Sample Category Title

USD/CHF Mid-Day Outlook

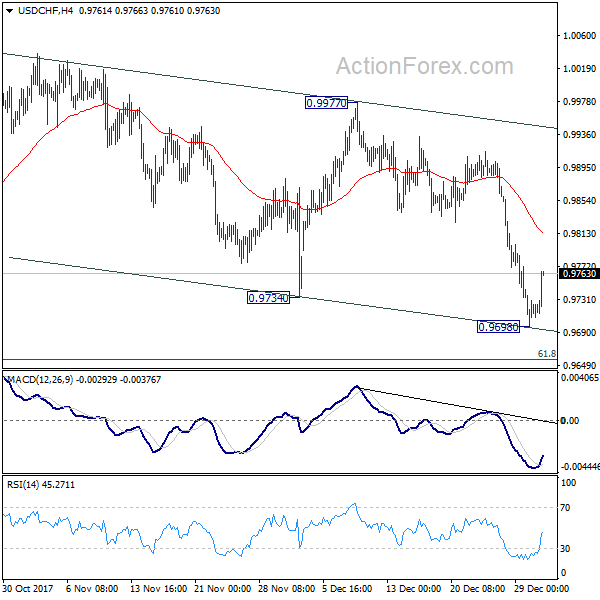

Daily Pivots: (S1) 0.9694; (P) 0.9721; (R1) 0.9744; More....

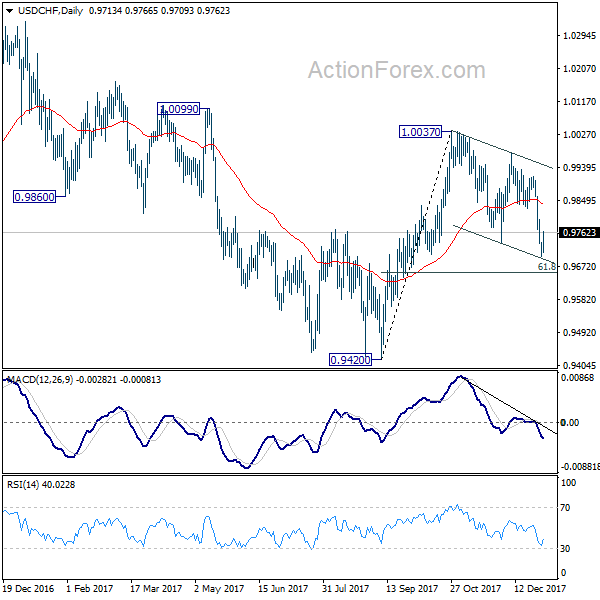

A temporary low is in place at 0.9698 in USD/CHF, just ahead of near term channel support. As long as 4 hour 55 EMA (now at 0.9813) holds, deeper fall is mildly in favor. But we'd expect 61.8% retracement of 0.9420 to 0.1.0037 at 0.9656 to contain downside and bring rebound. Sustained break of 4 hour 55 EMA will argue that the correction from 1.0037 has completed and turn focus to 0.9977 resistance for confirmation.

In the bigger picture, range trading continues between 0.9420/1.0342. At this point, 0.9420 appears to be a strong support level. Therefore, in case of decline attempt, we don't expect a firm break of this level. Nonetheless, strong break of 1.0342 is also needed to confirm upside momentum. Otherwise, medium term outlook will stay neutral.

EUR/USD Mid-Day Outlook

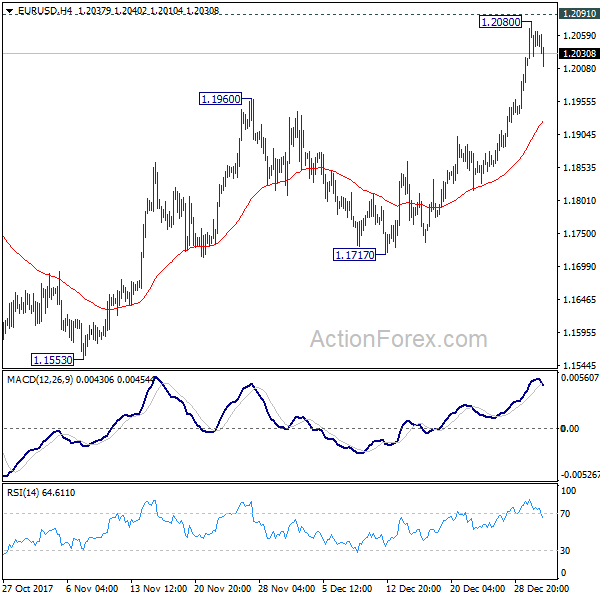

Daily Pivots: (S1) 1.2010; (P) 1.2045 (R1) 1.2094; More....

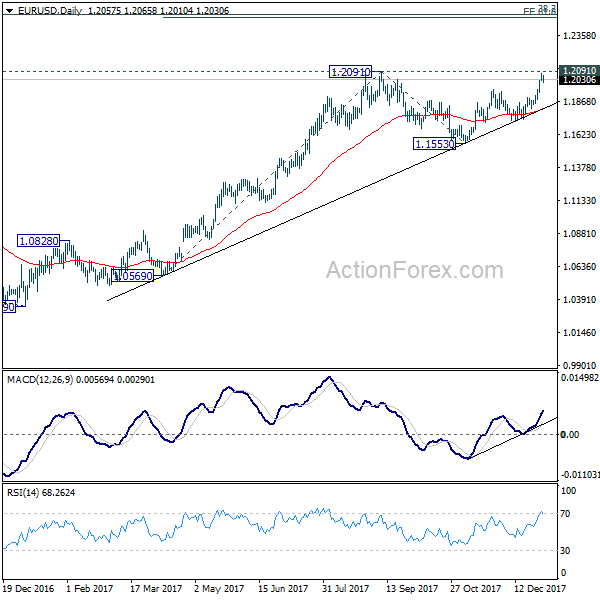

EUR/USD's retreat, with 4 hour MACD crossed below signal line, suggests that a temporary top is formed at 1.2080, ahead of 1.2091 key resistance. Intraday bias is turned neutral first. Some consolidation could be seen but further rise is expected as long as 4 hour 55 EMA (now at 1.1922) holds. Firm break of 1.2091 will confirm medium term rally resumption and target next key fibonacci level at 1.2494/2516. However, sustained break of 4 hour 55 EMA will extend the consolidation pattern from 1.2091 with with another decline through 1.1717 support.

In the bigger picture, rise from 1.0339 medium term bottom is seen as a corrective move for the moment. Therefore, in case of another rally, we'd be expect 38.2% retracement of 1.6039 (2008 high) to 1.0339 (2017 low) at 1.2516 to limit upside and bring reversal. That is also close to 61.8% projection of 1.0569 to 1.2091 from 1.1553 at 1.2494.

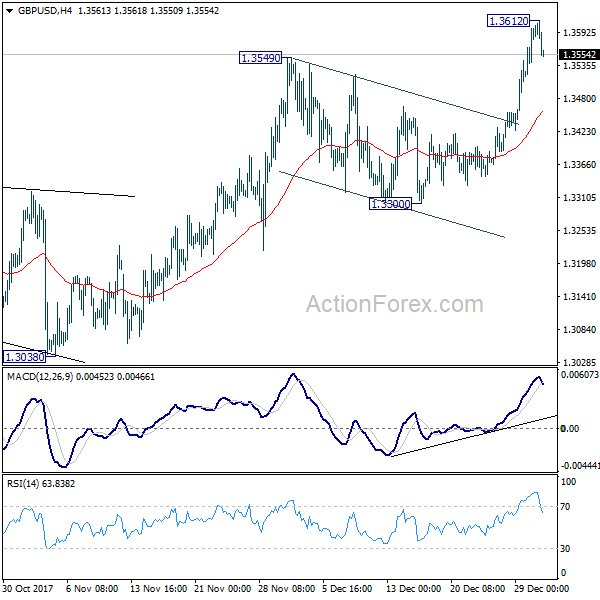

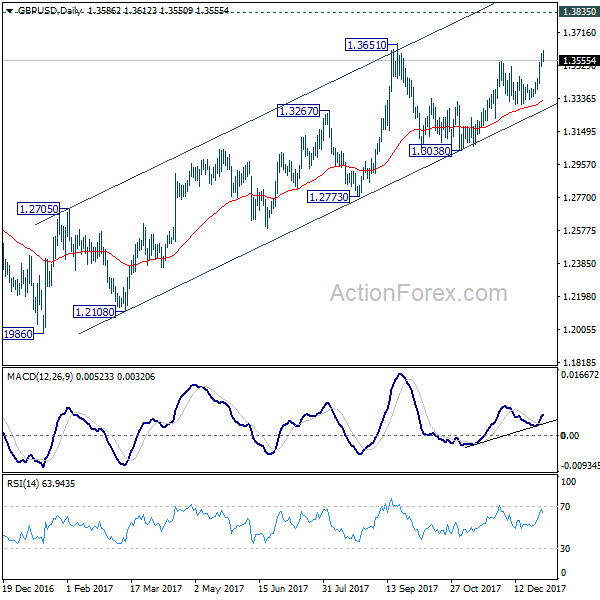

GBP/USD Mid-Day Outlook

Daily Pivots: (S1) 1.3527; (P) 1.3564; (R1) 1.3629; More.....

A temporary top is in place at 1.3612 in GBP/USD and intraday bias is turned neutral for consolidation first. As long as 4 hour 55 EMA (now at 1.3455) holds, further rally is expected. Above 1.3612 will target 1.3651 key resistance first. Break will resume medium term rise from 1.1946 and target key resistance level at 1.3835. However, sustained break of 4 hour 55 EMA will turn focus back to 1.3300 support.

In the bigger picture, while the medium term rebound from 1.1946 low was strong, it's limited below 1.3835 key support turned resistance. As long as 1.3835 holds, we'd view such rebound as a correction. That is, we'd expect another leg in the long term down trend through 1.1946 low. However, sustained break of 1.3835 should at least send GBP/USD to 38.2% retracement of 2.1161 (2007 high) to 1.1946 (2016 low) at 1.5466.

Euro Loses Ground But Remains above $1.20; FOMC Minutes Awaited

Here are the latest developments in global markets:

FOREX: The dollar posted some gains to climb further above a 3½-month low versus a basket of currencies hit on Tuesday. The euro eased versus the greenback despite the release of positive jobs data out of Germany, while pound/dollar lost some ground following the release of construction PMI figures that came in below analysts' expectations; the pair previously crossed above the 1.36 handle to record its highest since late September.

STOCKS: European equity markets were broadly in the green. The pan-European Stoxx 600 was 0.3% up near midday, while the blue-chip Euro Stoxx 50 traded higher by 0.25%. The UK's FTSE 100 was up on the margin after yesterday's retreat from record high levels; sterling being on the rise weighed on the export-heavy benchmark during Tuesday's trading. The German DAX and the French CAC 40 traded up by 0.5% and 0.4% respectively. The Italian FTSE MIB underperformed, being down by 0.2%. Retailer Next (up 7.7%) was a notable outperformer, leading gains within the FTSE as well as being one of the top performers within the Stoxx 600 after the firm upgraded its profit guidance on the back of better-than-anticipated Christmas sales. The new EU-wide MiFID financial market rules and what they mean moving forward were also gaining attention during today's European session. Dow, S&P 500 and Nasdaq 100 futures all traded up by 0.2%.

COMMODITIES: WTI and Brent crude recovered from morning losses to both trade higher by 0.4%, at $60.63 and $66.84 per barrel respectively. Both benchmarks were close to yesterday's 2½-year highs. Gold was down by 0.2%, at $1,315.12 an ounce after touching $1,321.33 earlier in the day, its highest since mid-September. Should it finish lower, this would mark its first daily decline in numerous days.

Day ahead: Fed meeting minutes awaited; euro retreats despite positive surprise in German labor data

The dollar index, which gauges the greenback's strength versus the currencies of six major US trading partners, was 0.25% up at 92.10 ahead of the FOMC minutes pertaining to December's meeting. This compares to 91.75 recorded on Tuesday, the index's lowest since September 20. A hawkish or bearish bias in policymakers' views has in the past spurred movements in the dollar and is expected to do so again as the minutes go public at 1900 GMT. Dollar/yen was roughly flat at 112.23 after touching 112.04 on Tuesday, its lowest since December 15.

Euro/dollar was 0.4% down, giving up most of yesterday's advance that saw it hit 1.2082, coming close to September 8's 1.2092 which is also the highest for the pair in nearly three years. The decline could be in part attributed to profit-taking ahead of sizable gains in preceding days as well as positioning ahead of upcoming releases, with lower European bond yields in today's trading also possibly playing a role. The pair failed to find support from largely upbeat labor market data out of Germany, eurozone's - and Europe's - largest economy that saw the unemployment rate decline to the post-reunification low of 5.5%. Despite the decline, euro/dollar remained above 1.20.

Pound/dollar was down by 0.2%. Despite falling, the pair consolidated around 3½-month high levels. Earlier in the day it touched 1.3612, its highest since September 20. The pair retreated after December's Markit/CIPS construction PMI came in below expectations and reflected a slowdown relative to November's five-month high of 53.1; the first such slowdown since September. The respective figure for the services sector - by far the largest sector in the UK - is due on Thursday.

In commodity currencies, the antipodeans recovered from earlier losses to trade roughly flat versus the greenback. Aussie/dollar and kiwi/dollar were at 0.7832 and 0.7099 respectively, trading not far below their highest since late October hit on Tuesday. The oil-linked Canadian dollar lost some ground versus the its US counterpart, though it still traded close to its highest in two-and-a-half months (as dollar/loonie touched 1.2496 earlier in the day).

In terms of other data, the US will see the release of figures on November construction spending and ISM's manufacturing PMI for the month of December. Both figures are expected to ease, though the latter one only slightly so. Any surprises are likely to see forex market participants positioning accordingly. December total vehicle sales out of the US are due at 2030 GMT, while the API's weekly report that includes information on, among others, US crude stocks, has the capacity to lead to movements in oil markets.

EURJPY Makes Corrective Move Back Below Key 135 Level

EURJPY was unable to sustain gains made after rising to 135.62 yesterday, its highest level in over two years. The pair has fallen sharply and broke below the key 135.00 level today.

The corrective selloff so far has stabilized. But looking at the 4-hour chart, near-term price action still looks a little soft, as RSI has dipped below 50, indicating risk is to the downside.

The recent retracement in EURJPY may extend a little lower towards 134.50. This level is seen as minor support ahead of 134.00.

If the market fails to rise and regain the 135.00 handle soon, then the recent bullish phase will likely lose momentum and EURJPY will essential stay in the broader range that it has been trading in since September, as seen on the daily chart.

GBPUSD Only Bullish Above 1.3550 Level

The British pound had turned lower against the U.S dollar during the European trading session, following softer UK data and a minor recovery in the U.S dollar index. In early Wednesday trading, the GBPUSD pair moved to its highest trading level since September 20th, hitting 1.3613. Selling momentum is currently accelerating on the H4 time frame, with the 1.3550 technical level the key daily pivot point for intraday direction. Traders now look to the United States ISM Manufacturing PMI and the release of the FOMC Meeting Minutes later today.

The GBPUSD pair is only intraday bullish while trading above the 1.3550 technical level. Buyers may target the 1.3610 and 1.3657 upside targets.

Should price-action on the GBPUSD pair move below the 1.3550 level, sellers will likely target the 1.3500 and 1.3468 support levels.

USDJPY Still Bearish Below 112.48 Level

The U.S dollar continues to trade at depressed levels against the Japanese yen, despite sellers failing to breach the 112.03 level. Price-action currently holds around the 112.20 mark, with the USDJPY failing to gain traction, despite a minor recovery in the U.S dollar index during the European trading session. The pair remains technically bearish below the 112.48 level, with sentiment remaining depressed. Traders now await the release of the ISM Manufacturing PMI, and the FOMC Meeting Minutes from the FED's December policy meeting.

The USDJPY sellers retain control of the pair while price-action trades below the key 112.48 level. Further selling towards 111.68 remains likely if the 112.03 level is breached.

Should the USDJPY pair encounter intraday buying interest above the 112.48 level, upside targets remain 112.70 and 113.10.

DAX Halts Slide, Investors Eye Fed Minutes

The DAX has reversed directions on Wednesday, moving upwards after three losing sessions. In the Wednesday session, the index is at 12,925.00, up 0.42% on the day. On the release front, German Unemployment Change in December declined by 29,000, well below the estimate of 13,000. This marked the second-highest decline in 2017. In the US, today's key event is the release of the Fed minutes from the December meeting.

Just a few days into the New Year, the Federal Reserve will be on center stage, with the release of the minutes of the December policy meeting. At that meeting, the Fed raised rates by 25 basis points, to a range between 1.25-1.50%. The hike marks a vote of confidence in the US economy, and if the minutes are hawkish, the US dollar could gain ground. The economy is expanding at an impressive clip of above 3 percent. If this pace continues, the Fed could raise rates up to four times in 2018. Currently, the CME Group has priced in a January rate hike at 98.5%. Despite the rosy economic conditions, inflation has been chronically soft, well below the Fed target of 2 percent. Outgoing Fed Chair Janet Yellen and other FOMC members have said that they expect that the strong labor market will push up wages and trigger higher inflation, but this is yet to happen.

The German economy continues to post solid numbers in the fourth quarter of 2017. In December, inflation accelerated to 0.6%, edging above the forecast of 0.5%. The strong gain matched the February reading, equaling the strongest gain recorded in 2017. Unemployment rolls continue to fall, as the labor market continues to remain tight in a robust economy. The numbers are all the more impressive as the political landscape remains uncertain, following inconclusive elections in September. President Angela Merkel is now eyeing the Social Democrats as a coalition partner, but negotiations are moving at a slow pace.

Global stock markets enjoyed a strong year in 2017, and the DAX climbed an impressive 13.0%. Investors gave a thumbs-up as the German and eurozone economies showed solid growth, and data in the fourth quarter has been strong so Expectations remain high that the positive trend will continue into 2018, which bodes well for the DAX. As the new year begins, the markets will be keeping a close eye on the political situation in Germany, as President Angela Merkel strives to put together a new coalition. If new elections are avoided and Merkel forms a new government, the DAX is likely to post strong gains.

Copper May Extend Correction as Descending Indicators Show Further Room at the Downside

Copper future contract extends pullback from new recovery high at $3.3200 on Wednesday, holding negative near-term tone and signaling the beginning of year 2018 in red. Correction after strong rally in past three weeks when metal's price rose over 11% was signaled by reversal of daily indicators from overbought territory, as traders booked their profits on strong advance. Pullback tests initial support at $3.2478 (rising 10SMA), with scope for further easing as daily RSI and slow stochastic head south and show a plenty of room downside. Correction may extend towards $3.2287 (rising daily Tenkan-sen), with deeper dips to be contained above $3.1758 (Fibo 38.2% of $2.9425/$3.3200 rally), to keep bulls intact for fresh attempts higher. Conversely, loss of $3.1758 Fibo support would signal stronger correction.

Res: 3.2790; 3.2850; 3.3085; 3.3200

Sup: 3.2478; 3.2000; 3.1758; 3.1389

Investors Look for Clarity in FOMC Minutes

Wednesday January 3: Five things the markets are talking about

Today's release of the December FOMC minutes (2pm ETD) may have the potential to curtail the 'mighty' U.S dollar's longest losing streak in nearly four-years.

Market bulls are hoping that the minutes' commentary could play down the prospect of a March rate-hike pause – it would be the first meeting to be led by Chairman-designate Powell.

Note: The fixed income market is currently pricing in a +68% chance of a Fed March hike and two more hikes for 2018.

On the on the other hand, dollar 'bears' continue to expect the currency to underperform against its G10 partners, pressured by the Fed taking a more cautious approach this year, while other central banks will likely appear more willing to tighten their own monetary policies (ECB and BoE).

Note: U.S dollar bulls were the biggest losers in 2017 as the dollar index fell just shy of -10 % against a plethora of G10 currency pairs with the EUR being the big winner, climbing +14% outright as the European economy performed much better than expected.

U.S construction spending and ISM manufacturing data are due at 10 am EDT.

1. Global stocks advance

Equity gauges have allied across Asia and Europe in the overnight session, although Japanese markets remained closed. Emerging-market shares also gained for a second consecutive session.

Down-under, resource stocks once again supported Australia's stock market, allowing it to rise slightly and reverse yesterday's small drop. The S&P/ASX 200 rose +0.2%. In S. Korea, the Kospi rallied +0.3%, notching a fourth-straight gain.

In Hong Kong, shares rose for the seventh straight session to a fresh decade-high, aided by strength in index heavyweight Tencent and consumer goods stocks. At close of trade, the Hang Seng index was up +0.15%, while the Hang Seng China Enterprises index rose +0.17%.

In China, equities rose for a fourth straight session overnight, aided by strong gains in consumer and transport firms. The Shanghai Composite index was up +0.65%, while the blue-chip CSI300 index was up +0.61%.

In Europe, regional indices trade higher across the board following on from the momentum seen Asia and stateside yesterday. Both the DAX and CAC lead the gainers recovering from declines seen yesterday, aided by a slight pullback in the EUR (€1.2041).

U.S stocks are set to open in the black (+0.2%).

Indices: Stoxx600 +0.3% at 389.4, FTSE flat at 7648, DAX +0.4% at 12920, CAC-40 +0.2% at 5299, IBEX-35 +0.2% at 10097, FTSE MIB -0.1% at 21812, SMI +0.4% at 9417, S&P 500 Futures +0.2%

2. Oil prices dip as higher output looms, gold softer

Oil prices trade a tad weaker, just shy of their mid-2015 highs reached Tuesday as high output in the U.S and Russia balanced tensions from a sixth day of unrest in OPEC member Iran.

Brent crude futures are at +$66.74 a barrel, up +17c but still trailing yesterday's high of +$67.29. U.S West Texas Intermediate (WTI) crude futures are at +$60.50 a barrel, up +13c cents from the close, though still not far off the $60.74 reached on the previous day that was the highest since June 2015.

Despite anti-government protesters continuing to demonstrate in Iran – a major oil exporter – market sentiment remains bullish on the back of falling inventories globally and strong economic growth forecasted.

Note: Oil markets have been supported by a year of production cuts led by OPEC and Russia. The cuts started 12-months ago and are scheduled to cover all of 2018. While in the U.S, commercial crude oil inventories have fallen by almost -20% from their historic highs last March, to +431.9m barrels.

Strong global demand growth, especially from China, has also been supporting crude.

A concern for the crude bull should be rising U.S production, which is on the verge of breaking through +10m bpd.

Gold prices have edged down ahead of the U.S open after hitting their four- month high, as the U.S dollar recovers from its overnight lows. Also providing pressure are some technical indicators that point to a short-term correction. Spot gold has fallen -0.4% to +$1,312.35 an ounce.

Note: The 'yellow' metal earlier hit +$1,321.33.

3. U.S yields back up

U.S Treasury prices have weakened in the past 24-hours as a wave of short-term Treasury bill supply is met with declines in prices for German Bunds and U.K Gilts.

Tuesday, U.S 10-year product backed up +6 bps to +2.465%, its biggest one-day jump in nearly a month. Investors will look to today's FOMC December minutes for guidance.

Note: The Fed is expected to offer more details on policy makers' outlook for 2018.In December, officials voted to raise their benchmark federal-funds rate by +25 bps to a range between +1.25% and +1.5%, and penciled in three quarter-point rate increases for 2018.

In Europe, yields have been rallying amid concerns that the strong EUR (€1.2041) may slow the European Central Bank (ECB) from winding down easy money policies, which could lead to a pickup in inflation.

Also providing pressure to sovereign yields is supply – this week, some corporate bonds and sovereign issuers (Ireland and Belgium come to the market) are in play and fixed income dealers have been making room to take down 'new' product by selling some benchmarks.

In Germany, the 10-year Bund yield has decreased -1 bps to +0.46%, while in the U.K, the 10-year Gilt yield has dipped -2 bps to +1.267%.

4. U.S dollar makes a small recovery

The USD is trying to recover some of its recent losses against the major pairs.

The EUR/USD (€1.2038) continues to trade in a tight holiday range, unable to penetrate the psychological €1.21 handle despite the ECB's Nowotny suggesting that the central bank "may end its QE operations in 2018 should the economy stay strong."

Note: The EUR bull continues to preach that the single unit has the potential to test the pivotal €1.24 area in H1.

In Scandinavia, both the SEK (€9.8300) and NOK (€9.7532) currencies are trading a tad firmer outright as Nordic central banks may now be in a position to bring forward their own tightening approach.

Elsewhere, Asian currencies continue to exhibit some strength into this New Year. THB (+0.48% to $32.24) has hit its strongest level since April 2015; PBoC set yuan (¥6.4920) at strongest level since May 2016.

5. U.K December construction PMI falls

U.K data this morning showed that the Purchasing Managers' Index (PMI) for construction fell to 52.2 in December, from 53.1 in November.

Digging deeper, the details of the survey showed new orders rising to a seven-month high and job creation the strongest since June.

The pounds reaction (£1.3562) is somewhat muted as investors remain relatively upbeat about the prospects for an improving U.K economy.

Note: The BoE is expected to keep its benchmark interest rate steady in Q1. The outlook for policy for the rest of 2018 will depend heavily on progress in the U.K's negotiations to withdraw from the E.U. The BoE raised its benchmark rate for the first time in a decade in November to +0.5% to keep a lid on accelerating inflation. The pickup in price growth last year was mostly fuelled by a weak pound.