Sample Category Title

USD/JPY Daily Outlook

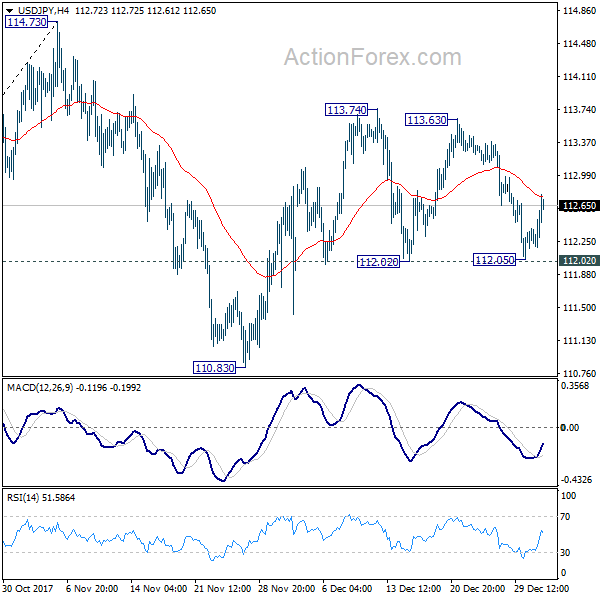

Daily Pivots: (S1) 112.25; (P) 112.42; (R1) 112.68; More...

USD/JPY formed a temporary low at 112.05, ahead of 112.02 support and recovered. As the pair is staying in range of 112.02/113.74, intraday bias remains neutral first. Also, near term outlook stays bullish as long as 112.02 support holds and further rise is expected. Break of 113.74 will resume the rebound from 110.83 and target 114.73 key resistance. Decisive break there will carry larger bullish implications. However, break of 112.02 will likely extend the corrective pattern from 114.73 with another leg through 110.83 support.

In the bigger picture, we're holding on to the view that correction from 118.65 is completed at 107.31. And medium term rise from 98.97 (2016 low) is going to resume soon. Sustained break of 114.73 should affirm our view and send USD/JPY through 118.65. However, break of 107.31 will dampen this view and extend the medium term fall back to 98.97 low.

Tax Cuts Optimism Boosted Stocks to Records, Dollar Trying to Rebound Again

US equities ended broadly higher overnight as boosted by tax cuts optimism. DOW gained 0.40% to 24922.68 and 25000 handle is within reach. S&P 500 closed solidly above 2700 handle at 2713.06, up 0.64%. NASDAQ also rose 0.84% to 7065.53. All three indices were at records. Nikkei follows today and surges close to over 2.6% through 23300. Dollar was also lifted by Fed officials's discussion that tax cuts could prompt faster rate hike. But for the moment, the greenback is still traded in red against all but Swiss Franc for the week. More support is needed from economic data, possibly non-farm payroll and wage growth, to give the greenback a turnaround.

FOMC minutes showed optimistic economic outlook

The FOMC minutes for the December meeting revealed that policymakers were optimistic about the path of economic expansion. The December rate hike of +25 bps was data-dependent but a key factor was the strong employment market. An important part of the optimism over the economic outlook was driven by the tax reform plan. "Many participants" expected the personal tax cut would "provide some boost to consumer spending" while "a few participants" noted that expectations of tax reform may have already raised consumer spending somewhat. More in Strong Job Market Lifted FOMC's Optimism, Views on Inflating Outlook Remained Divided.

Dollar index back above 92

The dollar index reached as low as 91.75 earlier this week but is back above 92 handle. 91 is still seen as the key long term support level but it's looking vulnerable. And, if the fall from 95.15 is a corrective move, it should be above to end soon. The index is close to 100% projection of 95.15 to 92.49 from 94.21 at 91.55, the three wave correction target level. But break of 92.49 support turned resistance is the first hurdle to overcome. The second will be 55 days EMA (now at 93.35). Or, further downside acceleration will push the index through this 91 cluster support level to resume the down trend from 103.82. In that case, the index could target next cluster level at around 84.5/85 before bottoming.

DOW on course for 25330.25

DOW's record fund continued as the new year starts. Long term up trend is still in progress for 200% projection of 20379.55 to 22179.11 from 21731.12 at 25330.25. Momentum is diminishing as seen with daily MACD turned below signal line in late December. But for the moment, near term outlook will remain bullish as long as 24697.11 support holds. Nonetheless, we'd pay attention to further loss of momentum as it approaches 25330.25.

On the data front

Japan PMI manufacturing was revised down to 54 in December. China Caixin PMI services rose to 53.9 in December, up from 51.9, above expectation of 51.8. PMI data will remain a focus in European session. UK will release PMI services, M4 and mortgage approvals. Eurozone will release PMI services final.

Later in the data, US job data will take center stage with ADP employment, jobless claims and Challenger job cuts featured. Canada will release IPPI and RMPI.

USD/JPY Daily Outlook

Daily Pivots: (S1) 112.25; (P) 112.42; (R1) 112.68; More...

USD/JPY formed a temporary low at 112.05, ahead of 112.02 support and recovered. As the pair is staying in range of 112.02/113.74, intraday bias remains neutral first. Also, near term outlook stays bullish as long as 112.02 support holds and further rise is expected. Break of 113.74 will resume the rebound from 110.83 and target 114.73 key resistance. Decisive break there will carry larger bullish implications. However, break of 112.02 will likely extend the corrective pattern from 114.73 with another leg through 110.83 support.

In the bigger picture, we're holding on to the view that correction from 118.65 is completed at 107.31. And medium term rise from 98.97 (2016 low) is going to resume soon. Sustained break of 114.73 should affirm our view and send USD/JPY through 118.65. However, break of 107.31 will dampen this view and extend the medium term fall back to 98.97 low.

Economic Indicators Update

| GMT | Ccy | Events | Actual | Forecast | Previous | Revised |

|---|---|---|---|---|---|---|

| 0:30 | JPY | PMI Manufacturing Dec F | 54 | 54.2 | 54.2 | |

| 1:45 | CNY | Caixin PMI Services Dec | 53.9 | 51.8 | 51.9 | |

| 7:00 | GBP | Nationwide House Price M/M Dec | 0.10% | 0.10% | ||

| 8:45 | EUR | Italy Services PMI Dec | 54.7 | 54.7 | ||

| 8:50 | EUR | France Services PMI Dec F | 59.4 | 59.4 | ||

| 8:55 | EUR | Germany Services PMI Dec F | 55.8 | 55.8 | ||

| 9:00 | EUR | Eurozone Services PMI Dec F | 56.5 | 56.5 | ||

| 9:30 | GBP | Mortgage Approvals Nov | 64.1k | 64.6k | ||

| 9:30 | GBP | Money Supply M4 M/M Nov | 0.40% | 0.60% | ||

| 9:30 | GBP | Services PMI Dec | 54 | 53.8 | ||

| 12:30 | USD | Challenger Job Cuts Y/Y Dec | 30.10% | |||

| 13:15 | USD | ADP Employment Change Dec | 190k | 190k | ||

| 13:30 | CAD | Industrial Product Price M/M Nov | 1.00% | |||

| 13:30 | CAD | Raw Materials Price Index M/M Nov | 3.80% | |||

| 13:30 | USD | Initial Jobless Claims (DEC 30) | 244K | 245K | ||

| 14:45 | USD | US Services PMI Dec F | 52.4 | 52.4 | ||

| 15:30 | USD | Natural Gas Storage | -112B | |||

| 16:00 | USD | Crude Oil Inventories | -4.6M |

Strong Job Market Lifted FOMC’s Optimism, Views on Inflating Outlook Remained Divided

The FOMC minutes for the December meeting revealed that policymakers were optimistic about the path of economic expansion. This was partly a result of the government's fiscal stimulus. On the tax cut, some members judged that it would help boost both capital and household spending, although the magnitude remains uncertain. The December rate hike of +25 bps was data-dependent but a key factor was the strong employment market. While wage growth was still "modest", a few members forecast it to accelerate as the job market tightened further. Many members expected that the tightening labor market would lead to higher inflation in the medium- term, but some continued to judge that core inflation would persistently stay below the 2% target. The rate hike in December was not unanimous as Chicago Fed President Charles Evans dissented.

The members generally agreed that economic activity had been "rising at a solid rate" and that "the labor market had continued to strengthen". The acknowledged the solid payrolls increase and the decline in the unemployment rate, "averaging through fluctuations associated with the recent hurricanes". The Summary of Economic Projections revealed that three members revised lower their estimates for the longer-run unemployment rate.

Inflation

The inflation remained largely unchanged from the October meeting. The members noted that both headline and core inflation continued to run "below that +2% target". However, they also noted that monthly core inflation had "edged up" recently, while "a couple" of participants indicated that year-over-year core inflation "appeared to be stabilizing". The debate over the nature of weak inflation continued. While some continued to judge the soft price levels were driven by "transitory factors", some noted that the secular trends are "muting inflation". As a result, two members lowered their core PCE projections for 2018, while others "generally viewed the medium-term outlook as little changed". A new ingredient in the the minutes was the risk that inflation pressures could build "unduly" if tax reform or financial conditions push output "well beyond" potential.

Tax Reform Plan

An important part of the optimism over the economic outlook was driven by the tax reform plan. "Many participants" expected the personal tax cut would "provide some boost to consumer spending" while "a few participants" noted that expectations of tax reform may have already raised consumer spending somewhat. Meanwhile, "a number" of participants noted that they were "uncertainty about the magnitude of the effects of tax reform on consumer spending". Meanwhile, "many participants" noted that the corporate tax cut could "provide a modest boost to capital spending, although the magnitude of the effects was uncertain".

Monetary Policy Outlook

On the whole, the members viewed the risks to growth as "balanced". The minutes noted that "most participants reiterated their support for continuing a gradual approach to raising the target range, noting that this approach helped to balance risks to the outlook for economic activity and inflation". This view was partly offset by "a few participants" who "were not comfortable with the degree of additional policy tightening through the end of 2018 implied by the median projections for the federal funds rate in the December SEP". This divergence reflected the different views of the members on the inflation outlook.

Trade ideas sponsorship survey

Within just a few days after discontinuing the trade ideas section, we received numerous enquiries offering to pay the service to keep it running. And there are offers to sponsor the whole section to keep it alive. We're overwhelmed by the generosity of our readers, our friends. A big thank you to you all first! We're seriously considering to re-open the section. But we'll need to have an assessment on the amount of donations we can get to sustain the operation of the section. Hence this simple poll.

The one thing that we always remember is our motto, "empowering the individual forex traders". We started with it more than 10 years ago and we keep it in our heart. And for those with us through the years, you know that everything in Action Forex is free, transparent and honest. If we're going to continue the trade idea section, it will be the same as before, free for all readers. Therefore, we'd prefer this donation route, rather than subscription.

Please take part in the survey here

https://apps.facebook.com/my-polls/trade-ideas-sponsorship-survey?from=admin_wall&v=361

For those who don't have, or who don't want to have a facebook account, please send us an email to contact@actionforex.com, and tell us how much you are willing to donate monthly to keep the section. We tried to setup a poll in our site earlier today but it crashed our database. So we don't want to risk it again.

Thanks.

(FED) Minutes of the Federal Open Market Committee December 12-13, 2017

A joint meeting of the Federal Open Market Committee and the Board of Governors was held in the offices of the Board of Governors of the Federal Reserve System in Washington, D.C., on Tuesday, December 12, 2017, at 1:00 p.m. and continued on Wednesday, December 13, 2017, at 9:00 a.m.

PRESENT:

Janet L. Yellen, Chair

William C. Dudley, Vice Chairman

Lael Brainard

Charles L. Evans

Patrick Harker

Robert S. Kaplan

Neel Kashkari

Jerome H. Powell

Randal K. Quarles

Raphael W. Bostic, Loretta J. Mester, Mark L. Mullinix, Michael Strine, and John C. Williams, Alternate Members of the Federal Open Market Committee

James Bullard, Esther L. George, and Eric Rosengren, Presidents of the Federal Reserve Banks of St. Louis, Kansas City, and Boston, respectively

James A. Clouse, Secretary

Matthew M. Luecke, Deputy Secretary

David W. Skidmore, Assistant Secretary

Michelle A. Smith, Assistant Secretary

Mark E. Van Der Weide, General Counsel

Michael Held, Deputy General Counsel

Steven B. Kamin, Economist

Thomas Laubach, Economist

David W. Wilcox, Economist

Thomas A. Connors, Michael Dotsey, Eric M. Engen, Evan F. Koenig, Daniel G. Sullivan, William Wascher, and Beth Anne Wilson, Associate Economists

Simon Potter, Manager, System Open Market Account

Lorie K. Logan, Deputy Manager, System Open Market Account

Ann E. Misback, Secretary, Office of the Secretary, Board of Governors

Matthew J. Eichner, Director, Division of Reserve Bank Operations and Payment Systems, Board of Governors; Andreas Lehnert, Director, Division of Financial Stability, Board of Governors

Jennifer Burns, Deputy Director, Division of Supervision and Regulation, Board of Governors; Rochelle M. Edge and Stephen A. Meyer, Deputy Directors, Division of Monetary Affairs, Board of Governors; Michael T. Kiley, Deputy Director, Division of Financial Stability, Board of Governors

Trevor A. Reeve, Senior Special Adviser to the Chair, Office of Board Members, Board of Governors

Joseph W. Gruber, David Reifschneider, and John M. Roberts, Special Advisers to the Board, Office of Board Members, Board of Governors

Linda Robertson, Assistant to the Board, Office of Board Members, Board of Governors

Antulio N. Bomfim, Edward Nelson, Ellen E. Meade, and Robert J. Tetlow, Senior Advisers, Division of Monetary Affairs, Board of Governors

Shaghil Ahmed, Associate Director, Division of International Finance, Board of Governors; Elizabeth Kiser, John J. Stevens, and Stacey Tevlin, Associate Directors, Division of Research and Statistics, Board of Governors; David López-Salido, Associate Director, Division of Monetary Affairs, Board of Governors

Norman J. Morin and Shane M. Sherlund, Assistant Directors, Division of Research and Statistics, Board of Governors

Eric C. Engstrom, Adviser, Division of Monetary Affairs, and Adviser, Division of Research and Statistics, Board of Governors

Penelope A. Beattie, Assistant to the Secretary, Office of the Secretary, Board of Governors

David H. Small, Project Manager, Division of Monetary Affairs, Board of Governors

Cynthia L. Doniger, Senior Economist, Division of Monetary Affairs, Board of Governors

Randall A. Williams, Senior Information Manager, Division of Monetary Affairs, Board of Governors

Kelly J. Dubbert, First Vice President, Federal Reserve Bank of Kansas City

David Altig, Kartik B. Athreya, Mary Daly, Beverly Hirtle, Geoffrey Tootell, and Christopher J. Waller, Executive Vice Presidents, Federal Reserve Banks of Atlanta, Richmond, San Francisco, New York, Boston, and St. Louis, respectively

Todd E. Clark and Marc Giannoni, Senior Vice Presidents, Federal Reserve Banks of Cleveland and Dallas, respectively

Jonathan L. Willis, Vice President, Federal Reserve Bank of Kansas City

Benjamin Malin, Senior Research Economist, Federal Reserve Bank of Minneapolis

Developments in Financial Markets and Open Market Operations

The manager of the System Open Market Account (SOMA) reported on developments in domestic and international financial markets over the intermeeting period. Equity prices moved higher over the period, with market participants pointing to the likely passage of tax reform legislation as an important factor contributing to the rise. The narrowing of the spread between long- and short-term Treasury yields over recent months had been a focus of market attention. Market participants cited a range of factors as contributing to this narrowing, including the gradual firming in the stance of monetary policy as well as an increasing expectation among investors that the Treasury Department would issue substantial volumes of shorter-term securities in meeting its financing needs over coming years.

The deputy manager discussed open market operations over the period. Take-up at the System's overnight reverse repurchase (ON RRP) agreement facility dropped to relatively low levels over the period. In part, the decline appeared to reflect an increase in yields on alternative investments; Treasury bill yields, for example, had moved higher over recent weeks as the Treasury boosted net issuance of Treasury bills. The Open Market Desk continued to execute reinvestment operations for Treasury and agency securities in the SOMA in accordance with the procedure specified in the Committee's directive to the Desk. The deputy manager also provided an update on plans for the Federal Reserve Bank of New York, in conjunction with the Treasury's Office of Financial Research, to begin publishing reference interest rates for repurchase agreements involving Treasury securities by the middle of next year.

By unanimous vote, the Committee ratified the Desk's domestic transactions over the intermeeting period. There were no intervention operations in foreign currencies for the System's account during the intermeeting period.

Staff Review of the Economic Situation

The information reviewed for the December 12-13 meeting indicated that labor market conditions continued to strengthen through November and suggested that real gross domestic product (GDP) was rising at a solid pace in the second half of 2017. Total consumer price inflation, as measured by the 12-month percentage change in the price index for personal consumption expenditures (PCE), remained below 2 percent in October and was lower than early in the year. Survey-based measures of longer-run inflation expectations were little changed on balance.

Total nonfarm payroll employment increased strongly in October and November, likely reflecting in part a rebound from the negative effects of the hurricanes in September. The national unemployment rate declined to 4.1 percent in October and remained at that level in November. The unemployment rates for Hispanics, for Asians, and for whites were lower in November than two months earlier, while the rate for African Americans was a little higher; the unemployment rates for each of these groups were close to the levels seen just before the most recent recession. The national labor force participation rate was lower in November than it had been in September but remained in the range seen over the past several years. The share of workers employed part time for economic reasons declined in October and was about unchanged in November. The rates of private-sector job openings and quits were little changed at relatively high levels in September and October, and the four-week moving average of initial claims for unemployment insurance benefits continued to be at a low level in early December. Recent readings showed that wage gains remained modest. Compensation per hour in the nonfarm business sector increased 1 percent over the four quarters ending in the third quarter, and average hourly earnings for all employees rose 2-1/2 percent over the 12 months ending in November.

Total industrial production increased briskly in October, boosted in part by a continued return to more-normal operations that reflected the waning of the negative effects of recent hurricanes in the previous two months. Automakers' schedules indicated that light motor vehicle assemblies would likely move up in the coming months. Broader indicators of manufacturing production, such as the new orders indexes from national and regional manufacturing surveys, pointed to further increases in factory output in the near term.

Real PCE increased modestly in October after expanding strongly in September. The pace of light motor vehicle sales slowed in November from the elevated rate in the preceding two months but continued to be above levels seen earlier in the year. Recent readings on key factors that influence consumer spending--including gains in employment, real disposable personal income, and households' net worth--continued to be supportive of moderate real PCE growth in the fourth quarter. Consumer sentiment in early December, as measured by the University of Michigan Surveys of Consumers, remained at a high level.

Recent information on housing activity suggested that real residential investment spending was edging up in the fourth quarter after declining in the previous two quarters. Both starts and building permit issuance for new single-family homes increased somewhat in October, and starts for multifamily units moved up considerably. Sales of both new and existing homes rose moderately in October.

Real private expenditures for business equipment and intellectual property appeared to be rising further in the fourth quarter. Nominal shipments of nondefense capital goods excluding aircraft increased in October, and new orders of these goods continued to exceed shipments, which pointed to further gains in shipments in the near term. In addition, readings on business sentiment remained upbeat. Firms' nominal spending for nonresidential structures excluding drilling and mining rose in October, and the number of oil and gas rigs in operation--an indicator of spending for structures in the drilling and mining sector--started to edge up in late November after declining earlier in the fourth quarter.

Total real government purchases looked to be rising in the fourth quarter. Nominal defense expenditures in October and November pointed to a flattening in real federal government purchases. However, real purchases by state and local governments appeared to be moving up, as these governments expanded their payrolls modestly over the two months ending in November and their nominal construction spending increased in October.

The nominal U.S. international trade deficit widened slightly in September and sharply in October. Exports picked up in September, led by exports of industrial supplies, but were flat in October. Imports grew significantly in both months, reflecting strength in most categories, although imports of automobiles declined. The available trade data suggested that the change in real net exports would make a neutral contribution to real U.S. GDP growth in the fourth quarter.

Total U.S. consumer prices, as measured by the PCE price index, increased slightly more than 1-1/2 percent over the 12 months ending in October. Core PCE price inflation, which excludes changes in consumer food and energy prices, was nearly 1-1/2 percent over that same period. The consumer price index (CPI) rose 2-1/4 percent over the 12 months ending in November, while core CPI inflation was 1-3/4 percent. Recent readings on survey-based measures of longer-run inflation expectations--including those from the Michigan survey, the Survey of Professional Forecasters, and the Desk's Survey of Primary Dealers and Survey of Market Participants--were little changed on balance.

Economic activity expanded at a solid pace in most foreign economies in the third quarter. In several advanced foreign economies (AFEs), economic growth slowed but remained firm. Economic activity in the emerging market economies (EMEs) continued to grow briskly for the most part, especially in Asia. However, the Mexican economy contracted in the third quarter, as hurricanes and earthquakes disrupted economic activity. Despite a boost from recent increases in oil prices, inflation remained relatively subdued in most AFEs and moderate in EMEs.

Staff Review of the Financial Situation

Movements in domestic financial asset prices over the intermeeting period reflected slightly stronger-than-expected economic data releases, announcements related to Treasury debt issuance, and an increase in the perceived probability that the Congress would enact tax legislation. On net, the Treasury yield curve flattened, U.S. equity prices moved up, and the foreign exchange value of the dollar was little changed. Financing conditions for businesses and households remained broadly supportive of continued growth in household spending and business investment.

Federal Reserve communications and economic data releases over the intermeeting period were characterized by market participants as reinforcing perceptions of a likely increase in the target range for the federal funds rate at the December meeting. The probability of an increase as implied by quotes on federal funds futures contracts edged up to around 95 percent, roughly consistent with the average probability indicated by responses to the Desk's surveys of primary dealers and market participants in December.

The nominal Treasury yield curve flattened over the intermeeting period, as short-dated Treasury yields rose and the 10-year Treasury yield moved up only slightly. Market participants pointed to the November 1 release of the Treasury's quarterly financing statement and accompanying analysis by the Treasury Borrowing Advisory Committee that highlighted some advantages of increasing issuance of relatively short-dated Treasury securities as factors contributing to the flattening of the yield curve over the period. Measures of inflation compensation based on Treasury Inflation-Protected Securities were little changed, on net, over the intermeeting period. Option-adjusted spreads of yields on current-coupon mortgage-backed securities (MBS) over Treasury yields also were little changed. Overall, market participants did not attribute any price changes in Treasury and agency MBS markets to the implementation of reductions in reinvestments of the SOMA portfolio.

Broad equity price indexes rose over the intermeeting period, likely reflecting in part investors' perceptions of increased odds for the passage of federal tax legislation and an associated potential boost to corporate earnings. One-month-ahead option-implied volatility on the S&P 500 index--the VIX--was little changed, on net, at levels close to historical lows. Spreads on both investment- and speculative-grade corporate bond yields over comparable-maturity Treasury yields were about flat on net.

Conditions in short-term funding markets remained stable over the intermeeting period. The effective federal funds rate held steady, and rates and volumes in other overnight markets were little changed. Take-up of ON RRPs declined notably as Treasury bill supply continued to increase, and short-dated bill yields rose to levels significantly above the ON RRP offering rate. On December 11, the Treasury declared a debt issuance suspension period to keep outstanding federal debt below the debt ceiling and began to use extraordinary measures to allow continued financing of government operations.

Financing conditions for large nonfinancial corporations continued to be accommodative on balance. Gross issuance of corporate bonds and gross equity issuance remained robust. Institutional leveraged loan issuance in November was brisk. Growth of bank-intermediated credit to nonfinancial firms, however, was tepid. On balance, the credit quality of nonfinancial corporations was little changed over the intermeeting period and appeared to remain solid. Financing conditions for small businesses also appeared to have remained favorable. In municipal bond markets, gross issuance was strong and credit quality remained stable.

In commercial real estate (CRE) markets, spreads of commercial mortgage-backed securities (CMBS) yields over comparable-maturity Treasury yields remained near the lower end of the range seen since the financial crisis, and delinquency rates on loans in CMBS pools continued to decrease. The growth of CRE loans held by the largest banks continued to slow, while CRE loan growth at smaller banks remained strong overall and even picked up a bit in October.

In the residential mortgage market, although credit standards had loosened gradually for borrowers with low credit scores, they continued to be tight for borrowers with low credit scores and hard-to-document incomes. Mortgage credit remained readily available for borrowers with strong credit scores. Similarly, consumer credit remained readily available to borrowers with strong credit histories, but conditions for subprime borrowers stayed tight in credit card markets and continued to tighten for auto loans. Issuance of asset-backed securities (ABS) funding consumer loans was robust in recent months, and ABS spreads were about unchanged over the intermeeting period.

On balance, the broad index of the foreign exchange value of the dollar was little changed, longer-term sovereign bond yields in AFEs declined modestly, and most foreign equity indexes moved lower over the intermeeting period. The euro appreciated modestly against the U.S. dollar, in part because of strong economic data for the euro area early in the intermeeting period. The British pound was somewhat volatile amid Brexit-related developments, and the Mexican peso fluctuated on news about negotiations associated with the North American Free Trade Agreement, but both currencies ended the period little changed. Following missed interest payments on its sovereign bonds, Venezuela was assigned selective default status by two credit rating agencies in early November, which precipitated a "credit event" ruling by the International Swaps and Derivatives Association. However, developments related to Venezuela generated little spillover to global financial markets.

Staff Economic Outlook

The U.S. economic projection prepared by the staff for the December FOMC meeting was generally comparable with the staff's previous forecast. Real GDP was forecast to have increased at a solid pace in the second half of 2017. Beyond 2017, the forecast for real GDP growth was revised up modestly, reflecting the staff's updated assumption that the reduction in federal income taxes expected to begin next year would be larger than assumed in the previous projection. The staff projected that real GDP would increase at a modestly faster pace than potential output through 2019. The unemployment rate was projected to decline further over the next few years and to continue running below the staff's slightly downward-revised estimate of the longer-run natural rate over this period.

The staff's forecast for total PCE price inflation was revised up a little for 2017, as somewhat higher forecasts for core PCE prices and for consumer energy prices were offset only partially by a lower forecast for consumer food prices. Total PCE price inflation in 2018 was projected to be about the same as in 2017, despite projected declines in consumer energy prices; core PCE prices were forecast to rise faster in 2018, reflecting the expected waning of transitory factors that held down those prices in 2017. Beyond 2018, the inflation forecast was little changed from the previous projection. The staff projected that inflation would be very close to the Committee's 2 percent objective in 2019 and at that objective in 2020.

The staff viewed the uncertainty around its projections for real GDP growth, the unemployment rate, and inflation as similar to the average of the past 20 years. On the one hand, many indicators of uncertainty about the macroeconomic outlook continued to be subdued; on the other hand, considerable uncertainty remained about a number of federal government policies relevant for the economic outlook. The staff saw the risks to the forecasts for real GDP growth and the unemployment rate as balanced. The risks to the projection for inflation also were seen as balanced. Downside risks to inflation included the possibility that longer-term inflation expectations may move lower or that the run of soft core inflation readings this year could prove to be more persistent than the staff expected. These downside risks were seen as essentially counterbalanced by the upside risk that inflation could increase more than expected in an economy that was projected to move further above its potential.

Participants' Views on Current Conditions and the Economic Outlook

In conjunction with this FOMC meeting, members of the Board of Governors and Federal Reserve Bank presidents submitted their projections of the most likely outcomes for real GDP growth, the unemployment rate, and inflation for each year from 2017 through 2020 and over the longer run, based on their individual assessments of the appropriate path for the federal funds rate. The longer-run projections represented each participant's assessment of the rate to which each variable would be expected to converge, over time, under appropriate monetary policy and in the absence of further shocks to the economy. These projections and policy assessments are described in the Summary of Economic Projections (SEP), which is an addendum to these minutes.

In their discussion of economic conditions and the outlook, meeting participants agreed that information received since the FOMC met in November indicated that economic activity had been rising at a solid rate and that the labor market had continued to strengthen. Averaging through fluctuations associated with the recent hurricanes, job gains had been solid and the unemployment rate had declined further. Household spending had been expanding at a moderate rate, and growth in business fixed investment had picked up in recent quarters. On a 12-month basis, both overall inflation and inflation for items other than food and energy had declined this year and were running below 2 percent. Market-based measures of inflation compensation remained low; survey-based measures of longer-term inflation expectations were little changed, on balance.

Real economic activity appeared to be growing at a solid pace, buttressed by gains in consumer and business spending, supportive financial conditions, and an improving global economy. Participants judged that hurricane-related disruptions and rebuilding had affected economic activity, employment, and inflation in recent months but had not materially altered the outlook for the national economy. They saw the incoming information on spending and the labor market as consistent with continued above-trend growth and a further strengthening in labor market conditions. Consequently, participants continued to expect that, with gradual adjustments in the stance of monetary policy, economic activity would expand at a moderate pace and labor market conditions would remain strong. Inflation on a 12-month basis was expected to remain somewhat below 2 percent in the near term but to stabilize around the Committee's 2 percent objective over the medium term. Near-term risks to the economic outlook appeared to be roughly balanced, but participants agreed that it would be important to continue to monitor inflation developments closely.

Participants expected moderate growth in consumer spending in the near term, underpinned by ongoing strength in the labor market, further improvements in households' net worth, and buoyant consumer sentiment. Business contacts in a few Districts reported strong pre-holiday sales. Many participants expected the proposed cuts in personal taxes to provide some boost to consumer spending. A few participants noted that expectations of tax reform may have already raised consumer spending somewhat to the extent that those expectations had spurred increases in asset valuations and household net worth. A number of participants expressed uncertainty about the magnitude of the effects of tax reform on consumer spending.

District contacts were optimistic, and their reports were generally consistent with continued steady growth in business spending. Reports from District contacts about both the manufacturing and service sectors were generally positive. In contrast, reports on housing and nonresidential construction were mixed. Activity in the energy sector continued to firm, with transportation bottlenecks and residual effects of the hurricanes putting some upward pressure on gasoline prices. In the agricultural sector, farm income was under downward pressure due to low crop prices, and contacts expressed concern about the effects of the possible renegotiation of trade agreements on exports.

Many participants judged that the proposed changes in business taxes, if enacted, would likely provide a modest boost to capital spending, although the magnitude of the effects was uncertain. The resulting increase in the capital stock could contribute to positive supply-side effects, including an expansion of potential output over the next few years. However, some business contacts and respondents to business surveys suggested that firms were cautious about expanding capital spending in response to the proposed tax changes or noted that the increase in cash flow that would result from corporate tax cuts was more likely to be used for mergers and acquisitions or for debt reduction and stock buybacks.

Labor market conditions continued to strengthen in recent months, with the unemployment rate declining further and payroll gains well above a pace consistent with maintaining a stable unemployment rate over time. Other indicators, such as consumer and business surveys of job availability and job openings, also pointed to a further tightening in labor market conditions. A couple of participants noted that broad improvements in labor market conditions over the past several years were evident across demographic groups. In several Districts, reports from business contacts or evidence from surveys pointed to some difficulty in finding qualified workers; in some cases, labor shortages were making it hard to fill customer demand or expand business. A few participants noted that a reduction in personal tax rates could potentially increase labor supply, but the magnitude of such effects was quite uncertain.

Against the backdrop of the continued strengthening in labor market conditions, participants discussed recent wage developments. Overall, the pace of wage increases had generally been modest and in line with inflation and productivity growth. In some Districts, reports from business contacts or evidence from surveys pointed to a pickup in wage gains, particularly for unskilled or entry-level workers. In a couple of regions, businesses facing tight labor market conditions were said to be offering more flexible work arrangements or taking advantage of technology to use employees more efficiently, rather than raising wages. A few participants judged that the tightness in labor markets was likely to translate into an acceleration in wages; however, another observed that the absence of broad-based upward wage pressures suggested that there might be scope for further improvement in labor market conditions.

PCE price inflation over the 12 months ending in October, at 1.6 percent, continued to run below the Committee's longer-run objective of 2 percent; core PCE price inflation for items other than consumer food and energy prices was only 1.4 percent over the same period. It was noted that recent readings on monthly inflation had edged up, and a couple of participants observed that core inflation on a year-over-year basis appeared to be stabilizing. Many indicated that they expected cyclical pressures associated with a tightening labor market to show through to higher inflation over the medium term. These participants generally judged that much of the softness in core inflation this year reflected transitory factors and that inflation would begin to rise as the influence of these factors waned. However, one of them noted that secular trends, such as technological innovation or globalization, could be affecting competition and business pricing, and muting inflationary pressures. With core inflation readings having moved down this year and remaining well below 2 percent, some participants observed that there was a possibility that inflation might stay below the objective for longer than they currently expected. Several of them expressed concern that persistently weak inflation may have led to a decline in longer-term inflation expectations; they pointed to low market-based measures of inflation compensation, declines in some survey measures of inflation expectations, or evidence from statistical models suggesting that the underlying trend in inflation had fallen in recent years. A few participants, however, noted that measures of inflation expectations had remained broadly stable this year despite the low readings on inflation and judged that this stability should support the return of inflation to the Committee's 2 percent objective.

With regard to financial markets, some participants observed that financial conditions remained accommodative, citing a range of indicators including low interest rates, narrow credit spreads, high equity values, a lower dollar, and some evidence of easier terms for lending to risky borrowers. In light of elevated asset valuations and low financial market volatility, a couple of participants expressed concern that the persistence of highly accommodative financial conditions could, over time, pose risks to financial stability. Participants also noted that term premiums on longer-term nominal Treasury securities remained low. A number of factors were seen as possibly contributing to the low levels of term premiums, including large holdings of longer-term assets by major central banks, persistently low global inflation, and substantial global demand for assets with long durations.

Meeting participants also discussed the recent narrowing of the gap between the yields on long- and short-maturity nominal Treasury securities, which had resulted in a flatter profile of the term structure of interest rates. Among the factors contributing to the flattening, participants pointed to recent increases in the target range for the federal funds rate, reductions in investors' estimates of the longer-run neutral real interest rate, lower longer-term inflation expectations, and lower term premiums. They generally agreed that the current degree of flatness of the yield curve was not unusual by historical standards. However, several participants thought that it would be important to continue to monitor the slope of the yield curve. Some expressed concern that a possible future inversion of the yield curve, with short-term yields rising above those on longer-term Treasury securities, could portend an economic slowdown, noting that inversions have preceded recessions over the past several decades, or that a protracted yield curve inversion could adversely affect the financial condition of banks and other financial institutions and pose risks to financial stability. A couple of other participants viewed the flattening of the yield curve as an expected consequence of increases in the Committee's target range for the federal funds rate, and judged that a yield curve inversion under such circumstances would not necessarily foreshadow or cause an economic downturn. It was also noted that contacts in the financial sector generally did not express concern about the recent flattening of the term structure.

In their discussion of monetary policy, participants saw the outlook for economic activity and the labor market as having remained strong or having strengthened since their previous meeting, in part reflecting a modest boost from the expected passage of the tax legislation under consideration. Regarding inflation, participants generally viewed the medium-term outlook as little changed, and a majority commented that they continued to expect inflation to gradually return to the Committee's 2 percent longer-run objective. A few participants again noted that transitory factors had likely held down inflation earlier this year. However, several participants observed that survey-based measures of inflation expectations or market-based measures of inflation compensation remained low, or that other persistent factors may be holding down inflation, which would present challenges for the Committee in promoting a return of inflation to 2 percent over the medium term.

Based on their current assessments, almost all participants expressed the view that it would be appropriate for the Committee to raise the target range for the federal funds rate 25 basis points at this meeting. These participants agreed that, even after an increase in the target range at this meeting, the stance of monetary policy would remain accommodative, supporting strong labor market conditions and a sustained return to 2 percent inflation. A couple of participants did not believe it was appropriate to raise the target range for the federal funds rate at this meeting; these participants suggested that the Committee should maintain the target range at 1 to 1-1/4 percent until the actual rate of inflation had moved further toward the Committee's 2 percent longer-run objective or inflation expectations had increased. They judged that leaving the target range at its current level would better support an increase in inflation expectations and thereby increase the likelihood that inflation will rise to 2 percent.

Regarding the determination of the appropriate timing and size of future adjustments to the target range for the federal funds rate, participants reaffirmed the need to continue to assess realized and expected economic conditions. Most participants reiterated their support for continuing a gradual approach to raising the target range, noting that this approach helped to balance risks to the outlook for economic activity and inflation. Participants discussed several risks that, if realized, could necessitate a steeper path of increases in the target range; these risks included the possibility that inflation pressures could build unduly if output expanded well beyond its maximum sustainable level, perhaps owing to fiscal stimulus or accommodative financial market conditions. Participants also discussed risks that could lead to a flatter trajectory for the federal funds rate in the medium term, including a failure of actual or expected inflation to move up to the Committee's 2 percent objective. While participants generally saw the risks to the economic outlook as roughly balanced, they agreed that inflation developments should be monitored closely. A few participants indicated that they were not comfortable with the degree of additional policy tightening through the end of 2018 implied by the median projections for the federal funds rate in the December SEP. They expressed concern that such a path of increases in the policy rate, while gradual, might prove inconsistent with a sustained return of inflation to 2 percent, or that the level of the federal funds rate might already be near its current neutral value. A few other participants mentioned that they saw as appropriate a pace of additional policy tightening through the end of 2018 that was somewhat faster than that implied by the December SEP median forecast. They noted that financial conditions had not materially tightened since the removal of monetary policy accommodation began, that continued low interest rates risked financial instability in the future, or that the labor market was increasingly tight. A couple of participants noted the need to continue to monitor and evaluate the effects of balance sheet normalization on long-term interest rates and economic performance.

Due to the persistent shortfall of inflation from the Committee's 2 percent objective, or the risk that monetary policy could again become constrained by the zero lower bound, a few participants suggested that further study of potential alternative frameworks for the conduct of monetary policy such as price-level targeting or nominal GDP targeting could be useful.

Committee Policy Action

In their discussion of monetary policy for the period ahead, members judged that information received since the Committee met in November indicated that the labor market had continued to strengthen and that economic activity had been rising at a solid rate. Averaging through hurricane-related fluctuations, job gains had been solid, and the unemployment rate had declined further. Household spending had been expanding at a moderate rate, and growth in business fixed investment had picked up in recent quarters. On a 12-month basis, both overall inflation and inflation for items other than food and energy had declined for the year to date and were running below 2 percent. Market-based measures of inflation compensation had remained low; survey-based measures of longer-term inflation expectations had changed little, on balance.

Members acknowledged that hurricane-related disruptions and rebuilding had affected economic activity, employment, and inflation in recent months but had not materially altered the outlook for the national economy. They continued to expect that, with gradual adjustments in the stance of monetary policy, economic activity would expand at a moderate pace and labor market conditions would remain strong. Members expected inflation on a 12-month basis to remain somewhat below 2 percent in the near term. They also expected inflation to stabilize around the Committee's 2 percent objective over the medium term, but a couple of members expressed concern about whether inflation would return to 2 percent on a sustained basis in the medium term if the Committee increased the target range for the federal funds rate at the pace that is implied by the medians of the projections from the December SEP. Members saw the near-term risks to the economic outlook as roughly balanced, but they agreed to monitor inflation developments closely.

After assessing current conditions and the outlook for economic activity, the labor market, and inflation, nearly all members agreed to raise the target range for the federal funds rate to 1-1/4 to 1-1/2 percent. These members noted that the stance of monetary policy remains accommodative, thereby supporting strong labor market conditions and a sustained return to 2 percent inflation. Two members preferred to leave the target range at 1 to 1-1/4 percent, suggesting that the Committee should wait to raise the target range until inflation moves up closer to 2 percent on a sustained basis or inflation expectations increase.

Members agreed that the timing and size of future adjustments to the target range for the federal funds rate would depend on their assessments of realized and expected economic conditions relative to the Committee's objectives of maximum employment and 2 percent inflation. They noted that their assessments would take into account a wide range of information, including measures of labor market conditions, indicators of inflation pressures and inflation expectations, and readings on financial and international developments. Members agreed that their assessments would also take into account actual and expected inflation developments relative to the Committee's symmetric inflation goal. Almost all members reaffirmed their expectation that economic conditions would evolve in a manner that would warrant gradual increases in the federal funds rate, and that the federal funds rate would be likely to remain, for some time, below levels that were expected to prevail in the longer run. Nonetheless, members reiterated that the actual path of the federal funds rate would depend on the economic outlook as informed by incoming data.

At the conclusion of the discussion, the Committee voted to authorize and direct the Federal Reserve Bank of New York, until it was instructed otherwise, to execute transactions in the SOMA in accordance with the following domestic policy directive, to be released at 2:00 p.m.:

"Effective December 14, 2017, the Federal Open Market Committee directs the Desk to undertake open market operations as necessary to maintain the federal funds rate in a target range of 1-1/4 to 1-1/2 percent, including overnight reverse repurchase operations (and reverse repurchase operations with maturities of more than one day when necessary to accommodate weekend, holiday, or similar trading conventions) at an offering rate of 1.25 percent, in amounts limited only by the value of Treasury securities held outright in the System Open Market Account that are available for such operations and by a per-counterparty limit of $30 billion per day.

The Committee directs the Desk to continue rolling over at auction the amount of principal payments from the Federal Reserve's holdings of Treasury securities maturing during December that exceeds $6 billion, and to continue reinvesting in agency mortgage-backed securities the amount of principal payments from the Federal Reserve's holdings of agency debt and agency mortgage-backed securities received during December that exceeds $4 billion. Effective in January, the Committee directs the Desk to roll over at auction the amount of principal payments from the Federal Reserve's holdings of Treasury securities maturing during each calendar month that exceeds $12 billion, and to reinvest in agency mortgage-backed securities the amount of principal payments from the Federal Reserve's holdings of agency debt and agency mortgage-backed securities received during each calendar month that exceeds $8 billion. Small deviations from these amounts for operational reasons are acceptable.

The Committee also directs the Desk to engage in dollar roll and coupon swap transactions as necessary to facilitate settlement of the Federal Reserve's agency mortgage-backed securities transactions."

The vote also encompassed approval of the statement below to be released at 2:00 p.m.:

"Information received since the Federal Open Market Committee met in November indicates that the labor market has continued to strengthen and that economic activity has been rising at a solid rate. Averaging through hurricane-related fluctuations, job gains have been solid, and the unemployment rate declined further. Household spending has been expanding at a moderate rate, and growth in business fixed investment has picked up in recent quarters. On a 12-month basis, both overall inflation and inflation for items other than food and energy have declined this year and are running below 2 percent. Market-based measures of inflation compensation remain low; survey-based measures of longer-term inflation expectations are little changed, on balance.

Consistent with its statutory mandate, the Committee seeks to foster maximum employment and price stability. Hurricane-related disruptions and rebuilding have affected economic activity, employment, and inflation in recent months but have not materially altered the outlook for the national economy. Consequently, the Committee continues to expect that, with gradual adjustments in the stance of monetary policy, economic activity will expand at a moderate pace and labor market conditions will remain strong. Inflation on a 12-month basis is expected to remain somewhat below 2 percent in the near term but to stabilize around the Committee's 2 percent objective over the medium term. Near-term risks to the economic outlook appear roughly balanced, but the Committee is monitoring inflation developments closely.

In view of realized and expected labor market conditions and inflation, the Committee decided to raise the target range for the federal funds rate to 1-1/4 to 1-1/2 percent. The stance of monetary policy remains accommodative, thereby supporting strong labor market conditions and a sustained return to 2 percent inflation.

In determining the timing and size of future adjustments to the target range for the federal funds rate, the Committee will assess realized and expected economic conditions relative to its objectives of maximum employment and 2 percent inflation. This assessment will take into account a wide range of information, including measures of labor market conditions, indicators of inflation pressures and inflation expectations, and readings on financial and international developments. The Committee will carefully monitor actual and expected inflation developments relative to its symmetric inflation goal. The Committee expects that economic conditions will evolve in a manner that will warrant gradual increases in the federal funds rate; the federal funds rate is likely to remain, for some time, below levels that are expected to prevail in the longer run. However, the actual path of the federal funds rate will depend on the economic outlook as informed by incoming data."

Voting for this action: Janet L. Yellen, William C. Dudley, Lael Brainard, Patrick Harker, Robert S. Kaplan, Jerome H. Powell, and Randal K. Quarles.

Voting against this action: Charles L. Evans and Neel Kashkari.

Messrs. Evans and Kashkari dissented because they preferred to maintain the existing target range for the federal funds rate at this meeting.

In Mr. Evans's view, with inflation continuing to run substantially below 2 percent and measures of inflation expectations lower than he believed to be consistent with a symmetric 2 percent inflation objective, it was important to pause in the process of policy normalization. Leaving the target range at 1 to 1-1/4 percent for a time would better support an increase in inflation expectations, increase the likelihood that inflation will rise to 2 percent and perhaps modestly beyond, and thus provide more support for the symmetry of the Committee's inflation objective. Such a pause also would better allow the Committee time to assess the degree to which earlier soft readings on inflation were transitory or more persistent.

In Mr. Kashkari's view, while employment growth remained strong, wage growth had not picked up and inflation remained notably below the Committee's 2 percent target. In addition, the yield curve had flattened as long-term rates had not moved higher even though the Committee raised the federal funds rate target range. He was concerned that the flattening yield curve was partly due to falling longer-term inflation expectations or a lower neutral real rate of interest. He preferred to wait for inflation to move closer to 2 percent on a sustained basis or for inflation expectations to move up before further raising the target range for the federal funds rate.

To support the Committee's decision to raise the target range for the federal funds rate, the Board of Governors voted unanimously to raise the interest rates on required and excess reserve balances 1/4 percentage point, to 1-1/2 percent, effective December 14, 2017. The Board of Governors also voted unanimously to approve a 1/4 percentage point increase in the primary credit rate (discount rate) to 2 percent, effective December 14, 2017.

It was agreed that the next meeting of the Committee would be held on Tuesday-Wednesday, January 30-31, 2018. The meeting adjourned at 10:15 a.m. on December 13, 2017.

Notation Vote

By notation vote completed on November 21, 2017, the Committee unanimously approved the minutes of the Committee meeting held on October 31-November 1, 2017.

FOMC Participants’ See Tax Cuts as Supportive of Continued above-Trend Economic Performance

The minutes of the Federal Open Market Committee's (FOMC) last meeting of 2017 highlighted the strong and strengthening pace of economic expansion despite hurricane-related distortions.

Many participants anticipated that the announced changes to business taxes would provide a "modest boost to capital spending, although the magnitude of the effects was uncertain". However, supply-side effects were deemed somewhat uncertain, citing industry contacts that tax savings were likely to be used for mergers and acquisitions rather than for capital expenditures.

The prospect of personal income tax cuts led many participants to expect "some boost to consumer spending", with a few noting that the expectation of a tax cut has likely already acted to boost asset prices, and thus household net worth. Similarly, personal tax cuts were viewed by a few participants to help boost labor supply by an uncertain amount.

A strengthening labor market outlook helped drive a debate on wages and inflation. Although wage growth has been largely viewed as modest, a few participants anticipated an acceleration in wage growth as labor markets tightened further. Furthermore, many participants expected the tightening labor market to result in inflation in the medium term, but some participants continued to fret about core inflation persisting below 2% target. On that note, several participants were concerned with inflation expectations falling further.

The flattening of the yield curve was discussed, with participants citing fed rate hikes, lower market estimates of the longer-run neutral real interest rate, lower inflation expectations, and lower term premiums as the main drivers. Interestingly, they generally agreed that "the current degree of flatness of the yield curve was not unusual by historical standards". But, the slope of the yield curve will likely continue to be monitored since historically an inversion of the yield curve has been a predictor of an economic slowdown.

Lastly, participants discussed the timing and the size of future adjustments of Fed policy, with most participants reiterating their support for a gradual increase in the target range. However, they discussed several risks that could result in a steeper path of rate hikes. One such risk was an unwarranted build-up in inflation if the economy was expanding "well beyond its maximum sustainable level", possibly due to fiscal or excess monetary stimulus. Similarly, risks that could result in a flatter yield curve were also discussed, including a risk that inflation could fail to move to the 2% target. On net, participants viewed the risks as "roughly balanced", and they will continue to monitor inflation developments closely.

Key Implications

Above-trend economic growth is likely to continue into the first half of 2018, suggesting that the FOMC could raise interest rates at its upcoming meetings in January or March. Moreover, the expected boost to economic growth from tax cuts helps to build a strong case for an additional two rate hikes before the end of this year, in line with the three rate hikes communicated in the FOMC's Summary of Economic Projections (SEP) last month.

The debate concerning the evolution of inflation continues at the Fed, ensuring that normalization will remain a gradual process. If inflation fails to make material progress in 2018 the Fed will likely only raise interest rates twice.

With four Federal Reserve board of governor seats still up for grabs, President Trump's administration has the ability to alter the composition of the Federal Reserve and the future course of monetary policy to align it better with its goals. As such, the nomination process will continue to be carefully watched by investors for any indications of a change in the pace of monetary policy normalization.

Gold Rally Pauses Ahead Of FOMC Minutes

Gold has paused on Wednesday, after posting strong gains in the Tuesday session. In North American trade, the spot price for an ounce of gold is $1316.19, down 0.06% on the day. On the release front, ISM Manufacturing PMI improved to 59.7, beating the forecast of 58.3 points. This marked a 3-month high. Later in the day, the Federal Reserve will release the minutes from its December policy meeting. On Thursday, the US releases ADP Nonfarm Payrolls and unemployment claims.

Gold continues to shine early in the New Year, after climbing 2.2% in December. On Tuesday, gold touched a high of $1321, its highest level since September 15. With the US economy expanding above 3% and the Fed poised to raise rates for a second straight month, the gold rally has surprised many experts, as stronger economic conditions usually translate into increased risk appetite, at the expense of safe haven assets such as gold. Traders can expect some movement from gold on Friday, as the US releases two key employment indicators – wage growth and nonfarm payrolls. If these releases beat expectations, the dollar could recover some of its recent losses and send gold prices lower.

The Federal Reserve will be in the spotlight on Wednesday, with the release of the minutes of the December policy meeting. At that meeting, the Fed raised rates by 25 basis points, to a range between 1.25-1.50%. The hike marked a vote of confidence in the US economy, and if the minutes are hawkish, the US dollar could gain ground. The economy is in fine form, expanding at an impressive clip of above 3 percent. If this pace continues, the Fed could raise rates up to four times in 2018. Currently, the CME Group has priced in a January rate hike at 98.5%. Despite the rosy economic conditions, inflation has been chronically soft, well below the Fed target of 2 percent. Outgoing Fed Chair Janet Yellen and other FOMC members have said that they expect that the strong labor market will push up wages and trigger higher inflation, but this is yet to happen.

Pound Dips As Construction PMI Misses Expectations

The British pound has posted considerable losses in the Wednesday, erasing the gains seen in the Tuesday session. In Wednesday’s North American trade, GBP/USD is trading at 1.3520, down 0.52% on the day. In economic news, British Construction PMI slowed to 52.2, missing the estimate of 52.8 points. In the US, ISM Manufacturing PMI improved to 59.7, beating the forecast of 58.3 points. This marked a 3-month high. Today’s key event is the release of the Fed minutes from the December meeting. On Thursday, the UK releases Services PMI. Over in the US, the focus will be on employment numbers, with the release of ADP Nonfarm payrolls and unemployment claims. On Friday, we’ll get a look at wage growth and US Nonfarm Payrolls.

British PMIs have not had a positive week. Construction PMI missed expectations, after Manufacturing PMI also disappointed on Tuesday. At the same time, the indicators continue to point to expansion in the manufacturing and construction sectors, with readings above the 50-level. The manufacturing sector has received a boost from strong global demand for British exports. As well, the weak pound has also made British products less expensive.

The Federal Reserve takes center stage later on Wednesday, with the release of the minutes of the December policy meeting. At that meeting, the Fed raised rates by 25 basis points, to a range between 1.25% and 1.50%. The hike marks a vote of confidence in the US economy, and if the minutes are hawkish, the US dollar could gain ground. The economy is expanding at an impressive clip of above 3 percent. If this pace continues, the Fed could raise rates up to four times in 2018. Currently, the CME Group has priced in a January rate hike at 98.5%. Despite the rosy economic conditions, inflation has been chronically soft, well below the Fed target of 2 percent. Outgoing Fed Chair Janet Yellen and other FOMC members have said that they expect that the strong labor market will push up wages and trigger higher inflation, but this is yet to happen.

Rarefied Air for ISM

The ISM Manufacturing Index for December came in at 59.7. That marks the fifth consecutive print of 58 or higher, a feat last accomplished in 2004. Prior to that, you'd have to go back to 1987.

Boom Goes the Dynamite

The ISM survey for December came in at a torrid 59.7–the second fastest pace of expansion in six years. New orders came at 69.4; that means that manufacturers are seeing orders expand at the fastest pace in more than 13 years. There are signs that factories are having trouble keeping up. Order backlogs jumped a full point to 56.0 and supplier deliveries are being held up as well. All the activity is giving supplier a degree of pricing power that has been a fleeting thing in this economic cycle. The prices paid component climbed to 69.0 in December.

It is more than just domestic developments that are lifting animal spirits. A number of the published industry comments focused on a pick-up in demand from overseas, and indeed, the export orders component jumped to six-month high of 58.5.

This is the thin air of the high peaks. It is quite uncommon for the ISM index to remain so firmly in expansion territory for such a long period of time. The only other time in the past 40 years that the ISM came in at 58 or higher for this many consecutive months was a streak that lasted from November 2003 to August 2004.

We went back into the archives and found our write-up from August 2004 for the August ISM to see what we were saying at that time so that we could compare with our assessment of where the economy is today. At that time, we wrote, "…today's manufacturing survey results are consistent with this theme [of moderation] as key components are down from their highs but above the 50 break even level…the pace of industrial production will also moderate from rapid recovery to expansion in the year ahead."

That was not too far afield from how things played out. Full year GDP growth for that expansion peaked in 2004 and slowed in each of the next three years before succumbing to recession at the end of 2007.

We compare that to today's print to our forecast today and after back-toback quarters of GDP growth of three percent or better growth, we anticipate growth of roughly two and a half percent in the fourth quarter of 2017 and in each quarter of 2018.

While the ISM may have lost some of its luster as a bellwether for broader growth as the U.S. economy has become less reliant on manufacturing, it is still vital as a harbinger of things to come for manufacturing. In that regard, we note that despite the nearly 14-year high for the new orders component, actual core capital goods are still not growing as fast as they were in 2010 and 2011. We expect some convergence between these measures in the months to come and acknowledge there is now some clear upside risk to our equipment forecast.

US: Manufacturing Activity Ended 2017 on a High Note

The Institute for Supply Management (ISM) index of manufacturing rose 1.5 points to 59.7 in December, well ahead of market expectations for a flat reading. This marks the 16th straight month that the index has been in expansionary territory.

The report details were generally positive, with increases in all major indexes with the exception of employment that slipped to 57.0 (from 59.7).

The prices paid index also rebounded to 69.0, after falling to 65.5 in November.

The spread between new orders and inventories - a good leading indicator of activity - widened further in December to 20.9 (+3.9 points), suggesting that the manufacturing is likely to hold onto recent gains in the coming months.

Key Implications

The manufacturing index regained its October peak, suggesting strong growth in the sector to end 2017. Momentum is strong heading into the New Year, and with tax stimulus boosting bottom lines and supporting demand, growth is likely to continue.

All signs point to the U.S. economy continuing to run above its cruising speed, which should eat up any remaining economic slack and set the stage for higher inflation. As the unemployment plunges to new lows, it will be the key indicator to watch for the pace of rate hikes from the Federal Reserve.