraday bias in EUR/AUD stays neutral for the moment and outlook is unchanged. The correction from 1.5570 could still extend lower. But again, near term outlook stays bullish with 1.5226 resistance turned support intact. Break of 1.5526 minor resistance will turn bias back to the upside for retesting 1.5770 resistance. However, sustained break of 1.5226 will indicate larger reversal and target 1.4949 support next.

In the bigger picture, we're holding on to the view that corrective decline from 1.6587 medium term top (2015 high) has completed at 1.3624. Rise from 1.3624 is expected to extend to retest 1.6587. We'll hold on to this bullish view as long as 1.5226 resistance turned support holds. Firm break of 1.6587 will resume long term rise from 1.1602 (2012 low). However, sustained break of 1.5226 will indicate trend reversal and target 1.3624 again.

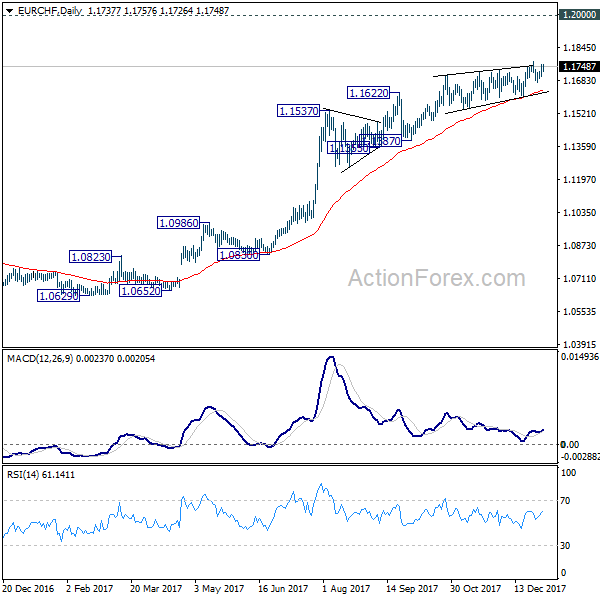

EUR/CHF Daily Outlook

Daily Pivots: (S1) 1.1701; (P) 1.1732; (R1) 1.1763; More...

EUR/CHF recovers further today but it's limited below 1.1776 so far. Intraday bias remains neutral for the moment. While there is no confirmation yet, we'd maintain that the cross is close to topping. And in case of another rise, strong resistance should be seen well below 1.2 handle to bring medium term reversal. On the downside, break of 1.1602 support will indicate reversal and turn outlook bearish for 1.1387 and below.

In the bigger picture, while a medium term top could be around the corner, there is no change in the larger outlook. That is, long term rise from SNB spike low back in 2015 is still in progress and would extend. As long as 1.1198 resistance turned support holds, we'll hold on to this bullish view and expect another to prior SNB imposed floor at 1.2000. Though, we'll reassess the outlook if 1.1198 is firmly taken out.

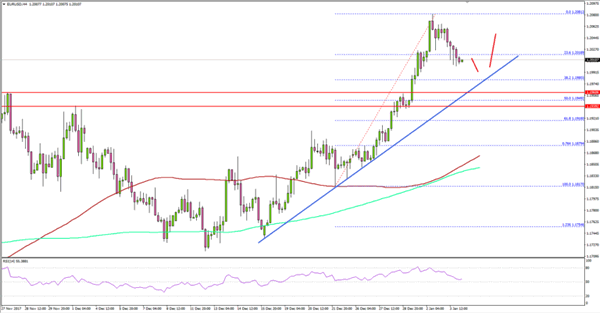

EUR/USD Starts 2018 With Lot Of Strength

Key Highlights

- The Euro surged higher recently and succeeded in breaking the 1.2000 handle against the US Dollar.

- There is a crucial bullish trend line forming with support at 1.1980 on the 4-hours chart of EUR/USD.

- The recent high at 1.2080 is a short-term resistance followed by 1.2100.

- The US ISM Manufacturing Index increased in Dec 2017 to 59.7 from the previous 58.2.

EURUSD Technical Analysis

The New Year started with a bang for the Euro as it climbed above the 1.2000 handle against the US Dollar. The EUR/USD pair is now in a major uptrend above 1.1900 and 1.1940.

While analyzing the 4-hours chart, it is quite clear that the pair started a major uptrend from mid December 2017. It succeeded in trading above the 1.1800 and 1.1880 resistance levels, which cleared the path for more upsides toward 1.2000.

EUR/USD was successful in closing above the 100 (red) and 200 (green) simple moving averages, and broke the 1.2000 handle.

A new high for 2018 was formed at 1.2081 from where a minor correction wave was initiated. It broke the 23.6% Fib retracement level of the last wave from the 1.1817 low to 1.2081 high.

On the downside, there is a crucial bullish trend line forming with support at 1.1980 on the same chart. Should the pair continue to correct lower, it will most likely find bids around the 1.1980 level.

The stated 1.1980 support is also the 38.2% Fib retracement level of the last wave from the 1.1817 low to 1.2081 high. Therefore, a break below 1.1980 won’t be easy. On the upside, the pair faces a short-term resistance at 1.2080. Above 1.2080, the Euro is likely to accelerate gains above the 1.2100 level.

Recently, the US saw December’s Institute for Supply Management (ISM) Manufacturing Index. It posted an increase from 58.2 to 59.7, which was better than the forecast of 58.1.

As a result, the EUR/USD pair might correct a few more pips in the near term, but it remains well supported above the 1.1980 and 1.1940 levels.

Forex: FOMC Backs Gradual Rate Hikes

Federal Open Market Committee Meeting Minutes were released on Wednesday. Most Fed officials agreed to continue with gradual rate hikes. They highlighted the expected increase in the pace of inflation as one of the reasons to shorten the time between hikes. However, they also highlighted the failure of inflation to increase above 2% as a reason to widen the time period between hikes. The consensus was for inflation to reach 2% and for labour inflation to gradually lift inflation. The medium-term inflation outlook appears little changed and the flatness of the yield curve is not unusual. Several officials were concerned by low inflation. EURUSD sold off to session lows close to 1.20000, while USDJPY rallied from 112.292 to 112.604 after the minutes were released.

German Unemployment Rate s.a.(Dec) data came in unchanged at 5.5% v an expected 5.6%. Unemployment Change (Dec) was out at the same time and came in at -29K v an expected -12K, from a prior of -20K. EURUSD was at 1.20420 when the data was released but sold off to 1.20110.

UK Construction PMI (Dec) was out at 52.2 v an expected 52.5, from a prior number of 53.1. While still expanding, this data point is much lower compared to the recent highs around 64.0 in 2014. GBPUSD was trading around 1.35925 but slowly sold off to 1.35000 following the release.

US ISM Prices Paid (Dec) came in at 69.0 v a consensus of 65.0. The previous reading was 65.5. ISM Manufacturing PMI (Dec) was also out at this time and came in at 59.7 v 58.2 expected, from 58.2 prior. And finally, Construction Spending (MoM) (Nov) was 0.8% v 0.6% expected, from the previous reading of 1.4%, which was revised to 0.9%. USDJPY was at 112.223 before the release but moved higher to 112.495 before pulling back.

EURUSD is up 0.14% overnight, trading at around 1.20308.

USDJPY is largely unchanged in the early session trading at around 112.539.

GBPUSD is up 0.10% to trade around 1.35244.

Gold is down -0.21% in early morning trading at around $1,310.14.

WTI is up 0.29%, trading at around $62.06.

Major data releases for today:

At 09.00 GMT, Eurozone Markit Services PMI (Dec) data is expected to be unchanged from the previous reading of 56.5. Markit PMI Composite (Dec) is also due out at this time and is expected to be unchanged at 58. EUR pairs could see price movement if the data released varies from the consensus.

At 09.30 GMT, UK Markit Services PMI (Dec) is out and expected to be unchanged from the previous value of 53.8. Also at this time, Net Lending to Individuals (MoM) (Dec) is expected at £4.9B v a previous reading of £4.8B. Mortgage Approvals (Nov) is expected at 64.000K v a prior 64.575K. Consumer Credit (Nov) is expected to be £1.500B v £1.451B previously. GBP crosses may experience volatility if the number differs from the expected reading.

At 13:15 GMT, US ADP Non-Farm Employment Change is expected to come in unchanged at 190K. USD crosses could be impacted by the volume of data releases at this time and may result in turbulent price action.

At 13:30 GMT, US Continuing Jobless Claims (Dec 22) is expected at 1.947M from a prior of 1.943M. Initial Jobless Claims (Dec 29) is expected to be 240K with a previous reading of 245K.

At 14:45 GMT, US Markit PMI Composite (Dec) is expected at 53.7 from a prior of 53.0. Markit Services PMI (Dec) is expected to come in unchanged from the previous reading at 52.4. This data could move Stocks, Bonds and USD pairs upon its release.

At 16.00 GMT, EIA Crude Oil Stocks change (Dec 29) is released, with a headline number of -5.260M from a previous -4.609M. This data release was delayed due to New Year’s festivities. WTI Oil may see volatility around this data release.

Currencies: Dollar Bottoms Going Into Tomorrow’s Key US Payrolls

Sunrise Market Commentary

- Rates: Sentiment-driven trading ahead of payrolls?

We expect trading to be subdued and sentiment-driven today ahead of tomorrow's US payrolls report. Ongoing strength on stock and oil markets might weigh on core bonds. The US Note future closes in on the contract low, but higher earnings/inflation readings will probably be necessary to trigger a break. - Currencies: Dollar bottoms going into tomorrow's key US payrolls

The recent USD decline slowed yesterday. Technical considerations (EUR/USD coming close to the cycle top) and strong US eco data helped to put a floor for the dollar. We expect the dollar to hold a wait-and-see mode today. Sterling tried to change fortunes at the first day of the year, but failed to sustain that constructive momentum.

The Sunrise Headlines

- US stock markets extended their record race, eking out gains between +0.4% and +0.84%. Asian risk sentiment is positive as well with Japan outperforming on their first trading day of the new year in a catch-up move.

- FOMC Minutes showed that Fed members wrestled with how much of an economic impact to expect from Donald Trump's tax cuts as they raised rates last month and continued to be flummoxed by persistent low inflation.

- China's services sector activity expanded at its fastest pace in over three years in December on solid growth in new business, with the outlook improving to a six-month high, the Caixin Chinese services PMI showed (rise to 53.9).

- UK PM May believes Barnier is bluffing when he says there will be no special deal for financial services, officials said, as the UK prepares to negotiate its post-Brexit ties with the EU.

- Chancellor Merkel's Christian Democrat-led bloc and its prospective coalition partner, the SPD, said the chances of a successful conclusion to their exploratory talks have improved after a meeting in Berlin yesterday.

- The US auto industry suffered its first annual sales decline since the financial crisis eight years ago, but a streak of strong profits is expected to overshadow a slowdown in dealership traffic.

- Today's eco calendar contains services PMI's in the UK and EMU (final), US ADP employment and weekly jobless claims. Spain and France tap the market while Fed Bullard is scheduled to speak

Currencies: Dollar Bottoms Going Into Tomorrow's Key US Payrolls

Dollar decline slows ahead of the payrolls

The dollar's slide slowed yesterday. The US currency regained modest ground against the euro as interest rate differentials widened again slightly. US data (auto sales & Manufacturing ISM) were better than expected, adding to USD constructive sentiment. The Fed minutes revealed different views on persistent low inflation and on the Fed's policy approach, but a majority of governors supports gradual normalisation. EUR/USD closed the day at 1.2010, off Tuesdays top of 1.2081. USD/JPY bottomed, finishing the day at 112.51.

The risk rally continues in Asia overnight, but the dollar holds near yesterday's closing. EMU services PMI's are expected to confirm strong readings from the preliminary report today. US ADP private job creation is expected at a solid 190 000. US jobless claims are expected marginally higher. US data will likely be OK, but won't change the broader picture ahead of tomorrow's US payrolls. Risk sentiment stays constructive, but is less supportive for the dollar than it was in the past. The USD might stabilize off recent lows ahead of the payrolls. Recently, the greenback suffered as the global recovery could force other major CB's (including ECB) to join policy normalisation. Still, we maintain the working hypothesis that it won't be that easy for EUR/USD to set a new cycle high without really important news. US payrolls and especially wage growth will be key for the next directional USD move.

Global picture USD: The Dec Fed & ECB meetings didn't bring clear directional guidance for EUR/USD. A narrowing in the (LT) interest rate differential finally drove EUR/USD to the topside of the 1.1554/1.2090 range. A break would improve the ST picture. We don't preposition for such a break, yet. Quite some good news on the euro/bad news on the dollar should be discounted. Price data remain in focus.

Sterling yesterday failed to hold a tentative improvement from the first day of the year. In order-driven trade, GBP lost ground against the euro and the dollar. Today's UK services PMI is expected marginally stronger at 54.0. Brexit noise might resurface as negotiators prepare next steps. EUR/GBP showed a consolidation pattern of late. We don't see a trigger for a big GBP comeback. A EUR/GBP rebound above 0.89 might reinforce the euro positive/sterling negative momentum. Recent UK data were mixed. We don't expect the BoE to raise interest rates soon. The EUR/GBP 0.8700/60 support looks solid. Ongoing euro strength or soft UK data might keep EUR/GBP 0.90 on the radar further down the road. We keep a EUR/GBP buy-on-dips in case of return action to 0.87.

EUR/USD topside test rejected