Sample Category Title

PMI Data Headlines Economic Calendar After New Year

The first trading session of the new year is expected to see limited activity, with only a handful of PMI data scheduled to make headlines.

Action begins at 08:15 GMT with a report on Spain's manufacturing PMI. For the next hour and a half, IHS Markit will release PMI reports for France, Italy, Germany, Greece, the United Kingdom and broader Eurozone.

In North America, Markit will also report on US and Canadian manufacturing conditions.

Earlier in the day, Caixin China said manufacturing conditions in the world's second largest economy improved unexpectedly last month. The December manufacturing PMI rose to 51.7 from 50.8 in November. Analysts in a median estimate called for a reading of 50.6.

'For the most part, the manufacturing sector remained stable in November, although some signs of weakness emerged,' Dr. Zhengsheng Zong said in the official PMI press release. 'In the fourth quarter, the economy is likely to maintain the stability observed since the start of the second half of the year. Economic growth in 2017 is expected to be higher than last year, but it may come under downward pressure in 2018.'

2017 was a banner year for global equities, with Asian, European and US stock indexes gaining between 7% and 36%. Much of the gains were led by Wall Street, which rallied behind President Trump's young presidency. The Trump administration is expected to adopt a cocktail of policy measures aimed at boosting economic growth. Optimism in the plan contributed to back-to-back quarters of solid GDP growth for the world's largest economy.

However, political optimism failed to lift the US dollar. The world's most actively traded currency is coming off its worst annual performance in well over a decade even as the Federal Reserve raised interest rates multiple times.

The Fed will hold its first meeting of the year on 30 January, which will be the final meeting with Janet Yellen at the helm. She will be replaced in February by current Fed Governor Jerome Powell.

EUR/USD

The euro was little changed on Tuesday after a solid week of gains in the final stretch of 2017. The EUR/USD is trading above 1.2000, and could be poised to re-test multi-year highs near 1.2100. The pair added 15% during 2017.

GBP/USD

The Cable also ended the year on solid footing, closing above 1.3500 for the first time in three weeks. The GBP/USD faces immediate support at 1.3490, followed by 1.3460. Key resistance levels include 1.3550 and 1.3595.

USD/CAD

The Canadian dollar was down slightly in Asian trading, but continued to hover near 10-week highs. The USD/CAD exchange rate is currently trading around 1.2535, with the bears eyeing a reversal back down toward 1.2500.

NZDUSD Intraday Analysis

NZDUSD (0.7113): The New Zealand dollar rallied to a 2-month high on Friday with early price action today suggesting that the currency pair is maintaining the bullish momentum. Further upside gains could be seen coming with the resistance level of 0.7160 likely to be tested. On the intraday chart, NZDUSD is seen bouncing off the lower median line which could keep prices supported. A breakout from the lower median line could however suggest a correction. Support at 0.7062 remains the first level of defence, failing which, NZDUSD could be seen correction to 0.6917.

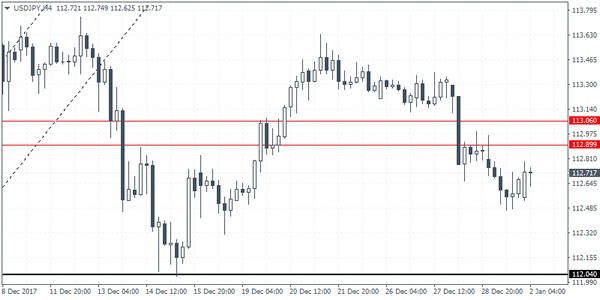

USDJPY Intraday Analysis

USDJPY (112.71): The USDJPY posted declines on Friday although the U.S. dollar is looking to pare some of those losses. In the near term, the modest recovery could see USDJPY rallying back to the 112.90 - 113.00 level where resistance could be established. A reversal near this resistance could keep USDJPY range bound. Support at 112.04 remains the key level to the downside. A breakout from this range is required in order for USDJPY to establish further direction.

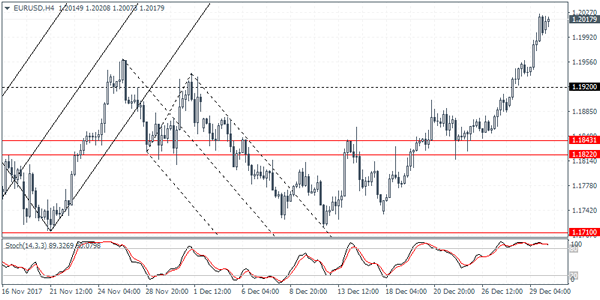

EURUSD Intraday Analysis

EURUSD (1.2017): The EURUSD rallied to a 3-monh high on an intraday basis on Friday closing in at 1.1997. The common currency maintained the gains as it opened on Tuesday near the same levels. In the short term, we expect that the EURUSD is likely to maintain the upside momentum. However, consolidation is expected as price action approaches the 1.2000 - 1.2050 handle. At the time of writing, EURUSD is seen trading near the highs. We expect to see short term correction in prices taking place. Support at 1.1920 remains the initial support to the downside, followed by a steeper test of support at 1.1843 - 1.1822.

Markets Open To A New Trading Week And A New Year!

The markets opened after the holiday season with a relatively quiet trading scene. The euro managed to post some gains on the last trading day of the year, as the U.S. dollar weakened into the final trading hours.

The weaker greenback led to the commodity markets holding their gains into the 2017 close. Geo-politics was largely stable over the week and did not impact the market sentiment by much. Trading is expected to remain light today ahead of a busy week starting from tomorrow.

On the economic calendar today, activity is slightly quiet. In the Eurozone, the Italian, French, German and the Eurozone final manufacturing PMI figures are expected to be released. No major surprises are expected as economists expect the final manufacturing PMI to remain steady at 60.6 same as the month before.

In the UK, the manufacturing PMI for December is expected to remain slightly weaker at 58.0 compared to 58.2 previously. In the U.S. trading session, the final manufacturing PMI is expected to show a steady print of 55.0. This comes ahead of the U.S ISM manufacturing PMI due on Wednesday.

GBPUSD Has Room For More Upside Following Break Above 1.3500

GBPUSD has held a neutral bias since late November, trading in a range between 1.3300 and 1.3550. The outlook is neutral as long as the market remains in the resistance zone between 1.3500 and the September 20 peak of 1.3656.

Near-term risk is to the upside after GBPUSD bounced off 1.3300, a level that was tested a few times in mid-December, proving to be a strong support level. If this support holds, more sideways trading is expected in the near term until prices make a sustained break above 1.3656. Support is seen at 1.3300 (50-day moving average). A drop below this support would target further support at 1.3000. Any move lower would change the short-term neutral bias to a more bearish one.

Momentum is bullish and RSI is rising. The 50-day and 200-day moving averages are positively aligned. As long as the market remains above these, there is room for further upside. In the bigger picture, GBPUSD is expected to remain steady in a broad, choppy range between 1.3000– 1.3500, as the pair consolidates after the rise from the 1.2000 area.

Market Update – Asian Session: Broad Dollar Weakness On The 1st Day Of Trade In 2018

Headlines/Economic Data

General Trend: Equity markets (ex-Japan) open 2018 generally higher, led by China and Hong Kong

Singapore Q4 GDP above estimates (first major Asian economy to issue Q4 GDP data)

China Dec Caixin PMI Manufacturing rises to highest level since Aug 2017

Taiwan Dec Manufacturing PMI hits multi-year high

Asian currencies gain: Korean Won (KRW) trades at highest level since Oct 2014; Singapore Dollar (SGD) hits highest since mid-2016; Taiwan Dollar (TWD) continues to trade at over 4 year highs

Japan

Nikkei 225 closed for holiday

Looking ahead: Japan to be closed for holiday on Wednesday

Korea

Kospi opened +0.3%

KRW rises to 3-yr high against USD, attributed to exporters selling dollars

(KR) South Korea Unification Min Cho: confirms have offered high ranking talks with North Korea on Jan 9th

(KR) South Korea Dec PMI Manufacturing: 49.9 v 51.2 prior

(KR) South Korea Finance Chief: Reiterates to take steps on drastic fx moves

(KR) Bank of Korea Gov: Further interest rate hikes should not be related to retirement of BoK Gov, but instead based on economic indicators

(KR) South Korea President Moon: To put policy in focus on jobs and household income

(KR) South Korea sells KRW1.0T in 3-month monetary stabilization bonds at 1.55%

005380.KR (Hyundai Motor) Vice Chairman: 2017 was the hardest year due to China sales slump; expect car demand to slow in major markets; -3% at the open

000270.KR (Kia Motor) Guides 2018 vehicles sales 2.88M units; Sees rising uncertainties including strong Korean Won (KRW) and geopolitical risks; 1.6%

035250.KR (Kangwon Land): To reduce casino operating hours and table facilities; -10.6%

090430.KR (Amore Pacific): +2.5%: China govt lifts ban on group tours to South Korea, according to a South Korean press report

China/Hong Kong

Hang Seng opened +0.4% before rising over 1% above 30,000; Shanghai Composite +0.2%

Hang Seng Property Index +2.8%: China may not adopt a property tax until 2020, said an earlier released Chinese press report.

(CN) CHINA DEC GOVT OFFICAL MANUFACTURING PMI: 51.6 V 51.6E; NON-MANUFACTURING: 55.0 V 54.7E

(HK) Macau Dec Gaming Rev +14.6% v ~20%e; Hang Seng Services Index -2% (weighed down by gaming stocks, Wynn Macau -3.5%, MGM China -3.5%)

(CN) PBoC: Skips OMO for 7th straight session; Net drains CNY290B

(CN) PBOC Gov Zhou reiterates prudent monetary policy and reasonable loan growth in 2018 – press

(CN) CHINA DEC CAIXIN PMI MANUFACTURING: 51.5 V 50.7E (highest reading since Aug 2017)

USD/CNY (CN) China PBoC sets yuan reference rate at 6.5079 v 6.5342 prior (strongest level since Sept 11th)

(HK) Overnight HK$ HIBOR -66bps (most since Nov 1st); 1-week HIBOR -47bps (most since Oct 2008)

54.HK Sells 66.69% stake in Hopewell Highway Infrastructure

Australia/New Zealand

ASX 200 opened flat, trading slightly lower with little direction; closed -0.2%

(AU) Australia Dec CoreLogic House Price Index M/M: -0.4% v -0.1% prior

(AU) Analysts caution that the risk of a rise in Australian inflation has not been adequately priced in - AFR

BLK.AU To raise A$36M through entitlement offering; to defer repayment of term loan to Jan 15th 2018; Names Milan Jerkovic as Executive Chairman as part of recapitalization plan

Other Asia

(SG) SINGAPORE Q4 ADVANCED GDP SAAR Q/Q: 2.8% V 1.6%E; Y/Y: 3.1% V 2.6%E; 2017 GDP: 3.5% v 2.0% prior v 3.0-3.5% official target

North America

(US) Democrats in high-cost, high-tax states are devising ways to blunt the impact of the recently passed tax law’s clampdown on the state and local tax (SALT) deduction – press

Looking ahead: US Weekly API Crude Oil Inventories to be released on Tuesday

Europe

(ES) Spain Econ Min sees Catalonia crisis cost at €1.0B

(UK) Economists see UK 2018 GDP growth of no more than 1.5% vs 1.4% forecast of the Office for Budget Responsibility (OBR) – FT Poll; The economists expect the BoE to raise rates by 50bps in 2018.

Looking Ahead: UK Dec Manufacturing PMI to be released

Levels as of 01:00ET

Nikkei225 closed, Hang Seng +1.7%; Shanghai Composite +1.0%; ASX200 -0.1%, Kospi +0.3%

Equity Futures: S&P500 +0.2%; Nasdaq100 +0.2%, Dax untraded; FTSE100 -0.1%

EUR 1.2023-1.2004; JPY 112.79-112.58; AUD 0.7843-0.7795;NZD 0.7122-0.7058

Feb Gold -0.0% at $1,309/oz; Feb Crude Oil +0.3% at $60.62/brl; Mar Copper -0.5% at $3.28/lb

Australia’s Manufacturing Sector Growth Moderated In December

For the 24 hours to 23:00 GMT, the AUD rose 0.18% against the USD and closed at 0.7809.

LME Copper prices declined 0.8% or $59.0/MT to $7157.0/MT. Aluminium prices declined 0.2% or $4.5/MT to $2241.5/MT.

In the Asian session, at GMT0400, the pair is trading at 0.7832, with the AUD trading 0.29% higher against the USD from yesterday's close.

Overnight data indicated that Australia's AiG performance of manufacturing index dropped to a level of 56.2 in December, after recording a level of 57.3 in the prior month.

Elsewhere in China, Australia's largest trading partner, the Caixin/Markit manufacturing PMI registered an unexpected rise to a level of 51.5 in December, surging to its highest level since August 2017 and reinforcing the notion that economic growth in the world's second largest economy has picked-up momentum. The PMI had registered a level of 50.8 in the previous month, while markets were anticipating for a fall to a level of 50.7.

The pair is expected to find support at 0.7806, and a fall through could take it to the next support level of 0.7781. The pair is expected to find its first resistance at 0.7846, and a rise through could take it to the next resistance level of 0.7861.

The currency pair is trading above its 20 Hr and 50 Hr moving averages.

German Inflation Rose Above Market Expectations In December

For the 24 hours to 23:00 GMT, the EUR rose 0.54% against the USD and closed at 1.2008, following better-than-expected inflation figures from Germany.

Data indicated that the flash consumer price index (CPI) in Germany advanced more-than-anticipated by 1.7% on an annual basis in December, thus offering tentative signs of sustained pick-up in inflation in the Euro-bloc’s largest economy. The CPI had climbed 1.8% in the prior month, while markets were expecting for a gain of 1.5%.

In the Asian session, at GMT0400, the pair is trading at 1.2013, with the EUR trading marginally higher against the USD from yesterday’s close.

The pair is expected to find support at 1.1998, and a fall through could take it to the next support level of 1.1982. The pair is expected to find its first resistance at 1.2026, and a rise through could take it to the next resistance level of 1.2038.

Moving ahead, market participants would look forward to the release of final Markit manufacturing PMI for December across the Euro-zone, due in a few hours. Moreover, the US final Markit manufacturing PMI for December, scheduled to be released later in the day, will be on investors’ radar.

The currency pair is trading above its 20 Hr and 50 Hr moving averages.

Pound Trading Marginally Higher In The Asian Session

For the 24 hours to 23:00 GMT, the GBP rose 0.45% against the USD and closed at 1.3513.

In the Asian session, at GMT0400, the pair is trading at 1.3516, with the GBP trading a tad higher against the USD from yesterday’s close.

The pair is expected to find support at 1.3503, and a fall through could take it to the next support level of 1.349. The pair is expected to find its first resistance at 1.3526, and a rise through could take it to the next resistance level of 1.3536.

Trading trend in the Pound today is expected to be determined by the release of UK’s Markit manufacturing PMI for December, slated to release in a few hours.

The currency pair is trading above its 20 Hr and 50 Hr moving averages.