Sample Category Title

CAC Slips as European Stock Markets Start New Year in the Red

European stock markets have started 2018 with losses, and the CAC index is in red territory in the Tuesday session. Currently, the index is at 5278.00, down 0.62% on the day and at its lowest level since late September. On the release front, French Manufacturing PMI improved to 58.8, but this missed the estimate of 59.3 points. Eurozone Manufacturing PMI climbed to 60.6 points, matching the forecast. On Wednesday, the Federal Reserve will publish the minutes of its December meeting.

At the Federal Reserve December meeting, policymakers raised rates by 25 basis points, to a range between 1.25% and 1.50%. The Fed will release the minutes of the meeting on Wednesday, and traders should consider the event a market-mover. The December hike marks a vote of confidence in the US economy, and if the minutes are hawkish, the US dollar could reverse directions and gain ground. If the US economy continues to expand at a clip exceeding 3%, the Fed is expected to raise rates up to four times in 2018. Currently, the CME Group has priced in a January rate hike at 98.5%. Although inflation remains well below the Fed target of 2.0%, outgoing Fed Chair Janet Yellen and other FOMC members have said that they expect that the strong labor market will lead to higher inflation. Although this is yet to materialize, of significance to the markets is the commitment of the Fed to press ahead with rate hikes, despite low inflation.

The French and eurozone economies rebounded in 2017, and inflation, which has chronically been at low levels, also moved higher. Annual average inflation inched up to 1.5% in November, up from 1.4% in October. This marked a multi-year high. In December, in a nod to stronger economic activity in 2017, the ECB raised its forecasts for growth and inflation for the eurozone from this year through to 2019. Still, inflation remains well below the ECB target of around 2.0%, and ECB policymakers are unlikely to announce an end to their stimulus package until inflation moves closer to the 2.0% target.

Copper Pauses its Incline Move after it Posted an Almost 4-Year High

Copper future contract with delivery in March is clearly in an uptrend since December 5, where it turned increasingly bullish following the rebound on 2.9398. The price snapped the 14 winning days, recording a red session on December 28 after it hit a near 4-year high at 3.3175.

In addition, the red metal is still trading comfortably above the 3.2563 support level, however, if the bearish move extends, the aforementioned level could be the first stop. A drop below 3.2563 could drive the price towards the 3.2324 strong support barrier, which overlaps with the 50-day simple moving average as well as with the 23.6% Fibonacci retracement level of the last big up-leg with low at 2.9395 and high at 3.3175.

From the technical point of view, on the 4-hour chart, the parabolic indicator signals for bearish movement along with the momentum indicators. The RSI indicator fell below the overbought zone and is softly sloping to the downside, whilst the MACD oscillator is losing momentum as it declined below its trigger line.

USDJPY Bearish Below 112.48 Level

The U.S dollar has fallen to a three-week trading low against the Japanese yen, as weakness in the greenback drives the pair lower. The USDJPY has fallen below its key 100-day moving average, indicating medium-term weakness, with price-action so far reaching an intraday-low of 112.11. The U.S dollar index has declined even further during the European trading session, falling towards the 91.90 support level. Traders now await the United States market open, with the major macroeconomic release of the day, the U.S Manufacturing PMI for the month of December.

The USDJPY pair remains strongly bearish while trading below the 112.48 level, further losses towards 112.03 and 111.60 appear likely.

Should price-action move above the 112.48 level, buyers will likely test towards the 112.70 level. Extended weekly resistance is found at the 113.10 level.

GBPUSD Further Bullish Above 1.3551 Level

The British pound has moved to its highest trading level against the greenback in four-weeks during the European trading session, hitting 1.3566. The GBPUSD pair has now pulled back marginally after the United Kingdom's Manufacturing PMI for the month of December came in weaker than expected. Price-action is currently testing the former monthly-high at 1.3551, which is being used as a major pivot point for intraday traders. Moving into the U.S trading session, financial markets will look to the rapid decline in the U.S dollar index, and the release of the United States Manufacturing PMI for December.

The GBPUSD pair is strongly bullish while trading above the 1.3551 technical level, buyers will likely target the 1.3610 and 1.3656 upside levels.

Should price-action on the GBPUSD pair fall below the 1.3551 level, strong intraday technical support is found at the 1.3500 and 1.3468 levels.

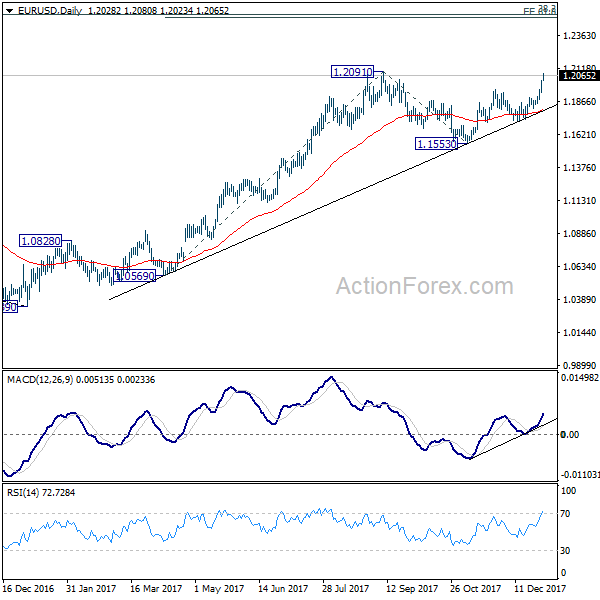

Dollar Selloff Continues, EUR/USD to Take on 1.2091 Resistance

Dollar's broad based selloff continues as 2018 starts. In particular, EUR/USD reaches as high as 1.2080 and is set to take on 1.2091 key resistance. USD/JPY is holding above 112.02 support for the moment, but it looks vulnerable. Among the currencies, Euro is so far trading as the strongest one, followed by Sterling. But Swiss Franc clearly lags behind its European rivals.

UK PMI manufacturing dropped more than expected

UK PMI manufacturing dropped to 56.3 in December, down from 58.2 and missed expectation of 57.9. Markit Director Rob Dobson said in the release that "expansion remained comfortably above long-term trend rates." And, "the sector has therefore broadly maintained its solid boost to broader economic expansion in the fourth quarter." Besides, "the outlook is also reasonably bright, with over 50 percent of companies expecting production to be higher one year from now."

From Eurozone, PMI manufacturing was finalized at 60.6 in December, unrevised. Germany PMI manufacturing was finalized at 63.3, unrevised. France PMI manufacturing was revised lower to 58.8. Italy manufacturing dropped to 57.4 in December.

China Caixin PMI manufacturing improved

China Caixin PMI manufacturing rose to 51.5 in December, up from 50.8 and beat expectation of 50.7. That's the highest level in four months. Zhengsheng Zhong, director of macroeconomic analysis at CEBM Group said in the release that "manufacturing operating conditions improved in December, reinforcing the notion that economic growth has stabilized in 2017 and has even performed better than expected,." However, he also warned of the "downward pressure on growth due to tightening monetary policy and strengthening oversight on local government financing."

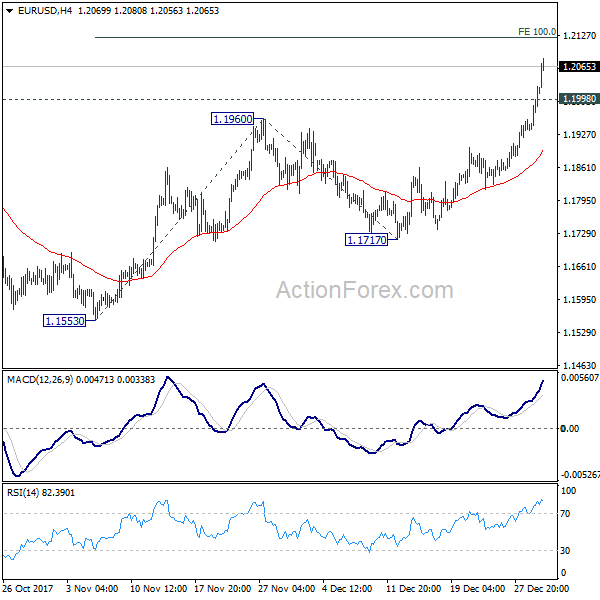

EUR/USD Daily Outlook

Daily Pivots: (S1) 1.1949; (P) 1.1987 (R1) 1.2039; More....

EUR/USD accelerates to as high as 1.2080 so far. Intraday bias remains on the upside for near term target at 100% projection of 1.1553 to 1.1960 from 1.1717 at 1.2124, which is above 1.2091 high. On the downside, below 1.1998 minor support will turn intraday bias neutral and bring consolidation before staging another rally.

In the bigger picture, rise from 1.0339 medium term bottom is seen as a corrective move for the moment. Therefore, in case of another rally, we'd be expect 38.2% retracement of 1.6039 (2008 high) to 1.0339 (2017 low) at 1.2516 to limit upside and bring reversal. That is also close to 61.8% projection of 1.0569 to 1.2091 from 1.1553 at 1.2494.

Economic Indicators Update

| GMT | Ccy | Events | Actual | Forecast | Previous | Revised |

|---|---|---|---|---|---|---|

| 1:45 | CNY | Caixin PMI Manufacturing Dec | 51.5 | 50.7 | 50.8 | |

| 8:45 | EUR | Italy Manufacturing PMI Dec | 57.4 | 58.5 | 58.3 | |

| 8:50 | EUR | France Manufacturing PMI Dec F | 58.8 | 59.3 | 59.3 | |

| 8:55 | EUR | Germany Manufacturing PMI Dec F | 63.3 | 63.3 | 63.3 | |

| 9:00 | EUR | Eurozone Manufacturing PMI Dec F | 60.6 | 60.6 | 60.6 | |

| 9:30 | GBP | PMI Manufacturing Dec | 56.3 | 57.9 | 58.2 | |

| 14:30 | CAD | RBC Manufacturing PMI Dec | 54.4 | |||

| 14:45 | USD | US Manufacturing PMI Dec F | 55 | 55 |

WTI Oil Futures Trading at Highest Level Since Over 2 Years

WTI oil futures are trading at the highest level since June 2015 after rising consistently and breaking above the key 60 mark.

Prices were trading sideways since late November between the 56 and 58 handles and a sudden surge higher on December 26 saw the market reach the key 60 level. This acted as strong resistance for a few sessions until a successful breach to rise to 60.71 earlier today. Consequently, upside momentum faded and prices started falling. The key 60 level is now expected to provide support.

Failure to hold at 60 would see prices move back into an important consolidation area between 59.50 – 60. Any move lower from this zone would likely see more sellers enter the market. Continued downside momentum would target 58.50. Breaking this support would take WTI back into its prior range (from late November to December).

Today's downside pressure may be limited and as long as the market remains above 60, then the bullish outlook is expected to remain intact in the short term. Looking at the 4-hour chart, RSI is still in bullish territory above 50.

Dollar on the Backfoot; Auto Shares Drag European Stocks Lower

Here are the latest developments in global markets:

FOREX: The dollar was the worst performer among its major peers during early European trading hours as optimism on the Eurozone's economic outlook and doubts over the effect of the US tax overhaul pushed the dollar index down to a three-month low of 91.75 (-0.29%). Euro/dollar approached a four-month peak at 1.2084 (+0.47%) and dollar/yen tumbled to 112.16 (-0.41%). Pound/dollar held strong above 1.35 (+0.30%) despite disappointing data on Markit UK manufacturing PMI. The antipodean currencies, the kiwi and the aussie , hovered near 2 ½ -month highs but were on track to close the day lower.

STOCKS: The European stocks started the year in the red as a decline in auto shares dragged the market down, while other sectors except energy were also in the backfoot. The pan European STOXX 600 and the blue chips STOXX 50 tumbled by 0.56% and 0.78% respectively at 1050 GMT. The German DAX 30 declined by 0.85% as the British Airways agreed to buy Air Berlin's insolvent Austrian airline Niki which Lufthansa backed down to acquire in December. The French CAC 40 fell by 0.88% and the British FTSE 100 pulled back by 0.41%.

COMMODITIES: Oil prices reversed earlier gains and deviated below the three-year highs reached in the Asian session amid anti-government protests in Iran. WTI crude was 0.13% down on the day at $60.34 per barrel and the Brent was weaker by 0.21% at $66.75. The dollar-denominated gold extended its gains towards a fresh three-month high of $1,312.74 per ounce.

Day ahead: US Manufacturing PMI & global dairy prices pending

A look ahead to the major economic releases expected later in the day, the IHS Markit company will publish final figures on the US manufacturing PMI for the month of December at 1445 GMT, while changes in global dairy prices will be also awaited at a tentative time.

According to forecasts, the US PMI is anticipated to remain unchanged at 55.0 in December, above the threshold mark of 50 which separates growth from contraction. However, since preliminary data are more important for the dollar, any upside or downside surprises in the data would influence moderately the greenback. In contrast, the FOMC meeting minutes due on Wednesday and Friday's nonfarm payrolls are predicted to offer a higher volatility to the dollar.

Investors will be also looking forward to the global dairy auctions to reveal changes in milk prices. A strong positive print could move the kiwi higher as milk is New Zealand's largest single export.

In energy markets, the API weekly report which tracks oil inventories in the US will be published at 2130 GMT.

DAX Dips to 15-Week Low Despite Solid German Mfg. Report

The DAX has started the New Year with losses, continuing the downward trend which marked trading late last week. In the Tuesday session, the index is at 12,816.50, down 0.72% on the day. The DAX has dropped to its lowest level since September 8. On the release front, German and Eurozone Manufacturing PMIs improved in December. German Manufacturing PMI came in at 63.3, while Eurozone Manufacturing PMI climbed to 60.6 points. Both indicators matched their estimates. On Tuesday, Germany releases Unemployment Change. In the US, the FOMC will publish the minutes of its December meeting.

Global stock markets enjoyed a strong year in 2017, and the DAX climbed an impressive 13.0%. Investors gave a thumbs-up as the German and eurozone economies showed solid growth, and data in the fourth quarter has been strong so Expectations remain high that the positive trend will continue into 2018, which bodes well for the DAX. As the new year begins, the markets will be keeping a close eye on the political situation in Germany, as President Angela Merkel strives to put together a new coalition. If new elections are avoided and Merkel forms a new government, the DAX is likely to post strong gains.

The markets will be keeping a close look on the Federal Reserve on Wednesday, with the release of the minutes of the December meeting. At that meeting, the Fed raised rates by 25 basis points, to a range between 1.25% and 1.50%. The hike marks a vote of confidence in the US economy, and if the minutes are hawkish, European stock markets could react with gains. If the US economy continues to expand at a clip exceeding 3%, the Fed is expected to raise rates up to four times in 2018. Currently, the CME Group has priced in a January rate hike at 98.5%. Although inflation remains well below the Fed target of 2.0%, outgoing Fed Chair Janet Yellen and other FOMC members have said that they expect that the strong labor market will lead to higher inflation. Although this is yet to materialize, of significance to the markets is the commitment of the Fed to press ahead with rate hikes, despite low inflation.

Canadian Dollar Gains as Greenback Sags

The Canadian dollar ended 2017 with gains, and the positive trend has continued into the New Year. In the Tuesday session, the pair is trading at 1.2537, down 0.33%. On the release front, there are no major events on the schedule. Both Canada and the US will release Manufacturing PMI reports.

At the Federal Reserve December meeting, policymakers raised rates by 25 basis points, to a range between 1.25-1.50%. The Fed will release the minutes of the meeting on Wednesday, and traders should consider the event a market-mover. The December hike marks a vote of confidence in the US economy, and if the minutes are hawkish, the US dollar could reverse directions and gain ground. If the US economy continues to expand at a clip exceeding 3%, the Fed is expected to raise rates up to four times in 2018. Currently, the CME Group has priced in a January rate hike at 98.5%. Although inflation remains well below the Fed target of 2.0%, outgoing Fed Chair Janet Yellen and other FOMC members have said that they expect that the strong labor market will lead to higher inflation. Although this is yet to materialize, of significance to the markets is the commitment of the Fed to press ahead with rate hikes, despite low inflation.

The Canadian dollar enjoyed a respectable 2017, posting gains of 6.6% against its US cousin. Will the positive trend continue in January? With the US economy booming, the Federal Reserve raised rates in December, and another move is expected this month. This will put strong pressure on the Bank of Canada to match with a rate hike, or risk seeing the Canadian dollar lose ground as investors move to a more attractive US dollar.

EUR/USD Daily Outlook

Daily Pivots: (S1) 1.1949; (P) 1.1987 (R1) 1.2039; More....

EUR/USD accelerates to as high as 1.2080 so far. Intraday bias remains on the upside for near term target at 100% projection of 1.1553 to 1.1960 from 1.1717 at 1.2124, which is above 1.2091 high. On the downside, below 1.1998 minor support will turn intraday bias neutral and bring consolidation before staging another rally.

In the bigger picture, rise from 1.0339 medium term bottom is seen as a corrective move for the moment. Therefore, in case of another rally, we'd be expect 38.2% retracement of 1.6039 (2008 high) to 1.0339 (2017 low) at 1.2516 to limit upside and bring reversal. That is also close to 61.8% projection of 1.0569 to 1.2091 from 1.1553 at 1.2494.