Sample Category Title

Market Update – European Session: UK And EU Try To Hammer Out Differences Ahead Of Upcoming Leader Summit

Asia:

BoJ Gov Kuroda reiterated that would continue current easing framework until 2% inflation was reached, Yield Control (YCC) program had been quite successful

China Ministry of Commerce (MOFCOM) expressed “strong dissatisfaction and firm opposition” to a statement by the US to the WTO that it opposes granting China market

Europe:

ECB's Villeroy (France) reiterated recovery in euro area was gaining momentum as current favorable economic winds were 'strong'. Still no room for complacency; needed to be 'vigilant' as inflation short of goal

European institutions reach a staff level agreement with Greece authorities on the policy package supporting the ESM program, will presented to EuroGroup on Dec 4th. Greek authorities planned to implement the prior actions necessary to conclude the 3rd review as soon as possible

Bank of International Settlements (BIS) Quarterly Review: Stock prices are above historical averages; Bond-market yields show even more froth than stocks. When and if interest rates begin to rise, corporates may have the incentive to tilt their capital structure back to equity, or at least to reduce stock repurchases, which could raise further questions about stock market valuations

Brexit:

UK Business Sec Clark: Optimistic that Britain and the EU will agree on all major issues before next week’s EU summit. UK fully recognized its payment obligation. Both sides needed to get a clear understanding what these duties are and when they were due. Agreement about rights of EU citizens living in UK an UK citizens living abroad was close

EU official: Britain and EU were 90% of the way to a deal that would open the door for transition and trade talks this month

Diplomatic sources noted that EU was expected to offer a 1st signal this week that enough progress has been made in Brexit talks to start new negotiations with London in Dec on future trade relations. PM May and EU's Juncker to sign a document after meeting in Brussels that would spell out both sides' commitment to sorting out the Irish border conundrum

EU's Tusk: if UK offer was not acceptable to Ireland then its not acceptable to the EU. Supportive of Irish request for no hard border with N. Ireland; To consult with Irish should UK offer on border be sufficient

Americas:

US Senate voted 51-49 to approve sweeping tax overhaul; talks between Senate and House of Representatives will likely begin during week of Dec 4th

President Trump tweets: Sec State Tillerson is not leaving the administration (**Note: Sec of State Tillerson: no truth to reports that he is being replaced)

ABC News suspended reporter Brian Ross for 'erroneous' story related to former national security adviser Michael Flynn. Noted that It was shortly after the election, that President-elect Trump directed Flynn to contact Russian officials on topics that included working jointly against ISIS

Economic Data:

(TR) Turkey Nov CPI M/M: 1.5% v 1.1%e; Y/Y: 13.0% v 12.5%e; CPI Core Index Y/Y: 12.1% v 12.3%e

(ES) Spain Nov Unemployment M/M: +7.3K v 56.8K prior

(EU) Euro Zone Dec Sentix Investor Confidence: 31.1 v 33.4e

(UK) Nov Construction PMI: 53.1 v 51.0e

(GR) Greece Q3 GDP Q/Q: 0.3% v 0.8% prior Y/Y: 1.3% v 1.6% prior

Fixed Income Issuance:

None seen

SPEAKERS/FIXED INCOME/FX/COMMODITIES/ERRATUM

Equities

Indices [Stoxx600 +0.7% at 386.7, FTSE +0.7% at 7349, DAX +1.1% at 13007, CAC-40 +0.9% at 5362, IBEX-35 +1.0% at 10184, FTSE MIB +1.1% at 22344, SMI +0.8% at 9348, S&P 500 Futures +0.5%]

Market Focal Points/Key Themes:

European Indices trade sharply higher tracking US futures after the US senate voted in favor of tax reform which in tern has also helped lift the dollar. M&A news was the primary theme this morning with Prysmian acquiring General Cable in a $3B deal while Trygvesta acquired Alka Forsinkring for DKK8.2B. Elsewhere Rio tinto provided initial FY18 outlook, whilst Alk Abello trades sharply lower after announces a 3 year investment plan, as well a temporarily suspending its dividend.

Dialog Semi continues to decline after it confirmed it continues to supply Apple, but will know in Q1 whether this relationship will change.

Equities

Materials: [Rio Tinto [RIO.UK] +1.1% (Initial FY18 outlook, Chairman appointment)]

Financials: [Trygvesta [TRYG.DK] +3.5% (Acquires Alka Forsinkring for DKK8.2B)]

Technology: [Soitec [SOI.FR] +2.3% (Capital markets day), Dialog Semi [DLG.DE] -16% (Confirms it continues to supply Apple)]

Telecom: [Prysmian [PRY.IT] -2.1% (Acquires General Cable Corp for $30/shr)]

Healthcare: [Odorsia [IDIA.CH] +3.9% (Collaboration with Janssen Biotech), Circasia [CIR.UK] +12.2% (Tudorza® Successfully Met Both Primary Endpoints in ASCENT Phase IV Study), Alk Abello [ALKB.DK] -11% (3 year investment plan)]

Speakers

Ireland European Affairs Min Mcentee: Not close to a breakthrough on Irish border issue but are making progress

Ireland Dep PM Coveney: Have seen progress on Irish issues. Need clear language that there will be no border. Have a text but no agreement. Could have a breakthrough as early as today

Bavarian Premier Seehofer to step down from position in Q1 (in-line with recent speculation). Soeder to become Bavaria PM with CSU backing

Turkey Dep PM Simsek: Lasting inflation decline to begin in Dec

Japan PM Abe: Infrastructure investment i not keeping up with demand

China reportedly will keep exempting 10% purchase tax on electric vehicles to 2020

China and Japan officials to hold 8th round of discussions regarding maritime affairs during Dec 5-6th period

Russia Nov Oil Production at 10.94M bpd v 10.93M m/m

Saudi Arabia Oil Min Al-Falih: Believed OPEC would not alter course in H2 of 2018. Will not flood the market

Currencies

The USD began the trading week exhibiting a relief rally after the US Senate passed the tax reform bill. Worries about the possibility of the bill being delayed had kept the dollar weak last week

EUR/USD lower by 0.2% at 1.1860 area

GBP/USD was relatively steady as Brexit talks head into the EU deadline for clarity. Pair off 0.2% at 1.3435 area

USD/JPY higher by 0.7% at 112.85

Fixed Income

Bund futures trade 162.99 down 56 ticks, after the U.S. Senate passed the tax cuts bill. Continued dowward pressure sees 162.10 followed by 161.50. A reversal targets 163.40 then 163.75.

Gilt futures trade at 125.11 down 34 ticks, following the move in Treasuries and Bunds. Continued upside eyeing 125.15 then 125.65. Downside targets include 124.01 then 123.75.

Friday’s liquidity report showed Thursday's excess liquidity rose to a record high of €1.912T from €1.886T. Use of the marginal lending facility fell to €243M from €265M prior.

Looking Ahead

(RO) Romania Nov International Reserves: No est v $37.6B prior

(UK) PM May's lunch with EU's Juncker ahead of key Brexit clarification deadline.

(CH) Swiss Parliament holds Winter Session in Bern

05:25 (BR) Brazil Central Bank Weekly Economists Survey

05:30 (NL) Netherlands Debt Agency (DSTA) to sell Bills

06:45 (US) Daily Libor Fixing

08:00 (BR) Brazil Oct CNI Capacity Utilization: No est v 77.5% prior

08:00 (SG) Singapore Nov Purchasing Managers Index (PMI): No est v 52.6 prior

08:00 (IN) India announces details of upcoming bond sale (held on Fridays)

08:00 (ES) Spain Debt Agency (Tesoro) announces size of upcoming actions in week

08:05 (UK) Baltic Dry Bulk Index

08:30 (CH) Swiss Government question time in Parliament

08:55 (FR) France Debt Agency (AFT) to sell combined €5.2-6.4B in 2-month, 3-month, 6-month and 12-month BTF Bills

09:00 (MX) Mexico Oct Leading Indicators M/M: No est v 0.12 prior

09:00 (EU) Eurogroup meeting

09:30 (EU) ECB announces Covered-Bond Purchases

09:35 (EU) ECB calls for bids in 7-Day Main Refinancing Tender

10:00 (US) Oct Factory Orders: -0.4%e v+ 1.4% prior, Factory Orders (Ex Transportation): No est v 0.7% prior

10:00 (US) Oct Final Durable Goods Orders: -1.0%e v -1.2% prelim; Durables Ex Transportation: No est v 0.4% prelim

10:00 (DK) Denmark Nov Foreign Reserves (DKK): No est v 464.3B prior

11:00 (IS) Iceland Q3 Current Account (ISK): No est v 16B prior

11:30 (US) Treasuries to sell to 3-month and 6-month bills

14:00 (CO) Colombia Nov Total PPI M/M: No est v 0.8% prior

GBP/USD: UK Manufacturing PMI

The Sterling depreciated initially against the Greenback, fuelled by stronger-than-anticipated Britain's manufacturing data. The GBP/USD exchange rate fell 15 base points or 0.11% to be seen trading lower, though bulls attempted to put the pair back above the 1.3510 mark.

The UK factories enjoyed the strongest monthly growth since 2013, indicating that manufacturing would fuel the country's sluggish economic expansion entering next year. The Markit/CIPS survey showed that Britain's Manufacturing PMI rose to 58.2 in November, following an upwardly revised 56.6 in the prior month. A strong manufacturing sector could remain a bright spot in 2018, while overall economic slowdown is expected to deepen as Brexit approaches in March 2019.

USD/CAD: Canadian Gross Domestic Product

The Loonie strengthened significantly against the Greenback on strong job data, rather than on cooling GDP growth showed in the report on Friday. The USD/CAD currency pair dropped 113 base points or 0.88% to touch 1.2771 level and depreciate futher nearing the 1.2700 area.

Statistics Canada said the country's the GDP rate was at an annualised 1.7% in the Q3, following a downwardly revised 4.3% in the preceding quarter. Canadian unemployment rate fell to 5.9% for the first time since 2008, while the economy added 79.5K jobs, which was twice as many positions compared with October. Average hourly wages kept rising at yearly 2.7% in the strongest performance since early 2016, being the one of the factors for the BoC to decide on further policy changes.

Euro Slips As US Senate Passes Tax Reform

The euro has posted slight losses in the Monday session. Currently, EUR/USD is trading at 1.1847, down 0.47% since the close on Friday. On the release front, Eurozone Sentix Investor Confidence dropped to 31.1, short of the estimate of 32.3 points. Eurozone PPI gained 0.4%, matching the forecast. In the US, today's sole release is Factory Orders, which is expected to decline 0.3%. On Tuesday, Germany and the eurozone release services PMIs, and the Eurozone will also release retail sales. The US will publish US ISM Non-Manufacturing PMI.

Brexit is on the menu in Brussels. as Britain and the European Union appear close to moving to trade talks. Prime Minister May and European Commission President Jean-Claude Juckner meet later on Monday in Brussels, hoping to move closer to wrapping up the first phase of the talks. May has moved closer to the European's demands on a divorce bill of around EUR 50 billion, but two items have yet to be resolved. One is the border between the UK (Northern Ireland) and Ireland, which is a member of the EU. The UK will clearly not remain in a customs union with the EU, but Ireland is insistent that there not be a hard border. The second issue is whether the European Court of Justice will have a role protecting European citizens in the UK. The EU is in favor of a role for the court, while many British lawmakers feel that such a move would impinge on British sovereignty.

All eyes are on Washington, as the Senate is set to vote on its version of tax reform. A vote was expected on Thursday night, but this has been delayed until Friday. Republican lawmakers are confident that they have the necessary votes to pass the bill, but with the vote expected along party lines, the results will be close. If the Senate does pass the bill, the stock markets and US dollar will likely respond with gains. The next step in the tax reform saga would be for the House and Senate to bridge the differences between the two bills and come up with a single version.

After some stumbling on Friday, the US Senate passed a tax reform bill on the weekend. The vote was a squeaker, with 51 Republicans voting yes, against 49 Democrats and 1 Republican. The Senate vote is a big win for President Trump, who wants to sign a tax bill before Christmas. The Senate and House must now reconcile their two bills, and the new uniform bill will then have be passed in both houses. Investors are pleased with the bill, and the US dollar has responded to the vote with broad gains.

Light Monday Schedule Kicks Off Active Week In The Market

A steady stream of economic data will make its way through the financial markets on Monday, giving investors a taste of what’s to come later in the week.

The European calendar begins at 08:00 GMT with a report on Spanish unemployment. Later in the morning, Markit and the Chartered Institute of Purchasing and Supply will release the latest UK construction PMI.

At the same time as the PMI release, Sentix will unveil its December investor confidence indicator covering the Eurozone. As the name implies, the monthly release conveys a snapshot of market opinion about the current economic situation in the currency region.

Earlier in the day, the University of Melbourne reported a 0.2% uptick in Australia’s inflation rate last month. That followed a gain of 0.3% the previous month. In annualized terms, this translated into 2.7% growth.

Later in the session, the European Commission will release the latest producer inflation report for the Eurozone.

The only noteworthy North American release takes place at 15:00 GMT when the US Commerce Department unveils the latest factory orders report.

AUD/USD

The Australian dollar was little changed against its US counterpart Monday, with the AUD/USD holding just above 0.7600. The pair broke out of a weeklong slump on Friday to reach a high of 0.7634. The technical picture remains neutral, with 0.7640 offering the key short-term resistance. That level continues to limit major upside moves for the pair. A break above this level would lead to a test of the 0.7700 region. On the opposite side of the spectrum, immediate support is located at 0.7595, followed by 0.7530, which corresponds with the November low.

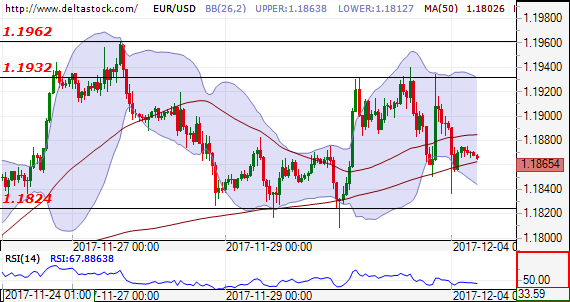

EUR/USD

The euro fell further below 1.1900 US on Monday, as investors awaited a deluge of fundamental indicators later in the week. The common currency has made a series of up moves in recent weeks, but is finding it difficult to return back above 1.2000 US. At last check, the EUR/USD was trading around 1.1872 for a loss of 0.2%. From a technical perspective, immediate support is located at the 1.1860 level, followed by 1.1820. On the opposite side of the ledger, resistance is likely found at 1.1930, followed by 1.1960.

GBP/USD

Cable has enjoyed a surge of momentum in recent weeks as investors shrugged off Brexit risks. The GBP/USD traded as high as 1.3548 on Friday before giving back most of its gains subsequently. At press time, the pair was seen trading at 1.3469. Cable is testing its immediate support level of 1.3450. A further breakdown below this level would expose 1.3420 as the next target. In terms of resistance, the first line of contention is offered at 1.3505, followed by 1.3550.

Technical Outlook: WTI Oil – Hanging Man On Weekly Chart Warns Of Correction

WTI oil price extended lower on Monday and returned below falling weekly 200SMA ($58.07) which was briefly broken in past two weeks. Reversal signal is developing on weekly chart after last week's action ended in weekly Hanging Man candle and closed in red after six straight bullish weeks. Overbought weekly slow stochastic and RSI turning lower after denting overbought zone border are additional negative signals. Today's weakness could extended towards key supports on daily chart at $57.10 (20SMA) and $56.75 (29 Nov low), with sustained break here needed to confirm reversal. Overall bias remains bullish with positive sentiment being boosted by OPEC's decision to extend output cut agreement until the end of 2018. Buying on correction remains favored for final push towards $60.00 target, with extended pullback to risk dip towards next key support at $54.80 14 Nov trough).

Res: 58.31, 58.86, 59.02, 60.00

Sup: 57.41, 57.10, 56.75, 56.41

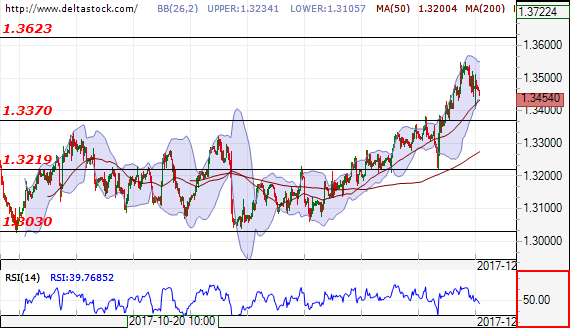

Forex Technical Analysis: EUR/USD, USD/JPY, GBP/USD

EUR/USD

Current level - 1.1865

The outlook is positive for breakthrough the level at 1.1932 for test at 1.1960 and uptrend up to 1.2050. In negative direction the support levels are at 1.1876 and after that at 1.1811.

| Resistance | Support | ||

| intraday | intraweek | intraday | intraweek |

| 1.1932 | 1.2090 | 1.1824 | 1.1690 |

| 1.1960 | 1.2090 | 1.1811 | 1.1550 |

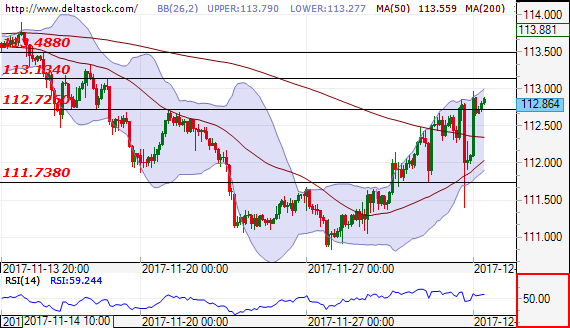

USD/JPY

Current level - 112.86

The movement of the currency pair is right before a test at the level 112.72. Successful breakthrough at this level will lead to movement up to 113.90. In negative direction the support level will be at 110.80.

| Resistance | Support | ||

| intraday | intraweek | intraday | intraweek |

| 112.72 | 113.90 | 111.73 | 109.50 |

| 113.40 | 114.70 | 109.50 | 107.30 |

GBP/USD

Current level - 1.3454

After the yesterday breakthrough of the resistance level at 1.3450, the forecast is positive for test at 1.3620. In negative direction for support level we could take the level at 1.3219.

| Resistance | Support | ||

| intraday | intraweek | intraday | intraweek |

| 1.3623 | 1.3460 | 1.3370 | 1.3220 |

| 1.3700 | 1.3660 | 1.3219 | 1.3020 |

Greenback On The Rise After US Senate Approves Tax Bill

USD rallies after US Senate passes tax bill

The US dollar has been rallying strongly since the market opening this morning. The greenback extended gains against all its G10 peers, rising the most against the Japanese yen and the Swiss franc (+0.65% both), the New Zealand dollar (+0.45%) and the Swedish krona (+0.38). On Saturday, the Senate finally approved the US tax-reform proposed by Donald Trump. The outcome of the vote was very close as the bill passed by a vote of 51 to 49. No democrats voted for the bill.

After months of struggle, this is the first victory for Donald Trump since he took office more than a year ago. However, the final bicameral version may take some time to come up, as the Senate and the House of Representatives have to find common ground. Potentially, the bill could lead to a reduction of the corporate tax rate to 20% (compared to 35% currently), in addition to a cut for individuals as well.

We have been waiting for this signal for quite some time. However, it seems that the news come a little late as investors have already shift attention to the ECB’s tightening move and the economic acceleration in the euro zone. We expect the single currency to keep appreciating against the greenback. On the other hand, high quality commodity currencies, such as the Aussie and the Kiwi, should suffer from narrowing interest rate differentials against US yields. EUR/USD is currently trading at around 1.1850, slightly below the 1.1961 resistance (high from November 27th). On the downside, a support lies at 1.1809 (low from November 30th).

Switzerland: Sight deposits decline

The Swiss franc keeps on weakening against the euro and is now trading below 1.17. Late last July the EUR/CHF pair jumped from 1.10 to 1.15 and since the pair continues rising. This morning the sight deposits have been released and it seems that at current levels, the SNB is less under pressure. Indeed sight deposits have slightly declined.

There is still nonetheless the fear of deflation and tomorrow will also see the release of the consumer prices for November. Inflation is coming back and we clearly believe it is a matter of time before imports create inflation. The Swiss economy is very resilient and the abandon of the peg is not a bad news any more.

On top of that, the EURCHF should continue to be bullish as markets are still very positive regarding the ECB monetary policy. In addition, even though we believe that the European economic uncertainties will largely weigh on the euro in the longer run. In the short to medium-term, there is a clear possibility to reach 1.20.

RBA and BoC meeting

For their final meeting of the year the RBA is expected to hold its policy rate at 1.5%. While not like to shift the RBA policy path the recent bout of weak housing data, retail sales and disappointing wage growth are clear downside risks to the economy (ie RBA outlook). Activity data has improved but concern over wage deceleration will push communications away from tighten monetary policy. The softness does suggest that we could hear a dovish RBA. Markets are not pricing in a rate hike until 2019, therefore dovish tone will have limited effect on AUD.

The Banks of Canada meeting does have the possibility of a surprise. The BoC has a recent history of surprising the markets with bot cuts and hikes. Heading into December there was only 10% probably of a hike yet stronger economic data has pushed pricing to 20%. In the BoC financial stability report, the banks discussed the high valuation and overleverage household as a primary risk. Gradually higher interest rate would help reduce these risks. With CAD weaker then September tighter policy, will unlikely raise red flags at the BoC. We suspect that market in underpricing the risk of an unexpected rate hike. That said, we are main bearish on comity currencies and Thursday OPEC meeting have been unable to break key technical resistance levels.

Technical Outlook: SPOT GOLD – Thickening Daily Cloud Pressures For Test Of 200SMA

Spot Gold stands at the back foot on Monday and dipped close to last week's low at $1270, after coming under fresh pressure on signals that US tax cut plan is closer to passage.

Rising bearish pressure could result in break below $1270 where basing attempts were seen and eventual push towards key supports at $1266 (200SMA), $1263 (27 Oct low) and $1260 (01 Oct low).

Last Friday's strong rejection at daily cloud base and weekly close in red (the second straight bearish week) were negative signals.

Also, thickening daily cloud continues to weigh and support bearish scenario, along with expectations for rate hike on next week's FOMC monetary policy meeting.

Monday's action stays under thick hourly cloud (spanned between $1276 and $1283) which is expected to limit upticks and keep near-term focus at the downside.

Res: 1276, 1283, 1285, 1289

Sup: 1270, 1266, 1263, 1260

Dollar Higher After Senate Passes Tax Bill, Sterling In Wait-And-See Mode

The U.S. Senate's approval to pass the tax cut bill on Saturday overshadowed the continuing investigation into connections between U.S. President's inner circle and Russia. The U.S. dollar rallied across the board with most gains seen against the Yen which fell to a two-week low early Monday. U.S. 10-year treasury yields rose above 2.4% after falling 10 basis points on Friday. Although it does not appear that investors' optimism will send yields towards 2017 highs, if the yield curve manages to steepen further in December, we are likely to see more inflows to the U.S. dollar. This would largely depend on how talks between the Senate and the House develop in the weeks ahead, but with the government shut down looming, there's likely to be some noise in currency markets.

Brexit talks resume

Sterling is the only major currency treading water against the dollar on growing confidence that Brexit negotiations will move to a new stage when E.U. leaders meet in mid-December. Numerous reports last week indicated that the U.K. is getting closer to announcing a divorce bill that will lead to significant progress in Brexit talks. Today's meeting between Theresa May, Jean Claude Junker and Michel Barnier will provide an early indication of whether the U.K. is getting closer to negotiating trade deals. The three main barriers to overcome are the Brexit divorce bill, Irish Border and E.U. expatriates' rights. Significant progress on this front will likely push Sterling higher -to retest 2017 highs at 1.3656.

It is the non-farm payrolls week

The Federal Reserve is expected to continue tightening monetary policy by raising rates another 25 basis points on 13 November. Given that a final rate hike is already priced in, the trajectory in 2018 remains unclear given the uncertainty towards the fiscal progress and inflation path. Friday's non-farm payrolls will be the final jobs report released in 2017 and will help the Fed assess whether inflation is likely to strengthen next year. Nonfarm payrolls are expected to have increased by 198,000 in November, after climbing by 261,000 in October. According to Thompson Reuters, the key figure traders should focus on, is wages which have been the missing ingredient throughout this year. An increase in wages of 0.4% or above, will support the central bank's argument that low inflation should be attributed to temporary factors, and this should provide a further lift to the U.S. dollar.