Sample Category Title

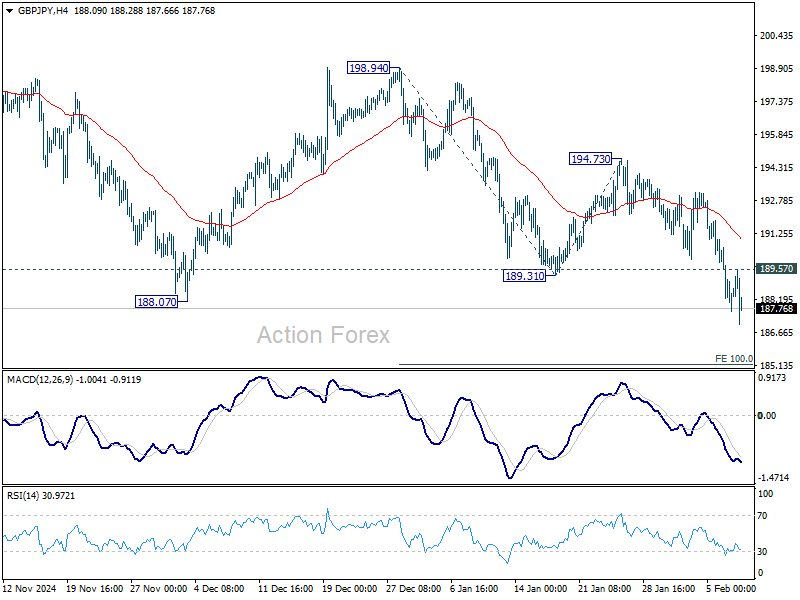

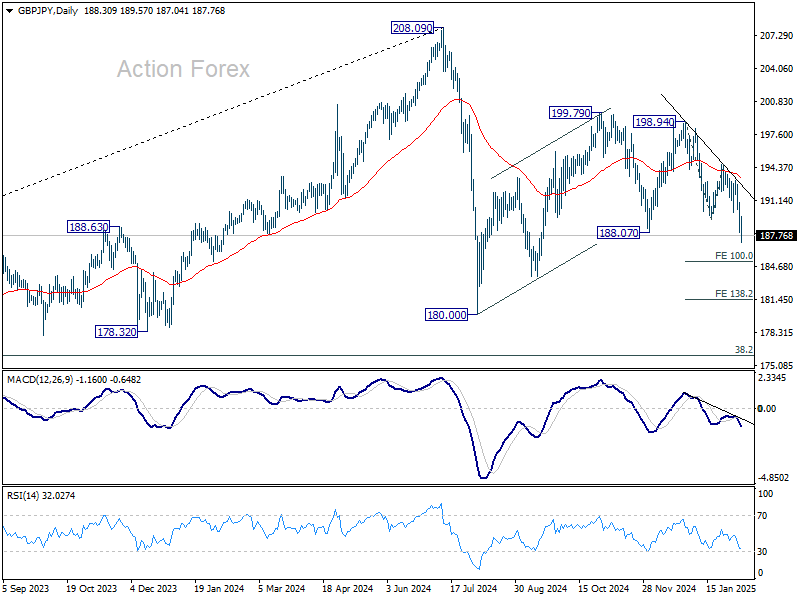

GBP/JPY Weekly Outlook

GBP/JPY's fall accelerated lower last week and there is no sign of bottoming yet. Initial bias stays on the downside this week for 100% projection of 198.94 to 189.31 from 194.73 at 185.10. Decisive break there will target 138.2% projection at 181.42. On the upside, above 189.57 minor resistance will turn intraday bias neutral first. But risk will stay on the downside as long as 194.73 resistance holds, in case of recovery.

In the bigger picture, price actions from 208.09 are seen as a correction to rally from 123.94 (2020 low). Strong support should be seen from 38.2% retracement of 123.94 to 208.09 at 175.94 to contain downside. However, sustained break of 152.11 will bring deeper fall to 100% projection of 208.09 to 180.00 from 199.79 at 171.70, even still as a correction.

In the longer term picture, while a medium term top was formed at 208.09 (2024 high), it's still early to conclude that the up trend from 122.75 (2016 low) has completed. But GBP/JPY is at least in a medium term corrective phase, with risk of correction to 55 M EMA (now at 173.92).

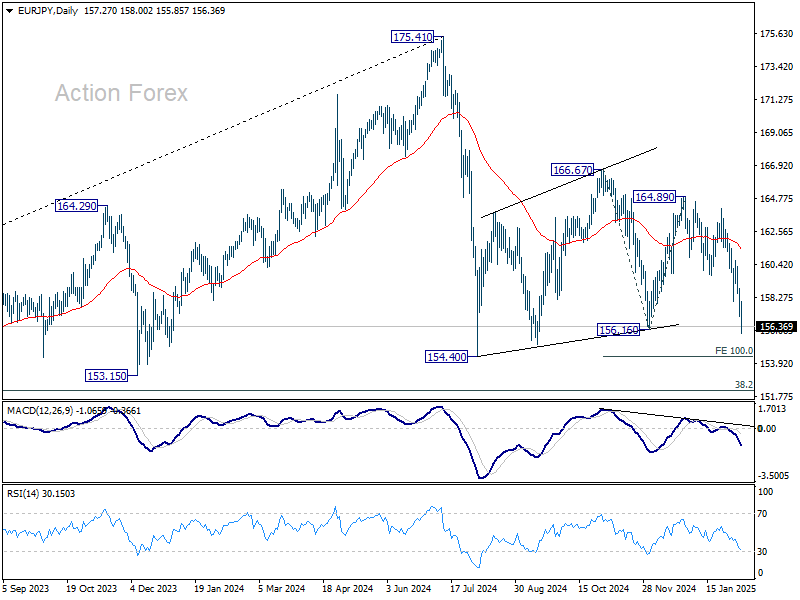

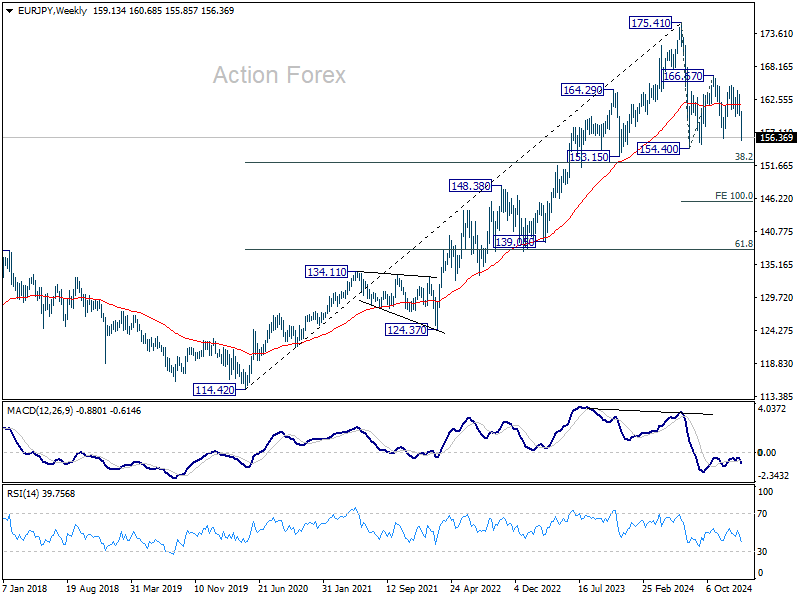

EUR/JPY Weekly Outlook

EUR/JPY's decline accelerated last week and there is no sign of bottoming yet. Initial bias stays on the downside this week for 100% projection of 166.7 to 156.16 from 164.89 at 154.38. Firm break of 154.40 will resume whole fall from 175.41 and target 152.11 key fibonacci support. On the upside, above 158.00 minor resistance will turn intraday bias neutral first. But risk will remain on the downside as long as 159.74 support turned resistance holds, in case of recovery.

In the bigger picture, price actions from 175.41 are seen as correction to rally from 114.42 (2020 low). Strong support should be seen from 38.2% retracement of 114.42 to 175.41 at 152.11 to contain downside. However, sustained break of 152.11 will bring deeper fall to 100% projection of 175.41 to 154.40 from 166.57 at 145.56, even still as a correction.

In the long term picture, while 175.41 is at least a medium term top, it's still early to conclude that up trend from 94.11 (2012 low) has completed. A medium term corrective phase is in progress with risk of deeper fall back to 55 M EMA (now at 148.27).

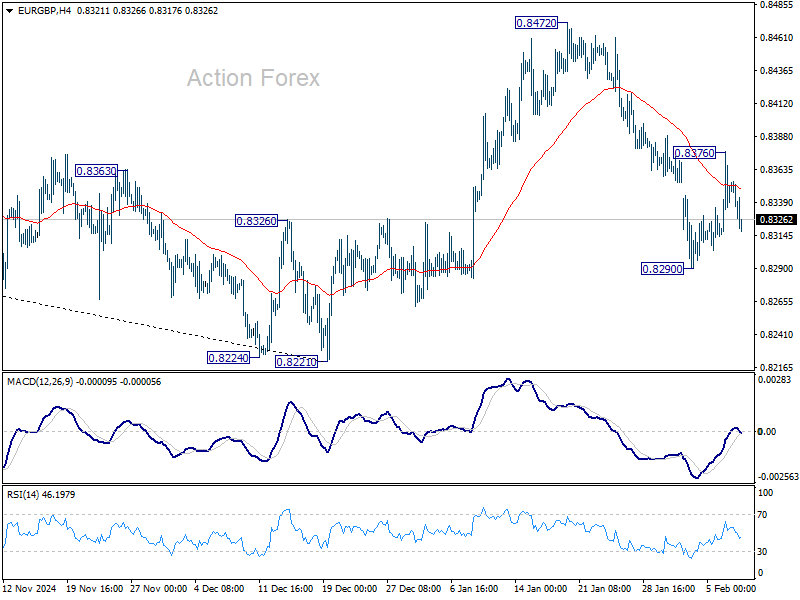

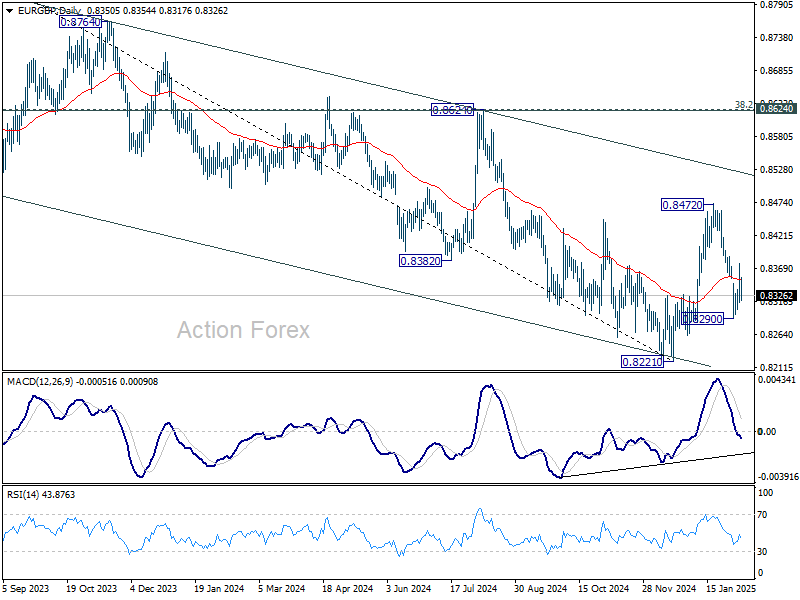

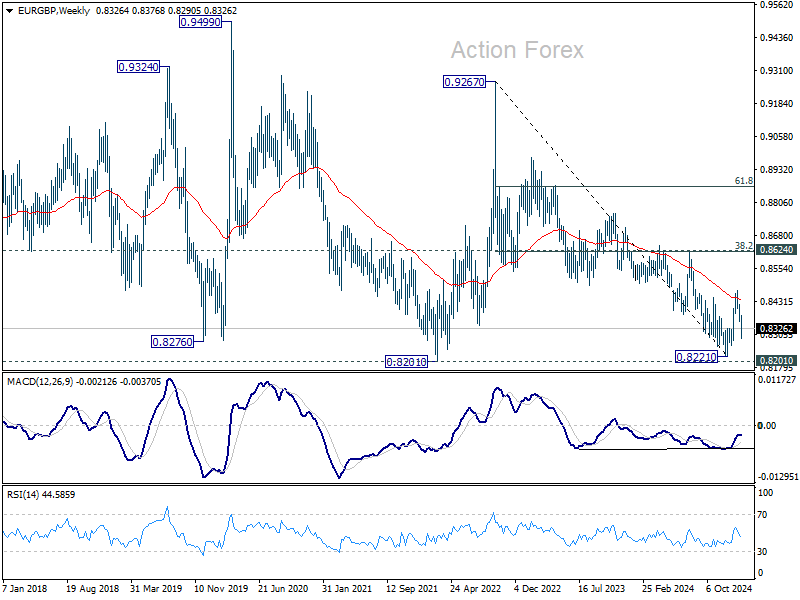

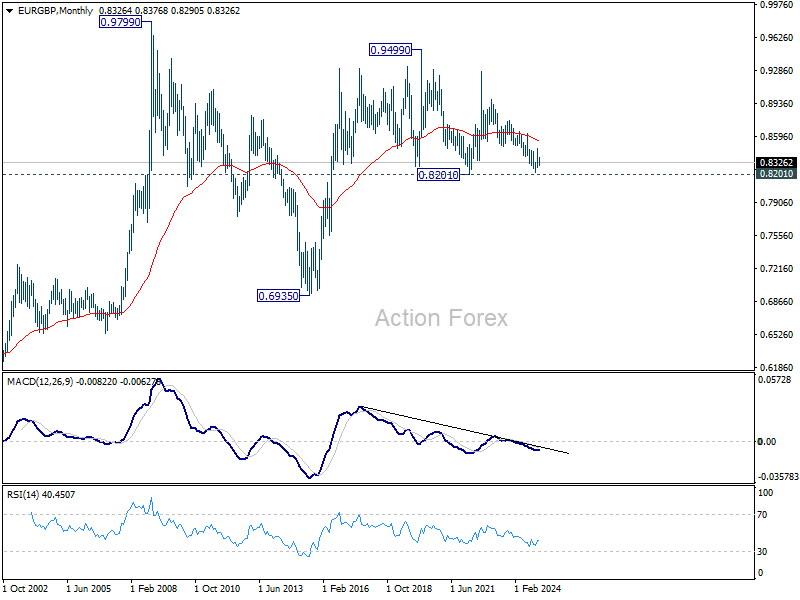

EUR/GBP Weekly Outlook

EUR/GBP's near term outlook is mixed up by the extended fall to 0.8290 and the short-lived recovery. Initial bias is turned neutral this week first. On the upside, above 0.8376 minor resistance will bring stronger rally towards 08472. However, on the downside, break of 0.8290 will resume the fall from 08472 to retest 0.8221 low.

In the bigger picture, rebound from 0.8221 medium term bottom could extend higher through 55 W EMA (now at 0.8439). However, medium term outlook will be neutral at best as long as 0.8624 cluster resistance zone (38.2% retracement of 0.9267 to 0.8221 at 0.8621) holds. Another decline through 0.8221 would remain mildly in favor.

In the long term picture, price action from 0.9499 (2020 high) is seen as part of the long term range pattern from 0.9799 (2008 high). Range trading should continue between 0.8201 and 0.9499, until there is clear signal of imminent breakout.

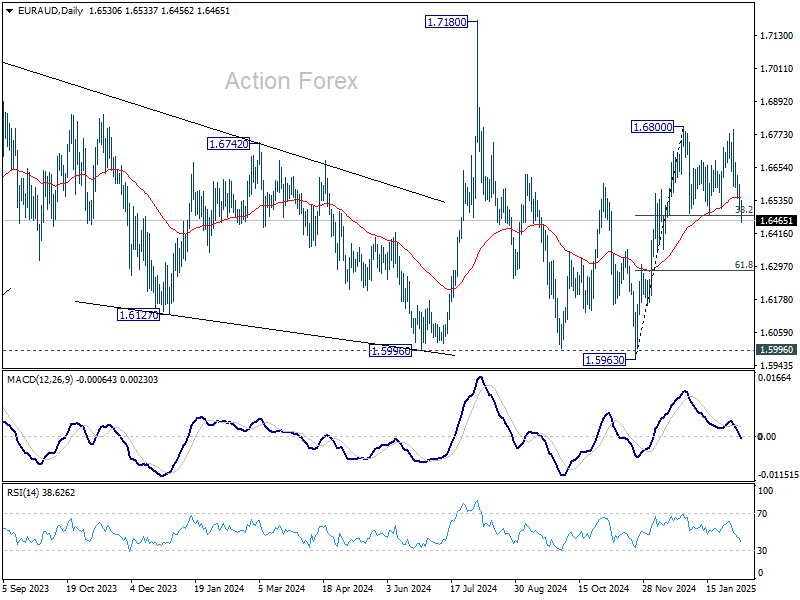

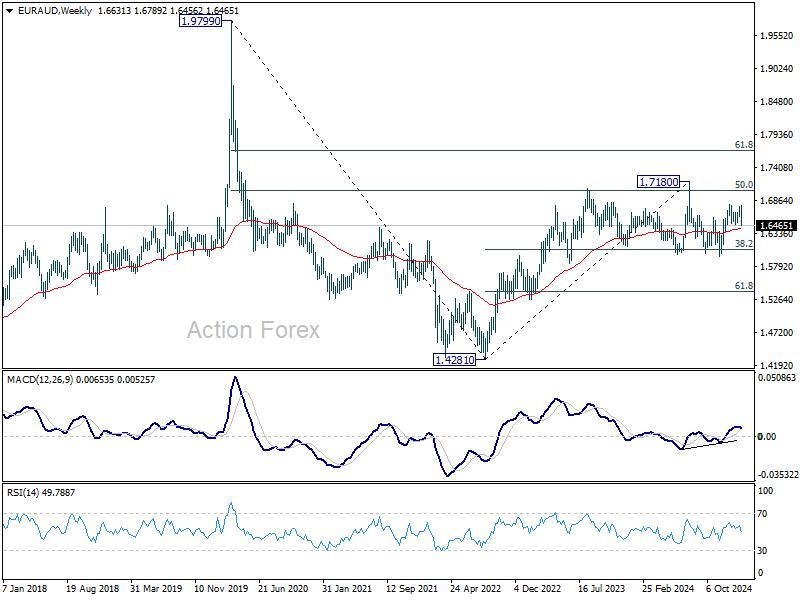

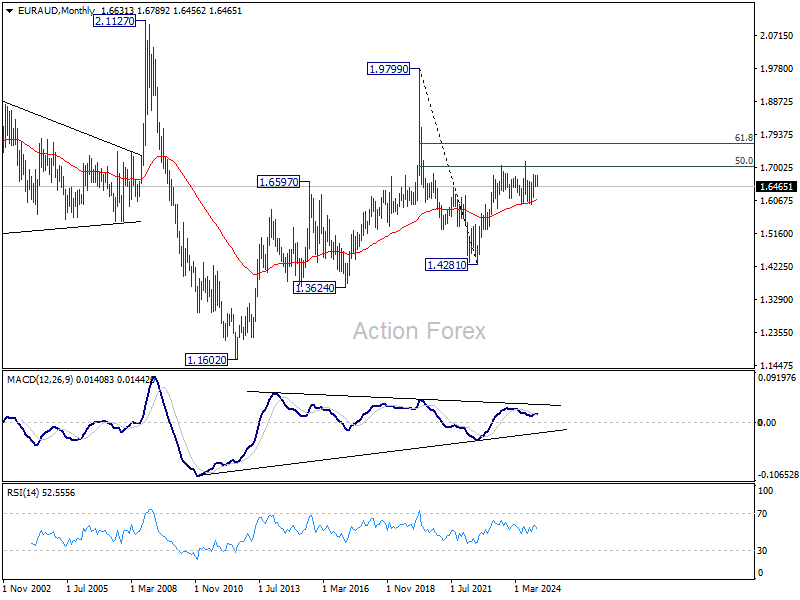

EUR/AUD Weekly Outlook

EUR/AUD's late break of 1.6481 cluster support (38.2% retracement of 1.5963 to 1.6800 at 1.6480) suggests that a double top reversal pattern (1.6800, 1.6789) might be completed. Initial bias is back on the downside this week for 61.8% retracement at 1.6283. On the upside, break of 1.6593 minor resistance will turn bias back to the upside for retesting 1.6800 instead.

In the bigger picture, with 1.5996 key support (2024 low) intact, larger up trend from 1.4281 (2022 low) is still in favor to resume through 1.7180 at a later stage. Nevertheless, sustained break of 1.5996 will indicate that such up trend has completed and deeper decline would be seen.

In the longer term picture, rise from 1.4281 is seen as the second leg of the pattern from 1.9799 (2020 high), which is part of the pattern from 2.1127 (2008 high). As long as 55 M EMA (now at 1.6090) holds, this second leg could still extend higher. However, sustained trading below 55 M EMA will open up the bearish case for extending the decline through 1.4281 low.

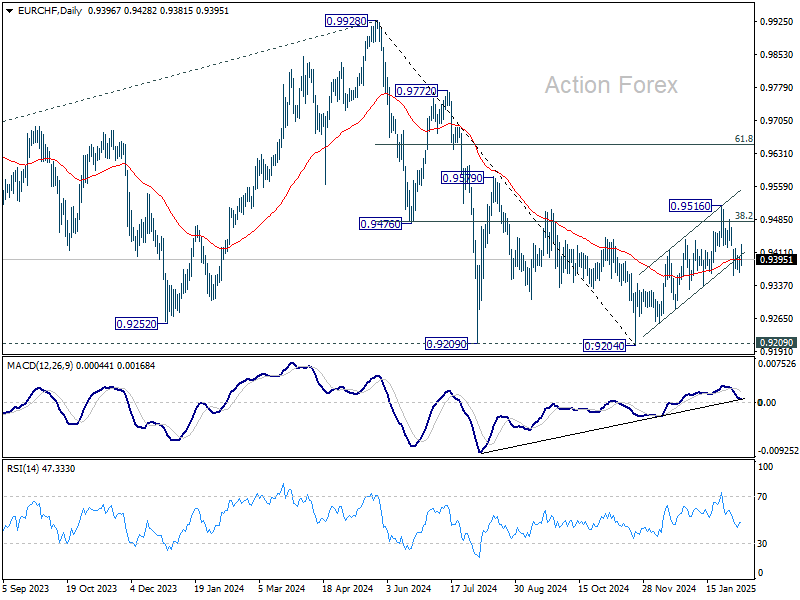

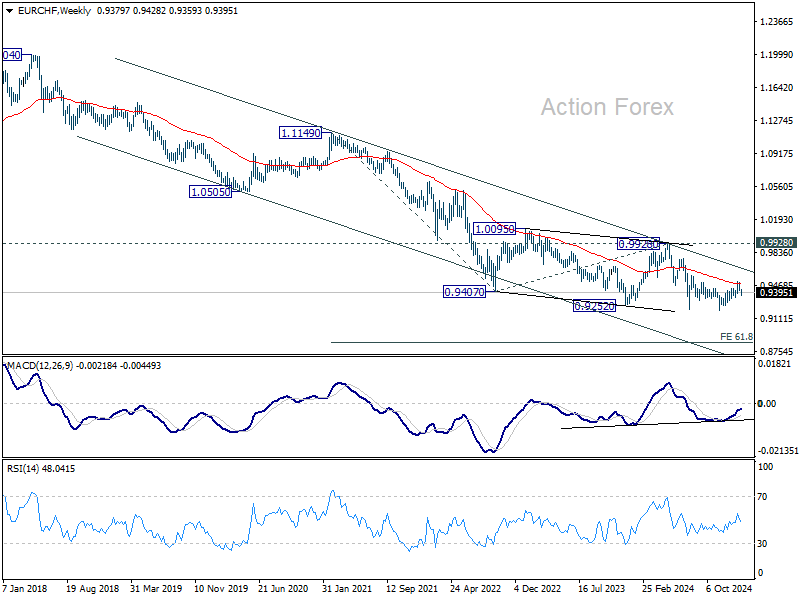

EUR/CHF Weekly Outlook

EUR/CHF's stabilized after steep decline to 0.9359 last week and turned into sideway trading. Initial bias stays neutral this week first. While another recovery cannot be ruled out, risk will stay on the downside as long as 0.9516 resistance holds. Firm break of 0.9336 support will solidify the case that corrective rebound from 0.9204 has already completed at 0.9516. Deeper fall would then be seen to retest 0.9204 low.

In the bigger picture, the rejection by 55 W EMA (now at 0.9489) argues that rebound from 0.9204 has completed as a corrective move after failing to sustain above 38.2% retracement of 0.9928 to 0.9204 at 0.9481. Firm break of 0.9204/9 support zone will confirm larger down trend resumption.

In the long term picture, as long as 0.9928 resistance holds, the multi-decade down trend remains intact, with fall from 1.2004 (2018 high) as another falling leg. Decisive break of 0.9252 (2023 low) will confirm long term down trend resumption to 61.8% projection of 1.1149 to 0.9407 from 0.9928 at 0.8851.

Summary 2/10 – 2/14

Monday, Feb 10, 2025

| GMT | Ccy | Events | Consensus | Previous |

|---|---|---|---|---|

| 23:50 | JPY | Bank Lending Y/Y Jan | 3.10% | 3.10% |

| 23:50 | JPY | Current Account (JPY) Dec | 2.73T | 3.03T |

| 05:00 | JPY | Eco Watchers Survey: Current Jan | 49.7 | 49.9 |

| 09:30 | EUR | Eurozone Sentix Investor Confidence Feb | -16.4 | -17.7 |

| 23:30 | AUD | Westpac Consumer Confidence Feb | -0.70% |

| GMT | Ccy | Events | |

|---|---|---|---|

| 23:50 | JPY | Bank Lending Y/Y Jan | |

| Forecast: 3.10% | Previous: 3.10% | ||

| 23:50 | JPY | Current Account (JPY) Dec | |

| Forecast: 2.73T | Previous: 3.03T | ||

| 05:00 | JPY | Eco Watchers Survey: Current Jan | |

| Forecast: 49.7 | Previous: 49.9 | ||

| 09:30 | EUR | Eurozone Sentix Investor Confidence Feb | |

| Forecast: -16.4 | Previous: -17.7 | ||

| 23:30 | AUD | Westpac Consumer Confidence Feb | |

| Forecast: | Previous: -0.70% | ||

Tuesday, Feb 11, 2025

| GMT | Ccy | Events | Consensus | Previous |

|---|---|---|---|---|

| 00:30 | AUD | NAB Business Confidence Jan | -2 | |

| 00:30 | AUD | NAB Business Conditions Jan | 6 | |

| 11:00 | USD | NFIB Business Optimism Jan | 104.6 | 105.1 |

| 13:30 | CAD | Building Permits M/M Dec | 2.30% | -5.90% |

| 23:50 | JPY | Money Supply M2+CD Y/Y Jan | 1.30% | 1.30% |

| GMT | Ccy | Events | |

|---|---|---|---|

| 00:30 | AUD | NAB Business Confidence Jan | |

| Forecast: | Previous: -2 | ||

| 00:30 | AUD | NAB Business Conditions Jan | |

| Forecast: | Previous: 6 | ||

| 11:00 | USD | NFIB Business Optimism Jan | |

| Forecast: 104.6 | Previous: 105.1 | ||

| 13:30 | CAD | Building Permits M/M Dec | |

| Forecast: 2.30% | Previous: -5.90% | ||

| 23:50 | JPY | Money Supply M2+CD Y/Y Jan | |

| Forecast: 1.30% | Previous: 1.30% | ||

Wednesday, Feb 12, 2025

| GMT | Ccy | Events | Consensus | Previous |

|---|---|---|---|---|

| 06:00 | JPY | Machine Tool Orders Y/Y Jan P | 11.20% | |

| 13:30 | USD | CPI M/M Jan | 0.30% | 0.40% |

| 13:30 | USD | CPI Y/Y Jan | 2.90% | 2.90% |

| 13:30 | USD | CPI Core M/M Jan | 0.30% | 0.20% |

| 13:30 | USD | CPI Core Y/Y Jan | 3.20% | |

| 15:30 | USD | Crude Oil Inventories | 8.7M | |

| 23:50 | JPY | PPI Y/Y Jan | 4.00% | 3.80% |

| GMT | Ccy | Events | |

|---|---|---|---|

| 06:00 | JPY | Machine Tool Orders Y/Y Jan P | |

| Forecast: | Previous: 11.20% | ||

| 13:30 | USD | CPI M/M Jan | |

| Forecast: 0.30% | Previous: 0.40% | ||

| 13:30 | USD | CPI Y/Y Jan | |

| Forecast: 2.90% | Previous: 2.90% | ||

| 13:30 | USD | CPI Core M/M Jan | |

| Forecast: 0.30% | Previous: 0.20% | ||

| 13:30 | USD | CPI Core Y/Y Jan | |

| Forecast: | Previous: 3.20% | ||

| 15:30 | USD | Crude Oil Inventories | |

| Forecast: | Previous: 8.7M | ||

| 23:50 | JPY | PPI Y/Y Jan | |

| Forecast: 4.00% | Previous: 3.80% | ||

Thursday, Feb 13, 2025

| GMT | Ccy | Events | Consensus | Previous |

|---|---|---|---|---|

| 00:00 | AUD | Consumer Inflation Expectations Feb | 4% | |

| 00:01 | GBP | RICS Housing Price Balance Jan | 27% | 28% |

| 02:00 | NZD | RBNZ Inflation Expectations Q1 | 2.12% | |

| 07:00 | EUR | Germany CPI M/M Jan F | -0.20% | -0.20% |

| 07:00 | EUR | Germany CPI Y/Y Jan F | 2.30% | 2.30% |

| 07:00 | GBP | GDP Q/Q Q4 P | -0.10% | 0.00% |

| 07:00 | GBP | GDP M/M Dec | 0.10% | 0.10% |

| 07:00 | GBP | Industrial Production M/M Dec | 0.30% | -0.40% |

| 07:00 | GBP | Industrial Production Y/Y Dec | -1.80% | |

| 07:00 | GBP | Manufacturing Production M/M Dec | 0.10% | -0.30% |

| 07:00 | GBP | Manufacturing Production Y/Y Dec | -1.20% | |

| 07:00 | GBP | Goods Trade Balance (GBP) Dec | -18.3B | -19.3B |

| 07:30 | CHF | CPI M/M Jan | -0.10% | -0.10% |

| 07:30 | CHF | CPI Y/Y Jan | 0.60% | |

| 09:00 | EUR | ECB Economic Bulletin | ||

| 10:00 | EUR | Eurozone Industrial Production M/M Dec | -0.60% | 0.20% |

| 13:30 | USD | PPI M/M Jan | 0.20% | 0.20% |

| 13:30 | USD | PPI Y/Y Jan | 3.30% | |

| 13:30 | USD | PPI Core M/M Jan | 0.30% | 0.00% |

| 13:30 | USD | PPI Core Y/Y Jan | 3.50% | |

| 13:30 | USD | Initial Jobless Claims (Feb 7) | 221K | 219K |

| 15:30 | USD | Natural Gas Storage | -174B | |

| 21:30 | NZD | Business NZ PMI Jan | 45.9 |

| GMT | Ccy | Events | |

|---|---|---|---|

| 00:00 | AUD | Consumer Inflation Expectations Feb | |

| Forecast: | Previous: 4% | ||

| 00:01 | GBP | RICS Housing Price Balance Jan | |

| Forecast: 27% | Previous: 28% | ||

| 02:00 | NZD | RBNZ Inflation Expectations Q1 | |

| Forecast: | Previous: 2.12% | ||

| 07:00 | EUR | Germany CPI M/M Jan F | |

| Forecast: -0.20% | Previous: -0.20% | ||

| 07:00 | EUR | Germany CPI Y/Y Jan F | |

| Forecast: 2.30% | Previous: 2.30% | ||

| 07:00 | GBP | GDP Q/Q Q4 P | |

| Forecast: -0.10% | Previous: 0.00% | ||

| 07:00 | GBP | GDP M/M Dec | |

| Forecast: 0.10% | Previous: 0.10% | ||

| 07:00 | GBP | Industrial Production M/M Dec | |

| Forecast: 0.30% | Previous: -0.40% | ||

| 07:00 | GBP | Industrial Production Y/Y Dec | |

| Forecast: | Previous: -1.80% | ||

| 07:00 | GBP | Manufacturing Production M/M Dec | |

| Forecast: 0.10% | Previous: -0.30% | ||

| 07:00 | GBP | Manufacturing Production Y/Y Dec | |

| Forecast: | Previous: -1.20% | ||

| 07:00 | GBP | Goods Trade Balance (GBP) Dec | |

| Forecast: -18.3B | Previous: -19.3B | ||

| 07:30 | CHF | CPI M/M Jan | |

| Forecast: -0.10% | Previous: -0.10% | ||

| 07:30 | CHF | CPI Y/Y Jan | |

| Forecast: | Previous: 0.60% | ||

| 09:00 | EUR | ECB Economic Bulletin | |

| Forecast: | Previous: | ||

| 10:00 | EUR | Eurozone Industrial Production M/M Dec | |

| Forecast: -0.60% | Previous: 0.20% | ||

| 13:30 | USD | PPI M/M Jan | |

| Forecast: 0.20% | Previous: 0.20% | ||

| 13:30 | USD | PPI Y/Y Jan | |

| Forecast: | Previous: 3.30% | ||

| 13:30 | USD | PPI Core M/M Jan | |

| Forecast: 0.30% | Previous: 0.00% | ||

| 13:30 | USD | PPI Core Y/Y Jan | |

| Forecast: | Previous: 3.50% | ||

| 13:30 | USD | Initial Jobless Claims (Feb 7) | |

| Forecast: 221K | Previous: 219K | ||

| 15:30 | USD | Natural Gas Storage | |

| Forecast: | Previous: -174B | ||

| 21:30 | NZD | Business NZ PMI Jan | |

| Forecast: | Previous: 45.9 | ||

Friday, Feb 14, 2025

| GMT | Ccy | Events | Consensus | Previous |

|---|---|---|---|---|

| 07:30 | CHF | PPI M/M Jan | 0.10% | 0.00% |

| 07:30 | CHF | PPI Y/Y Jan | -0.90% | |

| 10:00 | EUR | Eurozone Q/Q Q4 P | 0.00% | 0.00% |

| 13:30 | CAD | Manufacturing Sales M/M Dec | 0.60% | 0.80% |

| 13:30 | CAD | Wholesale Sales M/M Dec | 0.40% | -0.20% |

| 13:30 | USD | Retail Sales M/M Jan | 0.00% | 0.40% |

| 13:30 | USD | Retail Sales ex Autos M/M Jan | 0.30% | 0.40% |

| 13:30 | USD | Import Price Index M/M Jan | 0.50% | 0.10% |

| 14:15 | USD | Industrial Production M/M Jan | 0.30% | 0.90% |

| 14:15 | USD | Capacity Utilization Jan | 77.80% | 77.60% |

| GMT | Ccy | Events | |

|---|---|---|---|

| 07:30 | CHF | PPI M/M Jan | |

| Forecast: 0.10% | Previous: 0.00% | ||

| 07:30 | CHF | PPI Y/Y Jan | |

| Forecast: | Previous: -0.90% | ||

| 10:00 | EUR | Eurozone Q/Q Q4 P | |

| Forecast: 0.00% | Previous: 0.00% | ||

| 13:30 | CAD | Manufacturing Sales M/M Dec | |

| Forecast: 0.60% | Previous: 0.80% | ||

| 13:30 | CAD | Wholesale Sales M/M Dec | |

| Forecast: 0.40% | Previous: -0.20% | ||

| 13:30 | USD | Retail Sales M/M Jan | |

| Forecast: 0.00% | Previous: 0.40% | ||

| 13:30 | USD | Retail Sales ex Autos M/M Jan | |

| Forecast: 0.30% | Previous: 0.40% | ||

| 13:30 | USD | Import Price Index M/M Jan | |

| Forecast: 0.50% | Previous: 0.10% | ||

| 14:15 | USD | Industrial Production M/M Jan | |

| Forecast: 0.30% | Previous: 0.90% | ||

| 14:15 | USD | Capacity Utilization Jan | |

| Forecast: 77.80% | Previous: 77.60% | ||

Markets Weekly Outlook – Inflation Fears Rise with Tariffs Ahead of US CPI Release

- Inflation expectations are rising, driven by tariff concerns and impacting consumer sentiment.

- US job growth was lower than expected, adding to market concerns.

- Key events for the week ahead include the US CPI release and testimony from Fed Chair Jerome Powell.

Week in Review: Tariff Fears Sees Inflation Expectations Rise

Markets had an interesting end to the week with a mixed bag of jobs data leaving a lot to be desired. However, in 2025 Fridays have proven anything but disappointing thus far, and this week did not disappoint.

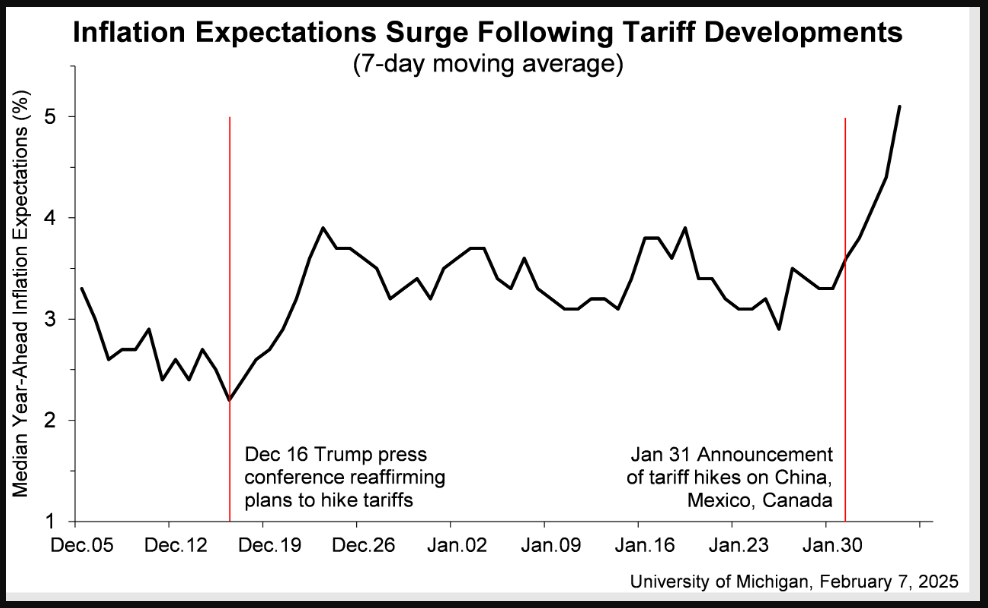

A significant uptick in inflation expectations was seen with the release of the preliminary Michigan consumer sentiment data. Inflation expectations for the next year jumped to 4.3%, the highest since November 2023, up from 3.3%. This is only the fifth time in 14 years that year-ahead inflation expectations have risen by one percentage point or more in a single month.

Many people are worried that high inflation could make a comeback within the next year. Meanwhile, long-term inflation expectations also increased slightly to 3.3%, the highest since June 2008, up from 3.2%.

Source: University of Michigan

There was also an impact on the overall sentiment, with the report showing sentiment in the US dropped to 67.8 in February 2025 from 71.1 in January. This was below expectations of 71.1. It marks the second month of declines, with sentiment hitting its lowest level since July 2024.

The current economic conditions index fell to 68.7 from 74, while the expectations index also dropped to 67.3 from 69.3. Additionally, views on buying durable goods fell by 12%, partly because many believe it’s too late to avoid the negative effects of tariff policies.

This news actually had a bigger impact on the markets than the actual NFP and jobs report which was highly anticipated.

The Labor Department reported that the U.S. economy added 143,000 jobs in January, which was less than the 170,000 jobs economists had predicted. The unemployment rate was 4%, slightly better than the expected 4.1%. However, the data also showed that the economy created 598,000 fewer jobs in the year up to March than previously estimated.

In the aftermath of the data releases we saw the US indices surrender the initial gains made to trade lower on the day. The S&P 500 was down around 0.83% while the Nasdaq was trading down around 1.15%.

My take on the data is that there is just enough in the data to stoke some concern in the minds of market participants.

On the FX Front, there was a solid end to the week for the US Dollar Index (DXY) after the rise in inflation expectations. The Dollar looked on course to end the week with a whimper before finishing the week strong and dragging all dollar denominated majors lower.

EUR/USD and GBP/USD both struggled on Friday with cable in particular surrendering some of its weekly gains.

Gold rose to print fresh all time highs once more before falling hard following the Michigan data release as well. Gold surrendered its all time high at 2886 before trading at 2858 at the time of writing.

Oil on the other hand enjoyed a rather mixed week but is set to conclude its third consecutive week of losses with Brent trading at 75.00 at the time of writing. Fear around Iranian sanctions were overcome by tariffs and how they may impact growth and thus global demand.

Weakening Oil demand remains an even greater concern following the arrival of the Trump administration and a period of tariff uncertainty.

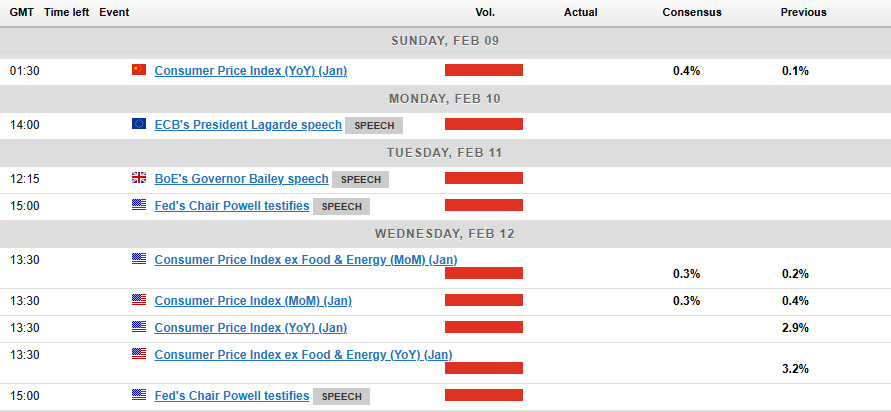

The Week Ahead: US CPI and Powell Testimony to Dominate

Asia Pacific Markets

The main focus this week in the Asia Pacific region is tariff developments and inflation data from China.

From China, the key event to watch is whether China and the US hold high-level talks soon. Currently, the US has added 10% tariffs on Chinese goods, though exemptions for items in transit mean the impact may take time.

China plans to impose its own tariffs on February 10, leaving a short window for potential negotiations to ease tensions. President Trump did say on Friday that he will probably meet Xi Jinping soon but no date has been given as yet.

On the data side, China will release January’s CPI inflation on Sunday. A slight increase to 0.4% YoY is expected, driven by higher food prices from the Lunar New Year, while non-food inflation is likely to stay low. The People’s Bank of China will also report January’s credit activity data next week.

Europe + UK + US

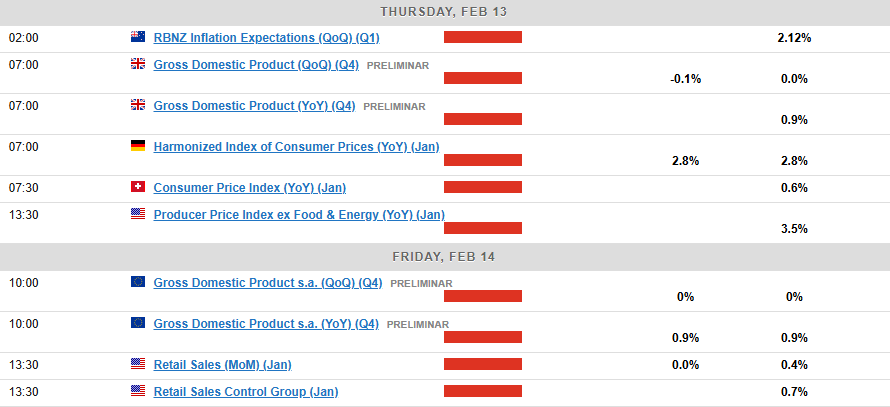

In developed markets, the US CPI release and testimony from Fed Chair Jerome Powell will dominate proceedings. We will also get a glimpse into the growth picture for both the UK and EU this week. GDP growth continues to plague the Euro Area, with Eurozone GDP Preliminary data being released on Friday.

US inflation data is expected to show a 0.3% monthly rise in both headline and core measures. Food and energy costs, housing prices, and rising vehicle prices are driving this increase. While tariffs have been paused for now, there’s a chance they could return later this year, keeping inflation high. This makes it unlikely the Fed will cut rates before June.

Fed Chair Jerome Powell will testify to Congress as the Fed releases its semi-annual monetary policy report. I expect the report to touch on the uncertainty caused by Trump’s policies but confirm that further rate cuts depend on economic data. Despite Trump’s initial rhetoric of pressure on the Fed, recent suggestions by his administration is that such a move is unlikely.

UK GDP data is due on Thursday with growth likely to have slowed in the second half of last year, and fourth-quarter GDP likely flat. Growth may improve in 2025 due to higher government spending, but it’s expected to fall short of the 2% forecast by the Office for Budget Responsibility. This, along with potential data revisions, adds pressure to the Treasury’s March Spring Statement, especially as rising debt costs have reduced fiscal flexibility.

Chart of the Week – US Dollar Index (DXY)

This week’s focus is on the US Dollar Index (DXY) after it recovered late on Friday and is looking like it is ready to print a fresh high.

The rising inflationary expectations may get a nod if US CPI comes in higher than expected, while any new tariff announcements will likely add to the USDs appeal.

Looking at the technical picture, the DXY has printed a higher low on the daily timeframe hinting at the possibility of a change in structure. The daily candle on Friday is struggling to close above the key 108.00 resistance level however, with a close above likely to give bulls confidence that further gains may materialize.

Failure to do so could see the DXY retest the 107.00 handle in the early part of next week which may add a further dimension to the US CPI release.

US Dollar Index Daily Chart – February 7, 2025

Source:TradingView.Com (click to enlarge)

Key Levels to Consider:

Support

- 107.00

- 106.13

- 105.63

Resistance

- 108.49

- 109.52

- 110.00

The Weekly Bottom Line: Tariffs On, Tariff Off, Tariffs On?

Canadian Highlights

- President Trump kept most Canadians glued to their TVs/socials this week, announcing tariffs to take effect February 1st, before quickly delaying them for 30 days following a big market selloff and further measures at the border from Canada.

- Canadian trade data came in quite positive in December as firms appear to be frontrunning potential tariffs. Exports for the fourth quarter of 2024 are now tracking double digit growth.

- The job market continues to hum along, with a gain of 76k net new jobs in January. That marks three straight months of above-trend job growth.

U.S. Highlights

- Tariffs on Canada and Mexico have been put on hold for one month, but a 10% tariff was imposed on imports from China.

- Companies have ramped up inventories ahead of tariffs, leading to a sharp increase in the trade deficit in December. Activity has eased off in the services sector, but continued to reaccelerate in manufacturing.

- Hiring has slowed in January, however, the labor market remains solid overall. Significant upward revisions to the fourth quarter figures suggest that job growth was stronger at the end of last year than previously thought.

Canada – Tariffs On, Tariff Off, Tariffs On?

It feels like the longest week ever for Canadians. Many of us with sleepy eyes last weekend were sorting out the impact of Trump’s tariffs and what they would mean for an economy that has been on weak footing for the last two years. Then the reprieve of a 30-day delay came on Monday, creating a whipsaw effect in Canadian financial markets. Economic data this week was also headline grabbing. Trade data showed that Canada’s export dependence on the U.S. increased through the end of last year (Chart 1), while employment growth gave a glimpse of what could have been/may still be a solid growth trajectory for 2025 (Chart 2).

President Trump kept most Canadians glued to their TVs/socials on Saturday, announcing a 25% tariff on Canadian exports (10% on energy) to take effect Tuesday, February 1st. With Canadian retaliation announced, financial markets went into panic on Monday. Government of Canada yields collapsed by nearly 20 bps and the Loonie reached a low of 67.5 U.S. cents. Although the President postponed tariffs, Monday’s reaction gave everyone a view into what could be in store for Canadian markets should a trade war come to pass. In the meantime, yields have recovered their lost ground, while the Canadian dollar is hovering close to 70 U.S. cents.

Canadian trade data came in quite positive in December as firms appear to be front running tariffs. Exports for the fourth quarter of 2024 are tracking double digit growth, a big rebound from the negative growth seen over much of last year. High demand for energy and metals from the U.S. led the gain, as the trade surplus with the U.S. clocked in at over $100 billion for the year. This overall figure could be used as fodder for President Trump to validate his claims that trade with Canada is ‘unfair’, even though the trade surplus would become a deficit when energy is excluded.

In any other week, Friday’s labour market report would have been the focus. But trade risks have bumped it to runner up. Yet, the jobs market continues to hum along. Today’s gain of 76k net new jobs in January marks three straight months of above trend job growth. Importantly, the unemployment rate dipped to 6.6%, as population growth ebbs. While the labour market has been a pillar of strength for the Canadian economy, the outlook has become precarious. We have been expecting the unemployment rate to decline over this year, but our tariff scenario analysis shows that it could quickly rise to 7%, if not higher, should tensions persist.

Canada has entered a period of great uncertainty. Tariff threats have cast a shadow over the economic outlook. Market pricing for the Bank of Canada has started to move towards a greater likelihood of another cut come March. The Bank has highlighted the growing downside risks, perhaps signaling a greater willingness to take out more insurance should risks become reality.

U.S. – Canada-Mexico Tariffs on Hold

This week was anything but boring. On Monday, an 11th-hour deal was reached to delay tariffs on Canada and Mexico for a month. However, while Canada and Mexico were spared, China was not, as an additional 10% tariff was imposed on all imports from the country.

The prospect of tariffs being imposed on North America in a month, or in April when the review of current trade policies is completed, looms large. Financial markets have largely recovered from their initial knee-jerk reaction to the tariff announcement, with the S&P 500 paring back losses by the end of the week. However, inflation expectations over the next two years have risen (Chart 1) while bond yields have declined. This points to investors’ concerns that tariffs will accelerate inflation and slow economic growth.

.

Businesses’ uncertainty about the looming tariffs were reflected in the trade data. The U.S. trade deficit widened sharply in December – the largest one-month increase since the early 1990s. Imports surged as companies rushed to ramp up inventories ahead of potential tariffs. Last month’s sharp increase in the trade deficit is likely temporary, but trade policy uncertainty will continue to affect trade flows throughout the year. Uncertainty about tariffs also clouds the outlook in the manufacturing sector, particularly in industries such as auto manufacturing. Even though the ISM manufacturing index has continued to improve in January, rising for the third consecutive month and finally moving into expansionary territory, supply chain disruptions could dent the sector’s nascent progress.

Activity in the services sector continued to expand robustly in January, although it dialed back a notch. The services sector is less exposed to trade than manufacturing, but it is not immune. The prices paid subcomponent remains elevated, and any supply chain disruptions and higher input prices could reignite inflationary pressure.

Additional inflationary impetus could also come from the labor market. Today’s employment report showed that the U.S. economy added 143k jobs in January. This is considerably less than December’s tally (+305k), but still a solid outturn, particularly when combined with a slight decline in the unemployment rate and an uptick in wage growth. Moreover, wildfires in Los Angeles and a cold weather spell nationwide could have also weighed on employment, suggesting a bounce-back next month could be in the cards. Lastly, revisions through the fourth quarter were notably higher, adding an extra 101k jobs to the previously reported figures and suggesting that hiring momentum was even stronger at the end of last year than previously thought (Chart 2).

With inflation progress having stalled in recent months, wage growth showing staying power and heightened uncertainties on how far the new administration will go on its policies, the Fed is likely to remain more cautious. Next week’s inflation report will likely show that the Fed’s patience is justified, as inflation remains persistently above the Fed’s 2% target.

Weekly Economic & Financial Commentary: The Tariff Man Cometh

Summary

United States: It Felt Like Much Longer than a Week

- It was a week of contradiction, where just when things looked like they were going badly, some mitigating factor offset a prior concern. By Friday, it felt more like survival than victory. The takeaways include an improving backdrop for manufacturing and construction, a little less heat in the service sector and a jobs market that refuses to fit into a tidy label.

- Next week: CPI (Wed.), Retail Sales (Fri.), Industrial Production (Fri.)

International: Foreign Central Banks Lower Rates

- This week saw rate reductions from central banks across emerging and advanced economies. In Mexico, Banxico lowered its policy rate by 50 bps to 9.50% and issued commentary that we view as consistent with another same-sized move in March. Elsewhere, the Reserve Bank of India delivered its first rate cut since 2020, lowering its policy rate by 25 bps, and the Bank of England also cut its policy rate by 25 bps.

- Next week: Norway CPI (Mon.), Brazil Inflation (Tue.), U.K. GDP (Thu.)

Credit Market Insights: The Wave of Credit Tightening Is Quickly Receding

- Banks appear to be changing their risk calculus. The Q4 Senior Loan Officer Opinion Survey revealed that banks are still tightening lending standards on net, but the prevalence of restriction is quickly fading.

Topic of the Week: The Tariff Man Cometh

- The week started off with a bang when the Trump administration announced plans on Saturday to place tariffs of 25% on goods imports from Canada and Mexico and a tariff of 10% on goods imports from China, effective Feb. 4. Though the Canada and Mexico tariffs were postponed for 30 days, the domestic upshot of the policies, if they are eventually realized, is higher inflation in the near term and slower growth in the outlook.