Sample Category Title

US Stocks Surged as Tax Bill Passed in House and Senate Finance Committee, Dollar Stays Soft

The US markets responded positively to the passage of the tax bill in House and in Senate Finance Committee. DOW jumped 187.08 pts, or 0.8% to close at 23458.36. Technically, it defended 23251.1 key near term support and maintained bullishness. Focus is back on historical high at 23602.1. NASDAQ has indeed made new record at 6806.67 before closing at 6793.29, up 1.3%. 10 year yield also showed some resilience and ended up 0.026 at 2.361, keeping itself well above 2.304 key support. In the currency markets, Dollar remains generally soft, though, except versus Aussie and Kiwi. Euro and Yen would probably end the week as the strongest ones.

House passed tax bill by 227-205

The House passed its version of tax reform bill with a 227-205 vote. The outcome had been widely anticipated as Republicans control 240 out of 435 seats there. Despite the passage of the bill, there were 13 Republicans who did not vote for the bill. Many of them defected as they were dissatisfaction with the elimination of some tax deduction. The House bill eliminates the deduction for state and local income taxes, but preserves the deduction for property tax up to US$ 10k. Yet, the partial preservation was not sufficient for the policymakers from high-tax states such as New York and New Jersey, and California and North Carolina.

Senate Finance Committee passed tax bill by 14-12

The House is presumably the easier hurdle for the tax reform bill. The next is the Senate. The Senate Finance Committee also approved the their version of tax bill yesterday, with 14-12 vote. The bill is expected to be considered on floor the week after Thanksgiving. Given the slim majority of Republicans in the senate, there is little margin for error. They could only afford to see two defections, one filled up by Ron Johnson already. Susan Collins has also expressed some concerns. Meanwhile, it should also be noted that there are some major differences between the House's version and the Senate's version. And the reconciliation effort is huge.

San Francisco Fed Williams urged monetary policy rethink

San Francisco Fed President John Williams continued his push for rethinking global monetary policies. He noted that the major economies of the world are all facing slower growth and lowest interest rates. And there is a need to expand to toolkits to prepare for the time when stimulus is needed. He said that "we will all be better able to contain the next economic recession if we develop approaches that succeed even when many countries are simultaneously constrained by the lower bound." Interest rate was the traditional convention tool. Then there were asset purchases and forward guidance, widely used in recent recession. Some countries adopted negative interest rates. And Williams also tried to push so called price-level targeting and also nominal-income targeting. He said that "each of these alternatives has significant advantages and disadvantages, which need further careful study and discussion."

Regarding the current situation, Williams support another hike in December. He said that "my view is that a perfectly reasonable path for policy would be one more increase this year, and three next year."

Dallas Fed Kaplan "very open-minded" about December hike

Dallas Fed President Robert Kaplan said his is "very open-minded" about "considering taking a next step in removing accommodation at upcoming meetings." He pointed out that unemployment at 4.1% is expected to fall further in a "deviation" from Fed's full employment mandate. And, "if the deviation on the full employment gets big enough that would be, for me, enough of reason to still remove accommodation, take another step." And, "prudent risk management means some action to remove accommodation gradually and patiently". He also emphasized that "it's not that you have see you are meeting both, then you move", regarding Fed's dual price and employment mandate.

ECB Villeroy de Galhau: Follow the path of gradual normalization

ECB Governing Council member Francois Villeroy de Galhau said that "we will clearly follow this path of gradual normalization, with caution but combining the whole range of our instruments - and there shouldn't be excessive focus on the net purchases of assets." He added that "monetary policy cannot be the only game in town, and therefore we should not overburden it,"

UK Brexit Secretary Davis: Incredibility unlikely for no-deal Brexit

UK Brexit Secretary David Davis said that it's "incredibly unlikely" there will be a no-deal Brexit. And he hopes that the next round of negotiation with EU will start before Christmas. But he also warned not to "politics above prosperity" in the post Brexit relationship with EU. Davis would want to seek a "deep and comprehensive free trade agreement" with EU. And continue "continued close cooperation in highly regulated areas such as transport, energy and data".

On the data front

New Zealand business manufacturing index dropped to 57.2 in October. PPI input rose 1.0% qoq in Q3, PPI output rose 1.0% qoq too. Eurozone current account is the only feature in European session. Canada will release CPI while US will release housing starts later in the day.

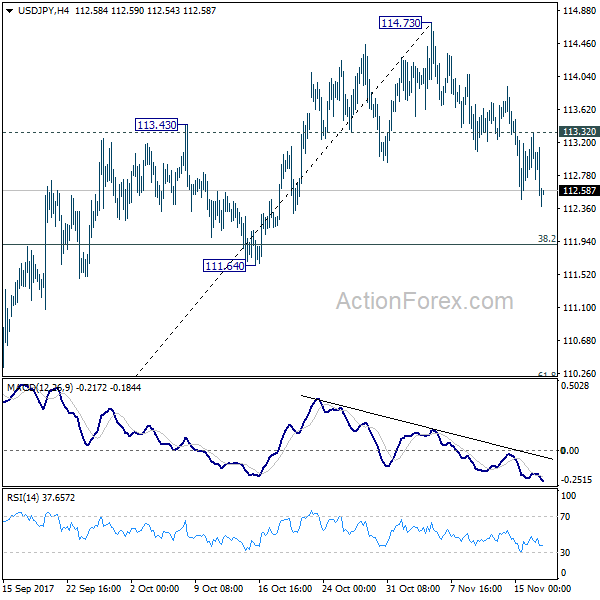

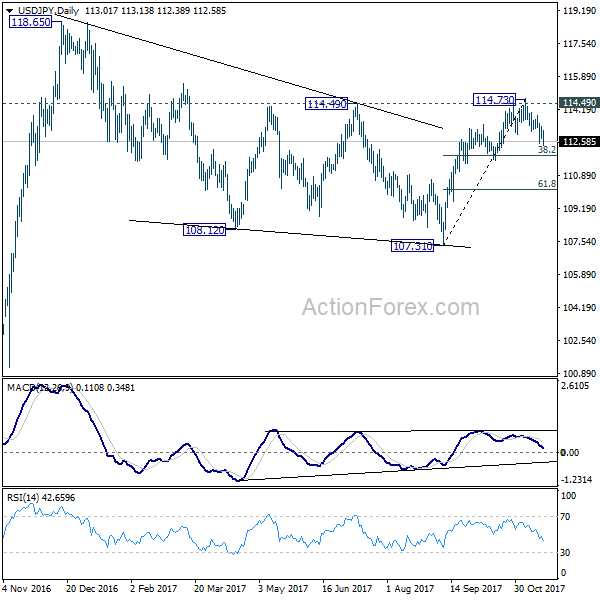

USD/JPY Daily Outlook

Daily Pivots: (S1) 112.75; (P) 113.03; (R1) 113.34; More...

USD/JPY's fall from 114.73 continues today and intraday bias stays on the downside for 38.2% retracement of 107.31 to 114.73 at 111.89 first. Sustained break of 111.64 support will now argue that rise from 107.31 has completed. In that case, USD/JPY should target 61.8% retracement at 101.14. On the upside, break of 113.32 minor resistance is needed to confirm completion of the fall. Otherwise, near term outlook will now stay cautiously bearish.

In the bigger picture, medium term rise from 98.97 (2016 low) is not completed yet. It should resume after corrective fall from 118.65 completes. Break of 114.49 resistance will likely resume the rise to 61.8% projection of 98.97 to 118.65 from 107.31 at 119.47 first. Firm break there will pave the way to 100% projection at 126.99. This will be the key level to decide whether long term up trend is resuming. However, firm break of 111.64 support will dampen this view and turn focus back to 107.31 instead.

Economic Indicators Update

| GMT | Ccy | Events | Actual | Forecast | Previous | Revised |

|---|---|---|---|---|---|---|

| 21:30 | NZD | Business NZ Manufacturing PMI Oct | 57.2 | 57.5 | 57.6 | |

| 21:45 | NZD | PPI Input Q/Q Q3 | 1.00% | 1.20% | 1.40% | |

| 21:45 | NZD | PPI Output Q/Q Q3 | 1.00% | 1.40% | 1.30% | |

| 9:00 | EUR | Eurozone Current Account (EUR) Sep | 30.2B | 33.3B | ||

| 13:30 | CAD | CPI M/M Oct | 0.10% | 0.20% | ||

| 13:30 | CAD | CPI Y/Y Oct | 1.40% | 1.60% | ||

| 13:30 | CAD | CPI Core - Common Y/Y Oct | 1.50% | |||

| 13:30 | CAD | CPI Core - Trim Y/Y Oct | 1.50% | |||

| 13:30 | CAD | CPI Core - Median Y/Y Oct | 1.80% | |||

| 13:30 | USD | Housing Starts Oct | 1.19M | 1.13M | ||

| 13:30 | USD | Building Permits Oct | 1.25M | 1.23M |

Aussie Trading A Tad Higher In The Asian Session

For the 24 hours to 23:00 GMT, the AUD slightly declined against the USD and closed at 0.7586.

LME Copper prices rose 0.7% or $48.5/MT to $6764.0/MT. Aluminium prices rose 1.2% or $24.0/MT to $2106.0/MT.

In the Asian session, at GMT0400, the pair is trading at 0.7588, with the AUD trading marginally higher against the USD from yesterday’s close.

The pair is expected to find support at 0.7577, and a fall through could take it to the next support level of 0.7565. The pair is expected to find its first resistance at 0.7604, and a rise through could take it to the next resistance level of 0.7619.

Next week, market participants would eye a speech by the Reserve Bank of Australia’s (RBA) Governor, Philip Lowe, along with the minutes of the latest RBA monetary policy meeting, both due next week.

The currency pair is showing convergence with its 20 Hr and 50 Hr moving averages.

Euro Trading On A Stronger Footing, Ahead Of ECB President’s Speech

For the 24 hours to 23:00 GMT, the EUR slightly declined against the USD and closed at 1.1772.

On the macro front, the Euro-zone's final consumer price index (CPI) climbed 1.4% on an annual basis in October, confirming the preliminary print and pointing to subdued inflationary pressures in the common currency region. The CPI had risen 1.5% in the previous month.

The greenback advanced against most of its major counterparts, after the US House of Representatives approved its version of tax reform proposals that includes $1.5 trillion in tax cuts for businesses and individuals.

On the data front, industrial production in the US jumped more-than-expected by 0.9% on a monthly basis in October, advancing by the most since April 2017, as factory activity recovered from the impact of Hurricanes Harvey and Irma. Market had expected industrial production to rise 0.5%, after recording a revised gain of 0.4% in the previous month. Further, the nation's manufacturing production rose 1.3% MoM in October, topping market consensus for an increase of 0.6% and following a revised rise of 0.4% in the prior month. Additionally, the nation's NAHB housing market index unexpectedly advanced to a level of 70.0 in November, hitting its highest level in eight months and confounding market expectations for a fall to a level of 67.0. In the prior month, the index had registered a reading of 68.0.

On the contrary, the number of Americans filing for fresh jobless claims unexpectedly rose to a 6-week high level of 249.0K in the week ended 11 November, against market anticipations for a drop to a level of 235.0K. Initial jobless claims had recorded a level of 239.0K in the previous week. Moreover, the nation's Philadelphia Fed manufacturing index fell to a level of 22.7 in November, higher than market expectations for a drop to a level of 24.6. The index had registered a reading of 27.9 in the prior month.

In the Asian session, at GMT0400, the pair is trading at 1.1809, with the EUR trading 0.31% higher against the USD from yesterday's close, as the greenback declined, on reports that investigators into possible Russian interference in the US presidential election issued a subpoena to campaign officials last month for documents.

The pair is expected to find support at 1.1770, and a fall through could take it to the next support level of 1.1731. The pair is expected to find its first resistance at 1.1835, and a rise through could take it to the next resistance level of 1.1861.

Going ahead, a speech by the European Central Bank (ECB) President, Mario Draghi, scheduled in a few hours, will attract significant amount of market attention. Additionally, the US housing starts and building permits data both for October, slated to release later in the day, will be on investors' radar.

The currency pair is trading above its 20 Hr and 50 Hr moving averages.

UK’s Retail Sales Sharply Rebounded In October

For the 24 hours to 23:00 GMT, the GBP rose 0.18% against the USD and closed at 1.3193, on the back of better-than-expected UK retail sales data.

Data showed that Britain's retail sales rebounded more-than-expected by 0.3% on a monthly basis in October, suggesting that consumer spending is likely to propel economic growth in the final quarter of 2017. In the prior month, retail sales had recorded a revised drop of 0.7%, while investors had envisaged for a rise of 0.2%.

Separately, the Bank of England (BoE) Governor, Mark Carney reassured that the central bank will probably need to hike interest rates a couple more times over the next few years, provided the British economy improves as expected. Further, Carney vowed that the central bank will do whatever it can to support the economy in the event of any Brexit shock and would remain “nimble enough” to control inflation.

In the Asian session, at GMT0400, the pair is trading at 1.3235, with the GBP trading 0.32% higher against the USD from yesterday's close.

The pair is expected to find support at 1.3165, and a fall through could take it to the next support level of 1.3096. The pair is expected to find its first resistance at 1.3274, and a rise through could take it to the next resistance level of 1.3314.

Amid no major macroeconomic releases in the UK today, investors would look forward to the release of second estimate of UK's 3Q GDP, scheduled next week.

The currency pair is trading above its 20 Hr and 50 Hr moving averages.

Japanese Yen Trading On A Stronger Footing This Morning

For the 24 hours to 23:00 GMT, the USD rose 0.22% against the JPY and closed at 113.11.

In economic news, Japan’s final machine tool orders rose 49.8% YoY in October, slightly less than the preliminary print indicating an advance of 49.9%. Machine tool orders had registered a rise of 45.00% in the previous month.

In the Asian session, at GMT0400, the pair is trading at 112.52, with the USD trading 0.52% lower against the JPY from yesterday’s close.

The pair is expected to find support at 112.17, and a fall through could take it to the next support level of 111.82. The pair is expected to find its first resistance at 113.10, and a rise through could take it to the next resistance level of 113.68.

Moving ahead, traders will direct their attention to Japan’s flash Nikkei manufacturing PMI, all industry activity index and adjusted merchandise trade balance data, all due to be released next week.

The currency pair is trading below its 20 Hr and 50 Hr moving averages.

Swiss Franc Reverses Its Losses In The Morning Session

For the 24 hours to 23:00 GMT, the USD rose 0.48% against the CHF and closed at 0.9940.

In the Asian session, at GMT0400, the pair is trading at 0.9917, with the USD trading 0.23% lower against the CHF from yesterday’s close.

The pair is expected to find support at 0.9888, and a fall through could take it to the next support level of 0.9858. The pair is expected to find its first resistance at 0.9946, and a rise through could take it to the next resistance level of 0.9974.

Moving ahead, market participants await a speech by the Swiss National Bank President, Thomas Jordan along with the release of Switzerland’s trade balance figures, both scheduled next week.

The currency pair is trading between its 20 Hr and 50 Hr moving averages.

Canada’s Manufacturing Shipments Surprisingly Grew In September

For the 24 hours to 23:00 GMT, the USD declined 0.11% against the CAD and closed at 1.2754.

Macroeconomic data revealed that Canada's manufacturing shipments unexpectedly advanced 0.5% on a monthly basis in September, defying market expectations for a fall of 0.5%. In the previous month, manufacturing shipments had recorded a revised rise of 1.4%.

In the Asian session, at GMT0400, the pair is trading at 1.2726, with the USD trading 0.22% lower against the CAD from yesterday's close.

The pair is expected to find support at 1.2699, and a fall through could take it to the next support level of 1.2671. The pair is expected to find its first resistance at 1.2769, and a rise through could take it to the next resistance level of 1.2811.

This afternoon will bring a crucial Canadian release, namely the consumer price inflation data for October.

The currency pair is trading below its 20 Hr and 50 Hr moving averages.

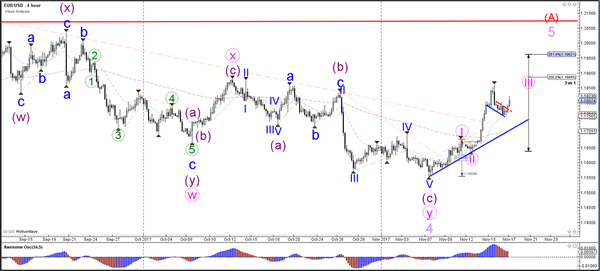

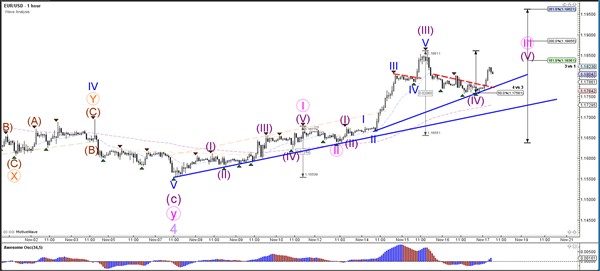

Daily Wave Analysis: EUR/USD Bullish Bounce At 50% Fibonacci And 1.1750 Support

Currency pair EUR/USD

EUR/USD retraced back to and bounced at the 1.1750 support level. Price then broke above the resistance trend line (dotted red) and therefore could be extending the wave 3 (pink).

The EUR/USD bounced at the 50% Fibonacci level of wave 4 (purple). There could be a wave 5 (purple) continuation as long as price stays above the support trend line (blue).

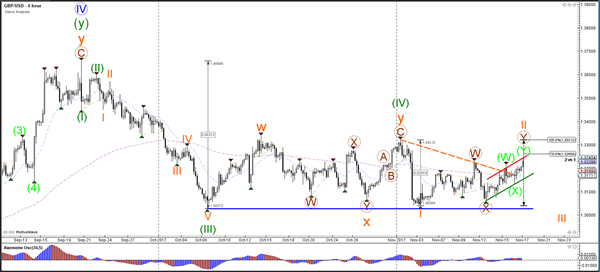

Currency pair GBP/USD

The GBP/USD broke above the resistance (dotted orange) trend line and moved up to retest the higher Fibonacci level at 1.3260. A breakout above the top (100% Fib) or below the support trend line (green) is needed before a larger directional move can be expected.

The GBP/USD has expanded the choppy correction via a complex correction of WXY (green) and price has now reached the top of the channel (red), which could create a bearish bounce back to test the bottom of the channel.

Currency pair USD/JPY

The USD/JPY's is moving lower as part of wave 2 or wave B (light purple). The 38.2% Fibonacci support level could be the next target of the bearish price action at 111.83.

The USD/JPY completed an ABC (blue) within wave B (blue) and broke below support (dotted blue) to continue with wave C (blue). Price is now building a falling wedge chart pattern (green/red lines). Price will need to break below support if it is able to accelerate the downtrend.

Elliott Wave View: SPX

SPX Short-Term Elliott Wave view suggests that the rally to 2597.02 ended Intermediate wave (3). Intermediate wave (4) pullback ended at 2557.45 as a double three Elliott Wave structure. Down from 2597.02, Minor wave W of (4) ended at 2566.33, Minor wave X of (4) ended at 2587.66, and Minor wave Y of (4) ended at 2557.45. Up from there, the rally appears to be unfolding as an impulse Elliott Wave structure. Minute wave ((i)) ended at 2572.84, Minute wave ((ii)) ended at 2563.3, and Minute wave ((iii)) ended at 2590.09. Expect Index to see another leg higher in Minute wave ((iv)) of 1 before ending cycle from 11/15 low. Afterwards, Index should pullback in Minor wave 2 to correct cycle from 11/15 low in 3, 7, or 11 swing before the rally resumes. A break above Intermediate wave (3) at 2597.02 will add conviction that Intermediate wave (4) has ended at 2566.3. We don’t like selling the Index.

SPX 1 Hour Elliott Wave Analysis

Will The NZD Continue To Consolidate Or Will It Break Higher?

Key Points:

- Price action forming a wedge pattern.

- RSI Oscillator continuing to rise within neutral territory.

- Watch for a move towards the supply zone within the coming week.

The New Zealand Dollar has been under siege of late as a range of political upsets have seen the pair facing a steady wave of depreciation. Subsequently, price action has tumbled from around the 70 cent handle, in late October, all the way to its present level at 0.6861. However, the question remains if the pair will continue to decline over the next few weeks as the New Zealand Labour Party continues to showcase their new social and economic policies.

Thankfully, the answer to the above question lays in the technical aspects of the pair’s chart with price action having formed some interesting patterns over the last few days. In fact, looking at the 4-hour timeframe shows a relatively clear low as having been formed on the 27th. Subsequently, the NZDUSD has been slowly creeping its way higher over this period and the lows are now starting to get higher.

Additionally, there is a relatively clear descending wedge formation on the 4-hour timeframe which would seem to suggest that we might have recently seen the full extent of the bearish push. In fact, the RSI Oscillator largely backs this view with the indicator steadily moving higher, within neutral territory, suggestive of further upside action to come.

Subsequently, the most likely scenario for the coming week is for price action to decline back towards the bottom of the wedge pattern, before commencing a sharp move towards the supply zone around the 0.6870 mark. At this level, a consolidation or reversal is equally likely and all will be off. However, any challenge to this level could see a solid bid form which would take the pair towards the top of the wedge.

Ultimately, the full extent of the shock of a labour party win appears to have run its course and the NZD’s valuation is expected to stabilise itself over the next few days. Subsequently, don’t expect too much negativity, at least in the short term, from the 'left wing labour' factor.