Sample Category Title

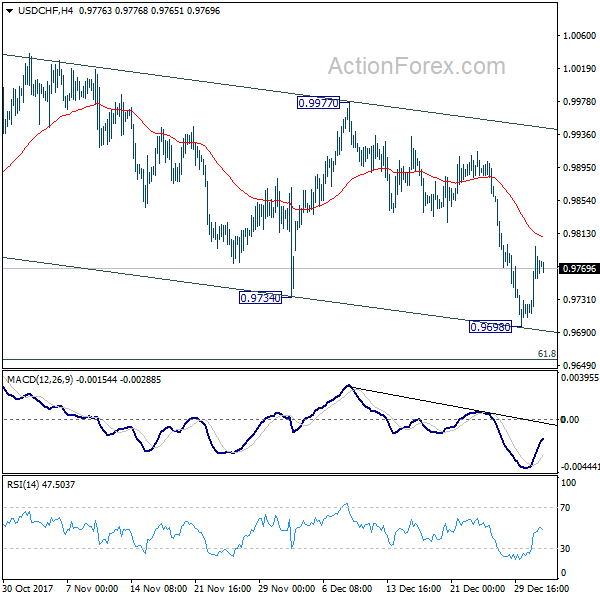

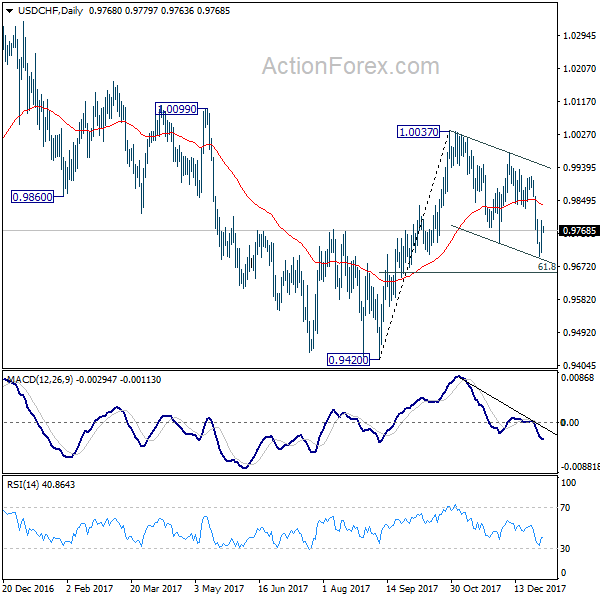

USD/CHF Daily Outlook

Daily Pivots: (S1) 0.9718; (P) 0.9758; (R1) 0.9807; More....

Intraday bias in USD/CHF remains neutral for the moment. As long as 4 hour 55 EMA (now at 0.9808) holds, deeper fall is mildly in favor. But we'd expect 61.8% retracement of 0.9420 to 0.1.0037 at 0.9656 to contain downside and bring rebound. Sustained break of 4 hour 55 EMA will argue that the correction from 1.0037 has completed and turn focus to 0.9977 resistance for confirmation.

In the bigger picture, range trading continues between 0.9420/1.0342. At this point, 0.9420 appears to be a strong support level. Therefore, in case of decline attempt, we don't expect a firm break of this level. Nonetheless, strong break of 1.0342 is also needed to confirm upside momentum. Otherwise, medium term outlook will stay neutral.

Australia’s Services Sector Climbed In December

For the 24 hours to 23:00 GMT, the AUD slightly rose against the USD and closed at 0.7831.

LME Copper prices declined 0.9% or $65.5/MT to $7115.5/MT. Aluminium prices declined 0.7% or $15.0/MT to $2241.0/MT.

In the Asian session, at GMT0400, the pair is trading at 0.7832, with the AUD trading a tad higher against the USD from yesterday's close.

Overnight data showed that Australia's AiG performance of services index advanced to a level of 52.0 in December, compared to a level of 51.7 in the prior month.

Elsewhere in China, Australia's largest trading partner, the Caixin/Markit services PMI unexpectedly rose to a level of 53.9 in December, expanding at its fastest pace in three-years, thus suggesting that the world's second economy is on a robust growth path. In the previous month, the PMI had recorded a level of 51.9, while market participants had expected for a fall to a level of 51.8.

The pair is expected to find support at 0.7810, and a fall through could take it to the next support level of 0.7787. The pair is expected to find its first resistance at 0.7850, and a rise through could take it to the next resistance level of 0.7867.

Looking ahead, Australia's trade balance numbers for November, set to release overnight, will be on investors' radar.

The currency pair is showing convergence with its 20 Hr and 50 Hr moving averages.

Germany’s Unemployment Rate Remained Unchanged In December

For the 24 hours to 23:00 GMT, the EUR declined 0.37% against the USD and closed at 1.2013, shrugging off upbeat German jobs report.

Data revealed that Germany's seasonally adjusted unemployment rate remained steady at a record low 5.5% in December, in line with market expectations, as the number of people unemployed sharply fell, thus pointing to a vibrant labour market in the wake of robust growth in the Euro-zone's largest economy.

The US Dollar gained ground against its key counterparts, after minutes of the Federal Reserve's (Fed) December monetary policy meeting indicated that officials are mulling a faster pace of rate increases this year.

As per the minutes, policymakers were optimistic that robust economic fundamental in the US economy would warrant a gradual pace for interest rate hikes in 2018. Further, most policymakers shared the view that the latest tax overhaul would likely benefit the economy, but remained split on whether the resulting growth would warrant a faster pace of rate hikes this year, as most believed it to provide a lift to consumer spending and business investment. However, it also revealed disagreement over the pace of rate hikes if inflation struggles to move up towards the central bank's 2.0% target.

Gains in the greenback were boosted further, on the back of encouraging economic reports in the US.

The US ISM manufacturing activity index unexpectedly climbed to a three-month high level of 59.7 in December, defying market expectations for the index to remain steady at 58.2, thus justifying the notion of strong economic momentum in the world's largest economy. Moreover, the nation's construction spending grew 0.8% on a monthly basis in November, advancing for the fourth consecutive month and exceeding market consensus for a gain of 0.5%. Construction spending had risen by a revised 0.9% in the prior month.

Other data showed that the nation's MBA mortgage applications rebounded 0.7% in the week ended 29 December 2017, after declining 4.9% in the prior week.

In the Asian session, at GMT0400, the pair is trading at 1.2017, with the EUR trading a tad higher against the USD from yesterday's close.

The pair is expected to find support at 1.1992, and a fall through could take it to the next support level of 1.1966. The pair is expected to find its first resistance at 1.2052, and a rise through could take it to the next resistance level of 1.2086.

Moving ahead, traders would look forward to the final Markit services PMI for December, scheduled to release across the Euro-zone in a few hours. Moreover, the US ADP employment change and the final Markit services PMI, both for December along with the weekly jobless claims data, all due to release later today, will keep investors on their toes.

The currency pair is showing convergence with its 20 Hr moving average and trading below its 50 Hr moving average.

UK’s Construction Sector Growth Eased From A 5-Month High In December

For the 24 hours to 23:00 GMT, the GBP declined 0.59% against the USD and closed at 1.3512, on the back of weaker-than-expected construction sector data in Britain.

The Markit construction PMI in the UK dropped more-than-expected to a level of 52.2 in December, easing for the first time since September 2017. The PMI had registered a reading of 53.1 in the prior month, while investors had envisaged for a fall to a level of 53.0.

In the Asian session, at GMT0400, the pair is trading at 1.3520, with the GBP trading 0.06% higher against the USD from yesterday's close.

The pair is expected to find support at 1.3472, and a fall through could take it to the next support level of 1.3425. The pair is expected to find its first resistance at 1.3590, and a rise through could take it to the next resistance level of 1.3661.

Trading trend in the Pound today is expected to be determined by the release of UK's Markit services PMI for December. Also, the nation's net consumer credit and mortgage approvals data, both for November, would garner a lot of market attention.

The currency pair is trading below its 20 Hr and 50 Hr moving averages.

Japan’s Manufacturing Sector Activity Rose Less Than Initially Estimated In December

For the 24 hours to 23:00 GMT, the USD rose 0.28% against the JPY and closed at 112.56.

In the Asian session, at GMT0400, the pair is trading at 112.65, with the USD trading 0.08% higher against the JPY from yesterday's close.

Data released overnight revealed that Japan's final Nikkei manufacturing PMI was revised lower to a level of 54.0 in December, while the preliminary figures had indicated a rise to a level of 54.2. The PMI had recorded a level of 53.6 in the prior month.

The pair is expected to find support at 112.30, and a fall through could take it to the next support level of 111.95. The pair is expected to find its first resistance at 112.89, and a rise through could take it to the next resistance level of 113.13.

Going ahead, market participants would eye the release of Japan's Nikkei services PMI for December, due overnight.

The currency pair is trading above its 20 Hr and 50 Hr moving averages.

Swiss Manufacturing Activity Expanded At Its Quickest Pace In Over 7 Years In December

For the 24 hours to 23:00 GMT, the USD rose 0.53% against the CHF and closed at 0.9773.

In economic news, Switzerland’s SVME–PMI registered an unexpected rise to a level of 65.2 in December, accelerating at its fastest pace in more than seven years. The PMI had recorded a reading of 65.1 in the prior month, while market had expected for a drop a level of 64.5.

In the Asian session, at GMT0400, the pair is trading at 0.9776, with the USD trading a tad higher against the CHF from yesterday’s close.

The pair is expected to find support at 0.9728, and a fall through could take it to the next support level of 0.9680. The pair is expected to find its first resistance at 0.9811, and a rise through could take it to the next resistance level of 0.9846.

With a lack of macroeconomic releases in Switzerland today, investor sentiment would be governed by global macroeconomic news.

The currency pair is trading above its 20 Hr and 50 Hr moving averages.

Loonie Trading A Tad Higher In The Morning Session

For the 24 hours to 23:00 GMT, the USD rose 0.22% against the CAD and closed at 1.2541.

In the Asian session, at GMT0400, the pair is trading at 1.2539, with the USD trading slightly lower against the CAD from yesterday’s close.

The pair is expected to find support at 1.2508, and a fall through could take it to the next support level of 1.2476. The pair is expected to find its first resistance at 1.2563, and a rise through could take it to the next resistance level of 1.2586.

The currency pair is showing convergence with its 20 Hr moving average and trading above its 50 Hr moving average.

Elliott Wave View: Nasdaq Has Resumed Higher

Elliott Wave view for Nasdaq suggests that the rally from Intermediate wave (4) on 12/5 unfolded as a double three Elliott Wave structure where Minor wave W ended at 6545.75 and Minor wave X ended at 6383.25. The Index has made a new high above Minor wave W at 6545.75, which brings validity to this view. Subdivision of Minor wave W unfolded as a double three Elliott Wave structure where Minute wave ((w)) ended at 6427.75, Minute wave ((x)) ended at 6383, and Minute wave ((y)) of W ended at 6545.75.

The Index then pullback in Minor wave X with subdivision of a triple three Elliott Wave structurewhere Minute wave ((w)) ended at 6463.25, Minute wave ((x)) ended at 6520.75, Minute wave ((y)) ended at 6432.25, and second Minute wave ((x)) of X ended at 6383.25. Near term, rally from 12/30 low (6383.25) looks impulsive and could see more upside to end 5 waves up in Minute wave ((a)). Afterwards, the Index should pullback in Minute wave ((b)) in 3, 7, or 11 swing to correct cycle from 12/30 low (6383.25) before the rally resumes. We don’t like selling the Index and while dips stay above 6383.25, and more importantly above 6232.30, expect the Index to extend higher.

Nasdaq 1 Hour Elliott Wave Chart

Market Update – Asian Session: Upcoming US ADP Nonfarm Payrolls Data In Focus

Headlines/Economic Data

General Trend: Nikkei 225 outperforms on catch up rally after being closed for past 3 sessions

Energy shares gain after Wednesday's up move in oil prices.

South Korean equities underperform

China Caixin Services PMI hits more than 3 year high in Dec

Japan

Nikkei 225 opened +1.4% (in first trading session of 2018); closed +3.3%

Japanese stocks at highest since 1991 as market reopens after New Year holiday break

Topix Securities Index +4.3%, Electric Appliances +3.1%, Iron & Steel +2.1%

Japanese mega banks start 2018 on a positive note: Sumitomo Mitsui Financials +2.7%, Mitsubishi UFJ +2.3%, Mizuho Financial +2.0%

Automakers track US gains: Toyota +2.3%, Honda +2.5%

SBI Holdings: +17.5% (gains attributed to the recent strength seen for the Ripple cryptocurrency)

Fast Retailing +2.7% (to report Dec SSS after close on Friday)

Softbank +4% (tracks gains on the Nasdaq)

Nintendo +4.4%: Pokemon Go expected to finally enter China market, said a press report released on Jan 2nd.

Shin-Etsu Chemical +4.8% (broker commentary)

Chip-related firm SUMCO +3.8% (broker commentary)

(JP) Japan Dec Final PMI Manufacturing: 54.0 v 54.2 prelim (highest level since Feb 2014)

(JP) Japan Fin Min Aso: GDP growth has steadily increased from 5-years ago; Economy, labor and wage environment has also truly changed

Korea

Kospi opened +0.7%, has since reversed gains

Hyundai Motor -2.5% (union announced partial strike), Kia Motors -2.4%: South Korea Dec Auto Exports Y/Y: -40.4%

LG Chemicals -3.4%: China continues to exclude South Korea battery makers from subsidy, said a South Korean Press report.

Amorepacific -2.5% (broker commentary)

Steelmakers track US gains: Posco +2.5%

Lotte Shopping +5.5% (broker commentary)

Mixed trading in the chip sector: Samsung Electronics -0.9% , Hynix +1.4%

(KR) South Korea Fin Min Kim and BOK Gov Lee agree to closely monitor risk factors and take swift measures if needed

(KR) South Korea military: No imminent missile launch seen from North Korea

(KR) South Korea Dec Foreign Reserves: $389.3B v $387.3B prior (record high): Bank of Korea said weakness in the US dollar (USD) increased the value of its holdings denominated in other currencies when converted.

China/Hong Kong

Hang Seng opened +0.4%, Shanghai Composite +0.1%

Hang Seng Energy Index +3%, Information Technology +1.4%

(CN) China researcher sees GDP growth of 6.3%/year by 2020 – 21st Century Herald

(CN) China PBOC outlined plan to limit power use by some bitcoin miners

(HK) Hong Kong Dec PMI Services: 51.5 v 50.7 prior (~4-yr high)

(CN) China PBoC: Skips OMO for 9th straight session; Net drains CNY130B v CNY90B prior

USD/CNY (CN) China PBoC sets yuan reference rate at 6.5043 v 6.4920 prior

(CN) CHINA DEC CAIXIN PMI SERVICES: 53.9 V 51.9 PRIOR (fastest rise since Aug 2014); PMI COMPOSITE: 53.0 V 51.6 PRIOR

Australia/New Zealand

ASX 200 opened +0.2%; closed +0.1%

ASX 200 Energy Index +1.2%, Financials flat ; Utilities -1.1%

(AU) According to industry expects with the Australia property cycle reaching its peak, new floats of A-REITs are unlikely and major offshore investors instead may be eyeing opportunities - AFR

(NZ) Realestate.co.nz reported that New Zealand Dec new listings totaled 7,133, -6.2% y/y

Looking ahead: Australia Nov Trade Balance due for release on Friday

Other Asia

(SG) Singapore Dec PMI Composite: 52.1 v 55.4 prior (first fall in six months and the slowest pace of expansion since July)

(TW) There is speculation that Taiwan could raise interest rates in Q3, would be first rate hike since 2011 – US financial press

(TW) Taiwan Premier: concerned about impact from US tax overhaul

(TW) Taiwan to cut central government budget - Taiwanese Press

North America

US equity markets ended higher: Dow +0.4%, S&P500 +0.6%, Nasdaq +0.8%, Russell 2000 +1.1%

S&P500 Energy Sector +1.5%, Health care +1%, Tech +0.8%

Intel: On Wednesday's session, Intel declined by over 3% amid a report from The Register that suggested that a design flaw in Intel's processor chips drove a security-related redesign of the Linux and Windows kernels

Costco Dec SSS above ests: Reports Dec SSS (ex-gas) 8.8%; US SSS (ex-gas) 9.1% v 6.8%e

CVS To hold conference call on Thursday Jan 4th to discuss 2017 and 2018 earnings guidance

(US) FOMC MINUTES FROM DEC 13 MEETING: OFFICIALS SAW MODEST BOOST FROM TAX CHANGES; Generally agreed flatness of yield curve not unusual by historical standards; some expressed concern a possible future inversion could portend economic slowdown; Several Fed officials concerned by low inflation expectations

(US) DEC ISM MANUFACTURING: 59.7 V 58.2E; PRICES PAID: 69.0 V 64.5E

(US) Pres Trump: [Former adviser] Steve Bannon has nothing to do with me or my Presidency. When he was fired, he not only lost his job, he lost his mind - White House

statement ** NOTE Earlier: Steve Bannon was quoted in a new book saying the June 2016 Trump Tower meeting between Donald Trump Jr. and a Russian lawyer was "treasonous"

(US) Weekly API Oil Inventories: Crude: -5M v -6M prior

Looking Ahead: US Dec ADP Nonfarm Employment Change due for release on Thursday, along with the weekly DoE Crude Oil Inventories

Europe

(UK) UK govt reportedly plans to guarantee EU-level farming grants post-Brexit - UK press

(UK) Tony Blair denies claim he told Trump about UK spying - Sky News

(UK) London link may allow for UK stock trading during China hours – US financial press

(DE) Chancellor Merkel's CDU/CSU and SPD agreed to hold exploratory talks on joint govt from Jan 7th

Looking ahead: UK Dec Services PMI to be released

Levels as of 01:00ET

Nikkei225 %, Hang Seng +0.5%; Shanghai Composite +0.7%; ASX200 +0.1%, Kospi -0.5%

Equity Futures: S&P500 +0.1%; Nasdaq100 +0.2%, Dax +0.3%; FTSE100 -0.1%

EUR 1.2023-1.2005; JPY 112.78-112.48; AUD 0.7842-0.7815;NZD 0.7110-0.7073

Feb Gold -0.6% at $1,310/oz; Feb Crude Oil +0.8% at $62.09/brl; Mar Copper +0.5% at $3.27/lb

Market Morning Briefing: The Euro Broke Above 1.19

STOCKS

Dow (24922.68, +0.40%), as per our expectations in the last briefing, has stayed below 25000 during the holiday week, and could now attempt to move towards resistance near 25400 on the daily candles over the next couple of weeks.

Dax (12978.21, +0.83%) tested support near 12767 on 2nd Jan, and is now seeing a bounce underway, which could take it to 13000 in the next couple of days and lead to a test of resistance near 13200 next week.

Nikkei (23326.06, +2.46%) has shot up since yesterday after being range bound in the narrow range of 22600-23000 during the festive week. It might see a dip from current levels or after testing resistance near 23400 on the 3 day line charts.

Shanghai (3382.02, +0.38%) has bounced from its sideway ranging just near support below 3300 in the past week and is now rapidly moving up, looking to test levels near 3500 which is a crucial resistance level, seen on 3 day and weekly candles.

Nifty (10443.20, +0.01%) and Sensex (33793.38, -0.06%) both haven’t seen much movement in the past week and might turn bearish for the near term, moving towards support near 10200-10250 and 33400-33500 respectively.

COMMODITIES

Gold (1308.20) has been on a continuous uprise since it tested support near 1236 in mid December. It broke resistance near 1285 (on daily candles) in end December and is now headed to test resistance near 1325 on the weekly line charts. With the recent bout of Dollar weakness expected to halt for a bit, we could see Gold stay below resistance at 1325, but in case of further bullishness, we could see attempt of 1350, seen as resistance on 3 day and weekly line charts.

Brent (67.93) and WTI (61.89) have both seen a rally in the last few days due to several factors like shutdown of the Forties North Sea pipeline, unrest in Iran and also, US stockpiles data showing a continuous decrease in inventory over the last few weeks. WTI might see a sloght corrective dip now, given that it is near resistance (61.90) on the daily & 3 day candles. Brent could find resistance near 68-68.50 on the weekly line charts.

Copper (3.2515) has been bullish since mid December, seeing a high near 3.30 at the beginning of the year from where a slight dip is now underway. It could dip further towards 3.10-3.15 before turning bullish again.

FOREX

2018 has started on a weak note for the Dollar.

The Euro (1.2015) broke above 1.19 to see a high of 1.2080 and has retreated a bit from there. It has intra-week support in the 1.1997-61 region and can target 1.21-22 in the next couple of weeks while the Support holds.

Dollar-Yen (112.68) has come down from the resistance at 113.50 and might try to break below 112.00. If successful it can target 110 in the coming weeks. Else it could move back up towards 113.50. Need to watch this.

The Euro-Yen (135.40) has risen well above earlier resistance at 134 but may have a channel resistance at 135.70 on the weekly candles. It will be crucial to see if this breaks or holds.

The Pound (1.3517) rose well above 1.35 standing upwards towards 1.36 and higher.

The Australian Dollar (0.7827) has been a star performer in December and looks bullish overall. But it has crucial 200-week moving average resistance just above current levels, which needs to break to allow the Aussie to move up further.

The Chinese Yuan (6.5060) has long term support just below current levels and could be a candidate for a bounce.

Dollar-Rupee (63.50) has fallen sharply last few days along with Euro strength. If the Euro again moves up from the 1.1997-61 Support region, then Dollar-Rupee may also find near term Resistance in the 63.60-80 region.

INTEREST RATES

US Yields dipped a bit in late December but have started to move up again in the last few days, perhaps on the back of higher crude prices. The US 10Yr (2.46%) seems to be straining to break above long term resistance at current levels. The 30Yr (2.80%) has room to rise on the upside. If so, it could lead to some much needed Curve-steepening.

German Yields have also been rising in the last few days and the German 10Yr (0.43%) could rise some more towards 0.50%. The last few days have seen the German-US Yield Spread (-2.03%) move up in favour of the Euro. Some more upside towards -2.00% or even -1.95% could be possible.

The 10Yr GOI (7.3447%) should have Resistance in the 7.40-45% region and ought to see a pullback towards 7.20% or evn 7.00%.