Sample Category Title

In The EU, Ongoing Brexit Negotiations Will Be In Focus Today

Market movers today

In the EU, ongoing Brexit negotiations will be in focus today, where the UK's Theresa May is set to have lunch with EU's Jean-Claude Juncker.

In the US, an agreement on tax reform is moving closer, while the suspension of the US debt ceiling will expire on Friday.

In addition, the ongoing investigation on Trump may draw headlines today as well.

In Denmark, FX reserve data for November is due for release today. We do not expect Danmarks Nationalbank to have intervened in FX markets in November.

The rest of the week bring interesting data releases though with US non-farm payrolls, ISM non-manufacturing and German industrial production due. In the Scandi calendar, the Norges Bank Regional Network Report, Norwegian house price data and Swedish industrial production and orders are up for release.

This morning, we have published our semi-annual Big Picture including our updated economic outlook for the global economy (US, euro area, the UK, Japan, China and emerging markets). We think the global expansion is going to continue in coming years driven by continued strong consumer spending and a robust investment recovery. We look for inflation to stay fairly muted and central banks to withdraw stimulus only very gradually.

Selected market news

Headlines over the weekend were centred on the development in the ongoing investigation into US President Trump's potential obstruction of justice. The political uncertainty in the US has clouded the skies over USD, which on the other hand looks set to receive a helping hand from the steady progress towards tax reform. On Friday, a vote on the tax reform in the Senate passed. Overall, however, the news did not move either EUR/USD or the US stock market significantly on Friday.

On Friday, Baker Hughes reported a small rise in the US oil rig count. US oil producers thus seem to be benefiting from the rise in oil prices in H2 by adding to production. Fundamentals in the oil market in general were in focus last week, where OPEC also agreed to extend production cuts for another nine months. Oil prices in the meantime have been relatively stable, with the price on Brent crude trading around the USD63/bbl level throughout much of last week

Market Update – Asian Session: Equity Markets Muted Despite US Passing Tax Bill

Headlines/Economic Data

General Notes/Themes: US equity futures open higher amid weekend Senate passage of tax reform bill

Asian equities gains capped despite US tax vote

Shares of Tencent rebound after dropping over 3% on Friday

Japan

Nikkei 225 opened +0.1%, later pared gains; closed -0.5%

Softbank -0.8%; Fast Retailing +0.9%

USD/JPY opened +0.5%: US Senate passes tax bill on Saturday, ABC News retracts story related to former NSA Michael Flynn

Japan PM Abe: Want to put together policy package this week

BoJ Gov Kuroda: Will continue current easing framework, YCC program has been quite successful, will continue until 2% inflation is reached

Japan Nov Monetary Base y/y: 13.2% v 14.5% prior; At End of Period: ¥471.5T v ¥476.6T prior

Japan may cut corporate tax rate to 20% through incentives – Japanese Press

7733.JP Cuts H2 domestic production by 15% to 510-520K (prior 590-610K) due to slower production while faulty inspection process is fixed

Korea

Kospi opened +0.5%

Samsung Electronics +0.3% (pared earlier losses)

Korean Won -0.5% (US dollar trades broadly firmer)

South Korea and US start air combat exercises amid North Korea threats

Bank of Korea (BOK) sells KRW400B in 6-month monetary stabilization bonds; avg yield 1.66%

South Korea sells 5-year government bonds; avg yield 2.38%

090430.KR Reports Nov cosmetics exports +34.2% y/y

China/Hong Kong

Markets opened lower: Hang Seng -0.4%, Shanghai -0.2%

Markets later pare losses: Hang Seng Information Technology Index +1.7% (Tencent +2%, declined over 3% on Friday)

(CN) China President Xi: China will not close its door to the global internet, but that cyber sovereignty is key in its vision of internet development

(CN) China PBoC and China Banking Regulatory Commission (CBRC) announces several key principles for new regulations on micro lending, banning unlicensed firms or individuals from carrying out lending business

(CN) China’s LexinFintech to delay Nasdaq listing timeframe as it plans to conduct more due diligence for IPO – financial press

(RU) Russia planning to sell yuan denominated sovereign bonds for the first time - financial press

Chinese metals rise: Dalian Iron Ore up over 6%, Shanghai Rebar Steel gains over 2%

(CN) China Gov Research Body sees 2017 crude steel output at 832Mt, +3% y/y; Sees 2017 Iron ore demand seen at 1.122Bt, +1.3% y/y; Sees 2018 iron ore demand 1.12B 1.12Bt, -0.2% y/y

(CN) China NDRC to hold meeting on how to help stabilize gas prices - Chinese press

(CN) Bank of Communications expects China inflation will drop mildly in November and remain tame until the end of the year due to stable food prices and a weakening carry-over effect - Xinhua

(CN) PBoC skips open market operation (OMO) for second straight session as it reiterates liquidity is at a ‘high level’; net drain CNY90B

(CN) PBOC said to have simplified open market demand gauging system

(CN) PBoC sets yuan reference rate at 6.6105 v 6.6067 prior

(CN) China Ministry of Commerce (MOFCOM) expressed “strong dissatisfaction and firm opposition” to a statement by the US to the WTO that it opposes granting China market economy status

(CN) China Ministry of Land and Resources research: China will step up exploration for oil and gas and develop unconventional resources to ease the country's reliance on imports

Looking Ahead: China Caixin Nov Services PMI due on Tuesday

Australia/New Zealand

ASX 200 opened +0.1%; closed +0.1%

ASX 200 Financials Index -0.6%; Resources Index +0.8%

Rio Tinto [RIO.AU] +1.2% (Guided mid-point of FY18 iron ore shipments up y/y; named new board Chairman)

MTS.AU Reports H1 (A$) underlying Net 99.0M v 87Me; EBIT 152M v 136Me; Rev 7.06B v 7.0Be; +8%

GEM.AU Cuts FY17 (A$) underlying EBIT ~160M (prior 170-180M); Avg like-for-like occupancy 77% v 79.7% y/y; cites slowing occupancy growth; -21%

NTC.AU Secures order for network connection device from NBN; +16%

(AU) AUSTRALIA Q3 BUSINESS INVENTORIES Q/Q: 0.2% V 0.0%E; CORPORATE OP PROFIT Q/Q: -0.2% V 0.1%E -(AU) Australia sells

A$400M v A$400M indicated in 3.25% April 2029 Bonds, avg yield 2.6438%, bid to cover 3.8x -(AU) Australia re-elects deputy Gov Barnaby Joyce after losing his job for having dual citizenship

(AU) Australia buys back A$400M in Oct 2018 and March 2019 bonds; avg yield 1.7250%; bid-to-cover 4.255x

(AU) Australia sells A$400M v A$400M indicated in 3.25% April 2029 Bonds, avg yield 2.6438%, bid to cover 3.8x

Looking ahead: Australia RBA decision, Q3 Current Account and Net Exports Contribution and Oct Retail Sales due to be released on Tuesday. RBNZ Gov Spencer also expected to deliver speech on ‘low inflation’

North America

S&P 500 and Nasdaq Futures opened +0.5%

(US) On Saturday, Dec 2nd the US Senate passed the tax reform bill with a final vote of 51 vs 49 (Senator Corker was the only Republican to vote ‘no’)

(US) On Saturday, ABC News suspended reporter Brian Ross for 'erroneous' story related to Michael Flynn (**Note: On Friday, US equities declined amid an ABC News report that Flynn was said to be willing to testify against President Trump)

M&A: Aetna [AET]: Confirmed to be acquired by CVS for $207/shr ($145/shr cash and 0.8378 in CVS shr) for ~$69B

Disney has restarted talks to acquire 21st Century Fox assets; Comcast also talking with Fox – press

Broadcom expected to on Monday disclose its slate to replace Qualcomm’s board – financial press

(US) Thomas Barkin could be named Richmond Fed President as soon as Monday

Europe

(UK) UK Govt: Plenty of discussions still to go on Brexit; meeting between PM May and EU Commission President Juncker is a 'staging post' (**Note: The comments from the UK government come ahead of a meeting between PM May and EU’s Juncker which is expected to be held on Monday.)

(EU) ECB's Villeroy (France): Reiterates recovery in euro area is gaining momentum, current favorable economic winds are 'strong'

(EU) DBRS affirmed EU rating at AAA; stable trend (from Dec 1st)

Levels as of 01:00ET

Nikkei225 -0.4%, Hang Seng +0.5%; Shanghai Composite -0.1%; ASX200 -0.1%, Kospi +0.7%

Equity Futures: S&P500 +0.6%; Nasdaq100 +0.5%, Dax +0.6%; FTSE100 +0.2%

EUR 1.1885-1.1851; JPY 112.98-112.13; AUD 0.7612-0.7587;NZD 0.6890-0.6848

Feb Gold -0.4% at $1,277/oz; Jan Crude Oil -0.7% at $57.97/brl; Mar Copper +0.7% at $3.11/lb

Aussie Trading On A Weaker Footing In The Morning Session

The pair is expected to find support at 0.7560, and a fall through could take it to the next support level of 0.7517. The pair is expected to find its first resistance at 0.7643, and a rise through could take it to the next resistance level of 0.7683.

For the 24 hours to 23:00 GMT, the AUD rose 0.71% against the USD and closed at 0.7612 on Friday.

LME Copper prices declined 0.4% or $27.0/MT to $6734.0/MT. Aluminium prices rose 0.7% or $13.5/MT to $2046.5/MT.

In the Asian session, at GMT0400, the pair is trading at 0.7604, with the AUD trading 0.11% lower against the USD from Friday’s close.

The pair is expected to find support at 0.7560, and a fall through could take it to the next support level of 0.7517. The pair is expected to find its first resistance at 0.7643, and a rise through could take it to the next resistance level of 0.7683.

Moving ahead, market participants would anxiously await the Reserve Bank of Australia’s (RBA) interest rate decision, due tomorrow. Additionally, Australia’s AiG performance of services index for November and retail sales data for October, will also be eyed by traders.

The currency pair is trading above its 20 Hr and 50 Hr moving averages.

Euro-Zone’s Manufacturing Sector Revised Higher To Hit A 17-Year High In November

For the 24 hours to 23:00 GMT, the EUR marginally declined against the USD and closed at 1.1892 on Friday.

In economic news, the Euro-zone's final Markit manufacturing PMI rose to a level of 60.1 in November, up from an earlier estimate that indicated an advance to a level of 60.0 and notching its highest level since April 2000. The PMI had registered a level of 58.5 in the previous month.

Moreover, Germany's final Markit manufacturing PMI advanced to a level of 62.5 in November, confirming the preliminary print. The PMI had recorded a level of 60.6 in the previous month.

The greenback declined against its key counterparts on Friday, after news emerged that former US national security adviser, Michael Flynn, is ready to testify that the US President, Donald Trump directed him to contact Russian officials during the 2016 presidential campaign.

On the macro front, the US ISM manufacturing activity index dropped more-than-anticipated to a level of 58.2 in November, compared to market expectations for a fall to a level of 58.3. The index had registered a level of 58.7 in the prior month. Additionally, the nation's final Markit manufacturing PMI fell less than initially estimated to a level of 53.9 in November, following a reading of 54.6 in the prior month. The preliminary print had recorded a drop to a level of 53.8.

On the other hand, the nation's construction spending grew at its fastest pace in five months, after it climbed more-than-anticipated by 1.4% on a monthly basis in October, amid a surge in public construction outlays. Market participants had expected construction spending to advance 0.5%, compared to a gain of 0.3% in the prior month.

In the Asian session, at GMT0400, the pair is trading at 1.1871, with the EUR trading 0.18% lower against the USD from Friday's close, as the US Dollar gained ground after the US Senate approved a long-awaited tax overhaul over the weekend.

The pair is expected to find support at 1.1835, and a fall through could take it to the next support level of 1.1798. The pair is expected to find its first resistance at 1.1924, and a rise through could take it to the next resistance level of 1.1976.

Going ahead, investors would look forward to the Euro-zone's Sentix investor confidence index for December, due to release in a few hours. Moreover, the US factory orders and final durable goods orders data, both for October, slated to release later in the day, will attract a lot of market attention.

The currency pair is trading below its 20 Hr and 50 Hr moving averages

UK’s Manufacturing Sector Activity Hit Its Highest Level Since August 2013 In November

For the 24 hours to 23:00 GMT, the GBP declined 0.38% against the USD and closed at 1.3470 on Friday, shrugging off robust manufacturing sector data in the UK.

Data indicated that UK's Markit manufacturing PMI unexpectedly advanced to a more than four-year high level of 58.2 in November, confounding market consensus for a fall to a level of 56.5, thus suggesting that manufacturing sector would give a boost to the sluggish British economy in the last quarter of 2017. In the previous month, the PMI had registered a revised level of 56.6.

In the Asian session, at GMT0400, the pair is trading at 1.3472, with the GBP trading slightly higher against the USD from Friday's close.

The pair is expected to find support at 1.3427, and a fall through could take it to the next support level of 1.3383. The pair is expected to find its first resistance at 1.3529, and a rise through could take it to the next resistance level of 1.3587.

Moving ahead, traders would keep a close watch on Britain's Markit construction PMI for November slated to release in a few hours and a meeting between British Prime Minister, Theresa May, EU Chief Executive Jean-Claude Juncker and his Chief Brexit negotiator Michel Barnier.

The currency pair is trading below its 20 Hr and 50 Hr moving averages.

Japanese Yen Trading Lower In The Asian Session

For the 24 hours to 23:00 GMT, the USD declined 0.52% against the JPY and closed at 112.06 on Friday.

In the Asian session, at GMT0400, the pair is trading at 112.75, with the USD trading 0.62% higher against the JPY from Friday’s close.

Overnight data showed that Japan’s monetary base climbed 13.2% on an annual basis in November. In the previous month, monetary base had recorded a rise of 14.5%.

The pair is expected to find support at 111.81, and a fall through could take it to the next support level of 110.86. The pair is expected to find its first resistance at 113.30, and a rise through could take it to the next resistance level of 113.84.

Looking forward, investors would focus on Japan’s Nikkei services PMI for November, scheduled to release overnight.

The currency pair is trading above its 20 Hr and 50 Hr moving averages.

Swiss Franc Reverses Its Gains In The Morning Session

.

For the 24 hours to 23:00 GMT, the USD declined 0.78% against the CHF and closed at 0.9764 on Friday.

In the Asian session, at GMT0400, the pair is trading at 0.9826, with the USD trading 0.63% higher against the CHF from Friday’s close.

The pair is expected to find support at 0.9750, and a fall through could take it to the next support level of 0.9675. The pair is expected to find its first resistance at 0.9886, and a rise through could take it to the next resistance level of 0.9947.

With no major macroeconomic releases in Switzerland today, investor sentiment would be governed by global macroeconomic news.

The currency pair is trading between its 20 Hr and 50 Hr moving averages.

Canadian Unemployment Rate Fell To Its Lowest In Nearly A Decade In November

For the 24 hours to 23:00 GMT, the USD declined 1.54% against the CAD and closed at 1.2698 on Friday.

The Canadian Dollar gained ground against the USD on Friday, after the latest Canadian jobs data painted a bright picture of the nation's labour market.

Canada's unemployment rate declined more-than-expected to 5.9% in November, dropping to a nearly ten-year low level and boosting optimism over the health of the nation's labour market. In the prior month, the unemployment rate had recorded a rate of 6.3%, while investors had envisaged for a fall to 6.2%.

Moreover, the nation's annualised gross domestic product (GDP) sharply slowed to 1.7% in the three months to September, compared to a revised expansion of 4.3% in the prior quarter, as exports tumbled and businesses pulled back on investment. Meanwhile, market participants had anticipated the GDP to slow down to 1.6%.

In the Asian session, at GMT0400, the pair is trading at 1.2715, with the USD trading 0.13% higher against the CAD from Friday's close.

The pair is expected to find support at 1.2635, and a fall through could take it to the next support level of 1.2556. The pair is expected to find its first resistance at 1.2843, and a rise through could take it to the next resistance level of 1.2972.

The currency pair is trading below its 20 Hr and 50 Hr moving averages.

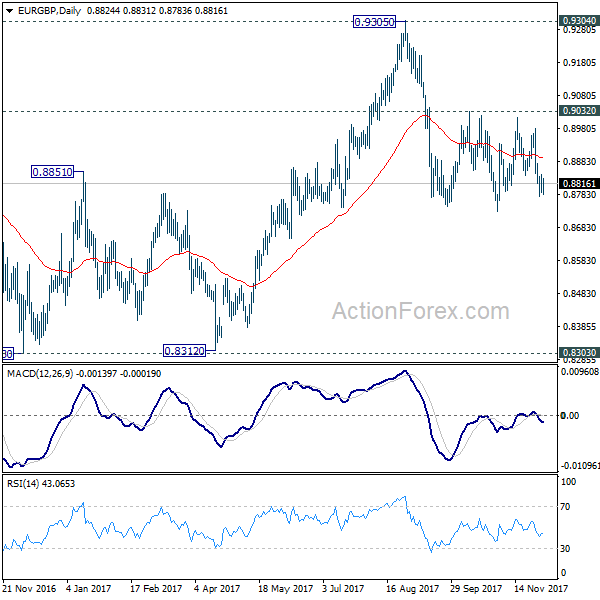

EUR/GBP Daily Outlook

Daily Pivots: (S1) 0.8793; (P) 0.8818; (R1) 0.8848; More...

Intraday bias in EUR/GBP remains neutral as it's bounded in sideway trading between 0.8732/9032 last week. Outlook stays bearish with 0.9032 resistance intact. That is, fall from 0.9305 is expected to resume later. Break of 0.8732 will target 0.8303 key support level. Nonetheless, decisive break of 0.9032 will confirm completion of the decline from 0.9305. In such case, intraday bias will be turned back to the upside for retesting 0.9305 key resistance.

In the bigger picture, there are various ways to interpret price actions from 0.9304 high. But after all, firm break of 0.9304/5 is needed to confirm up trend resumption. Otherwise, range trading will continue with risk of deeper fall. And in that case, EUR/GBP could have a retest on 0.8303. But we'd expect strong support from 0.8116 cluster support (50% retracement of 0.6935 to 0.9304 at 0.8120) to contain downside.

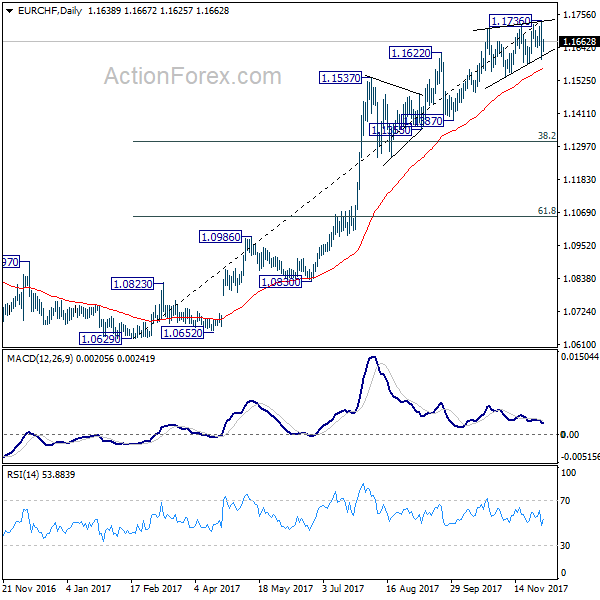

EUR/CHF Daily Outlook

Daily Pivots: (S1) 1.1665; (P) 1.1690; (R1) 1.1731; More...

EUR/CHF rebounds strongly ahead of 1.1584 support. But it's staying well below 1.1736 resistance and intraday bias remains neutral. As noted before, persistent bearish divergence condition in 4 hour MACD and rising wedge like structure suggests that the cross is near to forming a top, if not formed. Hence, even in case of another rise, we'd expect limited upside potential. On the downside, sustained break of 1.1584 support will be a strong sign of trend reversal and should turn outlook bearish for 38.2% retracement of 1.0629 to 1.1736 at 1.1313.

In the bigger picture, while a medium term top could be around the corner, there is no change in the larger outlook. That is, long term rise from SNB spike low back in 2015 is still in progress and would extend. As long as 1.1195 resistance turned support holds, we'll hold on to this bullish view and expect another to prior SNB imposed floor at 1.2000. Though, we'll reassess the outlook if 1.1195 is firmly taken out.