Sample Category Title

U.S Dollar Starts 2018 at New Lows

Tuesday January 2: Five things the markets are talking about

Despite the Fed backing up interest rates three-times in 2017 and starting the unwinding of its QE policy, the 'mighty' dollar ended up being the worst performing G10 currency last year (-9.5% vs. against its peers). The theme for the New Year, thus far, has not changed.

A plethora of manufacturing data is today's main releases (PMI surveys for the U.K, U.S and Eurozone), while the key focus this week will be this Friday's U.S and Canadian labor market report, where another strong headline rise is expected.

Tomorrow, the Fed will release minutes from its Dec. 12-13 policy meeting, when officials voted to hike short-term interest rates. Two FOMC members opposed the move, and the minutes may show if other participants shared their concerns about weak inflation. Investors will also be keen to know if U.S officials saw the Republican tax overhaul affecting the economy this year and beyond.

Note: The U.S dollar bull believe the tax plan could further support an already-growing U.S economy and push the Fed to hike rates at a faster pace in 2018.

For Friday's U.S jobs report, the market is not expecting any changes to the U.S jobless rate (+4.1%), and a healthy headline print of +180k new non-farm jobs last month, with average hourly earnings set to rise +0.3% on the month.

1. Global stocks mixed start to 2018

Euro equities is starting the New Year on the back foot, failing to capitalize on a positive Asian session, which was supported by Chinese equities rallying on the back of stronger manufacturing data (China's Dec. Caixin PMI Manufacturing rallied to its highest level in six-months).

Note: Markets in Japan remain closed until Thursday for holidays.

Down-under, Aussie shares were little changed on its first day of trade in 2018. The S&P/ASX 200 index closed out the year falling -0.4% on the last trading day of 2017, but logged a +7% gain for the year.

In Hong-Kong, stocks rallied the most in three-months to a new decade-high aided by China's stronger than expected factory activity. The Hang Seng index was up +1.99%, while the Hang Seng China Enterprises index rose +3.07%.

In China, the Shanghai Composite index closed up +1.27%, while the blue-chip CSI300 index was up +1.41%.

In Europe, regional indices have started January on the weak foot with notable weakness in the DAX and the French CAC - a stronger Euro (€1.2064) seems to be putting pressure on indices.

U.S stocks are set to open in the 'black' (+0.2%).

Indices: Stoxx600 -0.6% at 386.9, FTSE -0.3% at 7,650, DAX -0.3% at 12,942, CAC-40 % -0.1% at 5, IBEX-35 % at , FTSE MIB % at , SMI % at , S&P 500 Futures +0.2%

2. Oil starts the New Year strong as Iran unrest pushes up prices, gold stronger

Oil prices have started 2018 by posting their strongest opening in nearly four years, with crude rising amidst anti-government rallies in Iran and ongoing supply cuts led by OPEC and Russia.

Brent crude futures are at +$67.18 a barrel, up +31c, or +0.5%, while U.S West Texas Intermediate (WTI) crude are at +$60.63 a barrel, +21c, or +0.4%.

Despite anti-government protesters continuing to demonstrate in Iran - a major oil exporter - market sentiment remains bullish on the back of falling inventories globally and strong economic growth forecasted.

Note: Oil markets have been supported by a year of production cuts led by OPEC and Russia. The cuts started 12-months ago and are scheduled to cover all of 2018. While in the U.S, commercial crude oil inventories have fallen by almost -20% from their historic highs last March, to +431.9m barrels.

Strong global demand growth, especially from China, has also been supporting crude. A concern for the crude bull should be rising U.S production, which is on the verge of breaking through +10m bpd.

Gold prices (+0.2% to +$1,305 an ounce) have printed a three-month high overnight on strong technicals (closed above its 100-day moving last week) and on the back of a weaker U.S dollar.

Note: CFTC data last week show that investors have raised their net long position in COMEX gold for the second straight week in the week to Dec. 26, and cut their net short position in silver slightly.

3. Yields differentials to dictate shape of sovereign curves

Expect rate differentials to dominate trading in the New Year. In particular, the market will be focusing on the spread between the German 10-year Bund and U.S Treasury's - it has tightened to around +200 bps, but many expect the widening trend to resume as regional fundamentals are expected to reassert themselves this year.

The European Central Bank (ECB) is expected to remain one of the most accommodative central banks, given that its inflation target is expected to remain on the 'softer' side. If so, it should anchor Bund yields and lead to the German-U.S spread widening.

Note: The fixed income market now pricing in a +68% chance of a Fed March hike and two more hikes for 2018, investors will look to tomorrows FOMC's minutes for clues to assess how strong U.S policy makers confidence is for any pick-up in inflation.

The yield on U.S 10-year's has gained +2 bps to +2.43%, while Germany's 10-year Bund yield has backed up +3bps to +0.46%, the highest in almost three-months. In the U.K, the 10-year Gilt yield has advanced +3 bps to +1.217%, the highest in a week.

4. Dollar starts the New Year at new lows

The 'mighty' USD has begun 2018 with fresh broad declines. The U.S Dollar Index is trading atop of its three month lows.

The EUR/USD has added to its post holiday gains by +0.4% at €1.2966. The pair has been rising on expectations that ECB's QE program would not be extended when the program ends next September - On the weekend, comments from ECB's Coeure (France) - who noted that he saw a "reasonable chance" that bond buying would not be extended - is supporting the single unit.

Note: The ECB begins 2018 by cutting its monthly bond purchases by half to +€30B.

GBP/USD is again making an attempt to encroach on the post-Brexit £1.36 key resistance area. The pound has been supported outright by speculation that PM Theresa May will consider a cabinet reshuffle. Nevertheless, sterling edges lower against the EUR (€0.8909) after data this morning showed that U.K. manufacturing purchasing managers' index for December dropped to 56.3, below November's 58.2.

5. Eurozone manufacturing PMI confirmed at record high

Data releases this morning confirmed that PMI's for the eurozone's manufacturing sector hit a record high in December, rising to 60.6 from 60.1 in November, in line with expectations.

Digging deeper, last months high confirms how strongly the sector finished a year in which the eurozone economy exceeded expectations.

In addition to the currency area as a whole, there were series highs for Germany, Austria and Ireland, while the French and Greek sectors had their strongest months in a long time.

Strong new order flows suggest that Euro manufacturing will have a positive start to 2018.

USD/MXN 1H Chart: Greenback Likely To Consolidate

The dominant pattern that has guided the USD/MXN exchange rate for the last six months is an ascending triangle. As apparent on the chart, the pair reversed from its upper boundary on December 25 and has since traded in a narrow channel down. The US Dollar is currently stranded between two important support and resistance areas. The pressure from both sides might force the pair to consolidate in a narrow range in between their bounds. If looking at a longer term, a test of the senior channel should result in a new period of price decline, especially given the pair's steep appreciation during the past two months. Apart from the 200-hour SMA and the weekly R3, the rate also faces the support of the monthly PP and the weekly R2 near the 19.40 mark.

AUD/CAD 1H Chart: Pair Near Triangle Boundary

The Australian Dollar has been trading in an ascending channel against the Loonie since mid-November. The upper boundary of this pattern and a long-term channel down near 0.9880 was reached five weeks later. Since then, the Aussie's failure to move below the 0.9782 mark has resulted in the formation of a descending triangle. The pair had reached its upper boundary, likewise reinforced by the 200-hour SMA, on Tuesday morning. From theoretical point of view, this triangle should be breached to the upside. A breakout in this session is also signaled by technical indicators. The subsequent surge is not expected to be long-lasting, as the upper boundary of the senior channel is located nearby circa 0.9860. Taking all this into account, the base scenario favours a test of the senior channel and a reversal near this area.

Market Update – European Session: German And Euro Zone Dec Final Manufacturing PMI Levels At Record Highs

Notes/Observations

USD begins 2018 with fresh broad declines; Dollar Index at 3 1/2 month lows

Both German and Euro Zone Dec Final PMI Manufacturing unrevised and at record highs; France revised lower but still the highest reading since Sept 2000

Asia:

PBoC: To set up temporary liquidity facility for the China Lunar New Year which will allow banks to use official required deposit reserves of up to 200bps

China Dec Manufacturing PMI (Govt official): 51.6vV 51.6e; Non-Manufacturing: 55.0 v 54.7e

China Dec Caixin PMI Manufacturing: 51.5 v 50.7e (highest reading since Aug)

Europe:

PM May said to consider Brexit role for Boris Johnson in cabinet reshuffle

ECB's Coeure (France): saw "reasonable chance" bond buys will not be extended

ECB's Mersch (Luxembourg): We should take a position on the future of QE prior to summer 2018. Needed to move step by step toward monetary policy normalization; can't act too tentatively and too late

Americas:

President Trump tweet: Iran is failing at every level despite the terrible deal made with them by the Obama Administration. The great Iranian people have been repressed for many years. They are hungry for food & for freedom. Along with human rights, the wealth of Iran is being looted. TIME FOR CHANGE!

Energy:

Weekly Baker Hughes US Rig Count: 929 v 931 w/w (-0.2%) (2nd weekly decline in a row)

Economic Data:

(IN) India Dec PMI Manufacturing: 54.7 v 52.6 prior (5th month of expansion)

(IE) Ireland Dec Manufacturing PMI: 59.1 v 58.1 prior (record high)

(TR) Turkey Dec PMI Manufacturing: 54.9 v 52.9 prior (10th month of expansion)

(SE) Sweden Dec PMI Manufacturing: 60.463.0e

(NL) Netherlands Dec Manufacturing PMI: 62.2 v 62.4 prior (52nd month of expansion)

(NO) Norway Dec Manufacturing PMI: 57.8 v 57.0e

(PL) Poland Dec PMI Manufacturing: 55.0 v 54.6 (38th month of expansion and highest since Feb 2015)

(HU) Hungary Dec Manufacturing PMI: 60.0 v 58.8 prior (25th month of expansion)

(ES) Spain Dec Manufacturing PMI: 55.8 v 56.2e (50th month of expansion)

(CZ) Czech Republic Dec PMI Manufacturing: 59.8 v 59.2e (17th month of expansion)

(IT) Italy Dec Manufacturing PMI: 57.4 v 58.5e (16th month of expansion)

(FR) France Dec Final Manufacturing PMI: 58.8 v 59.3e (confirmed 15th month of expansion and highest since Sept 2000)

(DE) Germany Dec Final Manufacturing PMI: 63.3 v 63.3e (confirmed 37th month of growth and a record high)

(EU) Euro Zone Dec Final Manufacturing PMI: # v 60.6e (confirmed 53rd month of growth and a record high)

(GR) Greece Dec Manufacturing PMI: 53.1 v 52.2 prior (7th month of expansion and highest since Jun 2008)

(UK) Dec PMI Manufacturing: 56.3 v 57.9e

Fixed Income Issuance:

None seen

SPEAKERS/FIXED INCOME/FX/COMMODITIES/ERRATUM

Equities

Indices [Stoxx600 -0.6% at 386.9, FTSE -0.3% at 7,650, DAX -0.3% at 12,942, CAC-40 %-0.1 at 5, IBEX-35 % at , FTSE MIB % at , SMI % at , S&P 500 Futures +0.2%]

Market Focal Points/Key Themes: European Indices have started 2018 on the weaker foot with notable weakness in the Dax and French CAC, with the strong Euro putting pressure on indices after reaching a 4 month high. On the corporate front IAG trades higher after confirming the acquisition of NIKI from Air Berlin, while M&S trades slightly higher following the divestiture of its retail units in Hong Kong and Macau. BP trades slightly lower after the company expects a one off non cash charge of $1.5B in Q4 due to the US tax changes and Glencore trades lower after selling its Tahmoor Coal Mine in Australia.

Equities

Consumer Discretionary [International Consolidated Airlines [IAG.UK] +1.8% (Confirms acquisition of NIKI for €20M), Steinhoff [SNH.ZA] +12% (Update on restatement of financial statements), Stockmann [STCBV.FI] +4.4% (Completed the divestment of Delicatessen's business in Finland for €27M; Looks at possible divestment of its book house property)]

Energy [BP [BP.UK] -0.3% (Impact of US tax overhaul)]

Materials [Glencore [GLEN.UK] -0.6% (Divestiture)]

Speakers

Norway Central Bank (Norges) Gov Olsen: Interest rate to normalize

Norway PM Solberg: Domestic economy was doing better; Hoped for a three-party coalition

Currencies

EUR/USD was higher by 0.4% in the session as the pair added to its post-holiday gains. The pair has been rising on expectations that ECB's QE program would not be extended when the program ends in Sept (expectations heightened following weekend commentary by ECB's Coeure (France): who noted that saw a "reasonable chance" bond buys would not be extended). ECB begins 2018 by cutting its monthly purchases by half to €30B

GBP/USD was again approaching the post-Brexit 1.36 key resistance area. GBP aided by speculation that PM May would consider a Cabinet reshuffle to quell the storm within her own Tory party and provide a Brexit role for Boris Johnson.

Fixed Income

Bund Futures trade down 22 ticks at 161.46 bouncing off a low of 161.22 following the decline in Equities as the Euro continues to strengthen. A continued move below today's 161.22 low targets 161.00 then 160.71, with a continued rebound targeting 161.86.

Mondays liquidity report showed Friday's excess liquidity fell to €1.758T from €1.779T prior. Use of the marginal lending facility rose to €299M from €266M prior.

European corporate issuance rose 12.6% in 2017 to €1.27T with SSAs accounting for ~36% of the primary issuance. In total 1,776 tranches were issued via 828 issuers.

Looking Ahead

(IT) Italy Dec Budget Balance: No est v -€5.5B prior

05:25 (BR) Brazil Central Bank Weekly Economists Survey

05:30 (BE) Belgium Debt Agency (BDA) to sell 3-month and 6-month Bills

05:30 (HU) Hungary Debt Agency (AKK) to sell in 3-month Bills

06:45 (US) Daily Libor Fixing

07:00 (CA) Canada Nov Leading Indicator M/M: No est v 0.4% prior

07:00 (BR) Brazil Dec PMI Manufacturing: No est v 53.5 prior

(ZA) South Africa Dec Naamsa Vehicle Sales Y/Y: No est v 7.2% prior

08:00 (ES) Spain Debt Agency (Tesoro) announces size of upcoming issuance

08:05 (UK) Baltic Dry Bulk Index

08:50 (FR) France Debt Agency (AFT) to sell combined €4.5-5.7B in 3-month, 6-month and 12-month BTF Bills

09:00 (MX) Mexico Dec IMEF Manufacturing Index: 52.4e v 52.6 prior; Non-Manufacturing Index: 52.0e v 52.5 prior

09:30 (CA) Canada Dec Manufacturing PMI: No est v 54.4 prior

09:30 (EU) ECB paused its Covered-Bond Purchases into year-end (no update)

09:45 (US) Dec Final Markit Manufacturing PMI: 55.0e v 55.0 prelim

10:00 (MX) Mexico Nov Total Remittances: $2.5Be v $2.6B prior

10:30 (MX) Mexico Dec PMI Manufacturing: No est v 52.4 prior

11:30 (US) Treasury to sell 4-Week and 52-Week Bills

11:30 (US) Treasury to sell 3-Month and 6-Month Bills

12:00 (BR) Brazil Dec Trade Balance: $4.2Be v $3.6B prior; Total Exports: $17.1Be v $16.7B prior; Total Imports: $12.9Be v 13.1B prior

12:00 (IT) Italy Dec New Car Registrations Y/Y: No est v 6.8% prior

Euro Kicks Off New Year At 1.20

EUR/USD hasn't missed a beat as we start 2018, posting gains in the Tuesday session. Currently, EUR/USD is trading at 1.2067, up 0.55% on the day. The pair is at its highest level since early September. On the release front, German and Eurozone Manufacturing PMIs improved in December. German Manufacturing PMI came in at 63.3, while Eurozone Manufacturing PMI climbed to 60.6 points. Both indicators matched their estimates. On Tuesday, Germany releases Unemployment Change. In the US, the FOMC will publish the minutes of its December meeting, and we'll get a look at ISM Manufacturing PMI.

German inflation ended the year on a strong note, as Preliminary CPI accelerated to 0.6% in December. This edged above the forecast of 0.5%. The sharp gain matched the February reading, equaling the strongest gain recorded in 2017. Earlier this month, in a nod to stronger economic activity in 2017, the ECB raised its forecasts for growth and inflation for the eurozone from this year through to 2019. Still, inflation remains well below the ECB target of around 2.0%, and ECB policymakers are unlikely to announce an end to their stimulus package until inflation moves closer to the 2.0% target.

Investors will be monitoring the Federal Reserve on Tuesday, with the release of the minutes of the December meeting. At that meeting, the Fed raised rates by 25 basis points, to a range between 1.25-1.50%. The hike marks a vote of confidence in the US economy, and if the minutes are hawkish, the US dollar could gain ground and stem the euro rally. If the US economy continues to expand at a clip exceeding 3%, the Fed is expected to raise rates up to four times in 2018. Currently, the CME Group has priced in a January rate hike at 98.5%. Although inflation remains well below the Fed target of 2.0%, outgoing Fed Chair Janet Yellen and other FOMC members have said that they expect that the strong labor market will lead to higher inflation. Although this is yet to materialize, of significance to the markets is the commitment of the Fed to press ahead with rate hikes, despite low inflation.

Forex Technical Analysis: EUR/USD, USD/JPY, GBP/USD

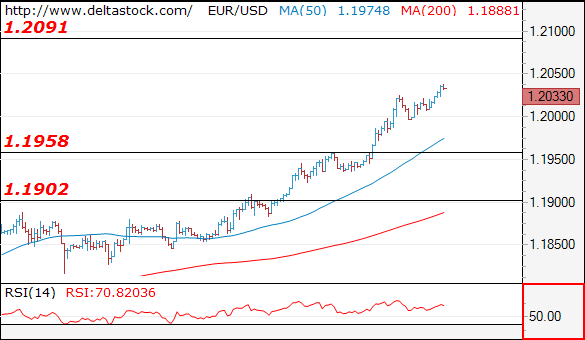

EUR/USD

Current level - 1.2033

The bias is still positive after 1.1715 low and the outlook is bullish, for a tight test of 1.2090 peak. Key support is projected at 1.1960, followed by 1.1910 area.

| Resistance | Support | ||

| intraday | intraweek | intraday | intraweek |

|

1.2050 |

1.2090 |

1.1960 |

1.1910 |

|

1.2090 |

1.2240 |

1.1910 |

1.1715 |

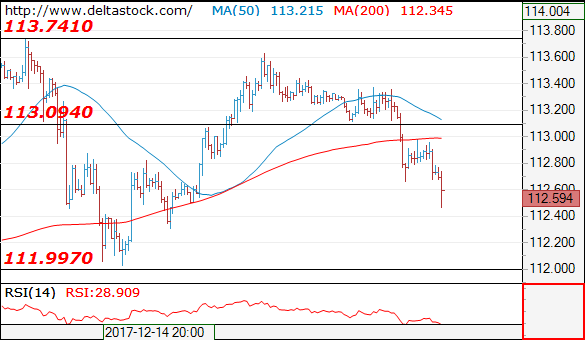

USD/JPY

Current level - 112.59

The intraday bias is bearish, for a slide towards 112.00 area. Initial resistance lies at 113.10 and crucial on the upside is 113.40 high. The whole slide from 113.65 should be considered a final leg of the consolidation pattern below 113.74, preceding a rebound towards 114.70.

| Resistance | Support | ||

| intraday | intraweek | intraday | intraweek |

|

112.65 |

113.09 |

112.00 |

111.00 |

|

113.09 |

113.65 |

111.00 |

111.00 |

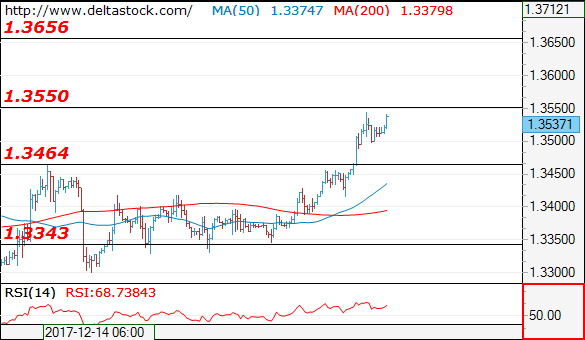

GBP/USD

Current level - 1.3537

The uptrend since 1.3300 lows is intact, ready for a break through 1.3550 hurdle, towards 1.3650 area. Initial key support lies at 1.3460.

| Resistance | Support | ||

| intraday | intraweek | intraday | intraweek |

|

1.3550 |

1.3660 |

1.3500 |

1.3460 |

|

1.3660 |

1.3660 |

1.3460 |

1.3300 |

EUR/USD Breaks Higher

An initially unexpected even has occurred on the EUR/USD currency pair's charts. The Euro has broken various resistance levels against the US Dollar.

Namely, the currency exchange rate moved past the previously drawn short term and medium term pattern resistance lines near the 1.1980 mark. Moreover, the currency rate did not stop there.

In the following hours and as the new year started the currency pair just extended the gains to the upside. On Tuesday morning the currency rate was already located at the 1.2050 mark.

Moreover, the closest resistance was near the 1.21 level.

GBP/USD Consolidates Near Three-Month High

Upside risks dominated GBP/USD during the last trading day of 2017. The pair managed to breach the 50.0% Fibo and eventually consolidated near the 1.3530 mark.

Technical indicators are in favour of a subsequent surge that would push the rate above its three-month high of 1.3550. The nearest resistance that could halt further advances is the distant weekly and monthly R1s circa 1.3610.

In case the British Manufacturing PMI to be published at 0930GMT does not put an upward pressure on the rate and it thus manages to maintain its movement sideways, this might signal to a soon change in the sentiment.

Possible donwside targets in this session is the 55-hour SMA and the weekly PP near 1.3475.

USD/JPY Recovers Lost Positions

Following a 40-pip plunge during the first half of Friday, the pair managed to recover some of its lost positions during the following hours. However, the strong resistance of the 55-hour SMA did not allow to surpass the 112.80 mark, thus leaving the rate lingering slightly above the monthly PP by Tuesday morning.

It is likely that the bullish sentiment prevails in this session which could push the US Dollar up to the weekly PP, the 100-hour SMA and the upper trend line breached on December 28 circa 113.00. Given that this area is likewise reinforced by the 55-day SMA, bulls could fail to overcome this psychological level.

In terms of downward pressure, the US Dollar is supported by the weekly S1 at 112.32.

XAU/USD Above 1,310 Mark

Due to the increase of the US Dollar's weakness the yellow metal's price has continued to climb. Moreover, the continuation of the surge is set to continue.

Just before the year changed and 2018 started, the currency pair reached already above the 1,300 mark. Meanwhile, during the first trading day of the year the commodity price had reached above 1,310 level.

However, after doing a review of the junior channel up pattern's borders it was discovered that the pair has been slowed down by an upper trend line of the junior pattern. It is possible that the resistance could force the metal's price slightly lower.

Although, that is highly unlikely.