Sample Category Title

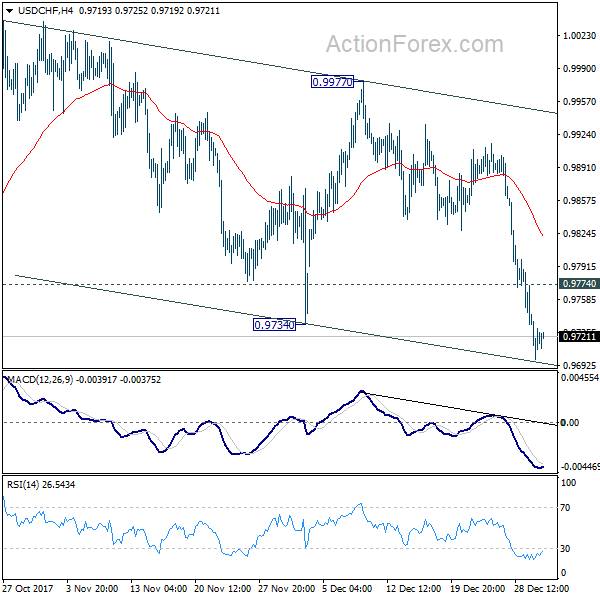

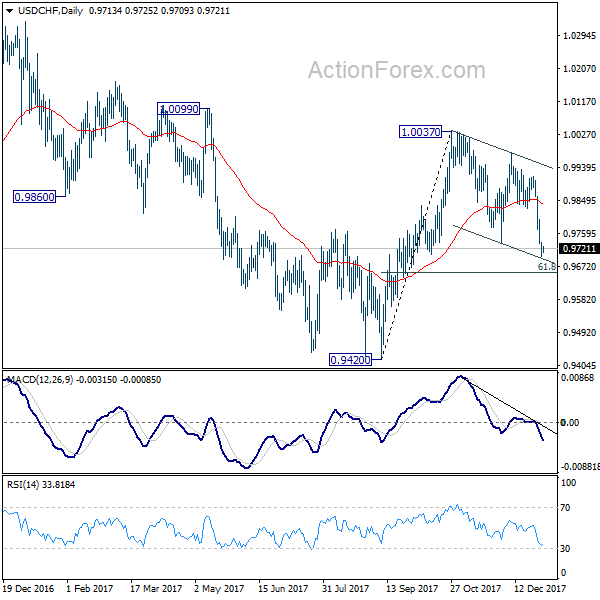

USD/CHF Daily Outlook

Daily Pivots: (S1) 0.9694; (P) 0.9721; (R1) 0.9744; More....

Intraday bias in USD/CHF remains on the downside as correction from 1.0037 could extend lower. At this point, we'd expect strong support from 61.8% retracement of 0.9420 to 0.1.0037 at 0.9656 to contain downside and bring rebound. On the upside, above 0.9774 minor resistance will turn intraday bias neutral first. But break of 0.9977 is needed to confirm completion of the correction. Otherwise, risk will stay on the downside in near term.

In the bigger picture, range trading continues between 0.9420/1.0342. At this point, 0.9420 appears to be a strong support level. Therefore, in case of decline attempt, we don't expect a firm break of this level. Nonetheless, strong break of 1.0342 is also needed to confirm upside momentum. Otherwise, medium term outlook will stay neutral.

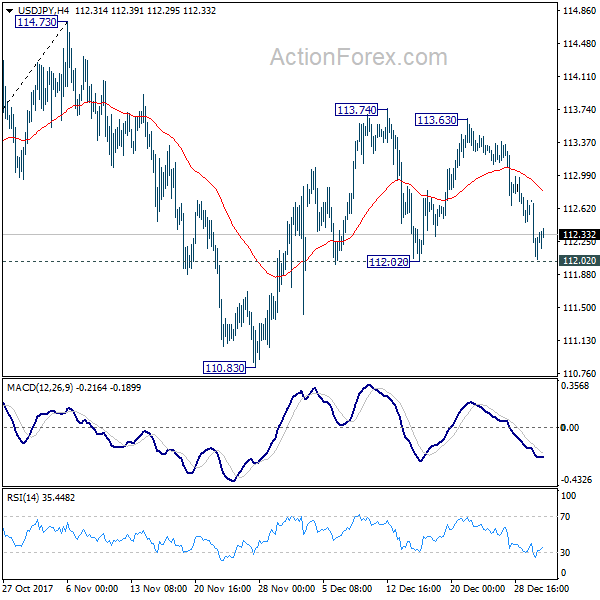

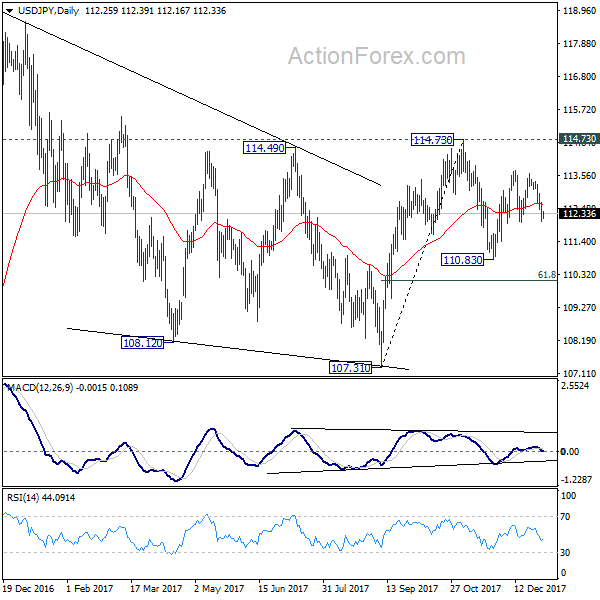

USD/JPY Daily Outlook

Daily Pivots: (S1) 111.96; (P) 112.37; (R1) 112.70; More...

At this point, USD/JPY is staying in range of 112.02/113.74 and intraday bias remains neutral first. Near term outlook stays bullish as long as 112.02 support holds. Break of 113.74 will resume the rebound from 110.83 and target 114.73 key resistance. Decisive break there will carry larger bullish implications. However, break of 112.02 will likely extend the corrective pattern from 114.73 with another leg through 110.83 support.

In the bigger picture, we're holding on to the view that correction from 118.65 is completed at 107.31. And medium term rise from 98.97 (2016 low) is going to resume soon. Sustained break of 114.73 should affirm our view and send USD/JPY through 118.65. However, break of 107.31 will dampen this view and extend the medium term fall back to 98.97 low.

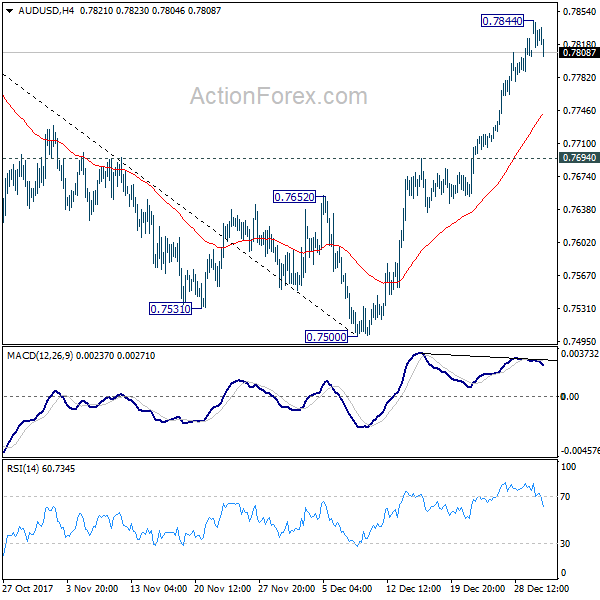

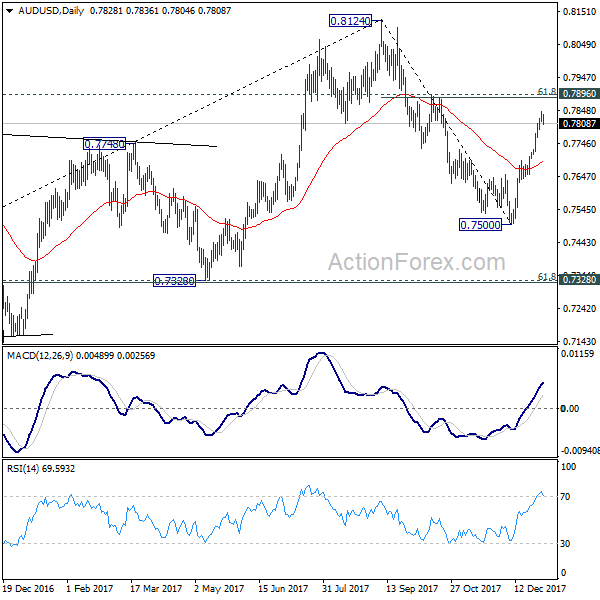

AUD/USD Daily Outlook

Daily Pivots: (S1) 0.7799; (P) 0.7821; (R1) 0.7852; More...

AUD/USD retreats mildly after hitting 0.7844 and intraday bias is turned neutral first. Another rise could still be seen. But considering bearish divergence condition in 4 hour MACD, upside should be limited by 0.7896 cluster resistance (61.8% retracement of 0.8124 to 0.7500 at 0.7886) to form a short term top. Meanwhile, break of 0.7964 support will suggest that rebound from 0.7500 has completed. In such case, intraday bias will be turned back to the downside for retesting 0.7500.

In the bigger picture, we're still slightly favoring the case that corrective rise from 0.6826 medium term bottom is likely completed at 0.8124, after hitting 55 month EMA (now at 0.8032). But stronger than expected rebound from 0.7500 is dampening this bearish view. On the downside, break of 0.7500 will target 0.7328 key cluster support (61.8% retracement 0.6826 to 0.8124 at 0.7322) to confirm this bearish case. But break of 0.8124 will extend the rise from 0.6826 to 38.2% retracement of 1.1079 (2011 high) to 0.6826 (2016 low) at 0.8451 before completion.

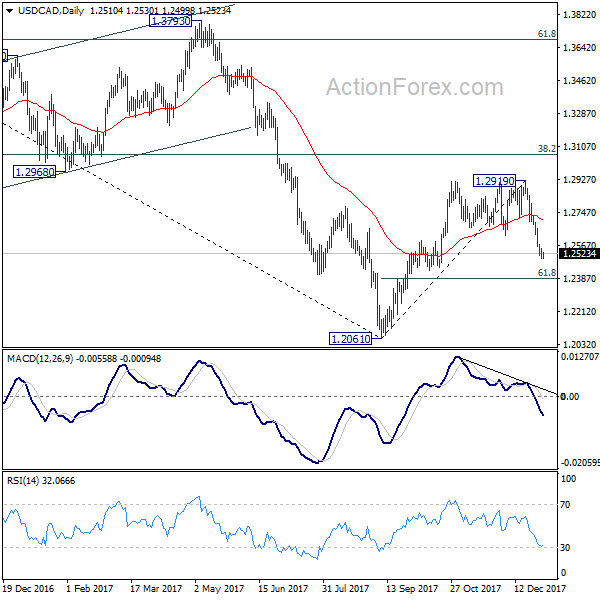

USD/CAD Daily Outlook

Daily Pivots: (S1) 1.2482; (P) 1.2528; (R1) 1.2557; More....

USD/CAD drops to as low as 1.2499 so. It's losing some downside momentum on oversold condition in 4 hour RSI. But intraday bias stays on the downside as long as 1.2566 minor resistance holds. Current fall from 1.2919 would extend to 61.8% retracement of 1.2061 to 1.2919 at 1.2389 or possibly below. On the upside, above 1.2566 will turn intraday bias neutral first.

In the bigger picture, we're still favoring the case that USD/CAD has defended 50% retracement of 0.9406 (2011 low) to 1.4689 (2016 high) at 1.2048. And with 1.2048 intact, we'd favor the case that fall from 1.4689 is a correction. With that in mind, fall from 1.2919 is viewed as a correction. Hence, we're not anticipating a break of 1.2061 low. In the long run, USD/CAD should have another medium term rise to take on 38.2% retracement of 1.4689 to 1.2061 at 1.3065.

Dollar Trying to Recover after New Year Selloff, FOMC Minutes and ISM Manufacturing Watched

Dollar is trying to recover in Asian session today after the steep new year selloff. Nonetheless, the greenback remains the second weakest one for the week, just next to Kiwi. S&P 500 and NASDAQ closed at records high at 26951.81 and 7006.90 overnight. DOW also gained 104.79 pts or 0.42% to 24824.01. 10 year yield staged a strong rebound by gaining 0.06 to 2.465 but that was mainly driven by surge in European yields, including Germany and UK. In other markets, gold breached 1320 handle before retreating mildly today. WTI crude oil is also holding above 60 handle.

ECB Nowotny: QE may end in 2018

ECB Governing Council member Ewald Nowotny said in a newspaper interview that the central bank could end the asset purchase program this year and there is continuous improvements in growth in Eurozone. Inflation is still expected to miss the 2% target ahead. But Nowotny said that "we should not see that too dogmatically." Instead, "if the economy continues to do so well, we could let the program run out in 2018". Meanwhile, he also warned that funds are "flooding" into European stock markets and warned of risks of bubble.

CDU and SPD still at odds for grand coalition

In Germany, leaders of Chancellor Angela Merkel's CDU/CSU will meet today to prepare for the exploratory coalition talk with SPD scheduled for January 7 through 12. The chance for the rebirth of grand coalition seems get dimmer as the two largest parties are still at odds over a couple of issues. SPD deputy leader Thorsten Schaefer-Guembel cited in a newspaper interview the differences with CUD/CSU over tax, healthcare, immigration, Europe and work regulations. And he emphasized that "a minority government remains an option, even if Chancellor Angela Merkel doesn't want to acknowledge that."

And, Wolfgang Steiger, secretary general of CDU's economic council, said that Germany could face "enormous financial burdens for generations" if SPD manages to push through the spending plans in the grand coalition. And he warned that "a grand coalition will be more expensive in the long term than a minority government."

UK in talks to join TPP

In UK, it's reported that the government is in talks to join the so called Trans-Pacific Partnership for post-Brexit international trades. British Trade Minister Greg Hands said despite the geographical difference, "nothing is excluded in all of this," and "with these kind of plurilateral relationships, there doesn't have to be any geographical restriction." The department of international trade also said that "it is early days, but as our trade policy minister has pointed out, we are not excluding future talks on plurilateral relationships."

But the initiative drew criticism from other politicians. Shadow Trade Minister Barry Gardiner complained that "this plan smacks of desperation. These people want us to leave a market on our doorstep and join a different, smaller one on the other side of the world. It's all pie in the sky thinking."

The TPP is renamed as Comprehensive and Progressive Agreement for Trans-Pacific Partnership (CPTPP) after the US withdrew last year under the decision of President Donald Trump. There are eleven remaining members including Australia, Brunei, Canada, Chile, Japan, Malaysia, Mexico, New Zealand, Peru, Singapore and Vietnam. A partial agreement was reached last November without US participation.

Looking ahead: FOMC Minutes and PMIs

FOMC minutes for December meeting will be a major focus of the day. Fed raised interest rate by the third time last year in December. The biggest difference that time was that Chicago Fed President Charles Evans joined Minneapolis Fed President Neel Kashkari in dissenting. What both have said during the meeting could be something of interest. Other than that, the minutes shouldn't reveal anything new given that there was a press conference, with new projections released after the meeting.

On the data front, Swiss will release PMI manufacturing while UK will release construction PMI. Germany will release unemployment. US ISM manufacturing will also be a focus and a strong set of number is needed to give Dollar a life.

USD/CAD Daily Outlook

Daily Pivots: (S1) 1.2482; (P) 1.2528; (R1) 1.2557; More....

USD/CAD drops to as low as 1.2499 so. It's losing some downside momentum on oversold condition in 4 hour RSI. But intraday bias stays on the downside as long as 1.2566 minor resistance holds. Current fall from 1.2919 would extend to 61.8% retracement of 1.2061 to 1.2919 at 1.2389 or possibly below. On the upside, above 1.2566 will turn intraday bias neutral first.

In the bigger picture, we're still favoring the case that USD/CAD has defended 50% retracement of 0.9406 (2011 low) to 1.4689 (2016 high) at 1.2048. And with 1.2048 intact, we'd favor the case that fall from 1.4689 is a correction. With that in mind, fall from 1.2919 is viewed as a correction. Hence, we're not anticipating a break of 1.2061 low. In the long run, USD/CAD should have another medium term rise to take on 38.2% retracement of 1.4689 to 1.2061 at 1.3065.

Economic Indicators Update

| GMT | Ccy | Events | Actual | Forecast | Previous | Revised |

|---|---|---|---|---|---|---|

| 08:30 | CHF | PMI Manufacturing Dec | 64.5 | 65.1 | ||

| 08:55 | EUR | German Unemployment Change Dec | -13k | -18k | ||

| 08:55 | EUR | German Unemployment RateDec | 5.50% | 5.60% | ||

| 09:30 | GBP | Construction PMI Dec | 53.1 | 53.1 | ||

| 15:00 | USD | Construction Spending M/M Nov | 0.50% | 1.40% | ||

| 15:00 | USD | ISM Manufacturing Dec | 58.2 | 58.2 | ||

| 15:00 | USD | ISM Prices Paid Dec | 64.5 | 65.5 |

Streaking Gold Kicks Off 2018 With Gains

It's up, up, up for gold prices. The base metal has not had a losing session since December 19 and the upward movement has continued on Tuesday. In the North American session, the spot price for an ounce of gold is $ 1311.93, up 0.64% on the day. On the release front, today's sole event was Final Manufacturing PMI, which climbed to 55.1, edging above the estimate of 55.0 points. This marked the highest level since March 2015. On Wednesday, the Federal Reserve will publish the minutes of its December meeting, and the US will release ISM Manufacturing PMI, a key manufacturing report.

Gold climbed 2.2% percent in December, and the upward trend has continued on Tuesday, with gold taking advantage of a broadly weaker US dollar. Gold has punched above $1310 earlier on Tuesday, for the first time since late September. With the US economy expanding above 3% and the Fed poised to raise rates for a second straight month, the gold rally has surprised many experts, as stronger economic conditions usually translate into stronger risk appetite, at the expense of gold prices. On Friday, the US releases wage growth and non-farm payrolls, and if the readings beat expectations, the dollar could recover some of its recent losses and send gold prices lower.

Traders can expect the Federal Reserve in the headlines a fair amount early in the New Year. Investors will be monitoring the Fed on Wednesday, with the release of the minutes of the December meeting. At that meeting, the Fed raised rates by 25 basis points, to a range between 1.25% and 1.50%. The hike marks a vote of confidence in the US economy, and if the minutes are hawkish, the US dollar could gain ground. If the US economy continues to expand at a clip exceeding 3%, the Fed is expected to raise rates up to four times in 2018. Currently, the CME Group has priced in a January rate hike at 98.5%. Although inflation remains well below the Fed target of 2.0%, outgoing Fed Chair Janet Yellen and other FOMC members have said that they expect that the strong labor market will lead to higher inflation. Although this is yet to materialize, of significance to the markets is the commitment of the Fed to press ahead with rate hikes, despite low inflation.

British Pound Gains Ground Despite Soft U.K. Manufacturing PMI

The British pound has started the New Year with gains. In Tuesday's North American trade, GBP/USD is trading at 1.3580, up 0.55% on the day. The pound is currently at its highest level since mid-September. On the release front, British Manufacturing PMI slowed to 56.3, shy of the forecast of 58.0 points. In the US, today's sole event was Final Manufacturing PMI, which climbed to 55.1, edging above the estimate of 55.0 points. This marked the highest level since March 2015. On Wednesday, the UK releases Construction PMI. In the US, the FOMC will publish the minutes of its December meeting, and we'll get a look at ISM Manufacturing PMI.

The new trading week kicked off in the UK with Manufacturing PMI. Although the index missed expectations, the reading pointed to expansion in the manufacturing sector, which has received a boost from strong global demand for British exports. As well, the weak pound has also made British products less expensive. The markets are expecting continued growth in the construction and services sectors later this week.

Traders can expect the Federal Reserve in the headlines a fair amount early in the New Year. Investors will be monitoring the Fed on Wednesday, with the release of the minutes of the December meeting. At that meeting, the Fed raised rates by 25 basis points, to a range between 1.25% and 1.50%. The hike marks a vote of confidence in the US economy, and if the minutes are hawkish, the US dollar could gain ground. If the US economy continues to expand at a clip exceeding 3%, the Fed is expected to raise rates up to four times in 2018. Currently, the CME Group has priced in a January rate hike at 98.5%. Although inflation remains well below the Fed target of 2.0%, outgoing Fed Chair Janet Yellen and other FOMC members have said that they expect that the strong labor market will lead to higher inflation. Although this is yet to materialize, of significance to the markets is the commitment of the Fed to press ahead with rate hikes, despite low inflation.

Yen Improves To 3-Week High, Markets Eye Fed Minutes

USD/JPY has started the week with losses. In the Tuesday session, USD/JPY is trading at 112.11, down 0.51%. On the release front, there are no Japanese events on the schedule, and Japanese bank are closed for a holiday. In the US, today’s sole event was Final Manufacturing PMI, which climbed to 55.1, edging above the estimate of 55.0 points. This marked the highest level since March 2015. On Wednesday, the FOMC will publish the minutes of its December meeting, and we’ll get a look at ISM Manufacturing PMI.

Japanese inflation indicators continue to point upwards. The final Japanese event of the year was Bank of Japan Core Inflation, which the BoJ relies on to measure inflation. The indicator climbed 0.6%, edging above the estimate of 0.5%. This marked a 3-month high. Earlier last week, other inflation indicators also beat their estimates, underscoring that inflation is on the move. Still, the BoJ has made it abundantly clear that it will not tighten its ultra-accommodative monetary policy until inflation is close to the Bank’s 2 percent inflation target. The minutes of the October meeting indicated that most members favored a continuation of the current ultra-accommodative policy. This could weigh on the yen, as other central banks, such as the ECB, the Federal Reserve and the Bank of Canada have tightened policy in recent months, widening divergence with the Bank of Japan.

Traders can expect the Federal Reserve in the headlines a fair amount early in the New Year. Investors will be monitoring the Fed on Wednesday, with the release of the minutes of the December meeting. At that meeting, the Fed raised rates by 25 basis points, to a range between 1.25% and 1.50%. The hike marks a vote of confidence in the US economy, and if the minutes are hawkish, the US dollar could gain ground. If the US economy continues to expand at a clip exceeding 3%, the Fed is expected to raise rates up to four times in 2018. Currently, the CME Group has priced in a January rate hike at 98.5%. Although inflation remains well below the Fed target of 2.0%, outgoing Fed Chair Janet Yellen and other FOMC members have said that they expect that the strong labor market will lead to higher inflation. Although this is yet to materialize, of significance to the markets is the commitment of the Fed to press ahead with rate hikes, despite low inflation

GOLD – Bullish, Remains On The Offensive

GOLD - The commodity faces further upside pressure but with caution of a corrective pullback. On the downside, support comes in at the 1,300.00 level where a break will turn attention to the 1,290.00 level. Further down, a cut through here will open the door for a move lower towards the 1,280.00 level. Below here if seen could trigger further downside pressure towards the 1,270.00 level. Conversely, resistance resides at the 1,320.00 level where a break will aim at the 1,330.00 level. A turn above there will expose the 1,340.00 level. Further out, resistance stands at the 1,350.00 level. Its daily RSI is bullish and pointing higher suggesting further strength. All in all, GOLD looks to strengthen further on correction.

New Zealand Dollar : All Eyes on the RBNZ

The kiwi dollar retreated in 2017 amid falling dairy prices, political uncertainties, and a less-than-hawkish stance by the RBNZ. Are better times ahead for the NZD? That may depend primarily on whether and when the Reserve Bank will begin to raise interest rates. Market pricing is leaning towards a rate hike in 2018, but the RBNZ's own forecasts suggest that will only happen in mid-2019. The market and the Bank are currently at odds, and something has to give.

The New Zealand dollar finished 2017 on the back foot, underperforming all its major peers besides the greenback. Dairy prices tumbled, the recent general election introduced considerable political uncertainty, and the Reserve Bank of New Zealand (RBNZ) refrained from providing any optimistic signals that rate hikes are looming. The Bank's verbal warnings regarding the strength of the NZD and hints of direct FX intervention also played a role in the kiwi's underperformance. Is a recovery, or further slump on the cards for 2018?

Kicking off with monetary policy, the RBNZ looks to be going nowhere fast. The Bank's latest forecasts suggest interest rates may only begin to rise in mid-2019. Indeed, despite the rapid tightening in the nation's labor market this year, wages hardly accelerated while core inflation remains subdued. Unless this changes drastically in 2018, it's unlikely that the RBNZ will hurry to raise rates.

However, market pricing is not in line with this view. New Zealand's overnight index swaps indicate a 72% probability for a quarter-point rate increase by the end of 2018. This has two major implications. First, if the Bank remains on hold as its own estimates suggest, that would come as a negative surprise to the market, thereby weighing on the NZD. Second, even if the Bank does act, so long as it only delivers one hike, any positive reaction in the kiwi could be relatively limited as most of this is priced in already. Most importantly, any major rallies in the NZD will likely see the RBNZ talking down the currency again, on concerns that a higher exchange rate could act as a drag on inflation and growth.

In terms of dairy products - New Zealand's biggest export - not much is expected by futures contracts. Looking at whole milk powder futures on the New Zealand Derivatives Exchange (NZX), prices are expected to finish 2018 practically unchanged. Thus, absent some major surprise that alters this outlook, commodity prices seem unlikely to affect the kiwi much over the year.

Finally, the new Government is not something to overlook. The NZD plunged after the election, as uncertainty over the new administration's policies set in. Some concerns were indeed justified, as the new regime soon cancelled tax cuts scheduled for 2018, and announced it will expand the RBNZ's mandate to include full employment in addition to its price stability target. Importantly though, the administration's agenda has since become much clearer in terms of what it will seek to implement, alleviating some uncertainty.

Taking everything together, downside risks seem to outweigh the upside ones for NZD, albeit not significantly. Kiwi/dollar could finish 2018 close to 0.6800, a level that acted as a reliable support barrier in 2017. On the other hand, if upside risks do materialize, for instance by the RBNZ raising interest rates or by milk prices rallying, the pair could surge and challenge the 0.7360 territory. However, a break above that hurdle could cause the Bank to intervene verbally by voicing concerns regarding the exchange rate, thereby keeping any further gains in check.