Sample Category Title

FOMC Minutes Eyed as Dollar Stages Small Rebound

- Will Fed Minutes Have Same Impact Ahead of Powell Appointment?

- GBPUSD Comes Off Highs After Second Weaker UK PMI;

- Bitcoin Unusually Stable Possibly Signalling Cautious Sentiment.

Will Fed Minutes Have Same Impact Ahead of Powell Appointment?

It's been a relatively quiet start to the new year in financial markets but with a number of notable economic events lined up over the coming days, things may start to pick up.

We have a number of key pieces of economic data being released over the next few days, most notably the jobs report on Friday, while the minutes from the December Federal Reserve meeting will also be picked apart later on today. It will be interesting to see how traders respond to the minutes given next month's change of leadership and the impact this could have on policy direction going forward.

While Jerome Powell is widely regarded as representing continuity within the Fed and is perceived to be slightly more hawkish than current Chair Janet Yellen, the dollar has come under renewed pressure over the last few weeks and only shorter term yields rose last year, despite the central bank raising interest rates three times and signalling three more in 2018. It will be interesting to see how worries some policy makers are becoming about the lack of inflation and what impact investors see this having on the rate path.

While the bulk of the economic releases will come over the next couple of days, we will get the ISM manufacturing PMI today, which is expected to fall slightly to 58.1. While we are seeing a small rebound in the greenback today, given the negative bias that appears to be building here, I wonder how vulnerable it will be once again to a weaker December reading.

GBPUSD Comes Off Highs After Second Weaker UK PMI

The pound is coming off its highs against the dollar this morning, having hit 1.36 in the last couple of days for the first time since September. While this has primarily been driven by what currently appears to be a dead cat bounce in the dollar, the softer construction PMI for the UK this morning – coming after an also soft manufacturing PMI on Tuesday – is likely not helping the pair as it closes in on post-Brexit referendum highs.

Bitcoin Unusually Stable Possibly Signalling Cautious Sentiment

It's been a rather timid session for Bitcoin so far today, which is very unusual for the cryptocurrency. Bitcoin started the session on the front foot but has struggled to hold onto its gains, a possible result of the pre-holiday season sell-off which may have weakened sentiment towards it from a speculator standpoint. This is not necessarily a bad thing for Bitcoin or the rest of the cryptocurrency market.

Bitcoin has consolidated since the sell-off, albeit while maintaining far more volatility than most other instruments and this festive period hangover may continue if people fear another sharp move lower. I think we're in for another wild year when it comes to Bitcoin and while prices could easily surpass last year's highs and possibly by a substantial amount, the sell-off was a reminder that the downside can be as, or more, aggressive that the upside which may in the near term lead to more gradual and cautious rallies.

DAX30 Equidistant Channel is Trapping the Price

As the EUR continues its strength against the USD, this may not be good for unhedged exporters on the Dax30 and future earnings. Yesterday we saw a continuation of the selling, but it has since then retraced. Commodities prices continue to increase, but this has only a minor bearing on the Dax30.

Nonetheless, the PMI Manufacturing numbers from Germany are showing significant expansion. Technically, at this point, the DAX30 is capped at resistance within the POC 12940-12950. However if the price breaks above POC it, we could see the POC2 12995-13028. Pay attention as the price might reject within any of the POC zones. Targets are 12865, 12828 and 12772. To the downside, continuation is possible on a breakout below 12772 towards 12678.

However if the price breaks 13028, this could completely negate the bearish scenario. Targets for the breakout are 13089 and 13163 on a further bullish momentum.

- H3 - Weekly Camarilla Pivot (Weekly Interim Resistance)

- W H4 - Weekly Camarilla Pivot (Strong Weekly Resistance)

- D H4 - Daily Camarilla Pivot (Very Strong Daily Resistance)

- D L3 - Daily Camarilla Pivot (Daily Support)

- D L4 - Daily H4 Camarilla (Very Strong Daily Support)

- PPR - Progressive Polynomial Channel

- POC - Point Of Confluence (The zone where we expect price to react aka entry zone)

Market Update – European Session: German Unemployment Continues To Hit Record Low Levels

Notes/Observations

German Dec Unemployment Claims Rate hits a record low of 5.5%

Asia:

PBOC: skips OMOs for 8th day citing current bank liquidity as relatively high (**Note: reports circulated that PBOC may resume open market operations (OMO) in H2 of Jan)

Survey of analysts expects China to raise money market rates 3 times by 5bps each time during 2018. PBoC expected to make modest increases in money-market rates in 2018 as it aims to keep up the pressure on deleveraging and prevent too much divergence with U.S. policy. Analysts did not forecast any change to the benchmark rate

North Korea Official: Kim Jong Un has given order to open boarder hotline between the Koreas at 06:30GMT to discuss inter-Korean dialogue

Europe:

ECB's Nowotny (Austria): End of is within sight this year if the euro area economy continues to grow strongly

UK reportedly considering joining the Trans Pacific Partnership (TPP) following Brexit

Americas:

President Trump: North Korean Leader Kim Jong Un just stated that the "Nuclear Button is on his desk at all times." Will someone from his depleted and food starved regime please inform him that I too have a Nuclear Button, but it is a much bigger & more powerful one than his, and my Button works!

Sen Hatch (R-UT): plans to retire from the Senate at the end of term (**Note: Former GOP presidential candidate Mitt Romney was said to plan to seek Hatch's seat if Hatch retired; Romney has been a sharp critic of Pres Trump at times)

Economic Data:

(NO) Norway Oct AKU Unemployment Rate: 4.0% v 4.0%e

(TR) Turkey Dec CPI M/M: 0.7% v 0.6%e; Y/Y: 11.9% v 11.9%e; CPI Core Index Y/Y: 12.3% v 12.1% prior

(ES) Spain Dec Net Unemployment M/M: -61.5K v -58.9Ke

(CH) Swiss Dec PMI Manufacturing: 65.2 v 64.5e

(HK) Hong Kong Nov Retail Sales Value Y/Y: 7.5% v 4.2%e; Retail Sales Volume Y/Y: 6.9% v 3.9%e

(DE) Germany Dec Unemployment Change: -29K v -13Ke; Unemployment Claims Rate: 5.5% v 5.5%e (record)

(DE) Germany CPI Brandenburg M/M: 0.6% v 0.4% prior; Y/Y: 1.5% v 1.6% prior

(UK) Dec Construction PMI: 52.2 v 53.0e (3rd month of expansion)

Fixed Income Issuance:

(IE) Ireland Debt Agency (NTMA) opened its book to sell May 2028 IGB bond; guidance seen +3bps to mid-swaps; order book over €10B

(ID) Indonesia sold total IDR25.5T vs.IDR17.0T target in 5-year, 10-year and 20-year bonds

(IN) India sold total INR140B vs. INR140B indicated in 3-month, 6-month and 12-month bills

SPEAKERS/FIXED INCOME/FX/COMMODITIES/ERRATUM

Equities

Indices [Stoxx600 +0.3% at 389.4 , FTSE flat at 7648 , DAX +0.4% at 12920, CAC-40 +0.2% at 5299 , IBEX-35 +0.2% at 10097, FTSE MIB -0.1% at 21812 , SMI +0.4% at 9417, S&P 500 Futures +0.2%]

Market Focal Points/Key Themes: European Indices trade higher across the board following on from the momentum seen in Wallstreet overnight. The Dax and Cac lead the gainers recovering from declines seen yesterday, aided by a slight pullback in the Euro. In the UK the retail sector outperforms after Next reported Q4 ahead of expectations as well as lifting its full year outlook. Next shares trade sharply higher, with M&S, Boohoo and Asos all trading up in sympathy. Plus500 also outperforms after guiding full year results ahead of consensus. In the healthcare space Addex Therapeutics trades over 15% higher after a partnership with Indivior, while Novartis is slightly higher after Kisqali received FDA breakthrough therapy designation.

Equities

Consumer Discretionary [Next [NXT.UK] +7% (Q4 update), M&S [MKS.UK] +1.5% (Sympathy with Next), Staffline [STAF.UK] -2% (Trading update), Ryanair [RYA.UK] +1.1% (Dec metrics)]

Financials [Plus500 [PLUS.UK] +15% (Trading update)]

Healthcare [Addex Therapeutics [ADXN.CH] +16% (partnership with Indivior), Basilea [BSLN.CH] +4% (Start of phase 1 study)]

Speakers

UK Trade Sec Fox: Would be foolish not to look at all trade options; joining TPP was not a priority. Wanted continuity of EU trade deals following Brexit

Sweden Fin Min Andersson reiterated govt view of not expecting any major drama in housing prices but did scope for stimulus in event of any crisis

Czech Central Bank Dec Minutes: Vote was not unanimous to keep policy steady; Most MPC members saw it more appropriate to raise rates gradually. Members Hampl and Benda voted for rate hike. Timing for further steps were conditional on evolution of all key macroeconomic variables including the CZK currency rate. Would be useful to have new forecasts before making further rate hike decision

China PBoC said top have held meeting to regulate Bitcoin mining power use

Currencies

USD trying to recover some of its recent losses against the major pairs.

EUR/USD unable to break above the 1.21 handle despite ECB's Nowotny suggesting the ECB may end its QE operations in 2018 should the economy stay strong. Dealers were turing optimistic that the current EUR rally could test the pivotal 1.24 area.

Both the SEK and NOK currencies were firmer as Nordic central banks could bring forward their own tightening approach

Asian currencies continue to exhibit strength in the new year. Thai Baht (THB) hits strongest level since April 2015; PBoC set yuan (CNY) at strongest since May 2016; Taiwan Dollar (TWD) continues to trade at over 4-year highs

Fixed Income

Bund Futures trade up 6 ticks at 161.40 bouncing off a low of 161.20 as the euro tests a 3-year high. A continued move below 161.00 low targets 160.71 then 160.45, with a continued rebound targeting 161.86.

Gilt futures trade at 124.37 down 23 ticks off the session lows. Continued upside eyeing 124.75 then 125.25. Downside targets include 123.25 then 122.75.

Wednesday's liquidity report showed Tuesday's excess liquidity rose to €1.789T from €1.758T prior. Use of the marginal lending facility rose to €317M from €299M prior.

Corporate issuance saw a total $7B come to market, headlined by Berkshire Energy, GM financial, Santander and BNP.

Looking Ahead

(ZA) South Africa Dec Naamsa Vehicle Sales Y/Y: No est v 7.2% prior

(RO) Romania Dec International Reserves: No est v $36.7B prior

05.30 (UK) Weekly John Lewis LFL sales data

06:00 (CZ) Czech Republic to sell bonds - 06:45 (US) Daily Libor Fixing

07:00 (US) MBA Mortgage Applications w/e Dec 29th: No est v -4.9% prior (2-weeks worth of data)

07:00 (CL) Chile Nov Retail Sales Y/Y: 3.6%e v 3.7% prior; Commercial Activity Y/Y: No est v 6.0% prior

(US) Dec Wards Total Vehicle Sales: 17.35Me v 17.40M prior; Domestic Vehicle Sales: 13.38Me v 13.46M prior

07:45 (US) Weekly Goldman Economist Chain Store Sales

08:00 (PL) Poland Dec Preliminary CPI: M/M: 0.3%e v 0.5% prior; Y/Y: 2.1%e v 2.5% prior

08:00 (CZ) Czech Dec Budget Balance (CZK): No est v -11.6B prior

08:00 (SG) Singapore Dec Purchasing Managers Index (PMI): No est v 52.9 prior; Electronic Sector Index: No est v 53.5 prior

08:05 (UK) Baltic Dry Bulk Index

08:30 (BR) Weekly Brazil currency flow data

08:55 (US) Weekly Redbook Sales

09:00 (EU) Weekly ECB Forex Reserves

09:30 (BR) Brazil Weekly Currency Flow data

10:00 (US) Dec ISM Manufacturing: 58.2e v 58.2 prior; Prices Paid: 64.5e v 65.5 prior

10:00 (US) Nov Construction Spending M/M: 0.5%e v 1.4% prior

10:00 (DK) Denmark Dec Foreign Reserves (DKK): 464.2Be v 464.2B prior

10:00 (CO) Colombia Nov Exports: $3.2Be v $3.1B prior

10:00 (MX) Mexico weekly International Reserves data

14:00 (US) FOMC Dec 13th Meeting Minutes

16:30 (US) Weekly API Oil Inventories: Crude

Technical Outlook: WTI OIL – Bulls Eye Fibo Targets At $60.97 And $61.62

WTI oil remains steady on Wednesday following strong rally in past three days which peaked at $60.72 on Tuesday.

Oil prices were boosted by recent situation in Iran and remain well supported by global efforts to tighten oil market by cutting production.

Oil is riding on extended third wave of five-wave cycle from $55.81 (07 Dec trough), pressuring cracked FE 161.8% barrier at $60.56, for extension towards targets at $60.97 and $61.62 (FE 176.4% and FE 200% respectively).

Bulls were so far ignoring negative signs from overbought daily studies however, corrective action could be anticipated in the near-term.

Rising 10SMA ($59.24) and previous top of 24 Nov ($59.02) are expected to ideally contain and keep bulls intact.

Res: 60.56, 60.97, 61.62, 62.71

Sup: 60.28, 60.00, 59.24, 59.02

US Dollar Index Faces Bullish Correction Following 10-Day Bearish Run

The US dollar index continues to hold within negative territory as it posted its tenth bearish day in a row on Tuesday. The price has plummeted more than 2% since December 2 and challenged a new more than 3-month low at 91.44.

In the short-term timeframe, the index is trading slightly above the aforementioned level, however, a break below it could expose the price towards the 90.95 support level, which is standing since September 8. Conversely, a retracement on the upside could open the door for the next resistance level at 92.40.

Remaining on the short-term timeframe the Relative Strength Index (RSI) is moving within the oversold zone but is close to exiting it as approaches the 30 level. As a result, the strong bearish momentum has weakened. The MACD oscillator has also lost some of its strong downside momentum and is holding near the trigger line, ready to post a bullish crossover in the bearish area. The three simple moving averages (50, 100 and 200) are moving southwards endorsing the scenario for further fall in the next sessions. However, traders need to be ready for a possible upwards correction before the potential resumption of a downward movement.

The past year marked the worst year for the US dollar in more than a decade with the dollar index falling over 10%. The last time it faced such difficult times was in 2003 when it lost 14.6% of its value.

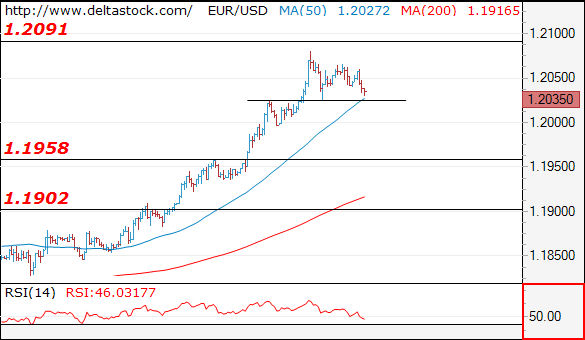

Forex Technical Analysis: EUR/USD, USD/JPY, GBP/USD

EUR/USD

Current level - 1.2035

Yesterday's test at 1.2080 should be enough for a corrective pullback and my outlook is bearish, for a break through 1.2025 minor support, towards 1.1960 area.

| Resistance | Support | ||

| intraday | intraweek | intraday | intraweek |

| 1.2050 | 1.2090 | 1.1960 | 1.1910 |

| 1.2090 | 1.2240 | 1.1910 | 1.1715 |

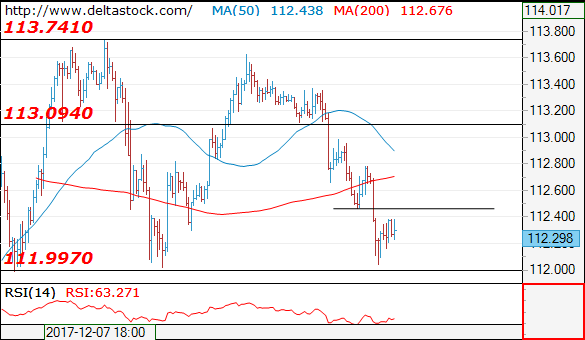

USD/JPY

Current level - 112.29

With yesterday's slide to 112.00 my outlook is already counter-trend, for a rise through 112.45 hurdle, towards 113.09 area.

| Resistance | Support | ||

| intraday | intraweek | intraday | intraweek |

| 112.45 | 113.09 | 112.00 | 111.00 |

| 113.09 | 113.65 | 111.00 | 111.00 |

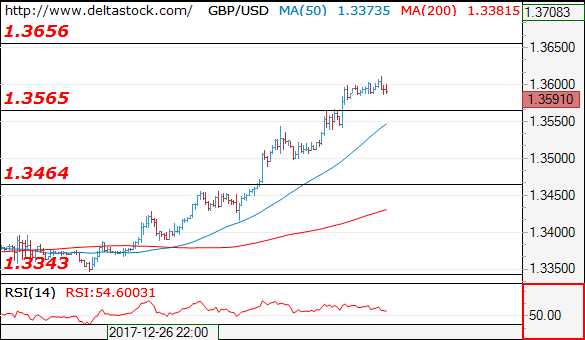

GBP/USD

Current level - 1.3591

Initial intraday support lies at 1.3565 and a break below will signal a more significant reversal, towards 1.3460 zone.

| Resistance | Support | ||

| intraday | intraweek | intraday | intraweek |

| 1.3660 | 1.3660 | 1.3565 | 1.3460 |

| 1.3660 | 1.3660 | 1.3460 | 1.3300 |

Euro Rally Stalls, German Unemployment Rolls Plunge

The euro has paused on Wednesday, after four consecutive winning sessions. Currently, EUR/USD is trading at 1.2031, down 0.23% on the day. On the release front, German Unemployment Change in December declined by 29,000, well below the estimate of 13,000. This marked the second-highest decline in 2017. In the US, ISM Manufacturing PMI is expected to inch lower to 58.1 points. Today’s key event is the release of the Fed minutes from the December meeting. On Thursday, Germany and the eurozone release Services PMIs. The US will publish ADP Nonfarm payrolls and unemployment claims.

German indicators for the fourth quarter continue to point upwards. December inflation accelerated to 0.6%, edging above the forecast of 0.5%. The strong gain matched the February reading, equaling the strongest gain recorded in 2017. Unemployment rolls continue to fall, as the labor market continues to remain tight in a robust economy. The numbers are all the more impressive as the political landscape remains uncertain, following inconclusive elections in September. President Angela Merkel is now eyeing the Social Democrats as a coalition partner, but negotiations are moving at a slow pace.

The Federal Reserve will be in the spotlight on Wednesday, with the release of the minutes of the December policy meeting. At that meeting, the Fed raised rates by 25 basis points, to a range between 1.25-1.50%. The hike marks a vote of confidence in the US economy, and if the minutes are hawkish, the US dollar could gain ground. The economy is expanding at an impressive clip of above 3 percent. If this pace continues, the Fed could raise rates up to four times in 2018. Currently, the CME Group has priced in a January rate hike at 98.5%. Despite the rosy economic conditions, inflation has been chronically soft, well below the Fed target of 2 percent. Outgoing Fed Chair Janet Yellen and other FOMC members have said that they expect that the strong labor market will push up wages and trigger higher inflation, but this is yet to happen.

Technical Outlook: AUDUSD – Bulls Focus Pivotal 0.7886/97 Barriers After Emerging Above Thick Daily Cloud

The Aussie dollar remains well supported and looks for extension strong rally in past three weeks.

Bulls pressure immediate barrier at 0.7859 (falling weekly 200SMA) which lies ahead of next pivotal resistances at 0.7886/0.7897 (Fibo 61.8% of 0.8124/0.7499 descend / 08 Oct lower top).

Techs remain in full bullish setup and favor further advance, however, bulls could be interrupted for extended consolidations under 0.7886/97 pivots with deeper dips not ruled out, as daily studies are strongly overbought.

Broken top of thick daily cloud marks initial support at 0.7816 (cracked on brief dip to 0.7805 today) which should ideally hold, with deeper dips expected to find support at 0.7777 (100SMA) and 0.7747 (rising daily Tenkan-sen) before bulls resume.

Res: 0.7844, 0.7859, 0.7886, 0.7897

Sup: 0.7816, 0.7805, 0.7777, 0.7747

Technical Outlook: USDJPY Consolidates Above Strong 112 Support, Near-Term Bias Remains Bearish

The pair is consolidating above important support at 112.00 (15 Dec low) on Tuesday after steep bearish acceleration in past three days found footstep here.

Support is reinforced by Fibo 61.8% of 110.83/113.74 rally and 100SMA and may hold bears for some time for extended consolidation.

Broken sideways-moving 30SMA offers solid resistance at 112.53, which is expected to ideally cap upticks, with the base of thickening daily cloud, laying at this zone and reinforcing resistance.

Sustained break below 112.00 handle is needed to complete failure swing pattern on daily chart and spark fresh weakness towards 200SMA at 111.64 and Fibo 76.4% of 110.83/113.74 at 111.52.

Res: 112.39, 112.53, 112.79, 112.84

Sup: 112.17, 112.00, 111.64, 111.52

Technical Outlook: GBPUSD – Shallow Correction Likely To Precede Final Push Towards Key 1.3655 Barrier

Cable cracked psychological barrier at 1.3600 on Tuesday and hit new multi-month high at 1.3612 in extension of steep bullish acceleration in past four days.

Subsequent easing was so far shallow, however, overbought daily studies warn of deeper correction.

Rising hourly cloud (spanned between 1.3533 and 1.3497) continues to underpin and is expected to ideally contain extended dips.

Bulls eye post-Brexit recovery high at 1.3655 (20Sep high and the highest in 2017), above which to signal continuation of broader recovery from post-Brexit fall low at 1.1930 towards next target at 1.3837 (Fibo 61.8% of 1.5016/1.1930 fall).

Construction PMI data are the sole release from the UK today (52.8 f/c in Dec vs 53.1 previous month) with US economic indicators due later today, being focused.

Res: 1.3612, 1.3643, 1.3655, 1.3701

Sup: 1.3588, 1.3549, 1.3533, 1.3497