Sample Category Title

Poor Wage Growth Caps Further USD Gains

- European equity markets gain between 0.5% and 1%. Gains mainly occurred in the European opening, welcoming political decisions in the US and the EU/UK. US stock markets opened open with gains of about 0.3/0.4% (Dow & S&P). The Nasdaq again outperforms (+0.75 %).

- US payrolls beat forecasts in November as net job growth increased by 228k vs 195k expectations. The previous two months' numbers were upwardly revised by 3k. The US unemployment rate stabilized at 4.1%, the lowest level since 2000. Average hourly earnings (0.2% M/M and 2.5% Y/Y) increased from October, but remained below consensus.

- German exports fell unexpectedly in October (-0.4% M/M) while vibrant domestic demand pushed up imports (+1.8% M/M), narrowing the trade surplus and adding to evidence that Europe's biggest economy started the fourth quarter on a weak footing.

- UK manufacturers extended their winning streak in October as foreign demand sent car production to a record. Factory output rose 0.1% from September, marking six consecutive increases for the first time since modern records began in 1997. Overall industrial production was unchanged as warmer weather reduced demand for energy.

- Italy's anti-establishment 5-Star Movement supports the EU and wants significant law-making powers transferred from governments to the European Parliament, its leader Luigi Di Maio told Reuters. 5-Star, which leads opinion polls ahead of an election to be held by May, is trying to reassure Italy's partners and financial markets that it can be trusted in government, and distance itself from its previously eurosceptic positions.

Rates

U-turn on disappointing wage inflation

Global core bonds trading showed two faces. They traded with a downward bias going into the US payrolls report on the back of positive risk sentiment. The US government averted an imminent shutdown, but the deal only postpones the problem by two weeks (Dec 22 new deadline). US President Trumps was rumoured to be readying phase two in its fiscal stimulus plan, infrastructure spending, by January. PM May and EC Juncker sounded confident on the completion of part 1 of Brexit-talks even if the agreement lacked details. Nevertheless, political developments weighed on core bonds. Trading made a U-turn after the payrolls report. Net job creation remained strong and the unemployment rate is still at the lowest level since 2000. However, earnings disappointed. The market reaction proves sensitivity to price/inflation data. The US Note future gradually gained momentum and trades currently around the intraday highs. The scale of the move remains limited though with next week's Fed meeting looming. Investors don't want to be wrongfooted by a Fed who still intends to hike rates three times next year.

At the time of writing, the German yields curve shifts 0.6 bps to 0.9 bps higher. The German 10-yr yield remains dangerously close to the 0.3% support level. The US yield curve steepens with yield changes ranging between -1.4 bps (2-yr) and +0.7 bps (30-yr). On intra-EMU bond markets, 10-yr yield spread changes versus Germany are unchanged with the periphery outperforming (-3 bps to -5 bps) and a stellar performance from Greece (-33 bps). Greek bonds continue to profit from last week's debt swap.

Currencies

Poor wage growth caps further USD gains

A positive risk sentiment kept the dollar near recent highs against the euro and the yen this morning as markets counted down to the US payrolls. US job growth remained strong, but wage growth again missed expectations. With markets currently giving more weight to prices rather than activity data, the dollar even declined off the intraday peak after the payrolls. EUR/USD trades in the 1.1760 area. USD/JPY is changing hands around 113.30.

Asian equities extended yesterday's comeback overnight with Japan taking the lead. Regional data (Japan Q3 GDP and Chinese trade data) were supportive for equities and so was the prospect of a EU/UK Brexit agreement and the US Congress avoiding a government shutdown. The overall positive sentiment via higher core yields supported the dollar. USD/JPY extended gains north of 113. EUR/USD drifted to the mid 1.17 area.

There were plenty of headlines on Brexit and US politics (Agreement to extend government funding till 22 Dec; Trump proposals on infrastructure investment) this morning. The reaction of global markets was quite similar to what often happened late. European equities succeeded quite an impressive risk rebound, but with little spill-overs to other markets, including interest rate and FX markets. The dollar held near the recent highs against the yen and the euro, but the rally ran into resistance, awaiting the US payrolls.

The payrolls brought again a diffuse picture. Job growth (228k) beat consensus by a substantial margin. The jobless rate remained at the lowest level since 2000, but wage growth disappointed 0.2% M/M and 2.5% Y/Y; 0.3% M/M and 2.7% Y/Y was expected). As markets are quite sensitive to price data these days, US yields and the dollar even declined slightly. USD/JPY trades in the 113.30 area. EUR/USD rebounds to the 1.1765 area, off the intraday low around 1.1730. The dollar showed quite constructive price action this week, but this mixed payrolls report probably hampers further US gains ahead of Wednesday's Fed policy decision.

Sterling rally stalls despite first 'Brexit agreement'

Sterling rallied yesterday evening and this morning on headlines that the EU and the UK agreed to move to the second stage of the Brexit negotiations. The agreement was officially announced at a press conference with EU commission head Juncker and UK PM early this morning. Sterling touched a ST top during (cable) or soon after (GBP/EUR) the press conference. Cable filled offers in the 1.3520 area. EUR/GBP almost exactly tested the 0.8593 62% retracement support. The negotiations proceeding to a next stage for sure is good news for the UK. However, markets soon realized that the hard work still has to be done, even on the details of the separation. The sterling rally ran into resistance and the UK currency gradually returned some of the overnight gain, especially against the dollar. UK production data were as expected. The trade deficit was smaller than expected. However, the data were not the focus of markets. EUR/GBP trades currently in the 0.8750/60 area. Cable dropped to the 1.34 area, but regained a few ticks on USD softness after the payrolls (currently 1.3425).

Weekly Focus: Central Bank Meetings for Christmas

Market movers ahead

- We have a very busy central bank week ahead, with Fed, ECB, BoE and Norges Bank meetings coming up. We expect only the Fed to change its policy rate, hiking the target range to 1.25-1.50%.

- We are due to get inflation data from the US, UK, Japan, Denmark, Sweden and Norway.

- We expect EU leaders to say that the UK and EU can start discussing the future relationship at next week's EU summit.

- Focus remains on US tax reform and whether the Republicans are able to pass it already before Christmas.

Global macro and market themes

- We expect the global expansion to continue lending support to profits and risk assets.

- We do not project a bond bear market though. Rather we look for more US curve flattening.

- Credit spreads are set to narrow further on a search for yield and low default rates.

- In the FX space, we look for a weaker USD and a stronger GBP and NOK in 2018.

Elliott Wave analysis: USDCAD and DAX Update

USDCAD came lower and is now testing a support level at 1.2812 from where we may see a new turn up if we consider the shape of an expanded flat formation in four. If we get a deeper pullback, then keep an eye on 1.2782 level.

USDCAD

DAX did not respond much to NFP figures; we see slow price move here around 13200 so it can be just a small and minor pause within uptrend that may continue up to around 13300 or even to 13350 area from where we will expect a turn lower next week.

Dax, 1h

Canada: Housing Starts Robust in November

Canadian builders broke ground on 252k (SAAR) housing units in November, 13% higher than October and marking a very robust level of activity. The 6-month moving average rose to 226k from 217k during the month.

Starts in the volatile multi-family segment drove the headline increase, advancing 16.5% in the month. Meanwhile, housing construction increased by 5.9% in the single-detached market.

Provincially, starts were up in 6 of 10 provinces, led by Ontario were starts increased by a whopping 38k to 98k units - marking the highest pace of construction since January. Starts were also higher in Manitoba (+1.5k to 6.9k units) and Alberta (+5k to 34k units) with the pace of homebuilding in the latter market the highest since March. New home construction also increased in all of the Atlantic Provinces except New Brunswick. In B.C., starts moderated slightly from the multi-decade high reached in October, though the level was nonetheless solid at 48k.

Starts in the closely watched Toronto market increased to 45k from 28k in October. However, they have slowed so far in Q4 versus Q3's robust pace. Homebuilding activity in Vancouver dropped by 3k to 32k in the month. However, this follows a surge in October, leaving starts at a very healthy level. A similar story emerged in Montreal, with starts falling to 26k (down 15k) retracing some of the strong gain in October.

Key Implications

Homebuilding activity was extremely solid in November, rising to its highest level since April 2012. Housing construction has remained resilient this year despite the 'one-two punch' of regulatory measures aimed at cooling housing demand and rising mortgage rates. Ultimately, a healthy economic backdrop and firm population growth have provided support to homebuilding activity nationally.

In particular, Ontario's sizzling monthly gain provides some evidence that market has so far been able to shake off the impacts of the Fair Housing Plan, which slowed sales and building activity earlier in the year.

Despite today's blowout report we expect homebuilding to ease to a sub-200k pace in 2018, as higher mortgage rates and updated B20 regulations from OSFI weighing on housing starts, with disproportional impact on the Toronto and Vancouver markets where housing affordability remains highly stretched. Recent building permit data supports this view, with a softening trend in construction intentions in recent months pointing to a cool-off of starts activity in coming quarters.

U.S. Economy Churns Out Another Solid Job Report in November

The U.S. economy churned out a solid 228k new jobs in November, better than markets were expecting. The unemployment rate held steady at 4.1%, a 17-year low.

The details of the report were solid. Employment growth on the goods side of the economy accelerated (+62k) on gains in construction (+24k) and manufacturing (+31k). The services sector posted a solid 159k new positions led by education & health (+54k) and business services (+46k).

The fact that the unemployment rate held steady is impressive, given last month's drop to 4.1% was driven by a sizeable drop in the labor force (-765k). In November growth in the labor force roughly kept pace with job creation. The overall participation rate was unchanged at 62.7%. The employment to population ratio fell slightly to 60.1%, but is still higher than a year ago.

One small cloud in the report was a modest gain in average hourly earnings (+0.2% m/m). On a year-on-year basis wage gains are up a 2.5%. That pace is faster than inflation, but is increasingly looking like a puzzle in a labor market where the pool of unemployed and discouraged workers is below its pre-recession levels.

Key Implications

The U.S. job market continued its impressive performance in November. The Fed is well justified in classifying the U.S. at full employment.

Modest wage gains are a little perplexing, but they are likely to pick up in the months ahead. Other measures of wage growth show healthier increases. The Atlanta Fed wage tracker has been hovering round 3.5% year-on-year over the past two years.

As Republicans in Washington work feverishly to finalize a tax plan, the tight labor market increasingly looks to be a constraint that will limit the impact on economic growth. As workers become harder to find, this may be the impetus that sparks the much-anticipated acceleration in wage growth.

It is all systems go for a rate hike next week by the FOMC. While there may be some on the Fed who express concerns about the modest pace of core inflation, we have seen some progress on that score. Continued progress in the labor market should see the Fed continue to raise rates at a gradual pace.

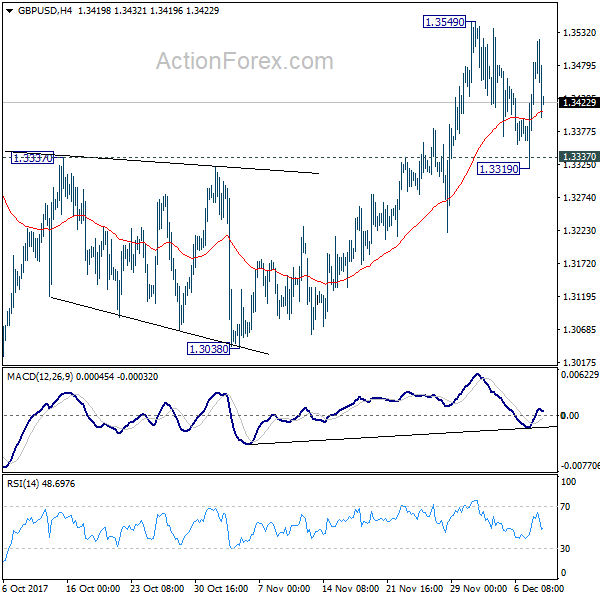

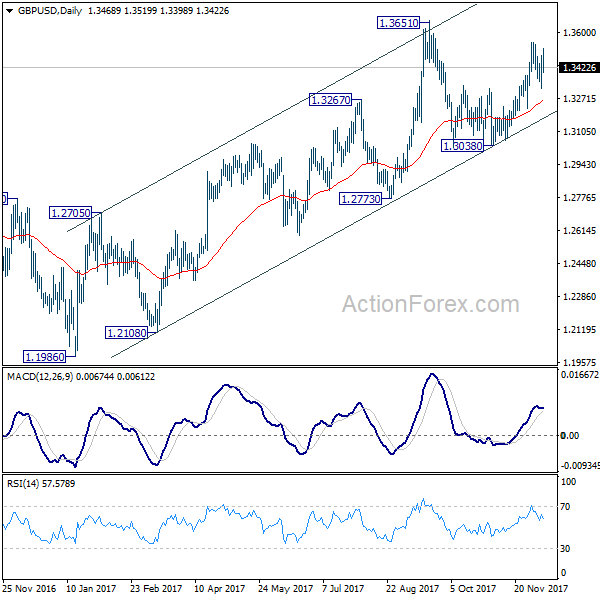

GBP/USD Mid-Day Outlook

Daily Pivots: (S1) 1.3366; (P) 1.3425; (R1) 1.3530; More....

GBP/USD failed to take out 1.3549 resistance and retreats. Intraday bias remains neutral at this point. As long as 1.3337 holds, further rise is expected. Break of 1.3549 will target 1.3651 high and above. However, decisive break of 1.3337 will argue that rise from 1.3038 has completed and turn bias back to the downside for this support.

In the bigger picture, while the medium term rebound from 1.1946 low is strong, it's still limited below 1.3835 key support turned resistance. As long as 1.3835 holds, we'd view such rebound as a correction. That is, we'd expect another leg in the long term down trend through 1.1946 low. However, sustained break of 1.3835 should at least send GBP/USD to 38.2% retracement of 2.1161 (2007 high) to 1.1946 (2016 low) at 1.5466.

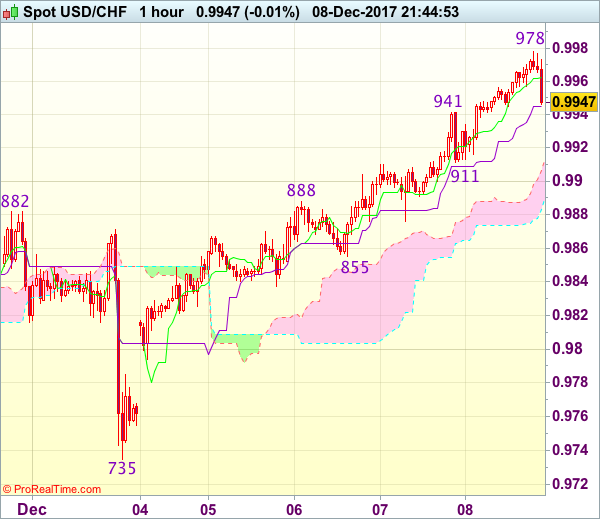

Trade Idea Wrap-up: USD/CHF – Buy at 0.9890

USD/CHF - 0.9943

Most recent candlesticks pattern : N/A

Trend : Near term up

Tenkan-Sen level : 0.9959

Kijun-Sen level : 0.9945

Ichimoku cloud top : 0.9913

Ichimoku cloud bottom : 0.9889

Original strategy :

Buy at 0.9900, Target: 1.0000, Stop: 0.9865

Position : -

Target : -

Stop : -

New strategy :

Buy at 0.9890, Target: 0.9990, Stop: 0.9855

Position : -

Target : -

Stop : -

As the greenback has surged again after brief pullback and broke above previous resistance at 0.9947, adding credence to our bullish view that the rise from 0.9735 low is still in progress, hence test of resistance at 0.9987 would be seen, above there would encourage for headway to 1.0000, however, near term overbought condition should limit upside and reckon recent high at 1.0038 would hold from here, risk from there is seen for a retreat later.

In view of this, would not chase this rise here and we are looking to buy dollar on dips as 0.9900 should limit downside and bring another rebound. Below previous resistance at 0.9882-88 (now support) would defer and risk correction towards support at 0.9855 but only break there would signal top is formed instead.

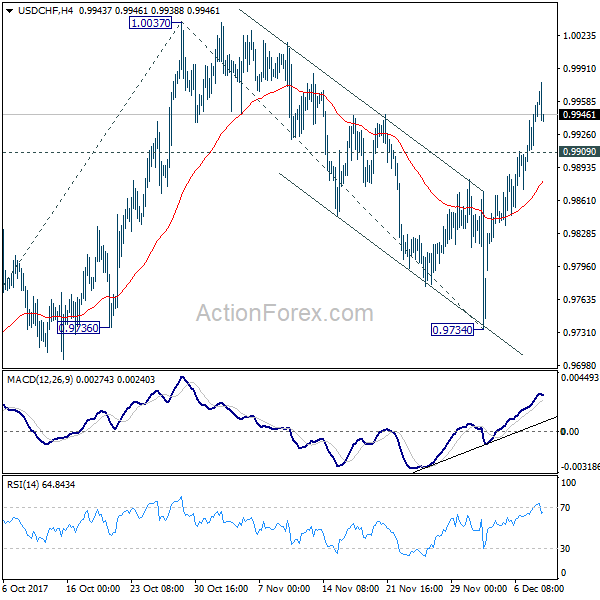

USD/CHF Mid-Day Outlook

Daily Pivots: (S1) 0.9892; (P) 0.9919; (R1) 0.9969; More....

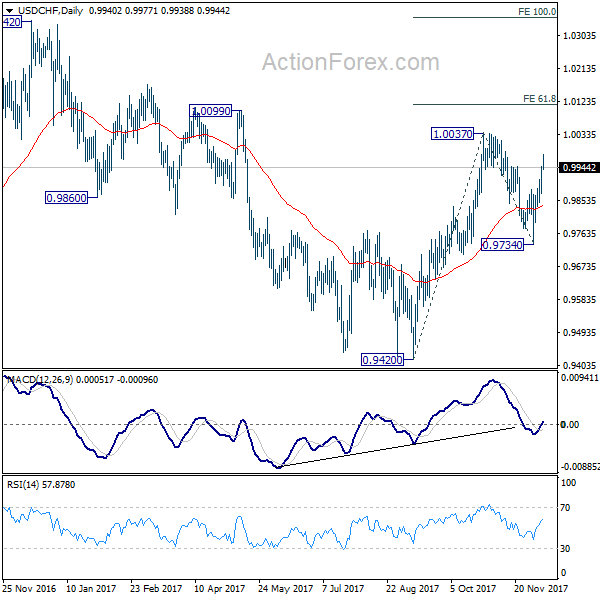

With 0.9909 minor support intact, intraday bias in USD/CHF remains on the upside for 1.0037 resistance. Firm break there will confirm resumption of whole rise from 0.9420 and target 61.8% projection of 0.9420 to 0.9734 from 1.0047 at 1.0115 next. On the downside, below 0.9909 minor support will turn bias neutral and bring consolidations first.

In the bigger picture, range trading continues between 0.9420/1.0342. At this point, 0.9420 appears to be a strong support level. Therefore, in case of decline attempt, we don't expect a firm break of this level. Nonetheless, strong break of 1.0342 is also needed to confirm upside momentum. Otherwise, medium term outlook will stay neutral.

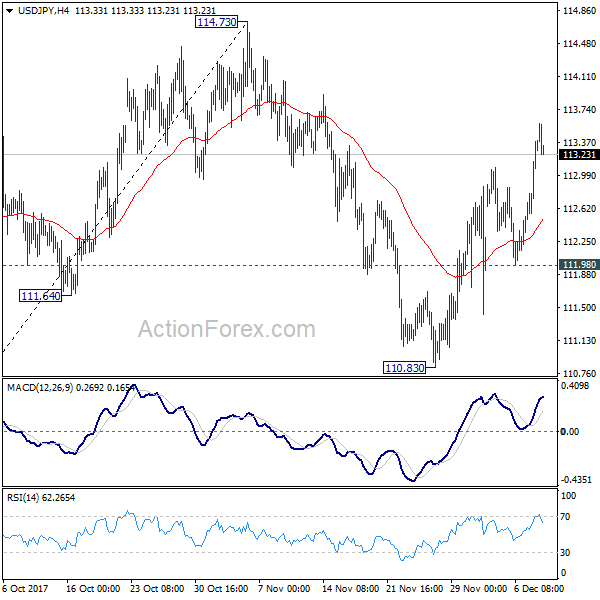

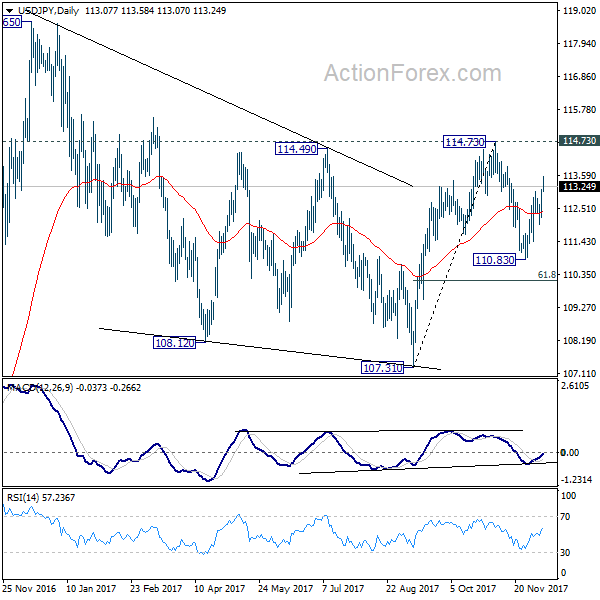

USD/JPY Mid-Day Outlook

Daily Pivots: (S1) 112.48; (P) 112.81; (R1) 113.42; More...

Intraday bias in USD/JPY remains on the upside for 114.73 key near term resistance. Decisive break there pave the way to retest 118.65 high. On the downside, break of 111.98 support is needed to indicate near term reversal. Otherwise, outlook will be mildly bullish in case of retreat.

In the bigger picture, we're holding on to the view that correction from 118.65 is completed a 107.31. And medium term rise from 98.97 (2016 low) is resuming. Sustained break of 114.73 should affirm our view and send USD/JPY through 118.65. However, break of 107.31 will dampen this will and extend the medium term fall back to 98.97 low.

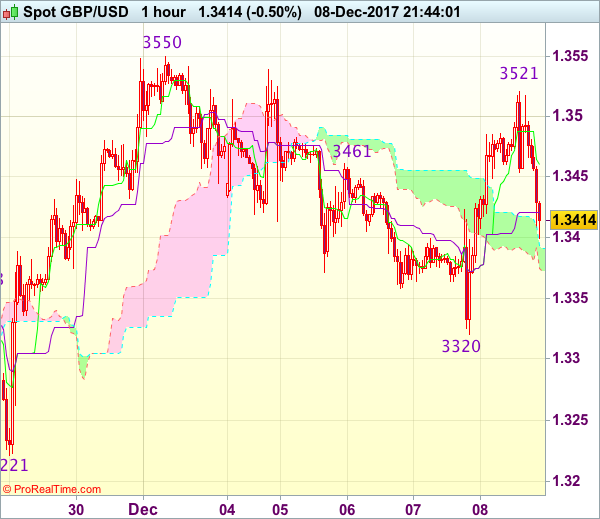

Trade Idea Wrap-up: GBP/USD – Stand aside

GBP/USD - 1.3423

Most recent candlesticks pattern : N/A

Trend : Near term up

Tenkan-Sen level : 1.3460

Kijun-Sen level : 1.3446

Ichimoku cloud top : 1.3391

Ichimoku cloud bottom : 1.3372

New strategy :

Stand aside

Position : -

Target : -

Stop : -

Despite yesterday’s anticipated selloff to 1.3320, the subsequent strong rebound on active cross-buying in sterling suggests low has been formed there and further choppy trading would take place, hence gain to 1.3525-30 cannot be ruled out, however, as outlook remains consolidative, reckon upside would be limited and recent high at 1.3550 should hold, bring retreat later.

As near term outlook is mixed, would be prudent to stand aside in the meantime. Below 1.3370-75 would prolong choppy trading and risk weakness to 1.3350 and price should stay well above said support at 1.3320, bring another rebound.