Sample Category Title

USD/CAD Canadian Dollar Higher After Strong Manufacturing Sales

The Canadian dollar appreciated on Thursday after a surprise gain by manufacturing sales. Oil prices continue to be under pressure after the large weekly buildup of US crude stocks reported on Wednesday. NAFTA talks are talking place in Mexico City where the Mexican Economy Minister said he did not agree with the US Commerce Secretary comments that if the US pulled out of the trade agreement it would be devastating for Mexico.

The NAFTA fifth round of talks have entered its second day and for this round the Trade Ministers from the three nations will not be present. They held talks at the APEC Meeting in Vietnam. This could free up the negotiators to move forward in the renegotiation of the Trade agreement with less political interference. Minister might not be present in the sixth round held in Washington.

Petroleum and coal products were behind the lift in Canadian manufacturing sales. The forecast form economists called for a 0.3 percent decline but instead showed a 0.5 gain. The energy industry was the big winner with a 10.3 percent increase in September.

The CAD was higher against the USD despite a report from private payroll processor ADP who published that the Canadian economy lost 5,700 jobs in October. The official figure from Statistics Canada was a gain of 35,300 jobs. While not in exact lockstep both reports share a long term direction and this type of divergence is unusual. The small sample size and other factors lend less credibility to the ADP numbers than the official data, but for now it would remain as something to look for in the next official release.

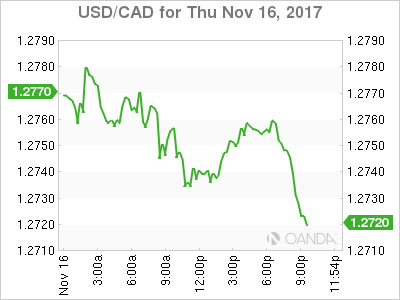

The USD/CAD lost 0.12 percent on Thursday. The currency pair is trading at 1.2749 despite oil losing momentum. The positive manufacturing sales indicator was enough to put the loonie over the US dollar in a day with little data releases on the agenda. Traders will be focused on tomorrow’s inflation numbers out of Ottawa. Canadian consumer price index (CPI) is expected to be almost flat at 0.1 percent. Yesterday Bank of Canada (BoC) Deputy Governor Carolyn Willing said that inflation pressures would be driven by economic growth than the short term swing of energy prices.

Canadian growth has cooled down after an impressive first half of 2017. The BoC hiked twice, once in July and then right way in September but has now turned dovish when talking about further hikes. Inflation is a huge reason why. Low inflation has started to be reported in the monthly indicators and now the central bank is not expected to move until the first quarter of 2018. NAFTA negotiations are a big unknown for Canada, with 75 percent of GDP going south. It would be hard for Canadian Trade Minister to claim that if the US leaves NAFTA it would not be devastated.

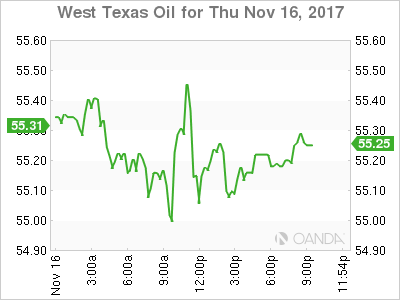

Oil continues its downward slide this week. The price of West Texas Intermediate is trading at $55.06 following strong US weekly crude buildups reported on Wednesday. The Energy Information Administration (EIA) published a rise of 1.9 million barrels. The market was expecting a miss on the forecast after the API reported an overnight rise of 6.5 million barrels. The International Energy Agency has already forecasted that the US energy industry will provide 80 percent of the growth in crude supply in the next 10 years.

The battle between the rise in production in the US and the cut agreement between OPEC and other major producers will continue. The Russian Energy Minister Alexander Novak spoke yesterday to reassure that Russian producers are committed to the agreement to cut output, but he did not mention if they will go ahead with an extension of said agreement. The OPEC and major producers will meet in Vienna on November 30.

Ecuador has stopped its plans to seek an exemption from the OPEC deal after prices have reacted to the group’s production agreement. The small oil producing nation had also floated the idea of leaving the cartel to be able to pump at levels that would make it easier to balance the country’s budget.

Iraqi and Turkish officials are close to reassuming crude exports form the Kurdish region of Kirkuk. The independence referendum was not recognized by Iraq and backed by Turkey it threatened military action. Oil production form the region has not been able to leave for export but those issues are now being worked out between Turkey and the Iraqi government.

Market events to watch this week:

Friday, November 17

8:30am CAD CPI m/m

8:30am USD Building Permits

Gold Edges Higher On Disappointing US Employment, Mfg. Numbers

Gold is trading slightly higher in the Thursday session. In North American trading, the spot price for an ounce of gold is $1279.94, up 0.21% on the day. On the release front, unemployment claims jumped to 249 thousand, well above the estimate of 235 thousand. The Philly Fed Manufacturing Index slipped to 22.7 points, short of the forecast of 24.5 points. On Friday, the focus will be on housing data, with the release of Housing Starts and Building Permits.

Investors are keeping a close eye on Congress, where the House of Representatives votes on tax legislation later on Thursday. With the Democrats fiercely against the bill, the House vote is expected to be very close. This is just the first round, as the Senate is working on its own version of a tax bill. President Trump is pushing hard for the legislation, as he desperately wants the Republicans to pass a major piece of legislation before the end of the year.

There were no surprises from key consumer spending and inflation data on Wednesday. CPI and Core CPI matched the forecasts, with gains of 0.1% and 0.2%, respectively. Consumer spending reports were a mix – retail sales gained 0.1%, shy of the estimate of 0.2%. Core Retail Sales came in at 0.2%, beating the forecast of 0.0%. The Federal Reserve would certainly like to see higher inflation numbers, which remain well below the Fed inflation target of 2.0%. Still, the markets are very bullish on additional rate hikes, as the odds of upcoming rate hikes continues to move higher. Currently, the likelihood of a rate hike in December stands at 96%, and a January raise is priced in at 94%.

Pound Edges Up to 1.32 as UK Retail Sales Rebound

The British pound is slightly higher in the Thursday session. In North American trade, GBP/USD is trading at 1.3199, up 0.21% on the day. On the release front, British Retail Sales gained 0.3%, beating the forecast of 0.1%. US key indicators were a disappointment. Unemployment claims jumped to 249 thousand, well above the estimate of 235 thousand. The Philly Fed Manufacturing Index slipped to 22.7 points, short of the forecast of 24.5 points. On Friday, the focus will be on housing data, with the release of Housing Starts and Building Permits.

There were no surprises from British employment numbers on Wednesday. Wage growth remained steady at 2.2%, but this is well below inflation, which means that the consumer is seeing her purchasing power drop, and weaker consumer spending could hurt the economy. The BoE raised interest rates to 0.50% earlier this week, but this move has yet to push inflation lower. Unemployment is at historical lows, and economists expect the robust labor market to produce higher wages. However, the current situation mirrors what is happening in the US, where an employment market running at capacity has not translated into higher wages for workers.

The Brexit talks are at an impasse, with large gaps between the sides, such as the size of Britain's divorce bill. Britain wants to talk with Europe about a trade deal, but the Europeans are demanding progress on a number of other matters, such as the size of Britain's divorce bill. The British government remains divided on Brexit policy, with senior ministers quarreling over how to handle Britain's departure from the EU, which is scheduled for March, 2019. May hasn't been able present a coherent Brexit policy to the Europeans or to the voters at home, raising doubts as to whether she can deliver the goods on Brexit. Earlier in the week, Brexit Secretary David Davis said he would introduce legislation that would allow MPs to vote on the final Brexit deal, but lawmakers would not be able to amend the legislation.

Dollar Flat as US House Puts Tax Plan to Vote; Pound Steady after Retail Sales Surprise

Major currencies were moving sideways during the European session on Thursday as investors were widely anticipating whether Republicans would pass their tax code in the House of Representatives later today. Economic releases out of the Eurozone, the US, the UK, and Canada were also in focus but had a moderate impact on the markets.

The US lawmakers were preparing for a crucial vote on tax reforms in the House of Representatives on Thursday after 1830GMT, with Republicans feeling confident that their tax version would gather enough votes. The biggest threat, though, comes from the Senate, with two Republicans expressing misgivings about the Senate version yesterday and therefore raising fears that the tax overhaul will fail to be approved before the end of the year as Trump's team desires.

Looking at today's US economic reports, initial jobless claims increased by 249,000 in the week ending November 11, exceeding the forecast of 235,000 and the 239,000 seen previously. This drove the four-week average measure, which is considered less volatile, up by 6,500 to 237,500. The Philadelphia Fed manufacturing index also disappointed traders, falling by 5.2 points to 22.7, below the forecast of 25.

The dollar index was in a range during the session at 93.85. Dollar/yen pared earlier gains, retreating to 112.84. Dollar/swissie jumped by 0.44% on the day to 0.9924.

In Eurozone, final figures on inflation matched flash estimates with headline CPI increasing steadily by 1.4% y/y in October but slowing down by 0.3 percentage points to 0.1% m/m. The core equivalent though, which excludes fuel and energy prices, surpassed expectations, growing by 1.1% y/y, above the forecast of 0.9%, while the monthly core measure declined by 0.1% after rising by 0.4% in September. Euro traders didn't react much to the data. On the day, the currency extended its downtrend relative to the dollar to reach 1.1776 as coalition talks in Germany to form a government led nowhere so far ahead of a deadline set by the chancellor Angela Merkel for the end of the week. Should the parties fail to come to an agreement, Germany would be forced to go through elections once again, potentially eroding confidence in Merkel's Conservative party and strengthening the far-right ADP.

Data on retail sales out of the UK caused moderate movements in the markets as investors were more concerned about the Brexit talks, which so far offer little clarity to business leaders as regards Britain's future relationship with the EU. UK retail sales fell for the first time since March 2013, retreating by 0.3% y/y in October, while analysts had forecasted a bigger decline of 0.6%. September's growth of 1.2% was also slightly revised up to 1.3%. Excluding automobiles and fuel, the gauge retreated by 0.3% after four-years of rising but with at a slower pace than analysts anticipated (-0.4%). The pound rebounded from a low of $1.3194 prior the data to $1.3195. Euro/pound was down by 0.27% at 0.8926.

Speaking in Liverpool in front of business leaders and students, the BOE Governor Mark Carney said that the central bank would alter monetary policy in a way to bring inflation back to the target whatever the outcome of Brexit negotiations is. Moreover, he highlighted the importance of the Brexit deal as well as the date of the implementation.

Elsewhere, stronger-than-expected manufacturing sales in Canada helped the loonie gain ground against the greenback, pushing dollar/loonie down to 1.2743 (-0.13%).

Turning to commodities, gold stood flat at $1,279.70 per ounce during the session. WTI crude inched down by 0.11% to $55.27 per barrel and Brent retreated by 0.23% to $61.73.

Intra-day Views on Gold and USD Index

Good day traders! Today's article is about gold and usd index.

Gold is moving nicely higher, now in red subwave b) which seems to be running into some short-term Fib. resistance level that may limit current intraday rally against the yesterdays sell-off which was very strong, so we assume that bears will remain on the stronger side.

Gold, 1H

USD Index is trading in a three-wave bearish decline. We see price trading in the middle of a corrective wave iv, that can search for limited upside near the Fibonacci ratio of 50.0 and make a new drop lower.

USD Index, 1H

Loonie Strengthens on Positive Data but Advance was So Far Limited

The pair eased on Thursday, remaining under for-day rally's high at 1.2789, as loonies got boosted by better than expected Canadian data which offset negative impact from lower oil prices. Today's dip to 1.2742 was contained by falling daily Tenkan-sen which marks pivotal support and sustained break lower would weaken near-term structure and risk deeper correction of 1.2665/1.2789 upleg.

Daily techs are giving mixed signals and require break below Tenkan-sen for bearish scenario (extension towards next pivot at 1.2700 zone or bounce above 1.2789 to generate bullish signal). Meantime, dip-buying remains favored near-term scenario while dips are limited by Tenkan-sen line.

Res: 1.2777; 1.2789; 1.2819; 1.2835

Sup: 1.2742; 1.2712; 1.2695; 1.2665

USD Gains Positions on Optimism of Tax Reforms Passing

The EUR/USD is falling against the US dollar due to rising interest in risky assets ahead of voting on tax reform in the US. Doubts about the ability to pass the law on tax cuts were the basis for the recent price appreciation of the EUR/USD. USD bulls were supported by strong macro data released today which showed that industrial production in the US increased by 0.9% in October against the 0.5% forecasted. The consumer price index for the Eurozone remained at 0.9% and had little impact on traders. Tomorrow, at the center of attention will be housing market data - the construction sector is key for the US economy.

The GBP/USD continued positive dynamics after the publication of positive news on British retail sales that grew by 0.3%, which by 0.2% better than forecasted. The growth potential of the British pound is limited due to fears linked to the outcome of the Brexit talks between the UK and the European Union.

The aussie quotes are consolidating today after controversial labour market statistics were published. Unemployment reduced to 5.4% in October, which is 0.1% better than expected, but employment has grown by only 3,700 against the 17,800 forecasted.

Among important events today investors should pay attention to the business NZ PMI and producer price index in New Zealand at 21:45 GMT.

EUR/USD

The EUR/USD price is falling today after it was not able to fix above 1.1825. Within the current descending correction, the quotes may return to the support at 1.1730 and the upper boundary of the channel which it had left earlier. In order to resume positive dynamics, quotes need to overcome the SMA100 on the 15-minute chart and the local high near 1.1800.

GBP/USD

The GBP/USD demonstrated positive dynamics today and reached the upper limit of the rising channel. Fixing beyond the limits of the channel may become a trigger for continued increases to 1.3250 and 1.3400. In case of opening short positions with potential goals near 1.3050, the stop should be set above 1.3230.

AUD/USD

The AUD/USD is consolidating under the support at 0.7600. Currently, quotes approached the upper limit of the descending channel and its breaking and gaining a foothold above 0.7600 may become a signal to buy, with potential targets at 0.7635 and 0.7700. On the other hand, we do not exclude the fall resuming with the first target at 0.7565.

Yen Subdued Despite Soft US Jobs, Mfg. Numbers

The yen has improved is showing little movement in the Thursday session. In North American trade, USD/JPY is trading at 112.90, up 0.02% on the day. On the release front, there are no Japanese events on the schedule. In the US, key indicators missed expectations. Unemployment claims jumped to 249 thousand, well above the estimate of 235 thousand. The Philly Fed Manufacturing Index slipped to 22.7 points, short of the forecast of 24.5 points. On Friday, the focus will be on housing data, with the release of Housing Starts and Building Permits.

There were no surprises from key consumer spending and inflation data on Wednesday. CPI and Core CPI matched the forecasts, with gains of 0.1% and 0.2%, respectively. Consumer spending reports were a mix – retail sales gained 0.1%, shy of the estimate of 0.2%. Core Retail Sales came in at 0.2%, beating the forecast of 0.0%. The Federal Reserve would certainly like to see higher inflation numbers, which remain well below the Fed inflation target of 2.0%. Still, the markets are very bullish on additional rate hikes, as the odds of upcoming rate hikes continues to move higher. Currently, the likelihood of a rate hike in December stands at 96%, and a January raise is priced in at 94%.

Japan recorded another quarter of growth in Q3, marking the longest economic expansion since 2001. However, Preliminary GDP came in at 0.3%, weaker than the 0.6% gain in Final GDP for the second quarter. The economy has improved in 2017, but this has not translated into higher inflation levels. Inflation remains persistently below the inflation target of around 2 percent, but the Bank of Japan has no plans to change policy. Earlier in the week, BoJ Governor Haruhiko Kuroda acknowledged the inflation issue, saying "it is not easy to quickly dispel the deflationary mindset that has formed over the course of 15 years of deflation." Kuroda added that he expects inflation levels to rise, but in the meantime the BoJ would continue its massive monetary easing, a key component of the "Abenomics" program.

Canadian September Manufacturing Sales Rise for a Second Consecutive Month

Highlights:

- The nominal value of manufacturing sales rose a stronger-than-expected 0.5% that built further onto the 1.4% increase in August that was revised down slightly from the previously reported 1.6% gain.

- The overall increase was helped by a 10.3% increase in the petroleum and coal component along with a 1.9% gain in machinery that more than offset a 0.7% drop in the transportation equipment component.

Our Take:

Though today's report showed a stronger-than-expected rise in manufacturing sales, it also indicated that once again part of the demand was met from existing stocks rather than new production with inventories dropping 0.7% after the 0.2% decline in August. As a result, we are assuming that the manufacturing component of September GDP will rise a more moderate 0.2%. However, this increase along with similar-sized gains among most services categories will provide an offset to expected flat mining and utilities components that is expected to result in overall monthly GDP returning to positive growth in September rising 0.1% after August's disappointing 0.1% drop. Beyond September a rebuilding of inventories is expected to help keep activity rising. Sustained positive growth is expected to eventually return the Bank of Canada to tightening mode though not until Q2 of next year.

Dollar Off Recent Lows, But Gain Still Far from Impressive

- European equities gain up to 1% today, rebounding following a 7 day sell-off. US stock markets opened around 0.5% higher.

- ECB Executive Board member Mersch said in an interview with CNBC that financial markets wouldn't be right to expect another extension of asset purchases after September.

- UK retail sales fell for the first time since March 2013 in the 12 months to October (-0.3%), but the figures were still stronger than economists had forecast. The M/M statistics look brighter: total volumes rose 0.3%, or 0.1% excluding the volatile automotive fuel component. That beat expectations for a rise of 0.1% and no change, respectively.

- A Brexit transition deal is in everyone's interest but the Bank of England will support the economy no matter what the result of the negotiations, BoE Governor Carney said in an ITV television interview.

- The Republican-controlled US Congress was approaching a major test later today of its ability to overhaul the federal tax code, as lawmakers prepared for their first full-scale vote on sweeping tax legislation.

- The number of Americans filing for unemployment benefits unexpectedly rose last week to 249k in part as a backlog of applications from Puerto Rico continued to be processed, but the underlying trend pointed to tightening labor market conditions. The Philly Fed Business outlook declined more than forecast, from 27.9 to 22.7 (vs 24.6 expected). Industrial production rose a strong 0.9% M/M in October, beating 0.5% M/M forecast.

Rates

Bonds lose slightly ground as risk sentiment improves

Global core bonds lost ground during Asian trading and in the first half of European dealings as risk sentiment improves. Following a 7-day sell-off and a test of key support in eg the German Dax, stocks found their composure and rebounded. Positive risk sentiment weighted on the US Note future and the Bund. The equity rally stalled around European noon, putting a bottom below core bonds. The German Bund even started outperforming the US Note future, erasing most of the intraday losses. US eco data printed mixed, but once again failed to move markets. ECB Mersch said that markets shouldn't anticipate APP to be extended beyond September 2018, clearing a misunderstanding which originated at Draghi's press conference after the October meeting. ECB Praet was dovish as usual. The US House is expected to vote on its tax reform proposal a first time tonight which remains a wildcard.

At the time of writing, the US yield curve shifts 2.1 bps (2-yr) to 2.7 bps (30-yr) higher, slightly bear steepening the curve (hopes on tax reforms?!). Changes on the German yield curve range between -0.8 bps (30-yr) and +0.4 bps (2-yr). On intra-EMU bond markets, 10-yr yield spread changes versus Germany range between -1 bp and +1 bp with Greece underperforming (+11 bps).

The French treasury held a small OAT auction by tapping two off the run (€ 1.02 bn 3.5% Apr2020 & €1.46 bn 0.5% May2025) and one on the run (€2.52 bn 0% Mar2023) bond. The amount sold was the upper bound of the indicative €4-5 bn range. Demand was very strong, resulting in an auction bid cover of 2.72. Additionally, the French treasury raided €2 bn via inflation-linked notes.. The Spanish debt agency sold 4 on the run bonds (€1.02 bn 0.05% Jan2021, €0.97 bn 0.45% Oct2022, €1.24 bn 1.45% Oct2027 and €1.43 bn 3.45% Jul2066). The combined amount sold (€4.65 bn) was in the upper half of the €4-5 bn target range with good auction bid cover of 1.92.

Currencies

Dollar off recent lows, but gain still far from impressive

An improvement in global risk sentiment and a rise in core yields supported a modest USD rebound, confirming yesterday's intraday trend-reversal. (US) data were mixed and had no significant impact on trading. EUR/USD trades in the 1.1775 area. USD/JPY changes hands near 113. The dollar trades off yesterday's lows, but the US currency has still a quite a long way to go to reverse the losses it occurred since the middle of last week.

Asian risk sentiment improved this morning as the downward correction of the previous days lost momentum. Most regional equity indices showed moderate gains with Japan outperforming. USD/JPY tried to regain the 113 level. EUR/USD was little changed from yesterday's close and traded in the high 1.17 area.

European equity indices joined the risk-on correction from Asia. Core yields rose and, contrary to what was often the case of late, US Treasuries underperform Bunds, (slightly) widening the interest rate differential in favour of the dollar. EUR/USD drifted to the 1.1760 area. USD/JPY gained a few more ticks north of 113. The dollar was in better shape compared to earlier this week, but the gains remained modest given the recent setback. ECB Praet defended the gradual ECB policy approach despite solid EMU growth. There was no noticeable negative impact on the euro. The early morning US data (import prices; Philly Fed and claims) were slightly below consensus, but the rise in the jobless claims may be partly due to statistical issues (Veterans day). Still the dollar lost a few ticks. Later in the session, the US production data were very strong, but again with little (positive) impact on the dollar. The US House and the Senate are developing parallel proposals on US tax reform, but it remains uncertain whether they will lead to a workable combined result in the end. EUR/USD trades currently in the 1.1775 area. USD/JPY trades near 113.

EUR/GBP 0.90+ test rejected

EUR/GBP traded off yesterday's top early in Europe. The pair hovered in the mid 0.89 area going into the publication of the October UK retail sales. The UK currency was supported by the better overall risk sentiment. Yesterday's potential trend reversal signal in EUR/GBP (and in EUR/USD) also weighed on the euro cross rates today. The UK retail sales were marginally stronger than expected at 0.3% M/M. Still, the series printed the first negative Y/Y reading since 2013 (-0.3%). EUR/GBP initially hardly reacted to the report, but sterling finally gained slightly further ground, especially against the euro. Some press headlines indicating that UK and EU (German) politicians acknowledge the need for an orderly, well-organised Brexit may have been slightly supportive for sterling. Investors don't want to be positioned aggressively sterling short as more constructive Brexit news remains possible. EUR/GBP trades currently in the 0.8920/25 area. The topside test looks rejected for now. Cable (1.3190 area) holds with the sideways consolidation pattern.