Sample Category Title

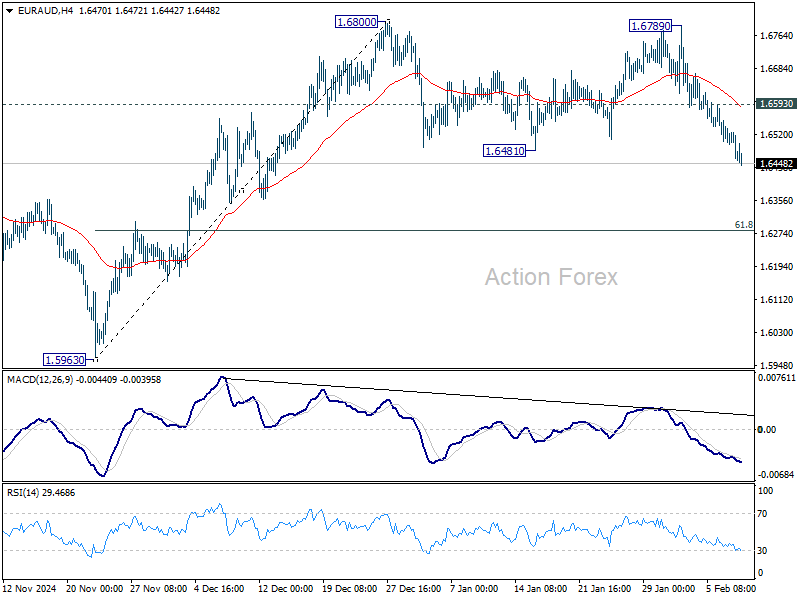

EUR/AUD Daily Outlook

Daily Pivots: (S1) 1.6428; (P) 1.6493; (R1) 1.6531; More...

Intraday bias in EUR/AUD remains on the downside for the moment. A double top reversal pattern (1.6800, 1.6789) could be formed. Deeper fall should be seen to 61.8% retracement of 1.5963 to 1.6800 at 1.6283. On the upside, however, break of 1.6593 minor resistance will dampen this bearish case and turn bias back to the upside for retesting 1.6800 instead.

In the bigger picture, with 1.5996 key support (2024 low) intact, larger up trend from 1.4281 (2022 low) is still in favor to resume through 1.7180 at a later stage. Nevertheless, sustained break of 1.5996 will indicate that such up trend has completed and deeper decline would be seen.

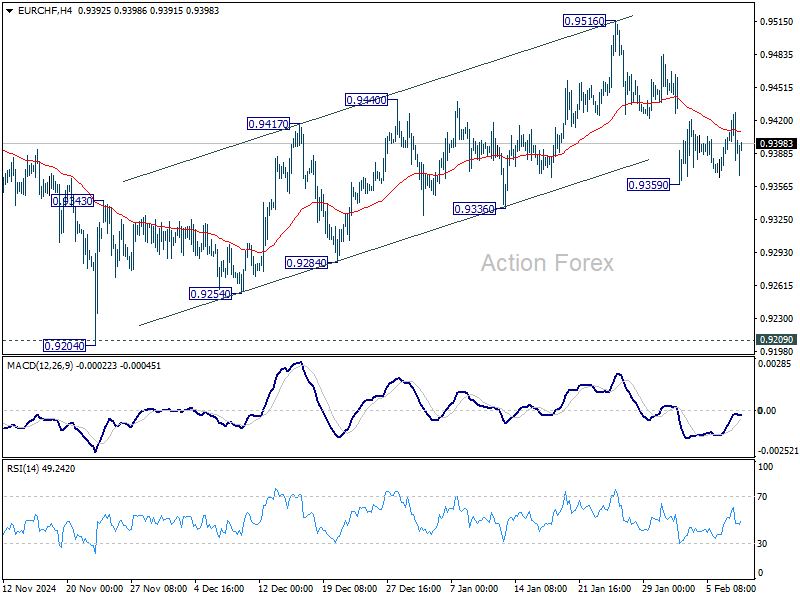

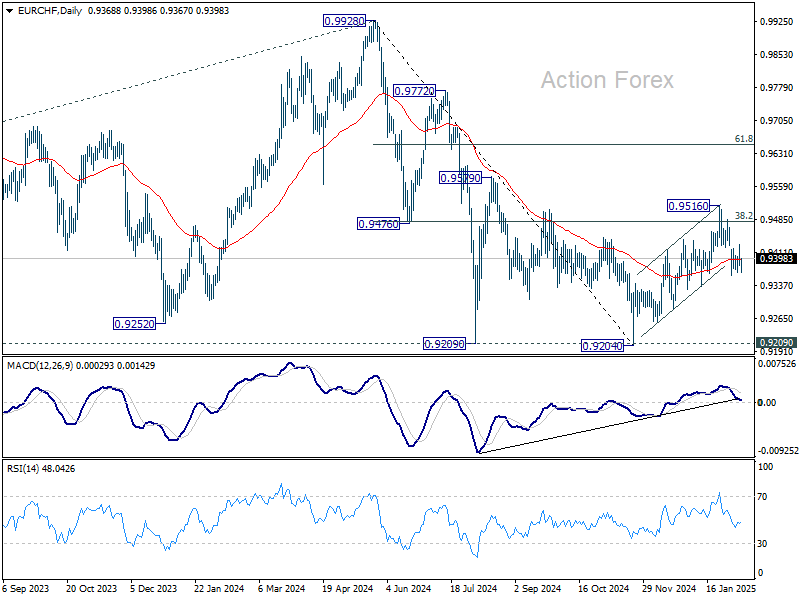

EUR/CHF Daily Outlook

Daily Pivots: (S1) 0.9377; (P) 0.9404; (R1) 0.9424; More....

EUR/CHF is staying in consolidations above 0.9359 and intraday bias remains neutral. While another recovery cannot be ruled out, risk will stay on the downside as long as 0.9516 resistance holds. Firm break of 0.9336 support will solidify the case that corrective rebound from 0.9204 has already completed at 0.9516. Deeper fall would then be seen to retest 0.9204 low.

In the bigger picture, the rejection by 55 W EMA (now at 0.9489) argues that rebound from 0.9204 has completed as a corrective move after failing to sustain above 38.2% retracement of 0.9928 to 0.9204 at 0.9481. Firm break of 0.9204/9 support zone will confirm larger down trend resumption.

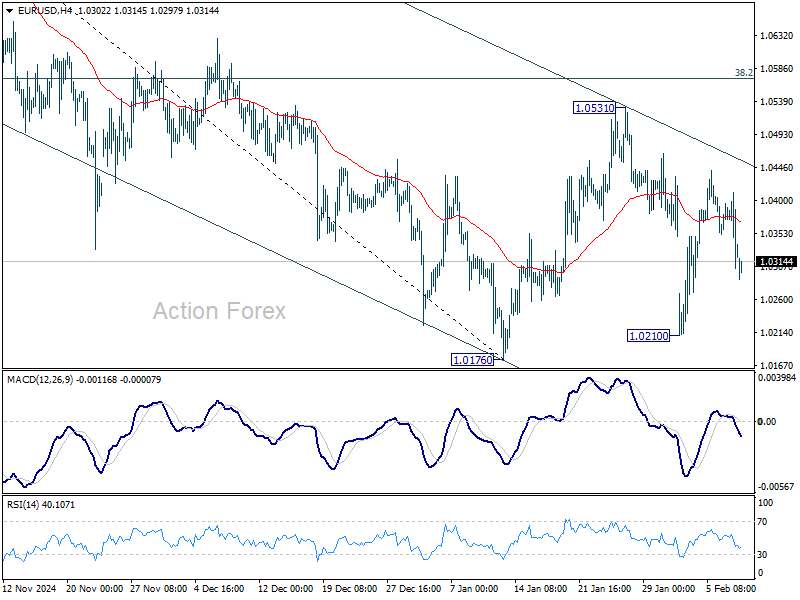

EUR/USD Daily Outlook

Daily Pivots: (S1) 1.0289; (P) 1.0345; (R1) 1.0383; More...

Intraday bias in EUR/USD remains neutral and consolidation from 1.0176 could extend. But outlook stays bearish as long as 38.2% retracement of 1.1213 to 1.0176 at 1.0572 holds. On the downside, break of 1.0176 will resume whole fall from 1.1213. However, decisive break of 1.0572 will raise the chance of reversal, and target 61.8% retracement at 1.0817.

In the bigger picture, immediate focus is on 61.8 retracement of 0.9534 (2022 low) to 1.1274 (2024 high) at 1.0199. Sustained break there will solidify the case of medium term bearish trend reversal, and pave the way back to 0.9534. However, reversal from 1.0199 will argue that price actions from 1.1274 are merely a corrective pattern, and has already completed.

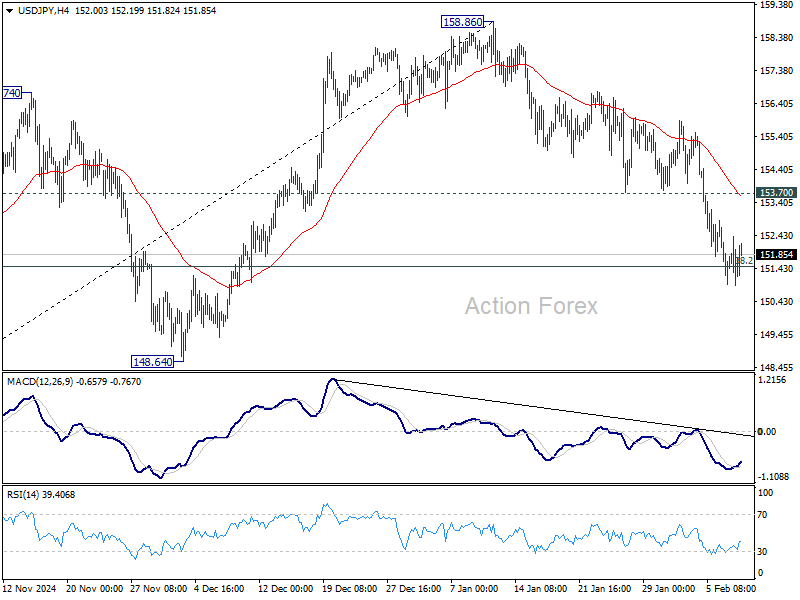

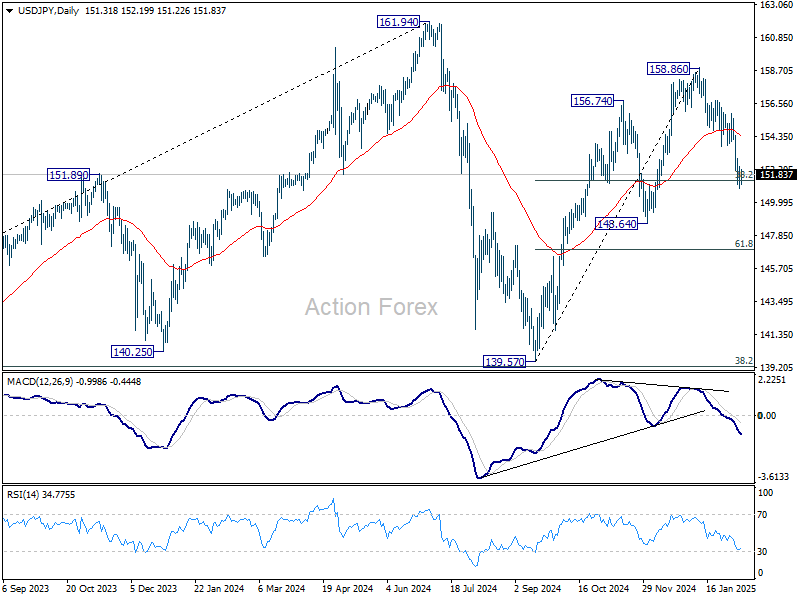

USD/JPY Daily Outlook

Daily Pivots: (S1) 150.73; (P) 151.57; (R1) 152.26; More...

Intraday bias in USD/JPY remains neutral with focus on 38.2% retracement of 139.57 to 158.86 at 151.49. Strong bounce from there, followed by break of 153.70 support turned resistance, will retain near term bullishness, and turn bas back to the upside for retesting 158.86. However, sustained trading below 151.49 will suggest that whole rise from 139.57 has completed, and bring deeper fall to 61.8% retracement at 146.32 next.

In the bigger picture, price actions from 161.94 are seen as a corrective pattern to rise from 102.58 (2021 low). In case of another fall, strong support should be seen from 38.2% retracement of 102.58 to 161.94 at 139.26 to bring rebound. However, sustained break of 139.26 would open up deeper medium term decline to 61.8% retracement at 125.25.

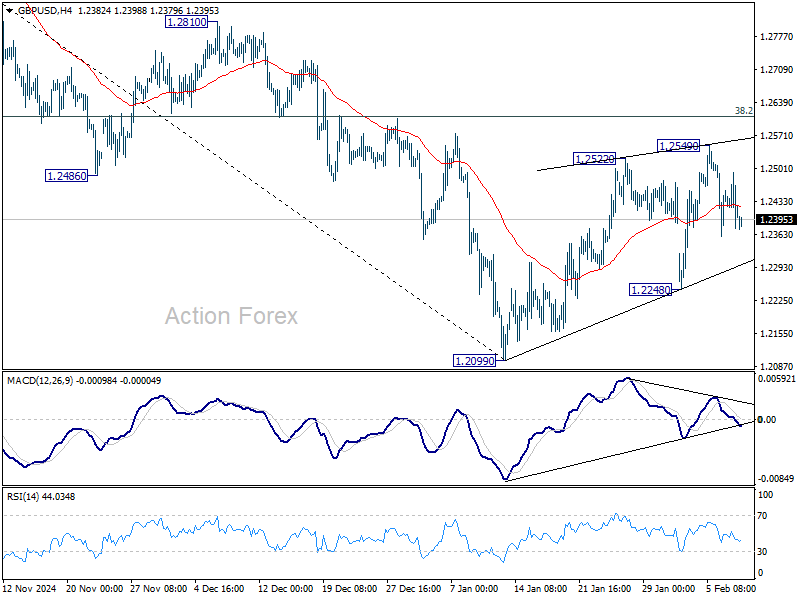

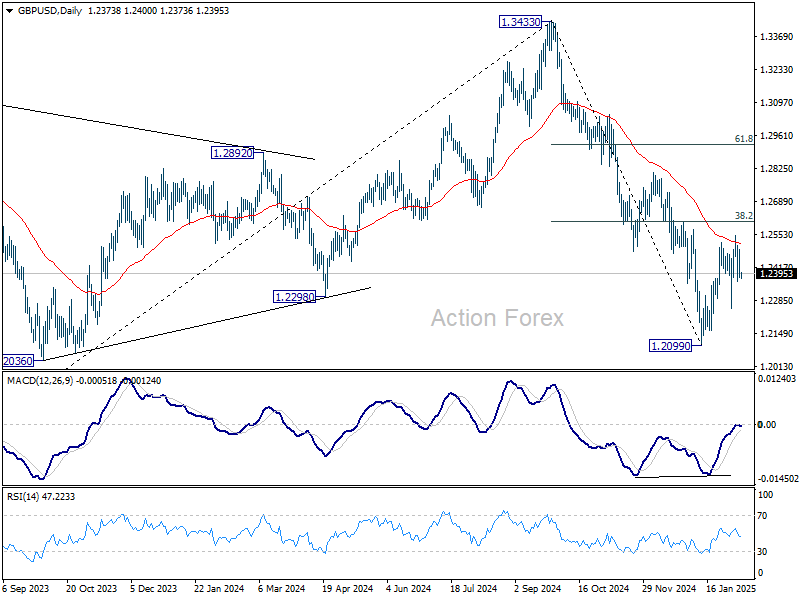

GBP/USD Daily Outlook

Daily Pivots: (S1) 1.2364; (P) 1.2417; (R1) 1.2458; More...

Intraday bias in GBP/USD remains neutral for the moment. Initial bias stays neutral this week first. While corrective rebound from 1.2099 might still extend, upside should be limited by 38.2% retracement of 1.3433 to 1.2099 at 1.2609. On the downside, break of 1.2248 support will bring retest of 1.2099 low. Firm break there will resume whole fall from 1.3433. However, decisive break of 1.2609 will raise the chance of near term reversal, and target 61.8% retracement at 1.2923.

In the bigger picture, rise from 1.0351 (2022 low) should have already completed at 1.3433 (2024 high), and the trend has reversed. Further fall is now expected as long as 1.2810 resistance holds. Deeper decline should be seen to 61.8% retracement of 1.0351 to 1.3433 at 1.1528, even as a corrective move. However, firm break of 1.2810 will dampen this bearish view and bring retest of 1.3433 high instead.

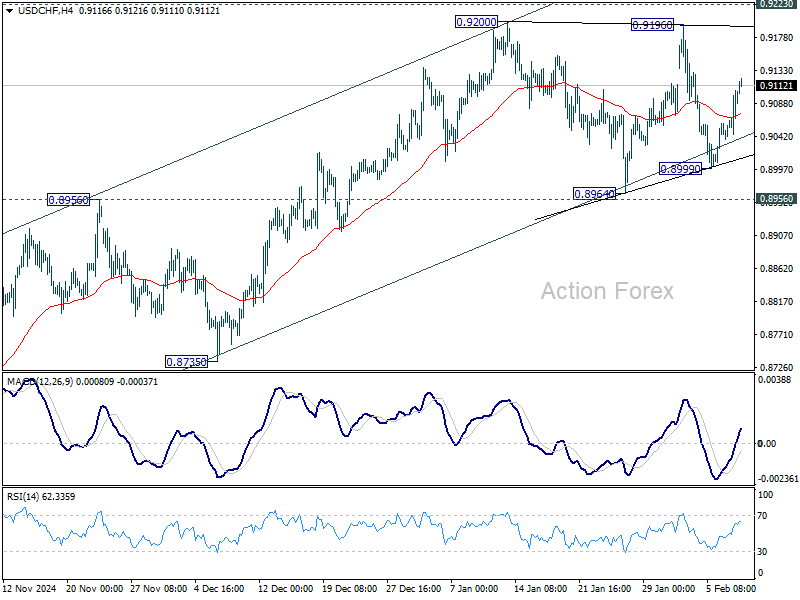

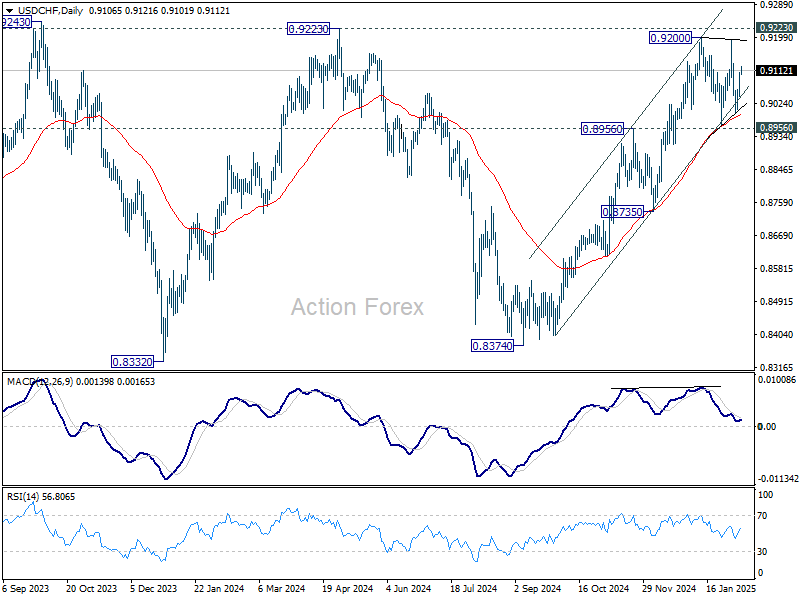

USD/CHF Daily Outlook

Daily Pivots: (S1) 0.9059; (P) 0.9083; (R1) 0.9122; More…

Intraday bias in USD/CHF remains neutral and consolidation from 0.9200 could extend further. But overall outlook stays bullish with 0.8956/64 support zone intact. On the upside, firm break of 0.9200/9223 will resume the whole rally from 0.8374 and carry larger bullish implication. However, sustained break of 0.8964 will be a sign of reversal and turn bias back to the downside.

In the bigger picture, decisive break of 0.9223 resistance will argue that whole down trend from 1.0342 (2017 high) has completed with three waves down to 0.8332 (2023 low). Outlook will be turned bullish for 1.0146 resistance next. Nevertheless, rejection by 0.9223 will retain medium term bearishness for another decline through 0.8332 at a later stage.

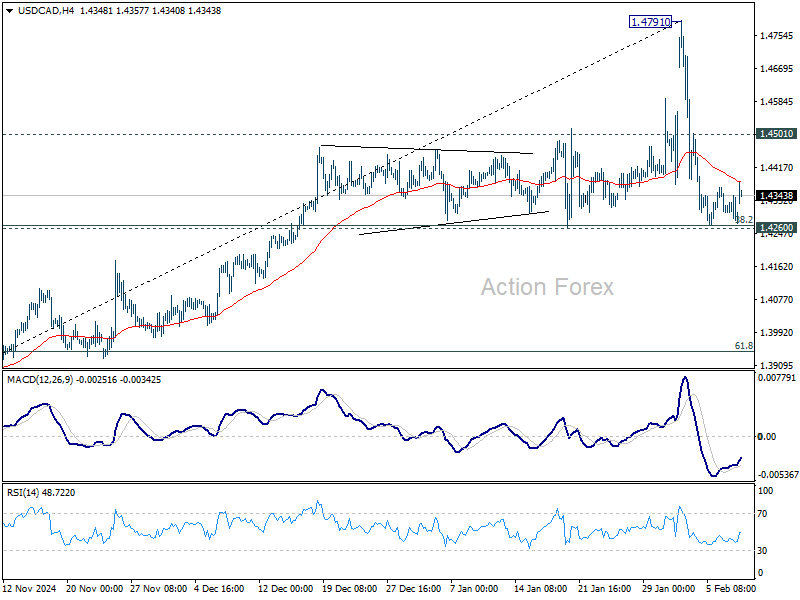

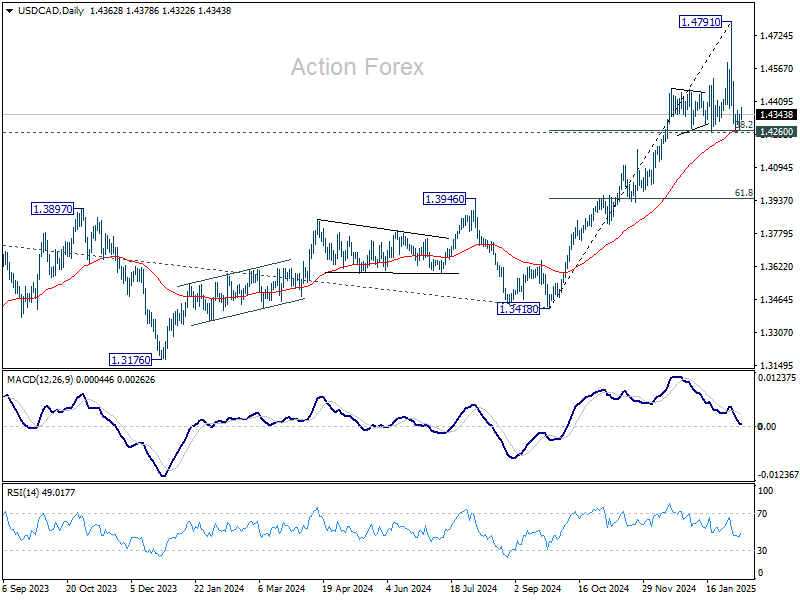

USD/CAD Daily Outlook

Daily Pivots: (S1) 1.4262; (P) 1.4304; (R1) 1.4333; More...

Intraday bias in USD/CAD remains neutral for the moment. Strong support is expected from 1.4260 cluster support (38.2% retracement of 1.3418 to 1.4791 at 1.4267), which is also close to 55 D EMA (now at 1.4267), to bring rebound. On the upside, above 1.4501 minor resistance will turn bias back to the upside for retesting 1.4791 short term top. However, firm break of 1.4260 will indicate that deeper correction is underway, and turn bias to the downside.

In the bigger picture, long term up trend is tentatively seen as resuming with breach of 1.4667/89 key resistance zone (2020/2015 highs). Next target is 100% projection of 1.2401 to 1.3976 from 1.3418 at 1.4993. This will remain the favored case as long as 1.3976 resistance turned holds (2022 high), even in case of deep pullback.

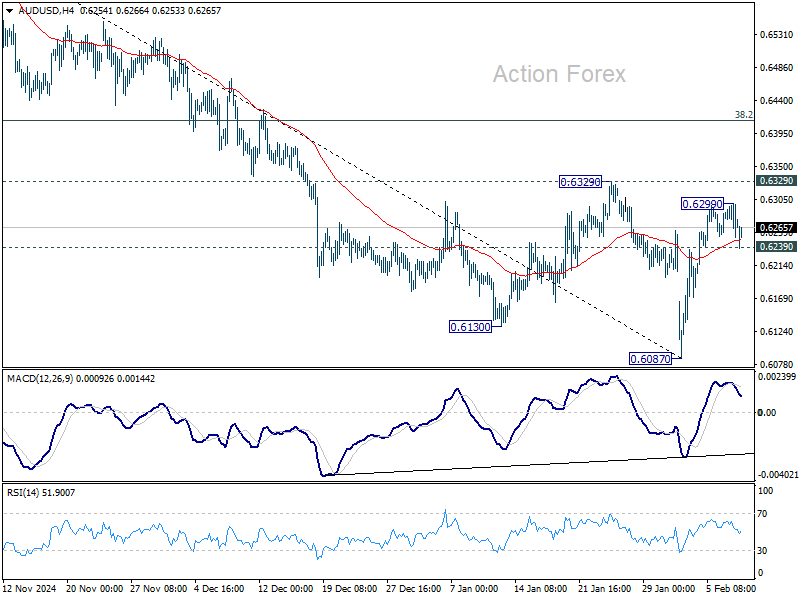

AUD/USD Daily Report

Daily Pivots: (S1) 0.6251; (P) 0.6275; (R1) 0.6296; More...

AUD/USD dips mildly today but stays above 0.6239 minor support. Intraday bas stays neutral first. With 0.6329 resistance intact, outlook will stay bearish. On the downside, break of 0.6239 minor support will turn bias back to the downside for retesting 0.6087 low. However, firm break of 0.6329 will bring stronger rebound to 38.2% retracement of 0.6941 to 0.6087 at 0.6413, even just as a corrective move.

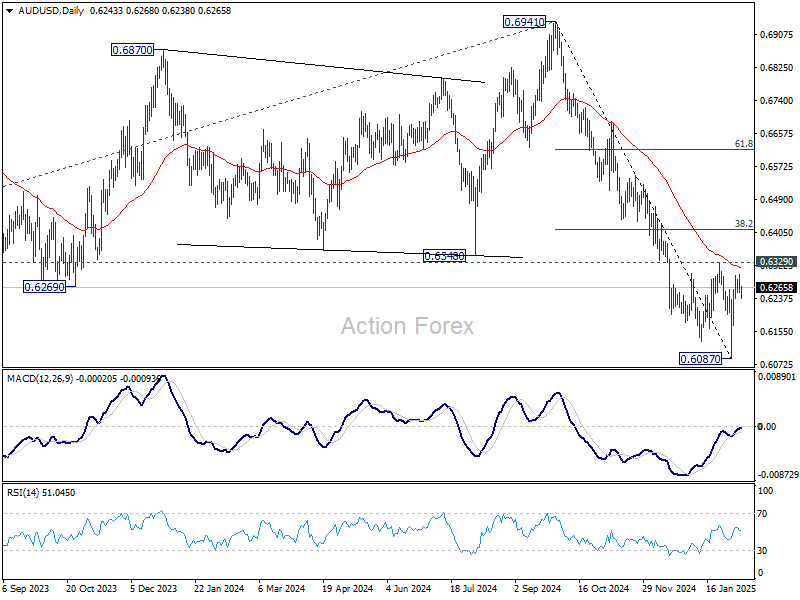

In the bigger picture, fall from 0.6941 (2024 high) is seen as part of the down trend from 0.8006 (2021 high). Next medium term target is 61.8% projection of 0.8006 to 0.6169 from 0.6941 at 0.5806. In any case, outlook will stay bearish as long as 55 W EMA (now at 0.6516) holds.

Tariff Wave Expands with Metals and Reciprocal Duties, Dollar Strengthens Slightly

Trade tensions remain at the forefront of market concerns as the US prepares to roll out another wave of tariffs. Over the weekend, President Donald Trump confirmed plans to impose a 25% tariff on all steel and aluminum imports, adding to the existing duties on these metals. The official announcement is expected today. Meanwhile, "reciprocal tariffs"—which would match the import duties imposed by other countries—are set to be unveiled between Tuesday and Wednesday, with immediate implementation.

The largest suppliers of steel and aluminum to the US are Canada, Brazil, and Mexico, followed by South Korea and Vietnam. Canada, in particular, dominates the aluminum export market to the US, contributing 79% of total imports in the first 11 months of 2024. The announcement raises questions about how these countries might respond, given that Canada and Mexico only recently secured a temporary reprieve from tariffs on other goods.

Interestingly, Hong Kong’s stock market has shown resilience, posting extended gains despite escalating trade tensions. Investors appear unfazed by the recent flurry of US tariff news, as well as China’s retaliatory levies on select American products. The factors supporting Hong Kong’s optimism remain unclear, and more time would be required to assess whether regional equities can maintain this momentum if trade frictions intensify further.

Technically, HSI's break of 21070.05 resistance last week suggests that correction from 23241.74 has completed at 18671.59 already, despite being deeper than expected. The medium term up trend from 14794.16 should remain intact, with notable support from 55 W EMA too. Retest of 23241.74 resistance should be seen next and firm break there will target 25k handle, which is close to 100% projection of 16964.28 to 23241.74 from 18671.49.

Looking ahead, markets will keep a close watch on Fed Chair Jerome Powell’s upcoming Congressional testimonies, particularly any remarks concerning inflation and labor market conditions. Major data releases this week include US CPI, UK GDP, Swiss CPI, and key confidence reports from Australia and New Zealand.

Looking ahead, markets will keep a close watch on Fed Chair Jerome Powell’s upcoming Congressional testimonies, particularly any remarks concerning inflation and labor market conditions. Major data releases this week include US CPI, UK GDP, Swiss CPI, and key confidence reports from Australia and New Zealand.

In Asia, at the time of writing, Nikkei is down -0.10%. Hong Kong HSI is up 1.15%. China Shanghai SSE is up 0.23%. Singapore Strait Times is up 0.63%. Japan 10-year JGB yield is up 0.0193 at 1.322, hitting a fresh high since 2011.

China’s CPI picks up to 0.5%, but factory prices remain stuck in deflation

China's consumer inflation accelerated at the start of 2025, with CPI rising from 0.1% yoy to 0.5% yoy in January, slightly exceeding market expectations of 0.4%. This marked the fastest annual increase in five months. On a monthly basis, CPI surged 0.7% mom, the strongest rise in over three years.

Core inflation, which strips out food and fuel prices, edged up from 0.4% yoy to 0.6% yoy, reflecting a modest pickup in underlying demand. Food prices climbed by 0.4% yoy, while non-food categories also posted a 0.5% yoy increase.

However, despite these gains, consumer inflation remains well below the government’s target, with full-year 2024 CPI growth coming in at just 0.2%, the lowest since 2009, and reinforcing the persistent weakness in domestic consumption.

Meanwhile, producer prices remained firmly in deflationary territory. PPI held steady at -2.3% yoy in January, missing expectations of a slight improvement to -2.2% yoy. This marks the 28th consecutive month of factory-gate deflation, highlighting ongoing struggles within the manufacturing sector and pricing pressures stemming from weak external demand and excess capacity.

Powell’s testimony, US inflation data, and UK GDP in focus this week

Fed Chair Jerome Powell’s upcoming Congressional testimony will be a key event this week as markets seek further clarity on Fed’s path. In particular, the main question is whether Fed’s hold at the last meeting is the start of a longer pause in the easing cycle.

Following January’s FOMC decision to hold rates steady, Powell stated explicitly that Fed is in "no hurry" to cut interest rates. Several Fed officials have since emphasized that declining inflation alone may not be sufficient for additional rate reductions, with the labor market's performance playing a crucial role. Lawmakers are expected to press Powell for further details on how Fed will balance these factors in shaping monetary policy.

Meanwhile, Friday’s Monetary Policy Report offered minimal commentary on the impact of US tariff policies. It merely noted that "some market participants" cited tariff-related uncertainties as a factor driving the dollar higher in recent months. Given the evolving nature of Trump's trade strategy and the lack of clear direction, Powell is unlikely to provide definitive answers on how tariffs will influence Fed policy. Nonetheless, market participants will closely follow any indication that trade-related uncertainties might alter the Fed’s rate outlook.

US CPI and retail sales data will also be closely watched. Headline inflation is expected to remain at 2.9% in January, with core CPI easing slightly from 3.2% to 3.1%. Risks remain that inflation could remain sticky as businesses begin adjusting for potential tariff impacts. If inflation prints in line with expectations or surprises to the upside, it would reinforce Fed’s cautious approach and likely prolong the current pause in rate cuts.

Elsewhere, UK GDP report will be another highlight. The economy is expected to contract by -0.1% in Q4, raising concerns about a potential recession. After last week’s dovish 25bps rate cut by BoE, speculation has increased that another cut could come as early as March. While this is not yet the consensus view, any downside surprise in GDP data could fuel expectations of a back-to-back rate reduction, particularly as known hawk Catherine Mann has already shifted to a more dovish stance.

Here are some highlights for the week:

- Monday: Japan bank lending, current account, Eco Watcher sentiment; Eurozone Sentix Investor confidence.

- Tuesday: Australia Westpac consumer sentiment, NAB business confidence; Canada building permits.

- Wednesday: Japan machine tool orders; US CPI; BoC summary of deliberations.

- Thursday: Japan PPI; New Zealand inflation expectations; Germany CPI final; UK GDP, trade balance; Swiss CPI; Eurozone industrial production; US PPI, jobless claims.

- Friday: New Zealand BNZ manufacturing; Swiss PPI; Eurozone GDP revision; Canada manufacturing sales, wholesales sales; US retail sales, industrial production.

AUD/USD Daily Report

Daily Pivots: (S1) 0.6251; (P) 0.6275; (R1) 0.6296; More...

AUD/USD dips mildly today but stays above 0.6239 minor support. Intraday bas stays neutral first. With 0.6329 resistance intact, outlook will stay bearish. On the downside, break of 0.6239 minor support will turn bias back to the downside for retesting 0.6087 low. However, firm break of 0.6329 will bring stronger rebound to 38.2% retracement of 0.6941 to 0.6087 at 0.6413, even just as a corrective move.

In the bigger picture, fall from 0.6941 (2024 high) is seen as part of the down trend from 0.8006 (2021 high). Next medium term target is 61.8% projection of 0.8006 to 0.6169 from 0.6941 at 0.5806. In any case, outlook will stay bearish as long as 55 W EMA (now at 0.6516) holds.

Euro’s Gains Restricted: EUR/USD Faces Strong Resistance

Key Highlights

- EUR/USD failed to continue higher above 1.0450 and trimmed gains.

- A connecting bearish trend line is forming with resistance at 1.0385 on the 4-hour chart.

- GBP/USD is consolidating near the 1.2380 zone.

- USD/JPY dipped toward the 151.20 level and started a consolidation phase.

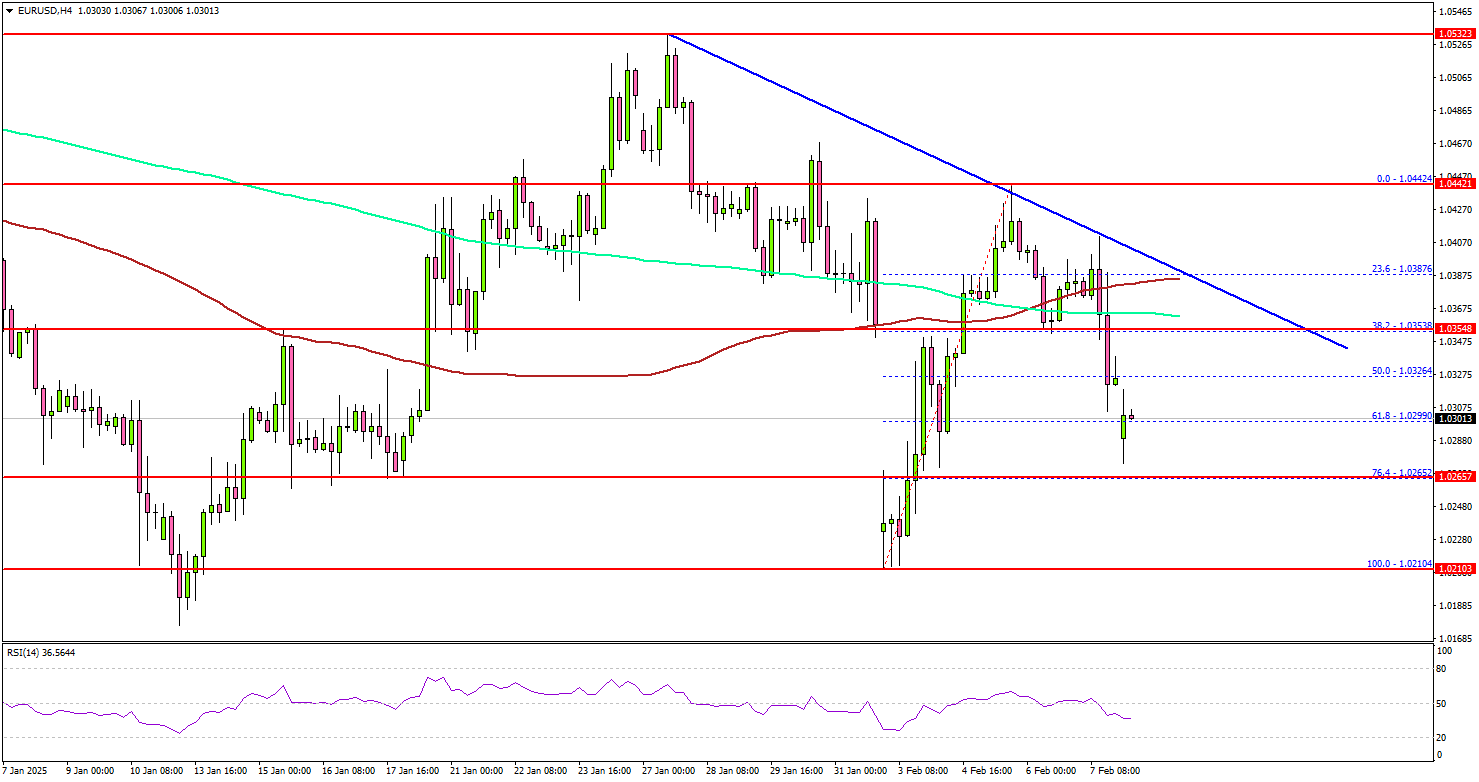

EUR/USD Technical Analysis

The Euro started a fresh increase above 1.0350 against the US Dollar. However, EUR/USD struggled near 1.0450 and recently trimmed gains.

Looking at the 4-hour chart, the pair settled below the 1.0380 level, the 100 simple moving average (red, 4-hour), and the 200 simple moving average (green, 4-hour). The bears pushed the pair below the 50% Fib retracement level of the upward move from the 1.0210 swing low to the 1.0442 high.

On the downside, immediate support sits near the 1.0365 level. It is near the 76.4% Fib retracement level of the upward move from the 1.0210 swing low to the 1.0442 high.

The next key support sits near the 1.0250 level. Any more losses could send the pair toward the 1.0210 level. On the upside, the pair seems to be facing hurdles near the 1.0330 level.

The next major resistance is near the 1.0360 level. The main resistance is now forming near the 1.0400 zone and the 100 simple moving average (red, 4-hour). A close above the 1.0400 level could set the tone for another increase. In the stated case, the pair could even clear the 1.0465 resistance.

Looking at GBP/USD, the pair was able to recover above the 1.2350 resistance, but the bears are still active below 1.2450.

Upcoming Economic Events:

- ECB's President Lagarde speech.