Sample Category Title

Elliott Wave Analysis On Crude Oil and S&P500

Good day traders and a happy new year!

Crude oil is bullish and unfolding a nice clear five wave pattern, which we labeled as a higher degree wave 5) in progress. Current strong five-wave rally that is on display away from 57.60 level can be labeled as black sub-wave 3 of 5), with potential top and resistance coming in at around the upper Elliott wave channel line. From there, a new three-wave pullback as black wave 4 can follow, and search for potential support and a turning point region around the 60.27/60.71 level.

Crude oil, 1h

S&P500 is strongly and sharply turning higher, away from 2672 base for former wave 4. Current strong rally can now approach levels near the 2710/2715 region, where Fibonacci projection of 161.8 sits and projects end of black wave 5 and resistance.

S&P500, 1h

Yen Pauses After Gains, Fed Minutes Next

USD/JPY is showing little movement in the Wednesday session, after starting the week with losses. In North American trade, USD/JPY is trading at 112.37, up 0.07%. On the release front, the first major US indicator in 2018 pointed higher. ISM Manufacturing PMI improved to 59.7, beating the forecast of 58.3 points. This marked a 3-month high. Today's key event is the release of the Fed minutes from the December meeting. On Thursday, the focus is on employment numbers, with the release of ADP Nonfarm payrolls and unemployment claims. On Friday, we'll get a look at wage growth and US Nonfarm Payrolls.

As we begin the New Year, what can investors expect from the Bank of Japan? BoJ Governor Haruhiko Kuroda has generally stuck to his script that the Bank will maintain its massive stimulus program until inflation rises, but there have been subtle hints form Kuroda that he could change course, if the economic rebound which marked 2017 continues. The stimulus program has failed to lift inflation above 1%, well below the BoJ inflation target of around 2%. Some analysts expect a 'stealth tapering', whereby the BoJ would reduce asset purchases and tighten policy, but in small, incremental steps. In this way, the BoJ could change its monetary stance, while minimizing market volatility.

The Federal Reserve will be on center stage on Wednesday, with the release of the minutes of the December policy meeting. At that meeting, the Fed raised rates by 25 basis points, to a range between 1.25-1.50%. The hike marks a vote of confidence in the US economy, and if the minutes are hawkish, the US dollar could gain ground. The economy is expanding at an impressive clip of above 3 percent. If this pace continues, the Fed could raise rates up to four times in 2018. Currently, the CME Group has priced in a January rate hike at 98.5%. Despite the rosy economic conditions, inflation has been chronically soft, well below the Fed target of 2 percent. Outgoing Fed Chair Janet Yellen and other FOMC members have said that they expect that the strong labor market will push up wages and trigger higher inflation, but this is yet to happen.

US 500 Index Crosses above 2,700 to Record All-time High; Looking Bullish in Short- and Medium-Term

The US 500 index recorded an all-time high of 2,701.80 during today's trading. A positive close would mark the second straight day of advancing after gaining 0.8% on Tuesday.

The Tenkan- and Kijun-sen lines are positively aligned, with the former being above the latter. This is pointing to positive momentum in the short-term. The stochastics are also painting a bullish picture in the very-short-term: the %K line has moved above the slow %D line and both lines are heading higher.

Coming into view as potential resistance to upside movements is the 423.6% Fibonacci extension level of the downleg from 2,596.18 to 2,556.21 at 2,725.44. Further above, 2,800 has the capacity to function as a psychological barrier to stronger bullish moves.

On the downside, the range around the current level of the Tenkan-sen at 2,685.00 might act as support; the area around this level was congested recently. Steeper declines could find support around 2,661.12, this being the 261.8% Fibonacci extension of the aforementioned downleg.

The medium-term picture is clearly bullish: the index is in an uptrend – recording higher highs and higher lows – with price action taking place above the 50- and 100-day moving average lines and both lines maintaining a positive slope.

Overall, the index is looking bullish in the short- and medium-term.

Sunset Market Commentary

In technical trade, US and European bonds stabilized after recent losses. Contrary to what was the case recently, German Bunds outperformed US Treasuries. US yields decline between 0.4 bps (2-yr) and 2.3 bps (30-yr). The German yield curve also bull flattens with yields declining between 0.6bps (2-yr) and 4.6 bps (30-yr).

The recent USD decline halted today. EUR/USD came within reach of the 1.2092 2017 top yesterday, but a real test/break didn't occur. German labour data were strong as expected, confirming other evidence of strong growth in Europe's largest economy. They couldn't inspire further euro gains though. Interest rate differentials widened marginally in favour of the dollar. For now this was enough for the USD decline to take a breather. EUR/USD traded in the in the 1.2025 going into the publication of the US manufacturing ISM. The ISM report was strong (59.7), potentially supporting further USD gains.

USD/JPY held a tight sideways trading in the lower half of the 112 big figure. The slight decline in core bond yields combined with a modestly positive risk sentiment kept USD/JPY trading in balance. Japanese markets still enjoyed a banking holding this morning, keeping yen trading at lows levels.

Sterling trading was mostly technical nature. EUR/GBP declined early in the session, inspired by an overall intraday setback of the euro. The pair bottomed in the 0.8850 area. In the same context, cable (currently 1.3530 area) lost slightly ground as the dollar was in better shape across the board. In the afternoon, sterling weakness added to the negative momentum in this cross rate. The UK construction PMI was slightly weaker than expected, but had little impact on sterling trading. Tomorrow's services PMI has more market moving potential.

Ireland sold €4 bn of its 5/2028 bond, the maximum amount targeted. The bond was priced at MS +2bp. The order book amounted above €14bn, showing strong investor buying interest. The strong performance of Irish bonds in the wake of the sale also supported sentiment on other intra-EMU bond markets. Yields spreads versus Germany narrowed marginally with Greece outperforming (-5 bps).

Global equities held a positive bias today. European equities show gains of about 0.5%. The slowdown of the rise of the euro removed a negative factor that weighed on regional equities yesterday. USD equities also opened again in positive territory showing gains of about 0.5%. The Nasdaq again outperforms

News Headlines

The German unemployment rate declined to 5.5% in December, a post-reunification low. The jobless total fell 29K. Only a decline of 13K was expected. The number of vacancies rose to 790k in December, indicating labour shortages in several sectors of the economy.

Growth in Britain's construction sector slowed last month for the first time since September. The IHS Markit/CIPS UK Construction PMI slipped to 52.2. It hit a five-month peak of 53.1 in November. The survey outcome was below the consensus forecast of 53.00.

Polish inflation declined to 2.0% Y/Y in December from 2.5% Y/Y in November. The figure was marginally lower than expected. However, the move mostly reflected a base effect from end 2016 that was not repeated in 2017. The zloty maintained recent gains despite the softer inflation report. EUR/PLN trades in the 4.16 area.

Markets Mixed ahead of FOMC Minutes, Dollar Attempting Weak Rebound

Quick update: Dollar recovers further after ISM manufacturing beat expectation. Price paid component also surged.

The forex markets are trading rather mixed ahead of FOMC minutes. Commodity currencies overtake Europeans as the main driver today, with Aussie and Loonie trading generally higher. Sterling dips on weaker than expected data but remains the second strongest for the week. Dollar is also trying to stage a rebound but stays in red for the week, except versus Swiss Franc. Strength in Dollar's rebound is rather unconvincing. Traders are relatively more active back from holiday. But would likely need more inspirations from today's ISM and Friday's NFP.

FOMC minutes for December meeting will be a major focus of the day. Fed raised interest rate by the third time last year in December. The biggest difference that time was that Chicago Fed President Charles Evans joined Minneapolis Fed President Neel Kashkari in dissenting. What both have said during the meeting could be something of interest. Other than that, the minutes shouldn't reveal anything new given that there was a press conference, with new projections released after the meeting.

North Korea ignored Trump and called South

Geopolitics are largely ignored by the markets. US President Donald Trump responded to North Korea, tweeting that "I too have a Nuclear Button, but it is a much bigger & more powerful one than his (Kim's), and my Button works!" Such comments did nothing to deter the Koreas in rebuilding their dialogue. It's reported that North Korea contacted South Korea authority over a special hotline for the first time in two years. According to Lee Yeon-du, a South Korea's Unification Ministry official, representatives from both countries talked several times today. There were some technical checks ahead of South Korean President Moon Jae-in's proposed talks on January 9 at the border village of Panmujom. That came after Kim Jung-un expressed the openness to join Winter Olympics.

Talks of UK joining TPP heat up

The talks of UK seeking to join the Trans-Pacific Partnership triggered some noises today. International Trade Secretary Liam Fox tried to talk down the speculations as he said the reports were "rather overblown". He added that "it is not full negotiated yet so we will want to see what emerges." But he also emphasized that "we would be foolish to rule anything out. We know that Asia-Pacific will be a very important market and we know a lot of the global growth in the future will come from there."

Trade Minister Greg Hands said despite the geographical difference, "nothing is excluded in all of this," and "with these kind of plurilateral relationships, there doesn't have to be any geographical restriction." The department of international trade also said that "it is early days, but as our trade policy minister has pointed out, we are not excluding future talks on plurilateral relationships."

The TPP is renamed as Comprehensive and Progressive Agreement for Trans-Pacific Partnership (CPTPP) after the US withdrew last year under the decision of President Donald Trump. There are eleven remaining members including Australia, Brunei, Canada, Chile, Japan, Malaysia, Mexico, New Zealand, Peru, Singapore and Vietnam. A partial agreement was reached last November without US participation.

UK construction PMI missed on commercial projects

UK construction PMI dropped to 52.2 in December, down from 53.1 and missed expectation of 53.1. That's also the second disappointing PMI data released this week. Markit maintained that "house building remained a key engine of growth, with residential work expanding for the sixteenth consecutive month in December." However, "latest data indicated a moderate fall in commercial construction, thereby continuing the downward trend seen since July." On the other hand, "civil engineering work stabilized during the latest survey period, which ended a three-month period of decline.

Elsewhere, Swiss manufacturing PMI rose to 65.2 in December, up from 65.1 and beat expectation of 64.5. German unemployment dropped more than expected by -29k in December, unemployment rate was unchanged at 5.5%.

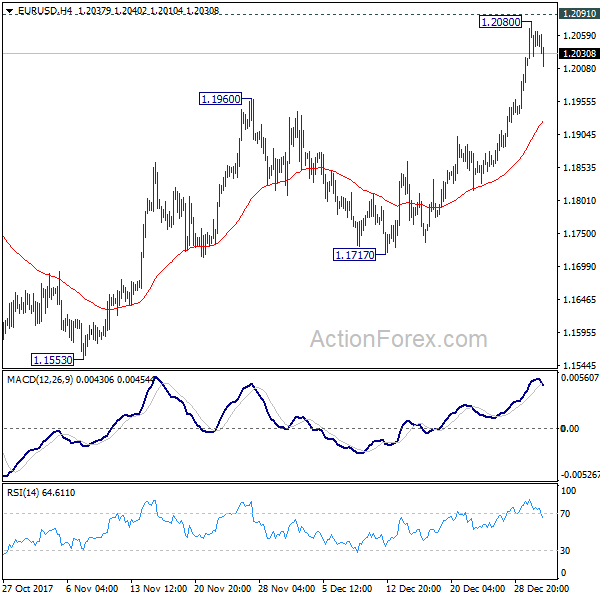

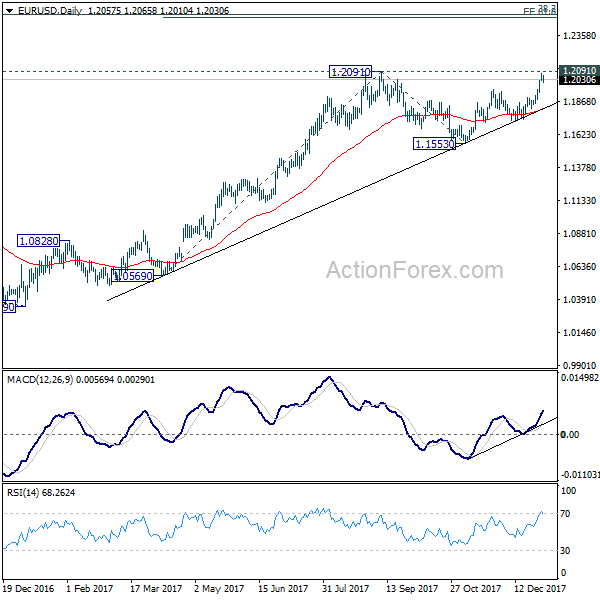

EUR/USD Mid-Day Outlook

Daily Pivots: (S1) 1.2010; (P) 1.2045 (R1) 1.2094; More....

EUR/USD's retreat, with 4 hour MACD crossed below signal line, suggests that a temporary top is formed at 1.2080, ahead of 1.2091 key resistance. Intraday bias is turned neutral first. Some consolidation could be seen but further rise is expected as long as 4 hour 55 EMA (now at 1.1922) holds. Firm break of 1.2091 will confirm medium term rally resumption and target next key fibonacci level at 1.2494/2516. However, sustained break of 4 hour 55 EMA will extend the consolidation pattern from 1.2091 with with another decline through 1.1717 support.

In the bigger picture, rise from 1.0339 medium term bottom is seen as a corrective move for the moment. Therefore, in case of another rally, we'd be expect 38.2% retracement of 1.6039 (2008 high) to 1.0339 (2017 low) at 1.2516 to limit upside and bring reversal. That is also close to 61.8% projection of 1.0569 to 1.2091 from 1.1553 at 1.2494.

Economic Indicators Update

| GMT | Ccy | Events | Actual | Forecast | Previous | Revised |

|---|---|---|---|---|---|---|

| 8:30 | CHF | PMI Manufacturing Dec | 65.2 | 64.5 | 65.1 | |

| 8:55 | EUR | German Unemployment Change Dec | -29k | -13k | -18k | |

| 8:55 | EUR | German Unemployment RateDec | 5.50% | 5.50% | 5.60% | 5.50% |

| 9:30 | GBP | Construction PMI Dec | 52.2 | 53.1 | 53.1 | |

| 15:00 | USD | Construction Spending M/M Nov | 0.80% | 0.50% | 1.40% | 0.90% |

| 15:00 | USD | ISM Manufacturing Dec | 59.7 | 58.2 | 58.2 | |

| 15:00 | USD | ISM Prices Paid Dec | 69 | 64.5 | 65.5 | |

| 19:00 | USD | FOMC Meeting Minutes Dec |

USDCAD Holds Slightly above its 14-Week Low at 1.2500

USDCAD had a strong sell-off in the previous days following the downward retracement of the 1.2915 resistance level. The pair plunged to a new 14-week low near the 1.2500 strong psychological level during Tuesday's session.

It's losing some downside momentum in oversold conditions in the 4-hour chart on the RSI and MACD indicators, but intraday bias remains bearish as long as the 1.2588 minor resistance holds. Moreover, the 100-simple moving average is ready to post a bearish crossover with the 50-SMA indicating for further losses in the short-term chart.

The Current fall from 1.2500 could extend to the 1.2450 support barrier. On the upside, a move above 1.2588 could turn the intraday bias to neutral first before the upside correction. The price may hit the 61.8% Fibonacci retracement level of the last big up-leg with the low at 1.2450 and the high at 1.2915.

In the bigger picture, the MACD oscillator is strengthening its downward momentum (in the daily chart), while the RSI indicator is standing near the 30 level and is slightly sloping to the upside. As a side note, USDCAD printed the second consecutive bearish week and slipped more than 2%.

EURUSD: Loses Upside Pressure, Vulnerable

EURUSD - The pair failed to follow through higher on the back of Tuesday gains on Wednesday. This development leaves it weak and vulnerable to the downside. On the upside, resistance comes in at 1.2050 level with a cut through here opening the door for more upside towards the 1.2100 level. Further up, resistance lies at the 1.2150 level where a break will expose the 1.2200 level. Conversely, support lies at the 1.1950 level where a violation will aim at the 1.1900 level. A break of here will aim at the 1.1850 level. Below here will open the door for more weakness towards the 1.1800. All in all, EURUSD faces further downside weakness on price halt.

Canadian Dollar Steady, Fed Minutes Loom

The Canadian dollar has ticked lower in the Wednesday session. Currently, the pair is trading at 1.2517, up 0.04%. On the release front, there are no Canadian events. In the US, ISM Manufacturing PMI is expected to inch lower to 58.1 points. Today's key event is the release of the Fed minutes from the December meeting. On Thursday, the focus is on employment numbers, with the release of ADP Nonfarm payrolls and unemployment claims. On Friday, there are key events on both sides of the border, led by US Nonfarm Payrolls and Canadian Employment Change.

The Canadian dollar started the New Year on a positive note, as USD/CAD briefly broke below the 1.25 line for the first time since mid-October. The currency enjoyed a respectable 2017, posting gains of 6.6% against its US cousin. Will the positive trend continue in January? With the US economy booming, the Federal Reserve raised rates in December, and another move is expected this month. This will put strong pressure on the Bank of Canada to match with a rate hike, or risk seeing the Canadian dollar lose ground as investors move to a more attractive US dollar.

The Federal Reserve will be in the spotlight on Wednesday, with the release of the minutes of the December policy meeting. At that meeting, the Fed raised rates by 25 basis points, to a range between 1.25-1.50%. The hike marks a vote of confidence in the US economy, and if the minutes are hawkish, the US dollar could gain ground. The economy is expanding at an impressive clip of above 3 percent. If this pace continues, the Fed could raise rates up to four times in 2018. Currently, the CME Group has priced in a January rate hike at 98.5%. Despite the rosy economic conditions, inflation has been chronically soft, well below the Fed target of 2 percent. Outgoing Fed Chair Janet Yellen and other FOMC members have said that they expect that the strong labor market will push up wages and trigger higher inflation, but this is yet to happen.

CAC Stems 3-Day Slide, French Services PMI Next

The CAC index has posted gains in the Wednesday session. Currently, the index is at 5309.50, up 0.40%. There are no French or eurozone events on the schedule. Later in the day, the Federal Reserve releases the minutes from the December policy meeting.

Then New Year marked the start of a taper in the ECB asset-purchase program, with monthly purchases dropping from EUR 60 billion to EUR 30 billion. The program has been extended until September 2018, leaving the markets guessing as to what happens then. As expected, the taper has sent European bond yields sharply higher. Benoit Coeure, who is in charge of ECB bond purchases, stated on the weekend that there was a "reasonable chance" that the ECB would terminate the program in September. If other policymakers reiterate this hawkish stance, we could see some gains in European stock markets.

The Federal Reserve will be in the spotlight on Wednesday, with the release of the minutes of the December policy meeting. At that meeting, the Fed raised rates by 25 basis points, to a range between 1.25-1.50%. The hike marks a vote of confidence in the US economy, and if the minutes are hawkish, the US dollar could gain ground. The economy is expanding at an impressive clip of above 3 percent. If this pace continues, the Fed could raise rates up to four times in 2018. Currently, the CME Group has priced in a January rate hike at 98.5%. Despite the rosy economic conditions, inflation has been chronically soft, well below the Fed target of 2 percent. Outgoing Fed Chair Janet Yellen and other FOMC members have said that they expect that the strong labor market will push up wages and trigger higher inflation, but this is yet to happen.

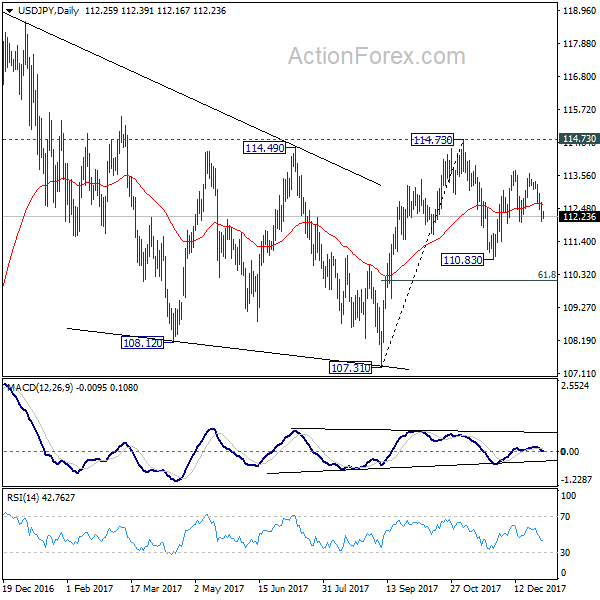

USD/JPY Mid-Day Outlook

Daily Pivots: (S1) 111.96; (P) 112.37; (R1) 112.70; More...

At this point, USD/JPY is staying in range of 112.02/113.74 and intraday bias remains neutral first. Near term outlook stays bullish as long as 112.02 support holds. Break of 113.74 will resume the rebound from 110.83 and target 114.73 key resistance. Decisive break there will carry larger bullish implications. However, break of 112.02 will likely extend the corrective pattern from 114.73 with another leg through 110.83 support.

In the bigger picture, we're holding on to the view that correction from 118.65 is completed at 107.31. And medium term rise from 98.97 (2016 low) is going to resume soon. Sustained break of 114.73 should affirm our view and send USD/JPY through 118.65. However, break of 107.31 will dampen this view and extend the medium term fall back to 98.97 low.