Sample Category Title

Germany Annual Inflation Pace Slows into Year-End (as Expected); South African Court Delivers Zuma Impeachment Blow

Notes/Observations

- European inflation annual inflation place slows into year-end (as expected)

- South African court delivers Zuma impeachment blow

Asia:

- South Korea Dec CPI M/M: 0.3% v 0.3%e; Y/Y: 1.5% v 1.4%e (**Note: inflation target is 2.0%)

- China PBoC skipped its OMO for 6th straight session; Weekly net drain CNY290B v CNY200B injection w/w; For 2017, the PBoC drained CNY65B

- Milk Producer Fonterra cuts New Zealand milk collections forecast on dry weather conditions

Europe:

- Italian President Mattarella signed decree to dissolve parliament ahead of elections (as expected) with general election set for March 4th

Americas:

- US President Trump: Been 'soft' on trade with China

Energy:

- WTI Crude Oil Futures traded above $60/bbl, highest since June 2015 amid US weekly inventories data

Economic Data:

- (NL) Netherlands Dec Producer Confidence: 8.9 v 9.1 prior

- (RU) Russia Dec PMI Services: 56.8 v 55.6e (23rd month of expansion), PMI Composite: 56.0 v 56.3 prior

- (ZA) South Africa Nov M3 Money Supply Y/Y: 6.6% v 5.8%e; Private Sector Credit Y/Y: 6.5% v 6.2%e

- (TR) Turkey Nov Trade Balance: -$6.3B v -$6.3Be

- (TH) Thailand Nov Current Account: $5.3B v $3.9Be; Overall Balance of Payments (BOP): $2.3B v $2.1B prior; Trade Account Balance: $3.3B v $1.6B prior; Exports Y/Y: 12.3% v 13.4% prior; Imports Y/Y: 11.9% v 16.6% prior

- (ES) Spain Dec Preliminary CPI M/M: 0.1% v 0.3%e; Y/Y: 1.2% v 1.5%e

- (ES) Spain Dec Preliminary CPI EU Harmonized M/M: 0.1% v 0.2%e; Y/Y: 1.3% v 1.5%e

- (DE) Germany Dec CPI Saxony M/M: 0.6% v 0.3% prior; Y/Y: 1.7% v 2.0% prior

- (SE) Sweden Nov Household Lending Y/Y: 7.1%e v 7.1% prior

- (EU) Euro Zone Nov M3 Money Supply Y/Y: 4.9% v 4.9%e

- (DE) Germany Dec CPI Hesse M/M: 0.6% v 0.4% prior; Y/Y: 1.7% v 2.0% prior

- (DE) Germany Dec CPI Bavaria M/M: 0.5% v 0.4% prior; Y/Y: 1.7% v 1.8% prior

- (ES) Spain Oct Current Account: €1.7B v €2.1B prior

- (CZ) Czech Nov M2 Money Supply M2 Y/Y: 8.3% v 9.1% prior

- (NO) Norway Central Bank (Norges) Jan Bank Daily FX Purchases (NOK): -900M v -900M prior

- (IT) Italy Nov PPI M/M: 0.4% v 0.4% prior; Y/Y: 2.8% v 2.2% prior

- (DE) Germany Dec CPI Baden Wuerttemberg M/M: 0.6% v 0.4% prior; Y/Y: 1.8% v 1.8% prior

- (DE) Germany Dec CPI North Rhine Westphalia M/M: 0.5% v 0.3% prior; Y/Y: 1.5% v 1.8% prior

Fixed Income Issuance:

- (IN) India sold total INR40B vs. INR150B indicated in 2022, 2031, 2033 and 2046 bonds

- (ID) Indonesia sold total IDR10.1T n 2018 non-tradable notes via private placement

SPEAKERS/FIXED INCOME/FX/COMMODITIES/ERRATUM

**Equities**

Indices [Stoxx50 -0.2% at 3,514, FTSE +0.3% at 7.647, DAX -0.3% at 12.943, CAC-40 -0.2% at 5.332, IBEX-35 -0.3% at 10.063, FTSE MIB %-0.6 at 21.997, SMI -0.3% at 9.379, S&P 500 Futures +0.2%]

Market Focal Points/Key Themes: European markets opened largely flat and traded slightly down as the session progressed; truncated trading session due to holidays; Euro strength putting a damper on potential upward trends in stocks; commodity prices continue to buoy material stocks; no major upcoming data events for the rest of the year

Equities

- Consumer discretionary [Barry Callebaut BARN.CH -0.8% (cocoa outlook)]

- Financials [Allianz ALV.DE -0.9% (acquisition completion)]

- Healthcare [Astrazeneca AZN.UK +0.9% (analyst action)]

- Industrials [Airbus AIR.FR -0.1% (Wizz Air order)]

Speakers

- ECB's Nowotny (Austria): Global trade has developed better than expected. Austria's economy gave reasons for optimism; Brexit effects not noticeable domestically

- Italy Stats Agency (ISTAT) Monthly Economic Note saws growth firming up. Leading indicators improved but slowed down in pace

- German BGA exporters association: Forecasts 2018 exports at €1.34T, +5% y/y

- South Africa Constitution Court ruling on President Zuma: Parliament did not hold Zuma accountable for unlawful use of State funds to pay for upgrade to his private home

- China PBoC reiterated its stance of prudent and neutral monetary policy, to maintain reasonable and stable liquidity and effectively control macro leverage ratio. It also reiterates that it would deepen exchange rate reform

- China State planner NDRC: To examine the risks of corporate bonds as 2018 faced big redemption pressures

- China Ministry of Finance (MOF): To cut corporate taxes from overseas gains

- Taiwan President Tsai Ing-wen reiterated stance to maintain status quo with China. Defense budget to grow steadily each year as China's military ambitions were becoming more apparent. Planned changes to tax and corporate rules along with measures to help workers receive higher pay; to continue raising the minimum base salary

- India Junior Fin Min: No proposal for plans to privatize the State-run banking sector

Currencies

- USD continued to limp into year-end. After initially rallying after the US election back in Nov 2016, the dollar had since retreated some 9% against the GBP and 12% against the euro this year.

- Italy President. Mattarella formally dissolved parliament on Thursday and called elections for early March. Dealers noted that the vote would highlight the economic and political problems still stalking Europe and the country's role as the weakest flank in the currency union.

- EUR/USD higher by .0.4% to approach the 1.20 handle for fresh 3-month highs. The pair ends 2017 in the middle of its historical tracing range

- GBP/USD holding above the 1.35 level with the pair ending 2017 higher by over 6.5% despite all the Brexit concerns.

Fixed Income

- Bund Futures trade 161.70 down 8 ticks in quiet trade on the last trading day of 2017. The curve continues to steepen slightly following the regional CPI data out of Germany. Further downside targets 161.49 while a reversal targets 162.38 initially then 163.00.

- Friday's liquidity report showed Thursday's excess liquidity fell to €1.779T from €1.796T prior. Use of the marginal lending facility rose to €266M from €216M prior.

Looking Ahead

- 06:00 (BR) Brazil Nov National Unemployment Rate: 12.0%e v 12.2% prior

- 06:00 (PT) Portugal Nov Industrial Production M/M: No est v -2.2% prior; Y/Y: No est v 3.5% prior

- 06:00 (PT) Portugal Nov Retail Sales M/M: No est v -2.3% prior; Y/Y: No est v 1.8% prior

- 06:00 (UK) DMO does not hold Bill auction (next scheduled for Jan 5th)

- 06:30 (IN) India Weekly Forex Reserves - 06:45 (US) Daily Libor Fixing

- 07:00 (CL) Chile Nov Unemployment Rate: 6.5%e v 6.7% prior

- 07:00 (CL) Chile Nov Manufacturing Production Y/Y: -0.8%e v +0.6% prior; Industrial Production Y/Y: 2.4%e v 5.0% prior

- 07:00 (CL) Chile Nov Total Copper Production: No est v 512.7K prior

- 08:00 (DE) Germany Dec Preliminary CPI M/M: 0.5%e v 0.3% prior; Y/Y: 1.5%e v 1.8% prior

- 08:00 (DE) Germany Dec CPI EU Harmonized M/M: 0.6%e v 0.3% prior; Y/Y: 1.4%e v 1.8% prior

- 08:00 (RU) Russia Dec Preliminary CPI M/M: 0.5%e v 0.2% prior; Y/Y: 2.6%e v 2.5% prior; CPI YTD: 2.6%e v 2.1% prior

- 08:00 (RU) Russia Q3 Final GDP Y/Y: 1.8%e v 1.8% prelim

- 08:00 (RU) Russia Q3 Final Current Account: No est v $1.2B prelim

- 08:00 (IN) India announces upcoming Bill auction (held on Wed)

- 08:30 (US) Weekly USDA Net Export Sales

- 10:00 (MX) Mexico Nov Net Outstanding Loans (MXN): No est v 3.936T prior

- 11:00 (CO) Colombia Nov National Unemployment Rate: No est v 8.6% prior; Urban Unemployment Rate: 9.2%e v 9.5% prior

- 13:00 (US) Weekly Baker Hughes Rig Count data

- 15:30 (MX) Mexico Nov YTD Budget Balance (MXN): No est v 108.5B prior

Weekend data

Sat:

- 20:00 (CN) China Dec Manufacturing PMI: 51.6e v 51.8 prior; Non-Manufacturing: 54.7e v 54.8 prior

Sun:

- 19:00 (KR) South Korea Dec Tarde Balance: $7.1Be v $7.8B prior; Exports Y/Y: 9.8%e v 9.6% prior; Imports Y/Y: 12.0%e v 12.3% prior

New Year's Day

- 00:00 (PE) Peru Dec CPI M/M: 0.2%e v -0.2% prior; Y/Y: 1.4%e v 1.5% prior

Australian Follar : Monetary Policy, Iron Ore, and Chinese Risks

The aussie enjoyed a decent run in 2017, but it is an open question if this will remain the case in 2018. Expectations for declines in iron ore prices and the prospect of a notable slowdown in the Chinese economy suggest that the risks surrounding the AUD over the coming year may be tilted to the downside. That said, many variables could change that and spell good news for the currency, including a potential hawkish shift in the RBA's language.

The Australian dollar is set to finish 2017 slightly higher against a basket of major currencies, despite the drop in iron ore prices and the Reserve Bank of Australia (RBA) showing no signs that it is ready to raise rates anytime soon. What are the future catalysts for the AUD, and how is it likely to fare in 2018?

Monetary policy may be the single most important variable to watch, with any change in the RBA's neutral tone likely to trigger massive movements in the aussie. The market currently sees roughly a 60% probability for a quarter-point rate increase by the end of 2018, according to Australia's overnight index swaps. However, for the RBA to begin hinting at rate hikes, wages need to accelerate substantially first, something that appears doubtful given there is still slack in the labor market. The Bank is also concerned about consumption growth, as household debt levels are already very high. Thus, it remains largely a guessing game as to whether rates will rise in 2018. Staying on hold would likely come as a disappointment since market pricing is leaning more towards a hike, and could prove AUD-negative.

Turning to iron ore, Australia's largest export, the outlook for prices appears rather gloomy. According to futures contracts on the Chicago Mercantile Exchange (CME), market participants are anticipating a sizeable drop in prices over 2018, something in line with the latest price forecasts from Thomson Reuters. In isolation, a fall in iron ore prices usually works against the Aussie, as it implies reduced revenues for Australian exporters and less demand for the AUD itself.

What happens in China will also be crucial for the aussie. The consensus among the economics community seems to be that Chinese growth is set to slow as the nation restricts credit in order to deleverage the economy and address financial stability risks. A slowdown in Australia's largest trading partner could also exert downward pressure on the AUD, as export growth would likely take a hit. Bearing all the above in mind, the risks surrounding the AUD in 2018 may be tilted to the downside. Aussie/dollar could drift lower and perhaps target the 0.7330 territory, marked by the lows of May. On the other hand, a more optimistic tone by the RBA, a less pronounced slowdown in China, or rising iron ore prices could all trigger advances. In such a scenario, the pair may aim for the 0.8100 zone.

Canadian Dollar : As Good as it Gets?

The Canadian currency outperformed most of its major peers in 2017. Whether that will continue or reverse in 2018 is likely to depend on monetary policy, the evolution of oil prices, and developments in the NAFTA negotiations. With the market having already priced in a significant degree of monetary tightening, and with oil prices likely to struggle to advance much further from current levels, the loonie may require a fresh positive catalyst to draw support from in order to continue its rally next year.

The Canadian dollar enjoyed a spectacular year in 2017, rallying more than 7% against its US counterpart, as the Bank of Canada (BoC) surprised many investors by raising its benchmark interest rate not once, but twice throughout the year. The continued strength in the nation's economic data and the notable gains in oil prices likely added to the currency's appeal. With the Canadian economy seemingly in a sweet spot, will the CAD extend its bull run into 2018, or give back its hard-earned gains?

The BoC appears set to continue hiking rates next year amid a tight labor market, an almost-closed output gap, and intensifying inflationary pressures. The main question for CAD-traders is whether the Bank will deliver more, or less tightening than investors currently anticipate. At the time of writing, markets have fully priced in three quarter-point rate hikes in 2018, according to Canada's overnight index swaps. Importantly, this implies that for the currency to strengthen further due to monetary policy next year, the BoC must deliver four quarter-point hikes, which seems a little too optimistic even factoring in Canada's strong economy. Simply raising rates three times will likely have little impact on the loonie as that is already priced in, while anything less than three will probably see the currency weaken.

What about oil? While gains in oil prices benefited the loonie in the past, it is doubtful whether this will remain the case. WTI is currently trading near $60/barrel. Any significant upside from current levels will probably invite US shale producers to step back into the market and increase their production drastically as their profit margins recover, thereby keeping a lid on future price gains. Thus, barring some major surprise from OPEC or any short-term supply disruptions, oil will likely struggle to advance much further in the coming year.

NAFTA negotiations represent another risk for the loonie. Despite some progress on less controversial issues recently, several complex subjects have not even been discussed yet, casting a cloud of uncertainty over the CAD's outlook. That said, it is crucial to note that any breakthrough in these negotiations will likely see the currency surge, as uncertainty dissipates and markets price out the NAFTA "risk premium".

All the above considered, any major rallies in the CAD during 2018 may remain somewhat limited. The BoC may disappoint relative to market expectations, oil prices could correct lower, and NAFTA negotiations appear unlikely to conclude anytime soon. Such a scenario could see dollar/loonie ending the year slightly higher, perhaps close to its recent highs at 1.2900. On the flipside, some material progress in the NAFTA talks or perhaps more rate hikes than expected by the BoC, could see the cross sinking back to its September lows near 1.2060.

Dollar Index Tumbles to 3-Month Low; FTSE at Fresh Record Highs

Here are the latest developments in global markets:

FOREX: The dollar index stretched its downtrend toward a fresh three-month low of 92.34 (-0.26%) as investors stood less confident on the outlook of the US economy, while gains in the euro and the pound pressured the index even further. Euro/dollar hit a three-month high of 1.1986 (+0.33%) and pound/dollar (+0.41%) surged to a three-week high of 1.3511. The kiwi, the aussie and the loonie drifted higher relative to the greenback to levels last seen in October.

STOCKS: The pan-European STOXX 600 and the blue-chip Euro STOXX 50 were flat at 1000 GMT, though, they were on track to post the strongest annual performance in four years. The Italian FTSE MIB tumbled by 0.46% after Italy's president dissolved the parliament on Thursday, opening the way for elections on March 4. The British FTSE 100 jumped to a fresh record high driven by rising tech shares and was 0.17% up on the day. The German DAX declined by 0.24% and the Spanish IBEX 35 fell by 0.30%. Futures on major Wall Street indices were all pointing to the upside.

COMMODITIES: Oil prices remained up on the day near mid-2015 peaks. WTI crude and Brent were last seen at $60.15 (+0.52%) and $66.47 (0.45%) per barrel respectively. Gold was building momentum on the back of a weaker dollar at $1,296.55 per ounce (+0.15%).

Day ahead: German CPI index & Baker Hughes oil rig count gather attention

Looking forward, market moves are expected to be limited in the last trading day of the year, with German preliminary inflation figures and the US Baker Hughes oil rig count being the only to gather attention. German and UK are scheduled to close earlier than usual during today's trading.

According to forecasts, the German CPI due at 1300 GMT is said to slow down to 1.5% on a yearly basis in December compared to 1.8% seen in November. If true, this would be the lowest level reached since May. On a monthly basis though, the measure is anticipated to climb by 0.2 percentage points to a nine-month high of 0.5%. The harmonized equivalent gauges will also accompany the above data.

In oil markets, the Baker Hughes company will give an indication of the number of active US oil rigs for the week ending December 22. The measure has been trending at two-year highs during 2017.

GBPUSD Sees Strengthening Bullish Momentum In Near-Term

GBPUSD is edging sharply higher since last Wednesday, adding around 1% relative to Tuesday's close and being well on track to post its fourth green day in a row. The price is still trading comfortably above the ascending trend line, which is roughly holding since March and is currently approaching the next immediate resistance level at 1.3550. The current risk is to the upside and the price could extend its gains to the 1.3655 barrier.

On the downside, support could come around 1.33, this being an area of congestion recently as well as one encapsulating a bottom and a couple of peaks from the recent past. Further below and looking at the bigger picture, if the pair slips below the rising trend line, this could eventually open the way for the 1.3060 support level.

In the daily time frame, trend and momentum indicators are in bullish territory, although the MACD oscillator is looking increasingly neutral. The RSI indicator has turned higher and is moving towards the 70 level. The three simple moving averages (50, 100 and 200) are bullishly aligned.

Having a brief look at the weekly time frame, cable is on the path to post the second consecutive bullish week and the RSI indicator is endorsing the case for further upside movement.

Canadian Dollar Hits 10-Week High

The Canadian dollar rally continues on Christmas week, as the currency has posted six straight winning sessions. In the Friday session, USD/CAD is trading at 1.2537, down 0.27%. With no Canadian or US indicators, on the schedule, traders can expect a quiet end to the last week of 2018.

Christmas week has been marked by thin trading, and there are no Canadian events this week. Still, the Canadian dollar is on the move, and has posted strong gains of 1.5%. Canada’s GDP in October disappointed, with a flat reading of 0.0%. Still, recent consumer indicators have been strong. Retail Sales sparkled with a gain of 0.8% in October, well above the forecast of 0.4%. This was the indicator’s highest gain since April. As well, CPI improved to 0.3% in November, marking a five-month high. This edged above the estimate of 0.2%. The Canadian dollar has enjoyed an excellent December, but could face some headwinds next month, as the Federal Reserve is widely expected to raise interest rates at its January meeting, following the rate hike earlier in December.

The US dollar remains under pressure, as key indicators this week were a mix. On Thursday, unemployment claims were unchanged at 245 thousand, above the forecast of 241 thousand. Earlier in the week, consumer confidence slowed, but housing numbers remained strong. New Home Sales sparkled, with a gain of 733 thousand. This easily beat the estimate of 654 thousand, and was the highest reading since September 2007.

DAX Dips Lower, Markets Eye German CPI

The DAX is lower in the Friday session. Currently, the index is at 12,933.50, down 0.33% on the day. The final trading day of 2017 has just one key event, German Preliminary CPI. The indicator is expected to accelerate to 0.5% in December. In the eurozone, M3 Money Supply and Private Loans both matched their estimates of 4.9% and 2.8%, respectively.

In a nod to stronger economic conditions in the eurozone, the ECB announced in October that it would begin tapering its monthly bond purchases in January 2018, from EUR 60 billion to 30 billion. Mario Draghi & Co. are playing it safe, however, as the ECB has extended the purchases through September 2018. If inflation remains below the ECB target of around 2.0%, the purchases will likely continue after that date. Economic growth in the bloc has been steady, with GDP expanding 0.7% in the third quarter, after a 0.6% in the second quarter. Of note, the ECB upwardly revised its 2018 growth forecast from 1.8% to 2.3%.

Investors have given a thumbs-up to the stronger German and eurozone economies, and the stock markets have responded with substantial gains. The DAX has climbed an impressive 13.8% in 2018. Data in the fourth quarter has been strong so far, and expectations are that the positive trend will continue into 2018, which bodes well for the DAX.

Euro Pushes To 13-Week High, German CPI Next

EUR/USD continues to rally, as the pair trades at its highest level since September 22. In Friday trade, EUR/USD is trading at 1.1980, up 0.33% on the day. The final trading day of 2017 has just one key event, German Preliminary CPI. The indicator is expected to accelerate to 0.5% in December. In the eurozone, M3 Money Supply and Private Loans both matched their estimates of 4.9% and 2.8%, respectively.

Christmas week is traditionally light on economic releases and the markets are in slow gear until after New Years’. Still, the euro has looked sharp and is up about 1.0% this week, with the symbolic 1.20 line in striking distance. The US dollar has been under pressure, and disappointing consumer confidence and unemployment numbers didn’t help the cause. We could see the greenback rebound in January, as the US economy continues to show strong growth and the Federal Reserve is widely expected to raise rates for a second straight month at its January policy meeting.

In a nod to stronger economic conditions in the eurozone, the ECB announced in October that it would begin tapering its monthly bond purchases in January, from EUR 60 billion to 30 billion. Mario Draghi & Co. are playing it safe, however, as the ECB has extended the purchases through September 2018. If inflation remains below the ECB target of around 2.0%, the purchases will likely continue after that date. Economic growth in the bloc has been steady, with GDP expanding 0.7% in the third quarter, after a 0.6% in the second quarter. Of note, the ECB upwardly revised its 2018 growth forecast from 1.8% to 2.3%.

EUR/USD Higher On Year’s End Profit Taking

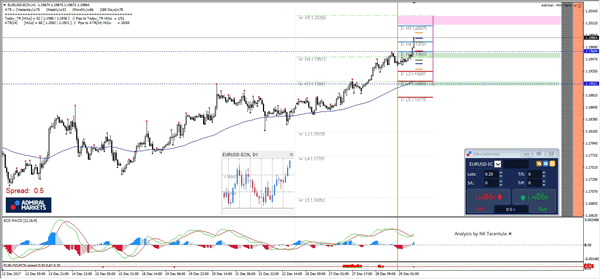

The previous EUR/USD analysis went exactly as expected and EUR/USD is challenging 1.2000 zone. Month's end fixing and additional yearly profit taking could also spur a new wave of sellers later in the day. Bullish rejections could happen within 1.1950-60 zone and 1.1900-10 while we may see sellers within 1.2007-1.2027. However, if the price proceeds upwards without any sign of making a u-turn, then traders should watch daily resistance levels (historical swing highs) and divergence around that particular levels. An excellent tool to use for a daily chart overlay on a trading timeframe is Admiral Mini Chart.

Watch for volatility today as the New Year is approaching. We might see larger price swings that are almost impossible to predict because they are influenced by the lighter trading volumes.

EURUSD Analysis: Tests Wedge Boundary

After bouncing off the 61.8% Fibo retracement at 1.1887 late on Wednesday, the broadly-base weakness of the US Dollar allowed the Euro to close Thursday’s trading session with a 55-pip gain. The second part of the session, however, did not show much change in the pair’s direction, as it remained fluctuating in the 1.1940/60 area during this time. Even though some technical indicators are still flashing strongly bullish signals, the rate is unlikely to surge massively. The nearest resistance—the weekly R3 located at 1.1982—could be the ultimate daily high for today. Meanwhile, the rate should edge lower in line with the aforementioned wedge. This fall, however, is not expected to be significant, as its lower boundary is supported by the weekly R1 and the 55-hour SMA circa 1.1920.