Sample Category Title

Bitcoin Bonanza

We are fast approaching the make-or-break moment for Bitcoin. Prices gyrated wildly Thursday with some exchanges nearing $20,000 but systems clearly came under a strain. In FX, sterling gathers upward momentum on news that DUP intends to strike a deal with PM May and on firm services PMI and the Australian dollar quietly fell to a six-month low. The US jobs report is up next. 2 new trade actions in the Premium Insights were issued on EURUSD.

It's impossible to avoid talking about Bitcoin at the moment, which is now surely the defining mania of our era. What's not clear is how and when it will end but aside from the violent price swings, the warnings signs are mounting. The first is the increasingly slow and expensive transaction costs. It's clear that Bitcoin will never replace fiat currency – long one of the tenants of the bull theory. It currently costs $13 to do any transaction and takes upwards of 7 hours to verify a transaction at that price.

One thing everyone will be hearing more about in the days ahead are the mempool. This is the backlog of transactions and it's growing at a fast rate. If there is ever a stampede to the exits, this problem will be a devastating bottleneck. At the same time, the exchanges are under increasing strain. Outages hit the main trading hubs again on Thursday. That's a major red flag.

Bitcoin has proven significant resilience to bad news. The dip after hitting $10,000 was bought and reports of hacks, theft and fraud are brushed aside. That's a sign of a roaring market.

The catalyst that everyone is watching is the introduction of futures trading this week at CBOE and next week at the CME. Both are cash-settled contracts so they shouldn't affect the underlying market, especially since short-term arbitrage is nearly impossible because of the transaction times.We will be watching closely.

Elsewhere, the US dollar founds its legs on Thursday as USD/JPY rose to a three-week high and AUD/USD fell to a six-month low. Non-farm payrolls is due on Friday and indications from the ADP report was another strong jobs print but the focus will remain on wages. If they tick up, then the dollar could start to recover much of the July/Aug declines.

Euro Falls To 2-Week Low, US Nonfarm Payrolls Ahead

The euro continues to lose ground this week. In the Friday session, EUR/USD is trading at 1.1735, down 0.32% on the day. In economic news, Germany's trade surplus fell to EUR 19.9 billion, missing the estimate of EUR 22.0 billion. This marked a 3-month low. There was better news out of France, as Industrial Production surged 1.9%, crushing the estimate of -0.1%. This marked the strongest manufacturing output reading since May. In the US, the focus is on employment numbers. Nonfarm payrolls is expected to soften to 198 thousand, while wage growth is forecast to rebound with a gain of 0.3%. The unemployment rate, which stands at a sizzling 4.1%, is expected to remain unchanged.

November's ADP nonfarm payrolls managed to beat expectations earlier this week, but the reading was sharply lower than the October release. Will the official nonfarm payrolls follow suit? The markets are bracing for a soft NFP, with a forecast of 200 thousand, down from 261 thousand in the previous release. Wage growth has been stubbornly low, despite a strong labor market and assurances from Fed policymakers that inflation and wages will move upwards. The markets are expecting some good news on Friday, with Average Hourly Earnings expected to gain 0.3%. The October reading of 0.0% was a disappointment, missing the forecast of 0.2%. Traders should be prepared for some movement from EUR/USD during the North American session.

Ireland is in the spotlight on both sides of the Channel, as the UK and European Union scramble to find a solution to the vexing question of the status of the Irish border after Brexit. An embattled Prime Minister May is desperate to move on to trade talks with the EU, but the Europeans want to wrap up the non-trade issues first. There had been hopes of a major announcement following a meeting between Prime Minister May and European Commission President Jean-Claude Juckner. However, these expectations were left on hold, as it became apparent that wide gaps remain on two key issues – Northern Ireland and the European Court of Justice. The European Union is willing to let EU rules apply to Northern Ireland, but the small DUP party, which is keeping the May government afloat, is against any steps which could be seen as separating the UK mainland from Northern Ireland. A solution that will satisfy the UK, the EU and the DUP over the Irish border remains elusive. Another thorny issue is whether the European Court of Justice will apply to European citizens in the UK after Brexit. While the EU is in favor of the court having authority over these citizens, many British lawmakers feel that such a move would undermines British sovereignty. The EU holds a key summit on December 12, and all sides are hoping to wrap up the non-trade sticking points before the meeting.

Market Update – European Session: Brexit Negotiations Poised To Move Into Phase 2

Notes/Observations

EU to recommend sufficient progress in Brexit talks; EU leaders to make final decision on progress after Britain made substantive changes to its proposed border text for a deal with the European Union

US Senate passing an interim spending bill through to December 22nd

Looking ahead; Nov US Payrolls in focus with wage data being key for inflation developments

Asia:

China Nov Trade Balance: $40.2B V $35.0BE; Exports registers its fastest growth since March) (Y/Y: 12.3% v 5.3%e); Imports best suggesting that China's rebalancing strategy was working

Japan Q3 Final GDP Q/Q: 0.6% v 0.4%e; GDP Annualized Q/Q: 2.5% v 1.5%e

Europe:

German SPD Party Congress voted in favor of entering talks on joining a ‘grand coalition' with Chancellor Merkel's CDU party. SPD wants open-ended talks that leave form of support open; talks could take months before next German government takes office - Ireland Dep PM Coveney (Foreign Min): Deal Confirmed! Ireland supports Brexit negotiations moving to Phase 2 now that we have secured assurances for all on the island of Ireland; no hard border

Americas:

US Congress passed legislation to fund Govt through Dec 22nd. House of Representatives voted 235-193; Senate voted 81-14

GOP congressional leaders reportedly mulling 22% corporate tax rate level (vs 20%) as bill deadline nears

White House Press Sec Sanders: expect Congress will pass a 'clean' stopgap spending measure

Economic Data:

(NL) Netherlands Oct Manufacturing Production M/M: -0.7% v +1.4% prior; Y/Y: 4.0% v 5.2% prior, Industrial Sales Y/Y: 6.6% v 6.0% prior

(DE) Germany Oct Current Account: €18.1B v €20.0Be; Trade Balance: 18.9B v €21.9Be; Exports M/M: -0.4% v +1.0%e; Imports M/M: 1.8% v 1.0%e

(DE) Germany Q3 Labor Costs Q/Q: 0.7% v 0.1% prior; Y/Y: 2.2% v 2.3% prior

(FR) France Oct Industrial Production M/M: +1.9%% v -0.1%e; Y/Y: 5.5% v 2.9%e

(FR) France Oct Manufacturing Production M/M: 2.7% v 0.4% prior; Y/Y: 6.9% v 3.1% prior

(FR) France Oct YTD Budget Balance: -€77.1B v -€76.3B prior

(TW) Taiwan Nov Trade Balance: $6.0B v $5.0Be; Exports Y/Y: 14.0% v 9.4%e; Imports Y/Y: 9.0% v 6.7%e

(CZ) Czech Nov Unemployment Rate: 3.5% v 3.5%e - (HU) Hungary Nov CPI M/M: 0.4% v 0.5%e; Y/Y: 2.5% v 2.6%e - (IS) Iceland Q3 GDP Q/Q: +2.2 v -1.1% prior; Y/Y: 3.1% v 3.4% prior

(UK) Oct Industrial Production M/M: 0.0% v 0.0%e; Y/Y: 3.6% v 3.5%e

(UK) Oct Manufacturing Production M/M: 0.1% v 0.0%e; Y/Y: 3.9% v 3.8%e

(UK) Oct Visible Trade Balance: -£10.8B v -£11.5Be, Overall Trade Balance: -£1.4B v -£3.0Be, Trade Balance Non EU: -£2.4B v -£3.3Be

(UK) BoE/TNS Nov Quarterly Inflation Survey (next-12months): 2.9% v 2.8% prior

(GR) Greece Nov CPI Y/Y: 1.1% v 0.7% prior; CPI EU Harmonized Y/Y: 1.1% v 0.5% prior

Fixed Income Issuance:

(IN) India sold total INR150B vs. INR150B indicated in 2022, 2031, 2033, 2035 and 2055 bonds

(ZA) South Africa sold total ZAR900M vs. ZAR900M indicated in I/L 2029, 2033 and 2050 bonds

(SE) Sweden sold SEK770M in 0.25% I/L 2022 bond; Avg Yield: -2.0557 v -1.8724% prior; Bid-to-cover: 1.77x v 4.04x

SPEAKERS/FIXED INCOME/FX/COMMODITIES/ERRATUM

Equities

Indices [Stoxx600 +0.9% at 389.7, FTSE +0.2% at 7338, DAX +1.1% at 13185, CAC-40 +0.7% at 5419, IBEX-35 +1.0% at 10366, FTSE MIB +1.3% at 22741, SMI +0.3% at 9297, S&P 500 Futures +0.2%]

Market Focal Points/Key Themes: European Indices trade higher across the board, with strong gains in Germnay Spain and Italy, as the EU recommends Brexit negotiation move on phase 2. The FTSE 100 underperforms as the rise in Cable weighs on the Index. Berkeley Group outperforms in the UK after first half results, while Carl Zeiss trades higher after full year results which came slightly ahead of views. In the Healthcare space Erytech trades over 25% lower afters its phase 2b study failed to meet primary endpoint; Thrombogenics trades sharply lower after its Circle trial has been discountinued. The Banking Sector outperforms afteBasel Committee publishes the results of a cumulative quantitative impact study alongside the finalisation of the Basel III post-crisis reforms

Equities

Consumer discretionary [Air France [AF.FR] +1.2% (Nov Metrics), Carl Zeiss [AFX.DE] +1.2% (Earnings)]

Financials: [ Swiss Re [SREN.CH] +0.7% (CFO Steps down)]

Healthcare: [ Erytech [ERYP.FR] -31% (Trial did not meet primary endpoint), Thrombogenics [THR.BE] -18% (Discontinues Phase II Circle trial)]

Real Estate: [Berkeley Group [BKG.UK] +9% (Earnings)]

Speakers

EU Commission stated that it had reached a breakthrough in Brexit negotiations and now ready for second phase of negotiations as it got the breakthrough needed via compromise. UK PM May assured that she had backing for deal. EU to recommend sufficient progress in Brexit talks while EU leaders to make final decision on progress, Hopeful member States share the Brexit assessment (**Note Summit is on Thurs, Dec 14th)

EU's Tusk confirmed that Brexit progress had been made; should begin negotiating the transition period for clarity. To ask EU leaders to begin transition period immediately and ready to explore close EU-UK trade links. UK wanted a transition period of 2 years; UK should respect all EU laws during the transition period as well as budgets and courts. EU decision making during the period will be without UK

EU Chief Brexit Negotiator Barnier to recommend that Brexit move into phase two of negotiations. Needed final version of withdrawal by Oct 2018. UK to honor all financial commitments and contributed to 2019 and 2020 budget. All phases are difficult in the Brexit negotiations; still need to spell out details . UK trade deal to be modeled after Canada's

UK Brexit Min Davis: Big step forward in delivering the Brexit

Ireland PM Varadkar: Sufficient progress made on Irish issues; UK committed to avoid a hard border. Citizens rights and common travel area remain. The Good Friday agreement was protected, Northern Ireland and UK will not drift apart

Northern Ireland's Democratic Unionist Party (DUP) saw a breakthrough in Brexit border talk as Britain made substantive changes to its proposed text for a deal with the European Union. No red line down the Irish Sea and clear confirmation that the entirety of the United Kingdom was leaving the European union

Swiss Stats Office updated its inflation forecasts which maintained 2017 CPI forecast at 0.5% and 2018 CPI forecast at 0.2%. It set 2019 CPI at 0.1%

Sweden Central Bank (Riksbank) Gov Ingves: Investigating whether an e-Krona currency is needed

Russia Central Bank's Morozov: 2018 CPI more likely to be below 4% than above it. Saw economic growth stabilizing around 1.5%

China govt to implement new concepts in its 2018 economic work. To curb leverage ratio in 2018

Currencies

The Brexit breakthrough paved the way for the 2nd phase of negotiations has aided the GBP currency. Britain made substantive changes to its proposed text for a deal with the European Union . EUR/GBP cross hit 6-months lows as it tested below the 0.87 level. GBP/USD did manage to retest above 1.35 but remained far below the key resistance of 1.36.

Overall the USD continued to gain ground across the board against the major pairs. EUR/USD at 1.1735 and USD/JPY at 113.55. Focus on the US jobs report due out later today.

Fixed Income

Bund futures trade 163.29 down 22 ticks, staying in a tight range so far in December. Continued downward pressure sees 162.10 followed by 161.50. A reversal targets 163.75 then 164.33.

Gilt futures trade at 124.68 down 54 ticks, sliding amid risk-on tone and Brexit progress. Continued upside eyeing 125.25 then 126.35. Downside targets include 124.25 then 123.75.

Friday's liquidity report showed Thursday's excess liquidity fell to €1.907T from €1.914T. Use of the marginal lending facility rose to €146M from €123M prior.

Corporate issuance saw 7 issuers raise $4.8B in the primary market. Lipper reports equity fund inflows of $3B in week ending Dec 6th. High yield funds saw inflows of $217.4M in the week.

Looking Ahead

(MX) Mexico Nov Nominal Wages: No est v 3.8% prior

(UR) Ukraine Nov CPI M/M: No est v 1.2% prior; Y/Y: No est v 14.6% prior

06:00 (BR) Brazil Nov IBGE Inflation IPCA M/M: 0.4%e v 0.4% prior; Y/Y: 2.9%e v 2.7% prior

06:00 (FI) Finland Parliament could hold confidence vote

06:00 (UK) DMO to sell combined £4.5B in 1-month, 3-month and 6-month Bills (£2.0B, £1.0B and £1.5B respectively)

06:30 (IS) Iceland to sell Bonds - 06:30 (IN) India Weekly Forex Reserves

06:45 (US) Daily Libor Fixing

08:00 (UK) Nov NIESR GDP Estimate: 0.4%e v 0.5% prior

08:00 (IN) India announces upcoming Bill auction (held on Wed)

08:05 (UK) Baltic Dry Bulk Index

08:15 (CA) Canada Nov Annualized Housing Starts: 213.0Ke v 222.8K prior

08:30 (US) Nov Change in Nonfarm Payrolls: +195Ke v +261K prior, Change in Private Payrolls: +198Ke v +252K prior, Change in Manufacturing Payrolls: +15Ke v +24K prior

08:30 (US) Nov Unemployment Rate: 4.1%e v 4.1% prior, Underemployment Rate: No est v 7.9% prior

08:30 (US) Nov Average Hourly Earnings M/M: 0.3%e v 0.0% prior; Y/Y: 2.7%e v 2.4% prior; Average Weekly Hours: 34.4e v 34.4 prior

08:30 (CA) Canada Q3 Capacity Utilization Rate: No est v 85.0% prior

10:00 (US) Dec Preliminary University of Michigan Confidence: 99.0e v 98.5 prior

10:00 (US) Oct Final Wholesale Inventories M/M: -0.4%e v -0.4% prelim; Wholesale Trade Sales M/M: 0.3%e v 1.3% prior

11:00 (EU) Potential Sovereign ratings after EU close

(EG) Egypt Sovereign Debt to be rated by Moody's

(IS) Iceland Sovereign Debt to be rated by Fitch

(PL) Poland Sovereign Debt to be rated by DBRS

(PL) Poland Sovereign Debt to be rated by Fitch

(RO) Romania Sovereign Debt to be rated by Moody's

13:00 (US) Weekly Baker Hughes Rig Count data

20:30 (CN) China Nov CPI M/M: No est v 0.1% prior; Y/Y: 1.8%e v 1.9% prior, PPI Y/Y: 5.8%e v 6.9% prior

US Nonfarm Payrolls To Boost The Dollar

US Nonfarm payrolls to boost the dollar

The dollar is strengthening ahead of the Nonfarm payrolls that will released as usual the first Friday of the month at 2.30pm. Expectations are anyway strong with markets awaiting a release slightly below 200k.

The greenback is driven higher and is now trading at levels around two-week highs against the single currency. In the same time US equities continue to increase. The famous Christmas Rally has already started and the NFPs will bring everything but stop the equity rally. Yet this definitely seems timid compared to what is happening now for Bitcoin.

Amid the NFPs' release, we will also carefully consider the hourly wages growth which will likely provide any hints of inflationary pressures. Expectations are of an increase to 2.7 y/y from 2.4. This is also why we maintain our view that inflation is coming back up in the US and even though the Fed will raise rates next week, markets are still unsure about what will be the Fed monetary policy for 2018. Three rate hikes a year seem like difficult to achieve as pressures on all asset classes will not be sustainable. This may be one opportunity to buy back the euro against the dollar on the dip this afternoon.

Step forward of EU / UK Negotiations

With the likelihood of a ‘soft' Brexit on the rise, the British pound jumped: in Friday trading, EUR/GBP fell to 0.8689 and GBP/USD rose to 1.3520.

Markets welcomed the news that the United Kingdom and the European Union have reached a preliminary agreement on the UK's departure from the EU, including a resolution of the tricky border between Northern Ireland and the Irish Republic. Also settled are the general financial terms and the rights of EU citizens living in the UK and UK subjects living in the EU. Just as all hope seemed lost, a deal was agreed, which makes it hard for us to see anything but a soft Brexit.

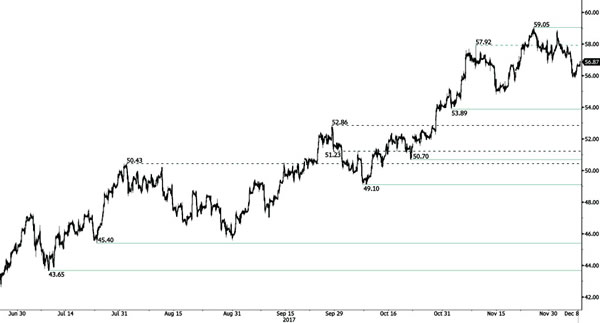

CRUDE OIL Losing Steam

Crude oil continues its consolidation phase and should not challenge the 60-dollar level. Expected to show continued sideways move. Support is given at a distance at 54.81 (14/11/2017 low)

In the long-term, crude oil has recovered after its sharp decline last year. However, we consider that further weakness are very likely. For the time being the pair lies in an upside momentum. Strong support lies at 35.24 (05/04/2016) while resistance can now be found at 55.24 (03/01/2017 high).

SILVER Collapsing

Silver is heading lower. Hourly support can be found at 15.61 (14/07/2017 low). Hourly resistance is given at 17.46 (13/10/2017 high). Expected to keep pushing lower.

In the long-term, the trend is rater negative. Further downsides are very likely. Resistance is located at 25.11 (28/08/2013 high). Strong support can be found at 11.75 (20/04/2009).

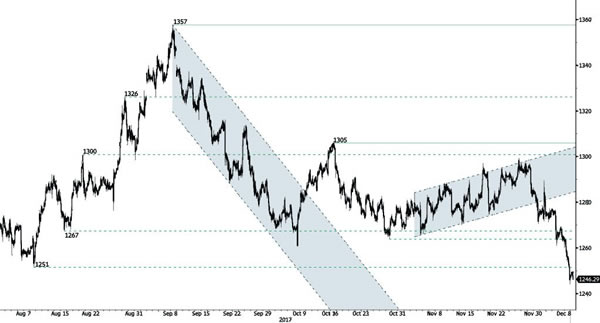

GOLD Ready For Further Downside

Gold is pushing lower. The technical structure confirms the end of the consolidation phase. Support given at 1251 (08/08/2017 high) is on target. Resistance is located at 1288 (20/10/2017).

In the long-term, the technical structure suggests that there is a growing upside momentum. A break of 1392 (17/03/2014) is necessary ton confirm it, A major support can be found at 1045 (05/02/2010 low).

BITCOIN Consolidating After Massive Increase

Bitcoin is now consolidating. The technical structure has shown a tremendous positive short-term momentum. Hourly support is located at 9000 (29/11/2017 low). Strong support stands very far at 2975 (22/08/2017 low). In the shortterm, the digital currency should continue rising at levels unseen so far.

In the long-term, the digital currency has had an exponential growth. There are decent likelihood that the asset will reach $40'000 in 2018.

EUR/CHF Monitoring The 1.17 Level

EUR/CHF continues to push towards resistance area above 1.17 and support given at 1.1610 (27/10/2017 low). Expected to show continued increase.

In the longer term, the technical structure has reversed. Strong resistance is given at 1.20 (level before the unpeg). Yet, the ECB's QE programme is likely to cause persistent selling pressures on the euro, which should weigh on EUR/CHF. Supports can be found at 1.0184 (28/01/2015 low) and 1.0082 (27/01/2015 low).

EUR/GBP Breaking Strong Support

EUR/GBP is heading lower. The pair has failed to hold above broken support at 0.8791 (07/11/2017 low). Resistance is located at 0.8943 (27/11/2017 high). Expected to go even lower.

In the long-term, the pair has largely recovered from recent lows in 2015. The technical structure suggests a growing upside momentum. The pair is trading above from its 200 DMA. Strong resistance can be found at 0.9500 (psychological level).