Sample Category Title

AUDUSD In Bullish Phase Reaching Highest Level In Over 2-Months

AUDUSD extended its bullish run yesterday but is currently taking a pause after hitting 0.7844, its highest level since October 20.

AUDUSD has room to extend towards 0.7900 since prices crossed above the 200-day moving average. The market is currently testing the key 0.7800 level. A daily close above it would help keep momentum to the upside.

However, the stochastic and RSI indicators are overbought, which suggests that prices could risk pulling back.

A drop back below the 200-day MA (around 0.7690) would indicate that the bullish phase has ended and AUDUSD risks dropping down to 0.7500. This is expected to provide strong support though. Any move lower would see a resumption of the downtrend from the 0.8124 peak.

In the meantime, the short-term bullish phase is still in progress. A sustained move above 0.7800 could see the rally continue, with dips supported at 0.7690.

Currencies: EUR/USD Nears 2017 Top

Sunrise Market Commentary

- Rates: Bear steepening in opening session of the year

Global core bonds started the New Year on a weak footing with bear steepening of both the US and German yield curves. Trading will be mainly guided by the US eco calendar today with US manufacturing ISM and FOMC Minutes. We hold our short positions in both the US Note future and the Bund even if FOMC Minutes give increased attention to low inflation. - Currencies: EUR/USD nears 2017 top

Recently, the dollar suffered. Ongoing strong global growth suggested that other CB's, including the ECB, might come closer to policy normalization. Interest rate differentials narrowed in favour of the euro. Today's US events (ISM/ Fed Minutes) probably won't change the global context. The EUR/USD might slow ahead of Friday's payrolls

The Sunrise Headlines

- US stock markets eked out gains on the first trading day of the new year. The Nasdaq significantly outperformed, closing above 7000 for the first time ever. Asian risk sentiment is positive as well overnight with Japan closed.

- The ECB may end its stimulus programme this year if the EMU economy continues to grow strongly, ECB Nowotny said. He also warned of European stock market bubble risks.

- Britain has held informal talks about joining the Trans-Pacific Partnership. The proposal would make the UK the first member that does not border the Pacific Ocean or the South China Sea.

- Brent crude rose above $67/barrel for the first time since 2015 yesterday, supported by tensions in Iran. Separate data showed a record net long position has been accumulated by hedge funds and other money managers in the five biggest futures and options contracts covering crude, gasoline and heating oil.

- Donald Trump has embarked on a foreign policy offensive on his return to the White House, piling pressure on Iran, Pakistan, North Korea and the Palestinians as he switches his focus beyond tax reform and other domestic priorities.

- South Korea can "in principle" consider measures to boost investment overseas if won rises sharply, a government official, who declined to be named on internal policy, said by phone.

- Today's eco calendar contains German unemployment data, the UK construction PMI, the US manufacturing ISM and FOMC Minutes

Currencies: EUR/USD Nears 2017 Top

EUR/USD nears 2017 top

Overnight, the dollar shows no clear trend even as risk sentiment stays positive. USD/JPY holds in the lower half of the 112 big figure. EUR/USD hovers in the mid 1.20 area. Today, German labour data are expected to improve further with the unemployment rate declining to 5.5%. The US manufacturing ISM is expected unchanged at a high 58.2. (FX) traders will keep an eye at the price indicators of the report. This evening, the minutes of last month's FOMC meeting will be published. Markets will also look for the Fed's assessment on ongoing low inflation. At least, it didn't cause a major change to the 2018 Fed dot plot.

Recently, the dollar suffered as the global recovery could force other major CB's (including ECB) to join policy normalisation. Today's data probably won't change market sentiment. That said, good US data might slow the recent USD decline ahead of Friday's payrolls. It also won't be that easy for EUR/USD to set new cycle high without really high profile news. At the same time, higher core yields and/or a risk-on sentiment as such were not enough to support the dollar of late.

Global picture USD: The outcome of the Dec Fed & ECB meetings didn't provide directional guidance for EUR/USD. A narrowing in the (LT) interest rate differentials finally propelled EUR/USD to the topside of the 1.1554/1.2090 range end 2017. A sustained break would improve the ST picture. For now we don't preposition for such a break. Quite some good news on the euro/bad news on the dollar should be discounted at current levels. Price data remain in focus.

EUR/GBP tried to regain the 0.89 mark yesterday on a softer than expected manufacturing PMI, but the attempt failed. Today, only the UK construction PMI is on the agenda (expected little changed at 53). More technical trading might be on the cards. A slowdown of the EUR/USD rally might cap the topside of EUR/GBP short-term.

Global picture EUR/GBP: The EUR/GBP decline stalled even as the EU agreed to start the next stage of Brexit negotiations. The pair settled in a 0.8760/0.8960 consolidation range. Recent UK data were mixed. We don't expect the BoE to raise interest rates anytime soon. The EUR/GBP 0.8700/60 support looks solid. Ongoing euro strength or soft UK data might keep EUR/GBP 0.90 on the radar further down the road. We keep a EUR/GBP buyon- dips approach in case of return action to the 0.87 area.

EUR/USD near 1.2092 range top

FOMC Minutes Under The Spotlight, Will Dollar Bulls Attack

Investors kicked off 2018 on a positive note sending U.S. stocks to fresh highs on the first trading day. The optimistic approach on day one was supported by encouraging economic data from China, where the Manufacturing Purchasing Managers' Index for December beat expectations by coming in at 51.5 versus expectations of 50.6. Europe was also a bright spot, as factories reported their most robust monthly performance since the creation of the single currency. Eurozone PMI hit 60.6 in December indicating that growth is likely to remain healthy in 2018.

The missing ingredient for global economic expansion throughout 2017 has been inflation, but with consumerdemand increasing, unemployment dropping, and commodity prices surging, it's difficult not to see inflation returning in 2018.

One of the most debated topics last year was the flattening yield curve in the U.S. In December the U.S. 10 Year / 2 Year Treasury spread fell to 50 basis points, a level last seen in 2007- signaling that a recession is around the corner. However, when we look at the economic performance in the U.S. and on a global scale, there isn't any indication of one occurring soon.

Looking forward, I believe Treasury Bond Yields will be a must watch indicator for how the U.S. stocks and the dollar perform in 2018. If the Phillips curve “the inverse relationship between the level of unemployment and the rate of inflation” finally wakes up after being dead for the last couple of years, the yield curve should start steepening. The dollar's performance which opened the New Yearon a downward trajectory, will depend on the magnitude of change in the yield curve. A rise in U.S. 10-Treasury yields towards 3% - 3.5% this year, will likely reverse some of the dollar's 2017 losses, however a steeper move will have negative consequences on stocks, with the probability of 5%-10% pullback increasingly likely.

Today's FOMC minutes will provide some assessment on the U.S. inflation outlook. If the central bank reveals concerns over upside inflation expectations due to fiscal policies and an improved labour market, investors are likely to cover some of the dollars short positions. This should be reflected in interest rate expectations for March which currently indicate a probability of 56.3% rate hike in March, according to CME's FedWatch.

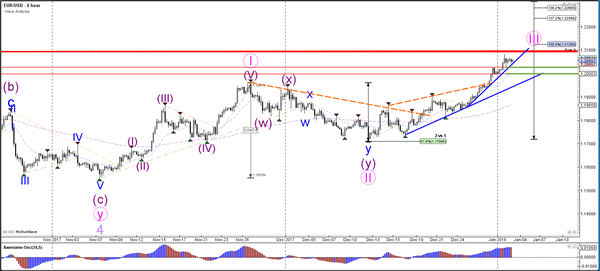

Daily Wave Analysis: EUR/USD Develops Bullish Wave 3 Momentum If Previous Top Breaks

Currency pair EUR/USD

The EUR/USD uptrend broke above the 1.20 round level resistance which now could become used as a potential support zone (green lines). There are also two support trend lines that could keep price from falling. The bearish wave count from yesterday has been invalidated and a bullish wave 3 (pink) is becoming more likely, but a break above the previous top is still needed (red).

The EUR/USD stopped at the previous top (red) and is building a correction. The sideways movement could be part of a wave 4 (blue) which typically retraces to a shallower Fibonacci level.

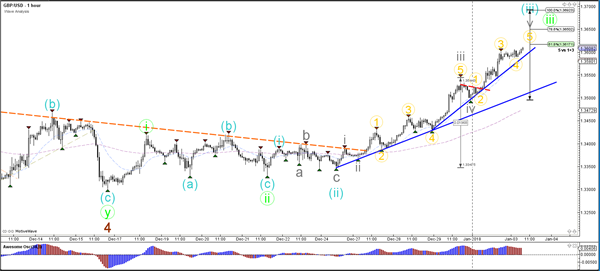

Currency pair GBP/USD

The GBP/USD bullish momentum keeps pushing higher and is moving towards the Fibonacci targets of waves 5, which seems to be part of a wave C (green).

The GBP/USD completed a wave 4 (grey) and is now building 5 internal wave (gold) within wave 5 (grey) of wave 3 (blue).

Currency pair USD/JPY

The USD/JPY bearish price action has broken below a larger support trend line (dotted blue), which could be part of a larger bearish wave C (purple) correction within wave 2 or B (light purple).

The USD/JPY is building another bear flag chart pattern (blue lines) and a bearish break of the flag could see price continue to fall towards the Fib targets of wave 5.

EUR/USD Traded Above 1.2050

Market movers today

NEW RESEARCH WEBSITE: We have launched our new research website with all our research across asset classes and countries.

In the US, we get the FOMC minutes from the December meeting and we will look for clues as to whether other members other than Charles Evans and Neel Kashkari came close to dissenting. ISM manufacturing is also in the spot light .

In Denmark, we get FX reserves data for December. In Norway, we get the labour force survey for October but remember the more stable labour market statistics from NAV is more important .

Finally, Mi fid2 is officially new regulation in Europe from today. It could potentially mean less market liquidity in the next couple of days as traders and asset managers adapt to the new regulations and rules in real-t ime.

Selected market news

European bond markets came under pressure on the first trading day of the year and the yield on 10Y Bund rose 4bp to 0.46% - the highest level since October 2017. The combination of generally strong PMI data indicating that inflation eventually will pick-up and comments over the weekend from ECB's Coeure weighed on the market . Coeure said that unless inflation disappointed there's a " reasonable chance" the central bank's extension of QE in October last for nine months could be the final extension. Especially, the lat ter weighed on periphery bond markets together with markets st ill wary ahead of the Italian March general elect ion.

The FI sell-off also comes ahead of a busy bond supply calendar in Q1 and especially here in January, where a number of syndications are due and the ordinary auction calendar is full. Yesterday, the Irish Debt Management Office said thatithas mandated six banks including Danske Bank as joint lead managers for a forthcoming new 10-year bond that – subject to market conditions – is due to today. The Coeure comments and the recent pick-up in long-term inflation expectations, where the 5y5y EUR inflation swap is at 1.74% which is close to the highest level in a year, underline that the risk of further pressure on European FI markets here in January should not be neglected. It seems that the global ‘reflation trade' is once again back in focus.

The factors that pushed yields higher in the Euro zone yesterday also added to the strength of the Euro and EUR/USD traded above 1.2050 – the highest level in three years. The cross is not only supported by EUR strength but also by a general dollar weakness seen here in 2018. European stocks had a hard time following the positive Asian sentiment yesterday as the strong Euro weighed on sentiment . US stocks on the other hand had a strong opening day with tech stocks taking the lead as Nasdaq rose 1.5%. In respect of financial market s preparing for today's Mifid2 launch Bloomberg reported that turn-over was lower than usual yesterday. We expect that any potential market impact on liquidity will be temporary.

Market Update – Asian Session: Upcoming FOMC Minutes In Focus

Headlines/Economic Data

General Trend:

Asian currencies continue to exhibit strength in the new year. Thai Baht (THB) hits strongest level since April 2015; PBoC set yuan (CNY) at strongest since May 2016; Taiwan Dollar (TWD) continues to trade at over 4-year highs

Japan

Nikkei 225 closed for holiday

Looking ahead: Equity markets in Japan resume trading on Thursday, following 3-day holiday; Japan Dec final manufacturing PMI to be released

Korea

Kospi opened +0.2%

Semiconductors track earlier gains in the US: Samsung Electronics +1.5%, Hynix +1.4%

Posco Steel +5%, Hyundai Steel +2.6% (US Dow Jones Iron & Steel index rose 4.6% on Tuesday; positive broker commentary)

073240.KR (Kumho Tire) +11%: KDB set up task forces to deal with Kumho Tire restructuring and M&A

LG Display (034220.KR) +3%: To begin supplying OLED panels for over 15M new iPhone units which are expected to be unveiled in H2, says a press report.

009540.KR Hyundai Heavy +9.5% (Issued FY18 sales guidance)**Reminder: On Dec 27, 2017 the company’s share price declined by over 28%, as it announced a plan to raise KRW1.29T in capital.

(KR) Bank of Korea (BOK) Gov Lee: Reiterates stance of closely monitoring FX movements

(KR) Korean press comments on rising number of mortgages in South Korea despite govt's measures to slow the housing market

(KR) Bank of Korea (BoK) sells KRW2.4T in 2-year monetary stabilization bonds: yield 2.06%

(KR) Moody's: domestic and global credit impact of Korea conflict would depend on duration and severity

(KR) North Korea Official: Kim Jong Un has given order to open boarder hotline between the Koreas at 06:30GMT to discuss inter-Korean dialogue

(KR) South Korea Q4 Foreign Direct Investment (FDI) y/y: +49.8% v -9.0% prior; 2017 FDI record high

China/Hong Kong

Hang Seng opened +0.5%, Shanghai Composite flat

Hang Seng Services Index +1.7% (strength in airlines), Consumer Goods +1.5% (automakers gain), Materials +1.3%, Information Technology +1.2%; Telecom -1% (China Mobile -1.4%), Utilities -0.1%

(CN) China researcher suggests China should allow yuan to fall this year; sees 2018 GDP at 6.5% -21st Herald

(CN) PBOC may resume open market operations (OMO) in H2 of Jan - Chinese press

(CN) China Securities Times Op Ed: PBOC should stabilize yuan fx rate

(CN) Survey of analysts expects China to raise money market rates 3 times - financial press

(CN) China PBoC: Skips OMO for 8th straight session; Net drains CNY90B v CNY290B prior

USD/CNY (CN) China PBoC sets yuan reference rate at 6.4920 v 6.5079 prior (strongest setting since May 2016)

(HK) Overnight HK$ HIBOR -66bps (most since Nov 1st); 1-week HK$ HIBOR -47bps (most since Oct 2008); 1-month HK$ HIBOR -7bps (most since Jan 2009)

Looking ahead: China Dec Caixin Services PMI to be released on Thursday

Australia/New Zealand

ASX 200 opened +0.2%; closed: +0.2%

ASX 200 Resources Index +1.4%, Energy +0.6%;Financials -0.2, Consumer Discretionary -0.5%

MWY.AU Guides FY18 H1 earnings to be lower due to delayed export shipments; -3%

YOW.AU Cuts FY18 Rev to +17% y/y (prior 55%); Names Mark Schuessler new CEO; -33%

Other Asia

(PH) Philippines Central Bank (BSP): May tweak monetary stance if there is a 2nd CPI effect; To restore 28-day term deposits in due time

North America

US equities ended higher: Dow +0.4%, S&P500 +0.8%, Nasdaq +1.5%, Russell 2000 +0.9%

S&P500 Energy Sector +1.6%, Consumer Discretionary +1.5%

SEMI: Sees 2018 global fab equipment spending $63B, +11% y/y; 2017 global fab equipment spending $57B, +41% y/y (record high)

(US) Sen Hatch (R-UT): plans to retire from the Senate at the end of term; Hatch was first elected to the Senate from Utah in 1976

Looking ahead: US Dec ISM manufacturing PMI to be released on Wednesday, along with Dec FOMC Minutes and Weekly API Crude Oil Inventories.

Europe

(UK) UK reportedly considering joining the Trans Pacific Partnership (TPP) following Brexit - FT

(EU) ECB's Nowotny (Austria): sees a risk of a European stock market bubble - press interview

Levels as of 01:00ET

Nikkei225 closed, Hang Seng +0.0%; Shanghai Composite +0.5%; ASX200 +0.2%, Kospi +0.3%

Equity Futures: S&P500 +0.1%; Nasdaq100 +0.1%, Dax +0.2%; FTSE100 +0.0%

EUR 1.2066-1.2042; JPY 112.39-112.17; AUD 0.7837-0.7806;NZD 0.7109-0.7073

Feb Gold +0.0% at $1,316/oz; Feb Crude Oil +0.0% at $60.38/brl; Mar Copper -0.5% at $3.26/lb

Aussie Trading Lower In The Asian Session

For the 24 hours to 23:00 GMT, the AUD rose 0.24% against the USD and closed at 0.7828.

LME Copper prices rose 0.3% or $24.0/MT to $7181.0/MT. Aluminium prices rose 0.7% or $14.5/MT to $2256.0/MT.

In the Asian session, at GMT0400, the pair is trading at 0.7811, with the AUD trading 0.22% lower against the USD from yesterday’s close.

The pair is expected to find support at 0.7796, and a fall through could take it to the next support level of 0.7780. The pair is expected to find its first resistance at 0.7836, and a rise through could take it to the next resistance level of 0.7860.

Looking forward, Australia’s AiG performance of services index for December, set to release overnight, would garner significant amount of market attention.

The currency pair is trading below its 20 Hr and 50 Hr moving averages.

Manufacturing Sector Activity Confirmed At A Record High Across The Euro-Zone In December

For the 24 hours to 23:00 GMT, the EUR rose 0.42% against the USD and closed at 1.2058, following upbeat economic data across the Euro-zone which suggested that the upturn in the manufacturing sector would continue to surge in the new year.

The Euro-zone’s final Markit manufacturing PMI advanced to a record high level of 60.6 in December, confirming the preliminary print. The PMI had registered a level of 60.1 in the previous month.

Separately, activity in Germany’s manufacturing sector jumped as initially estimated to a level of 63.3 in December, expanding at its fastest pace on record and compared to a level of 62.5 in the prior month.

The US Dollar nursed losses against its major peers, as investors turned sceptical about the Federal Reserve’s monetary policy outlook.

On the economic front, the US final Markit manufacturing PMI was revised higher to a level of 55.1 in December, surging at its quickest pace in nearly three years and signalling a solid improvement in the health of the nation’s manufacturing sector. The preliminary figures had indicated an advance to a level of 55.0, compared to a reading of 53.9 in the prior month.

In the Asian session, at GMT0400, the pair is trading at 1.2047, with the EUR trading 0.09% lower against the USD from yesterday’s close.

The pair is expected to find support at 1.2012, and a fall through could take it to the next support level of 1.1976. The pair is expected to find its first resistance at 1.2082, and a rise through could take it to the next resistance level of 1.2116.

Moving ahead, market participants would eye the release of Germany’s unemployment rate data for December, scheduled to release in a few hours. Later in the day, investors will turn their attention to the minutes of the Fed’s December policy meeting as well as the US ISM manufacturing PMI for December and construction spending data for November.

The currency pair is showing convergence with its 20 Hr moving average and trading above its 50 Hr moving averages.

UK’s Manufacturing Sector Growth Came In Weaker-Than-Expected In December

For the 24 hours to 23:00 GMT, the GBP rose 0.58% against the USD and closed at 1.3592.

Macroeconomic data revealed that Britain's Markit manufacturing PMI dropped more-than-expected to a level of 56.3 in December, after recording a four-year high level of 58.2 in the prior month, while markets were expecting for a fall to a level of 57.9.

In the Asian session, at GMT0400, the pair is trading at 1.3596, with the GBP trading marginally higher against the USD from yesterday's close.

The pair is expected to find support at 1.3538, and a fall through could take it to the next support level of 1.3479. The pair is expected to find its first resistance at 1.363, and a rise through could take it to the next resistance level of 1.3663.

Moving ahead, traders would closely monitor UK's Markit construction PMI for December, scheduled to release in a few hours.

The currency pair is trading above its 20 Hr and 50 Hr moving averages.

Japanese Yen Trading On A Weaker Footing This Morning

For the 24 hours to 23:00 GMT, the USD declined 0.37% against the JPY and closed at 112.25.

In the Asian session, at GMT0400, the pair is trading at 112.34, with the USD trading 0.08% higher against the JPY from yesterday’s close.

The pair is expected to find support at 112.02, and a fall through could take it to the next support level of 111.70. The pair is expected to find its first resistance at 112.70, and a rise through could take it to the next resistance level of 113.06.

Going ahead, traders would focus on Japan’s final Nikkei manufacturing PMI for December, set to release overnight.

The currency pair is trading between its 20 Hr and 50 Hr moving averages.