Sample Category Title

NZDUSD Intraday Analysis

NZDUSD (0.7103): The New Zealand dollar closed with a doji session for the third consecutive day on Wednesday. Price action shows a potential exhaustion to the rally since mid-November, which saw prices rising from the lows near 0.68. The Kiwi dollar is looking bullish at the moment but with the breakout from the median line, we expect that the current momentum could result in price posting a lower high. Unless NZDUSD manages to break past the previous high we expect to see a decline to 0.7062 initially.

USDJPY Intraday Analysis

USDJPY (112.64): The USDJPY was seen posting some gains on Wednesday as it’s price closed bullish, forming an inside bar on the daily session. A follow through with a breakout to the upside could potentially send USDJPY to the intraday resistance level near 113.00 area. We however expect a fake breakout, with price likely to resume its decline. Support at 112.04 remains in focus as a firmer test of this support is likely in the near term. In the event that USDJPY manages to break out higher, a close above 113.00 is required in order to maintain further gains.

EURUSD Intraday Analysis

EURUSD (1.2019): The EURUSD closed with losses yesterday and price action settled within the range from Tuesday. Price is seen trading just below the 1.2091 level of resistance. On the intraday charts, we see that EURUSD has slipped past the lower median line. We expect to see a retracement as the common currency could be seen paring losses. Another short term rally to the upside, potentially to 1.2091 could eventually complete the rally, as we now expect the currency pair to start posting a correction.

USD Rebounds On FOMC Minutes And ISM Manufacturing

The U.S. dollar turned slightly bullish yesterday as the greenback managed to post a rebound following a long stretch of declines. The gains came as the ISM's manufacturing PMI surprised everyone with a reading of 59.7. This was higher than the estimates of 58.1 and manufacturing activity advanced from 58.2 in November.

The Fed meeting minutes released later in the day showed that officials factored in the tax cuts. Officials, according to the minutes, were optimistic that the tax cuts were one of the factors that led the central bank to hike interest rates in December. Inflation however, is expected to remain below the Fed's target for longer.

Looking ahead, the economic data today will see ADP/Moody's publishing the December private payrolls report. Economists forecast 191k jobs for December, slightly higher from 190k in November.

In the UK, the services PMI data is expected to remain stable with estimates pointing to reading of 56.5 in the index.

Robust Economic Growth And Loose Monetary Policy Remain The Central Theme

Equity investors across the globe are finding no reasons to take profits after an excellent performance in 2017. Asian stocks are trading at record highs after Japan kicked off the first trading day of 2018, European markets are poised for a higher open today despite cautiousness amid the launch of new market rules from the EU, and all U.S. major indices closed at all-time highs with S&P 500 breaching 2,700.

With economic reports across the Atlantic showing robust economic growth and monetary policymakers, including the Fed, continuing to back a gradual approach to tightening monetary policy, the rally in equities is justified.

After European factories reported their strongest monthly performance in December, U.S. manufacturing data also blew expectations. According to the Institute of Supply Management, gains in orders and production in 2017 were the highest since 2004. New orders which grew 69.4 versus 64.4 in November, suggest manufacturing strength is likely to remain strong in Q1 2018, especially since the survey occurred prior to signing the tax legislation. Such optimism should drive hard data and I won't be surprised to see Q4 GDP exceeding 4%.

However, the dollar only managed to squeeze out small gains given that the Fed doesn't seem concerned about rising inflation at the moment. According to the FOMC minutes, some participants observed that there was a possibility that inflation might stay below the 2% for longer than currently expected. That's why Neel Kashkari and Charles Evans voted against raising rates at the December meeting.

Fed policymakers also seem uncertain about the impact of tax reduction on capital spending and the overall economy, which sounds somehow dovish to me. But on the hawkish side, particularly for equity investors, the Fed believes that the additional savings from tax cuts will go to M&A and stock buybacks.

Despite the shorter end of the U.S. yield curve moving higher on increased expectations of a March rate hike, the longer end was unmoved. This led the yield curve to flatten further, dropping to 51 basis points, which is not the best news for dollar bulls.

The CBoE's VIX index fell below 9 for the first time since touching a record low back in November, suggesting that volatility is likely to remain low and few investors are seeking protection to the downside. However, it always worries me when investors are complacent to such extent.

The final services PMI release across Europe may drive some action in the Euro today, but given that Nonfarm payroll's report is due on Friday, I expect the range-bound trading to resume throughout the day.

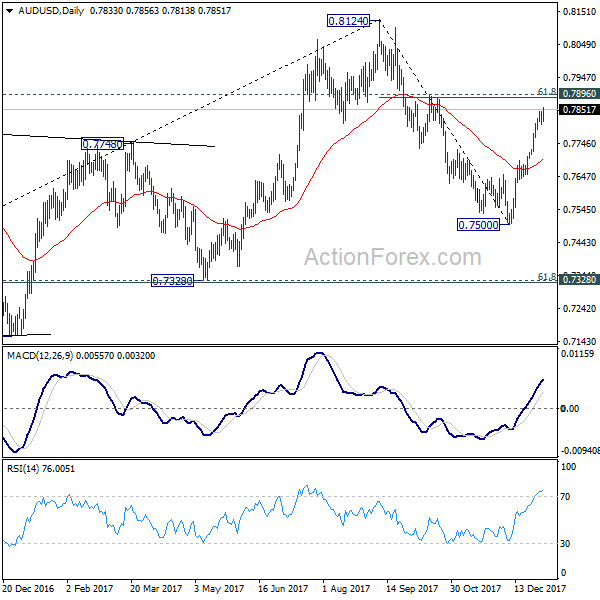

AUD/USD Daily Outlook

Daily Pivots: (S1) 0.7811; (P) 0.7828; (R1) 0.7850; More...

AUD/USD's rally resumed after brief consolidation and intraday bias is back on the upside for 0.7896 cluster resistance (61.8% retracement of 0.8124 to 0.7500 at 0.7886). Considering bearish divergence condition in 4 hour MACD, upside should be limited by 0.7896/44 to bring a short term top. Break of 0.7804 minor support should turn intraday bias back to the downside for 4 hour 55 EMA (now at 0.7764) and below.

In the bigger picture, we're still slightly favoring the case that corrective rise from 0.6826 medium term bottom is likely completed at 0.8124, after hitting 55 month EMA (now at 0.8032). But stronger than expected rebound from 0.7500 is dampening this bearish view. On the downside, break of 0.7500 will target 0.7328 key cluster support (61.8% retracement 0.6826 to 0.8124 at 0.7322) to confirm this bearish case. But break of 0.8124 will extend the rise from 0.6826 to 38.2% retracement of 1.1079 (2011 high) to 0.6826 (2016 low) at 0.8451 before completion.

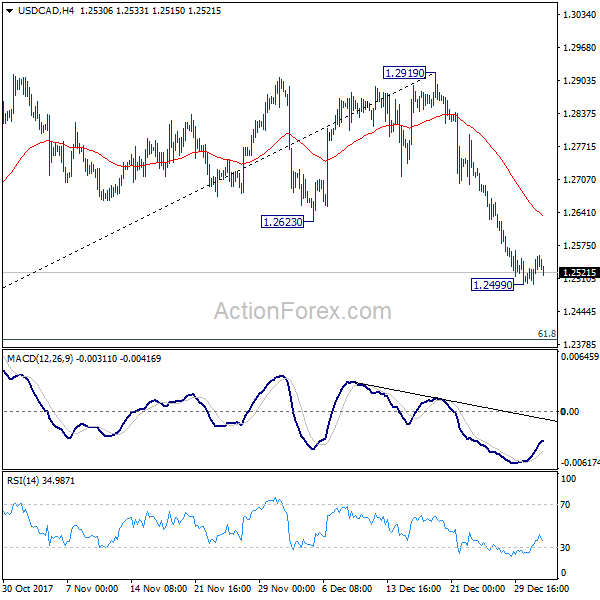

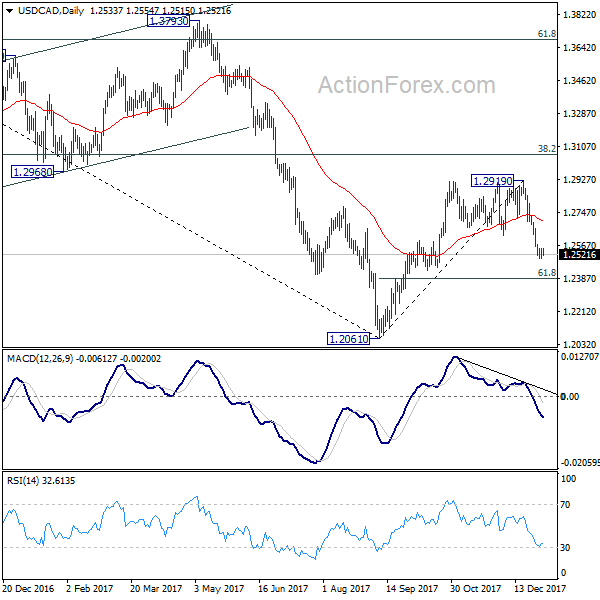

USD/CAD Daily Outlook

Daily Pivots: (S1) 1.2504; (P) 1.2529; (R1) 1.2559; More....

A temporary low is in place at 1.2499 in USD/CAD and intraday bias is turned neutral first. As long as 4 hour 55 EMA (now at 1.2363) holds, deeper decline is expected. Below 1.2499 will extend the fall from 1.2919 to 61.8% retracement of 1.2061 to 1.2919 at 1.2389 or possibly below. Nonetheless, sustained break of 4 hour 55 EMA will argue that the decline is completed. In such case, intraday bias will be turned back to the upside for retesting 1.2919 instead.

In the bigger picture, we're still favoring the case that USD/CAD has defended 50% retracement of 0.9406 (2011 low) to 1.4689 (2016 high) at 1.2048. And with 1.2048 intact, we'd favor the case that fall from 1.4689 is a correction. With that in mind, fall from 1.2919 is viewed as a correction. Hence, we're not anticipating a break of 1.2061 low. In the long run, USD/CAD should have another medium term rise to take on 38.2% retracement of 1.4689 to 1.2061 at 1.3065.

The USD As Well As Short

Market movers today

NEW RESEARCH WEBSITE. We have launched our new research website with all our research across asset classes and count ries.

Today is the big Markit PMI service day with releases across Europe and in the US. From a market perspective, the release in the UK is among the most important: we expect the service index – which is a key gauge for overall economic growth – to be broadly unchanged at 53.8.

Even if the ADP jobs report in the US has been a poor indicator for non-farm payrolls (due tomorrow), markets will follow today's release for any clues as to tomorrow's direction.

In Norway, house prices are due out at 11:00 CET. Housing prices have fallen in seven of the past eight months and are almost 3% down on their March peak. However, there are some signs of stabilisat ion, see Scandi markets and NOK FX comment on the next page.

Selected market news

Market focus this morning is on Japan returning from holiday and most major Asian equity indices following the European and US counterparts into green territory. The USD as well as short and longer-end US rates are roughly unchanged after last night 's FOMC minutes (see next section). Gold is rading a little lower while oil prices have continued to trade higher overnight. In our view, the recent rise in oil prices has been caused mainly by the freezing polar vortex hitting the US, firing up heating demand and spurring concerns about the potential impact on oil production and trade. API reported yesterday that crude stocks dropped 5mb last week , which should be at tributed mainly to the winter season effect .

The FOMC minutes yesterday evening did not give markets much news to trade on, as was reflected in the muted market reaction. The Fed is still divided between doves and hawks/centrist : doves think inflation is below 2% due to slack in the labour market and lower inflation expectations while the hawks/centrists think the tighter labour market will soon translate into higher wage growth and hence underlying inflation pressure. One interesting thing to note from the minutes, however, was that an alternative policy framework of price level targeting again was discussed (for more information see: Research US – The subtle push for price level targeting continues, 3 January). We continue to expect two-three hikes this year with two hikes as our base case. We do not think the change of Fed board members will change that.

Prior to the FOMC minutes, ISM manufacturing rose to 59.7 in December from 58.2 in November, thereby heavily beat ing our and market expectations. The details were also encouraging with not least the new order component rising to the highest level since the midearly 00s (see chart). The release suggests that the manufacturing recovery is not only continuing in the US but that it might re-accelerate slightly.

Yesterday's FX reserve and balance sheet data from Danmarks Nationalbank (DN) showed a rise in the FX reserve to DKK468bn in December via an unspecified DKK4bn purchase by DN. Meanwhile, for the ninth consecutive month, DN did not intervene in FX markets, which is the longest period of no FX intervention since the beginning of 2014.

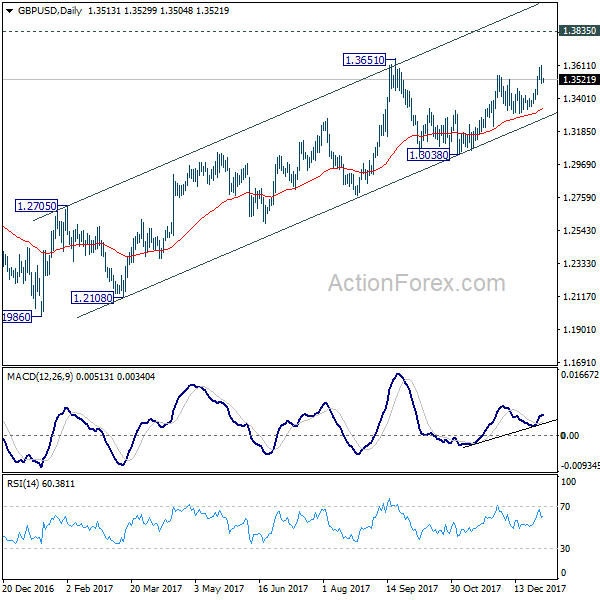

EUR/USD Daily Outlook

Daily Pivots: (S1) 1.1987; (P) 1.2026 (R1) 1.2052; More....

Intraday bias in EUR/USD remains neutral first. Some consolidation could be seen below 1.2091 key resistance but further rise is expected as long as 4 hour 55 EMA (now at 1.1941) holds. Firm break of 1.2091 will confirm medium term rally resumption and target next key fibonacci level at 1.2494/2516. However, sustained break of 4 hour 55 EMA will extend the consolidation pattern from 1.2091 with with another decline through 1.1717 support.

In the bigger picture, rise from 1.0339 medium term bottom is seen as a corrective move for the moment. Therefore, in case of another rally, we'd be expect 38.2% retracement of 1.6039 (2008 high) to 1.0339 (2017 low) at 1.2516 to limit upside and bring reversal. That is also close to 61.8% projection of 1.0569 to 1.2091 from 1.1553 at 1.2494.

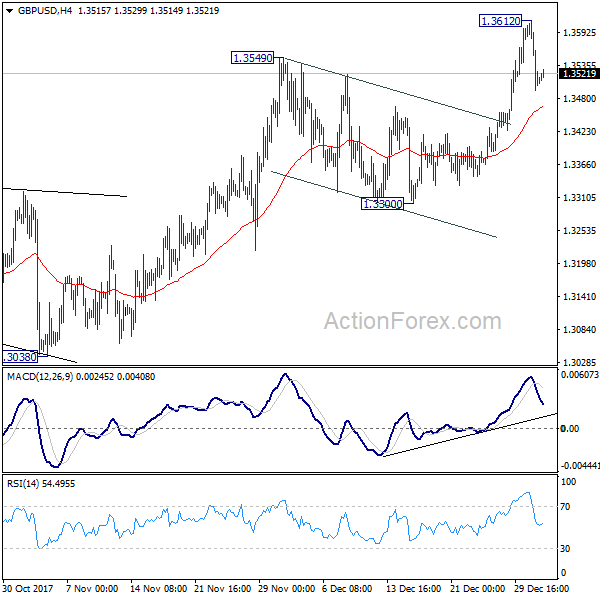

GBP/USD Daily Outlook

Daily Pivots: (S1) 1.3469; (P) 1.3540; (R1) 1.3588; More.....

Intraday bias in GBP/USD remains neutral for the moment. As long as 4 hour 55 EMA (now at 1.3465) holds, further rally is expected. Above 1.3612 will target 1.3651 key resistance first. Break will resume medium term rise from 1.1946 and target key resistance level at 1.3835. However, sustained break of 4 hour 55 EMA will turn focus back to 1.3300 support.

In the bigger picture, while the medium term rebound from 1.1946 low was strong, it's limited below 1.3835 key support turned resistance. As long as 1.3835 holds, we'd view such rebound as a correction. That is, we'd expect another leg in the long term down trend through 1.1946 low. However, sustained break of 1.3835 should at least send GBP/USD to 38.2% retracement of 2.1161 (2007 high) to 1.1946 (2016 low) at 1.5466.