Sample Category Title

Markets Poised for a Dovish Rate Hike by Bank of England

The pound has been on an uptrend for much of 2017, led by a weaker dollar in the first half and by expectations of a UK rate rise in the second half. Its high of the year and post Brexit peak of $1.3656 was reached soon after the Bank of England's September policy meeting when MPC members signalled "some withdrawal of monetary stimulus is likely to be appropriate over the coming months".

However, recent communication by some policymakers has been not as hawkish, if not dovish, casting doubt about the Bank's intentions. The BoE's newest deputy governor, Dave Ramsden, recently said he was not part of the majority who in September saw a case for tightening policy soon. Another deputy governor, Jon Cunliffe, said the timing of a rate hike was an "open question". Meanwhile, Governor Mark Carney hasn't disappointed in living up to his reputation of flip flopping on policy, changing his tone from a hawkish one to a more cautious one at a recent hearing before Parliament's Treasury Select Committee.

The mixed signals from the British central bank have led investors to pare back their expectations of UK interest rate increases, pushing sterling to the $1.30-1.33 region from a brief spell above $1.36. Although most analysts are still predicting the BoE will raise rates for the first time in a decade by 0.25% to 0.50% on November 2, expectations for subsequent rate hikes have fallen to just one quarter percentage point increase in 2018.

A possible split vote on Thursday could diminish the odds of any follow-up move. Consensus forecasts are for a 6-3 vote in favour for a hike. A 5-4 vote would be viewed as very dovish and could send the pound lower to retest the $1.30 level, while a 7-2 vote could trigger a fresh rally, driving sterling back above $1.34.

In addition to the rate decision, the Bank's quarterly inflation report should also shed some light on future policy. Carney has said he expects inflation to rise further in the coming months above September's 3.0% level. A sharp upward revision to the inflation outlook would fuel expectations of more policy tightening in the coming months. The growth forecasts will also be watched closely following the surprise beat of third quarter GDP growth. The GDP figures may have helped ease the concerns of some MPC members that the UK economy is not strong enough to support higher rates.

However, even with more optimistic projections of growth and inflation, the ongoing Brexit uncertainty and the slowdown in consumer spending would likely prevent the Bank from moving too fast on rates, with the eventual outcome of Brexit playing a larger role on the pound's longer-term prospects than BoE policy.

Elliott Wave Analysis: EURUSD Can Reach 1.1450-1.1500 Zone

EURUSD broke down last week through 1.1730 level that cause a drop to a new low of the month which impacted some of recent bullish wave structure. What is really important at this stage is that current drop is accelerating which normally occurs in wave three, so we think there can be a new five wave drop in progress right now from 1.1870 since current leg is the strongest bearish reaction since September high. It's very important to listen to the market and not get to attached to the "bullish idea". That said, we adjusted the structure and are now looking at a three wave drop from the September high which can either be a new five wave drop in progress for new euro bearish cycle, or is going to be just a deep A)-B)-C) pullback. In either case there is room for pair to touch 1.1450-1.1500 area, especially if we consider an important zone on a daily time frame.

EURUSD, 4H

CAC Rally Continues On Strong Corporate Earnings

The CAC index continues to have a quiet week. Currently, the CAC is trading at 5,530.00, up 0.50% on the day. On the release front, there are no French or eurozone indicators. In the US, today’s highlight is the Federal Reserve rate statement. On Thursday, the focus will be on manufacturing, as France and the eurozone release Final Manufacturing PMI.

The CAC continues to move upwards, and has climbed 2.8% since October 23. European stock markets have posted strong gains on Wednesday, in response to positive European corporate earnings. Strong performers on the CAC include French car makers Peugeot and Renault, which have gained 1.67% and 0.87%, respectively. On Tuesday, French data was positive, as the French economy continues to improve. Flash GDP remained at 0.5% in the third quarter, matching the estimate. Consumer spending rebounded with a gain of 0.9%, beating the estimate of 0.6%. Preliminary CPI improved to 0.1%, matching the forecast.

After staying on the sidelines for months, the ECB announced last week that it will begin tapering its asset purchase program, from EUR 60 billion/mth to EUR 30 billion/mth. The program, which was scheduled to end in December, has been extended to April 2018. However, ECB President Mario Draghi added a dovish twist to the move, stating that the program would remain open-ended. This provides the cautious ECB with the ability to keep the program in place beyond April without causing strong movement in the currency and stock markets. The euro has reacted sharply to ECB moves (or lack of a move) in the past, and Draghi would like to minimize the ECB’s involvement in market movement.

Fed Statement Eyed But Focus On Yellen Replacement

- Optimism Returns After Brief Consolidation;

- Fed Statement Eyed But Focus on Yellen Replacement;

- Sterling Rallies Ahead of Potential BoE Rate Hike.

Optimism Returns After Brief Consolidation

US indices are on course to open around half a percentage point higher on Wednesday, as we enter the business end of what promised to be a very busy and important week for markets.

There's been no shortage of optimism in the equity market rally in recent weeks but as we entered month end it did appear to lose some of its spark, triggering some consolidation at record highs. With futures pointing to a higher open on Wednesday, it seems that spark may be returning, with optimism over tax reform and another solid earnings season providing the catalyst for the rally. The week has not been short of major economic events but the bulk of these, and arguably the most important ones, are still to come.

Fed Statement Eyed But Focus on Yellen Replacement

The Fed's monetary policy decision would typically be one of, if not the most important event of the week but that may not be the case today. For one, it's extremely unlikely that any change in interest rates will be announced, with December remaining far more likely for the final hike of the year. With Chair Janet Yellen not making an appearance after the announcement, we instead have to rely on the accompanying statement for clues as to whether another hike in December is still planned.

Moreover, with Donald Trump poised to announce who will succeed Yellen from February on Thursday, investors may take the statement with a pinch of salt when considering interest rates beyond the end of the year. All things considered, not only is today's announcement not the biggest market event this week, it's unlikely to even be the most important Fed event.

When it comes to the statement, I don't expect the central bank to deviate much, if at all, from previous rhetoric as the data has been broadly consistent with expectations, barring the understandable weak jobs report last month. This Friday's report is expected to be much better than normal which should mostly offset the weakness in job creation in September, something the Fed may allude to.

Sterling Rallies Ahead of Potential BoE Rate Hike

The pound is rising ahead of Thursday's Bank of England meeting, at which the central bank is expected to announce its first rate hike in more than a decade. This morning's manufacturing PMI is largely behind the latest rally in the pound, with the survey having highlighted robust domestic demand as well as rising inflation pressures, something policy makers have become increasingly concerned about due to the already elevated price growth.

While above-target inflation is being almost entirely driven by the pound's post-Brexit drop, a growing number of policy makers now appear to be of the belief that last year's rate cut is no longer necessary and a return to the previous lower bound is warranted. Markets are heavily pricing in a rate hike tomorrow which may limit any upside in the pound in relation to this, with the accompanying commentary probably more important. With a split among policy makers being clear from recent commentary, a failure to hike tomorrow could trigger a sharp decline in the pound.

Market Update – European Session: UK PMI Manufacturing Beats Expectations, Focus On Central Banks

Notes/Observations

FOMC expected to keep policy steady with door open for a possible 3rd hike in Dec

Participation light in Europe due to all-souls day holiday (Austria, Hungary, Lithuania, Poland, Slovakia, Slovenia)

UK PMI Manufacturing registers a slight beat; focus on BOE rate decision on Thursday with consensus for a dovish hike

Overnight

Asia:

China Oct Caixin Manufacturing PMI: 51.0 v 51.0E (4-month low)

Japan Oct Final Manufacturing PMI revised higher (52.8 v 52.5 prelim)

New Zealand Unemployment at lowest level since financial crisis (4.6% v 4.7%e)

South Korea Oct CPI below forecast and under BOK’s 2% inflation target.

South Korea Oct Trade Balance and components miss expectations

Europe:

UK Brexit Sec Davis: seek to strategically accelerate the Brexit negotiation process. 'Basic' EU deal likely even if trade talks failed. A 'no deal' Brexit would mean no free trade customs accords, no accords on aviation

National Institute of Economic and Social Research (NIESR): Expects UK inflation to peak at 3.2% in Q4, BoE rates to peak at 2% in 2021

Greece said to plan to swap €29.7B in 20 bonds issued following the 2012 private debt restructuring for up to 5 new fixed-coupon bonds; could be launched in mid-Nov

Americas:

US House Tax Committee Chairman Brady: Republican tax bill text to be released on Thursday (one day delay)

NYC 'terror' attack leaves 8 dead, several injured- At least eight people are dead after a driver barreled into a bike path and crashed a rental pickup truck into a crowd in Lower Manhattan

Bank of Canada (BOC) Gov Poloz: We are at a crucial spot in the economic cycle, and significant uncertainties are clouding the way forward

Energy:

Weekly API Oil Inventories: Crude: -5.1M v +0.5M prior

Economic Data

(IN) India Oct Manufacturing PMI: 50.3 v 51.2 prior (3rd month of expansion)

(IE) Ireland Oct Manufacturing PMI: 54.4 v 55.4 prior (53rd month of expansion)

(RU) Russia Oct Manufacturing PMI: 51.1 v 52.3e (15th month of expansion)

(UK) Oct Nationwide House Prices M/M: 0.2% v 0.2%e; Y/Y: 2.5% v 2.2%e

(TR) Turkey Oct Manufacturing PMI: 52.8 v 53.5 prior

(SE) Sweden Oct Manufacturing PMI: 59.3 v 63.5e

(NL) Netherlands Oct Manufacturing PMI: 60.4 v 60.0 prior (50th month of expansion and highest since Feb 2011)

(NO) Norway Oct Manufacturing PMI: 54.5 v 54.0e

(CZ) Czech Oct Manufacturing PMI: 58.5 v 57.0e (14th month of expansion)

(CH) Swiss Oct Manufacturing PMI: 62.0 v 61.3e (6-year high)

(DE) Germany Oct CPI Brandenburg M/M: -0.1% v +0.2% prior; Y/Y: 1.3% v 1.6% prior

(GR) Greece Oct Manufacturing PMI: 52.1 v 52.8 prior (5th straight expansion)

(ZA) South Africa Oct Manufacturing PMI: 47.8 v 45.5e (4th straight contraction)

(UK) Oct Manufacturing PMI: 56.3 v 55.9e (15th month of expansion)

Fixed Income Issuance:

(IN) India sold total INR110B vs. INR110B indicated in 3-month, 6-month and 12-month Bills

(DK) Denmark sold total DKK3.08B in 2020 and 2027 DGB bonds

SPEAKERS/FIXED INCOME/FX/COMMODITIES/ERRATUM

Equities

Indices [Stoxx600 +0.6% at 397.7, FTSE +0.4% at 7523, DAX 1.3% at 13400, CAC-40 +0.5% at 5532, IBEX-35 +0.4% at 10570, FTSE MIB +1.1% at 23031, SMI +0.6% at 9296, S&P 500 Futures +0.3%]

Market Focal Points/Key Themes:

European Indices trade higher once again with continued risk on sentiment bought about by strong earnings globally. UK retail giant Next did report underwhelming 3rd quarter results, with shares down sharply as a result, Marks and Spencer also trades lower in sympathy. Elsewhere Standard Chartered trades over 4% lower after missing on the top and bottom line, Novo Nordisk after missing on Rev trades lower in Denmark.

Looking ahead notable earnings include Groupon, Allergan, Bunge

Equities

Consumer discretionary [Next [NXT.UK] -6% (Earnings), Marks and Spencer [MKS.UK] -3.4% (Sympathy with Next), Paddy Power Betfair [PPB.UK] +3.9% (Earnings)]

Industrials: [Morgan Sindell [MGNS.UK] +3.3% (Earnings)]

Financials: [ Standard Chartered [STAN.UK] -4% (Earnings)]

Healthcare: [Novo Nordisk [NOVOB.DK] -2.8% (Earnings), Indivior [INDV.UK] +11.1% (Confirms FDA Advisory Committees Recommend Approval of Indivior's RBP-6000)]

Energy: [Lundin Petroleum [LUPE.SE] +4.0% (Earnings)]

Speakers

Greece and EU officials said to be negotiating a bailout exit that would involve Greece getting debt relief in exchange for carrying out new reforms. A clean bailout exit with no new financing or a fourth bailout program were less likely post-program scenarios that are on the table

Turkey Central Bank Gov Cetinkaya: Monetary policy stance has become more cautious, pledges continuation of such stance

Japan Abe re-elected as PM during special Parliamentary session (as expected)

Currencies

GBP/USD was higher by 0.2% ahead of Thursday BOE rate decision. The strength in Cable attributed to reports that the UK signaled it was preparing to compromise in its stand-off with the European Union over the Brexit bill, with new talks scheduled next week in an effort to break the deadlock. In addition NIESR expects BoE rates to peak at 2% in 2021.

USD/JPY was higher and probing the 114 neighborhood. JPY currency (Yen) weakness aided by Japan Abe being re-elected as PM during special Parliamentary session

Fixed Income

Bund futures trade at 162.71 up 1 ticks as core euro-bonds are little changed during a public holiday for Austria, Belgium, France, Portugal and Spain. Support lies at 161.00, followed by 160.38. Resistance stands initially at 163.51, followed by 164.25.

Gilt futures trade at 124.31 down 4 ticks, with the focus remaining on the BOE meeting on Thursday. Continued downside eyeing 123.26. Upside targets 124.90 then 125.24.

Wednesday’s liquidity report showed Tuesday’s excess liquidity fell to €1.8225T from €1.833T and use of the marginal lending facility dropped to €172M from €431M

Corporate issuance saw 6 issuers raise $12.3B in the primary market

Looking Ahead

(AR) Argentina Oct Government Tax Revenue (ARS): No est v 224.1B prior

(IL) Israel Sept Leading 'S' Indicator M/M: No est v 0.3% prior

(IT) Italy Oct Budget Balance: No est v -€15.8B prior

(RO) Romania Oct International Reserves: No est v $37.0B prior

05:50 (EU) ECB allotment in 7-day USD Liquidity Tender

06:00 (DK) Denmark Oct Manufacturing PMI: No est v 60.3 prior

06:00 (UK) BOE’s Cunliffe in Parliament

06:00 (EU) Daily Euribor Fixing

06:00 (NO) Norway to sell Bonds

06:00 (GR) Greece Debt Agency (PDMA) to sell €875M in 26-Week Bills

06:00 (ZA) South Africa announces details of next bond auction (held on Tuesdays)

07:00 (US) MBA Mortgage Applications w/e Oct 27th: No est v -4.6% prior

07:00 (BR) Brazil Sept Industrial Production M/M: +0.7%e v 0.8% prior; Y/Y: 3.2%e v 4.0% prior

07:00 (CA) Canada Sept MLI Leading Indicator M/M: No est v 0.2% prior

07:00 (IE) Ireland Oct Unemployment Rate: No est v 6.1%e

08:00 (ZA) South Africa Oct Naamsa Vehicle Sales Y/Y: No est v 7.0% prior

08:00 (BR) Brazil Oct PMI Manufacturing: No est v 50.9 prior

08:00 (UK) PM May weekly question time in House of Commons

08:00 (RU) Russia to sell combined RUB25B in 2021 and 2027 OFZ bonds

08:15 (US) Oct ADP Employment Change: +200Ke v +135K prior

09:00 (BR) Brazil Sept CNI Capacity Utilization: No est v 77.8% prior

09:00 (CZ) Czech Oct Budget Balance (CZK): No est v 17.4B prior

09:05 (UK) Baltic Dry Bulk Index

09:30 (CA) Canada Oct Manufacturing PMI: No est v 55.0 prior

09:45 (US) Oct Final Markit Manufacturing PMI: 54.5e v 54.5 prelim

10:00 (US) Oct ISM Manufacturing: 59.5e v 60.8 prior; Prices Paid: 67.8e v 71.5 prior

10:00 (US) Sept Construction Spending M/M: -0.2%e v +0.5% prior

10:00 (BR) Brazil to sell 2023 LFT bills

10:00 (BR) Brazil to sell 2018, 2019 and 2021 LTN Bills

10:30 (US) Weekly DOE Crude Oil Inventories

11:00 (CO) Colombia Sept Exports: $3.2Be v $3.1B prior

11:00 (MX) Mexico Central Bank Economist Survey

11:00 (MX) Mexico Sept Total Remittances: $2.4Be v $2.5B prior

11:00 (US) Treasury announcement for upcoming 3-year, 10-year and 30-year bonds during week of Nov 5th

11:30 (MX) Mexico Oct Manufacturing PMI: No est v 52.8 prior

12:00 (NZ) New Zealand Oct QV House Prices Y/Y: No est v 4.3% prior

13:00 (IT) Italy Oct New Car Registrations Y/Y: No est v 8.1% prior

13:00 (BR) Brazil Oct Trade Balance: $5.3Be v $5.2B prior; Total Exports: $19.4Be v $18.7B prior; Total Imports: $14,.0Be v $13/.5B prior

13:15 (CH) SNB's Zurbruegg speaks in Bern

14:00 (US) FOMC Interest Rate Decision: Expected to leave Interest Rates unchanged

14:00 (MX) Mexico Oct IMEF Manufacturing Index: 52.0e v 52.9 prior; Non-Manufacturing Index: 52.0e v 52.5 prior

16:15 (CA) Bank of Canada (BOC) Gov Poloz with member Wilkins in Parliament

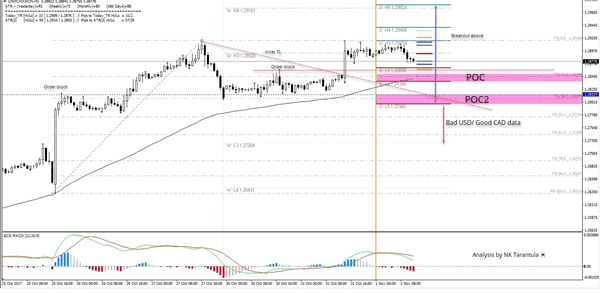

USD/CAD Is Waiting For Fundamental Data Release

The USD/CAD has formed a double top pattern exactly at D H3 pivot. At this point we see a retracement that shows another proof how strong camarilla pivot points are. From a fundamental point of view the market might be waiting for ADP data today as well as CAD Employment change and trade balance. We should see a bit of volatility during the NY/LO Session overlap. From a technical point we see the two POC zones. The first POC 1.2840-55 (order block, EMA89, D L4, 23.6) or the second POC zone 1..2800-15 (inner TL, D L5, 38.2, order block) might reject the price towards 1.2915, 1.2940 and 1.2982 on good ADP / bad CAD data. However if the price drops due to bad USD / good CAD data breakout below 1.2798 should target 1.2774, 1.2740 and 1.2726. Mixed data should keep the price action within the technical outlook.

W L3 - Weekly Camarilla Pivot (Weekly Interim Support)

W H3 - Weekly Camarilla Pivot (Weekly Interim Resistance)

W H4 - Weekly Camarilla Pivot (Strong Weekly Resistance)

D H4 - Daily Camarilla Pivot (Very Strong Daily Resistance)

D L3 – Daily Camarilla Pivot (Daily Support)

D L4 – Daily H4 Camarilla (Very Strong Daily Support)

POC - Point Of Confluence (The zone where we expect price to react aka entry zone)

API Inventories Throw Fuel On Oil’s Fire

The first inventory figures of the weeks from the API showed a massive drawdown, fuelling crude's rally still higher through the Asia session.

The American Petroleum Institute (API) crude oil inventories added fuel to the oil fire overnight, reporting a massive draw of 5.1 million barrels against an expected draw of 1.4 million barrels. This saw Brent and WTI move still higher in New York with both contracts rallying one percent. Brent closed at 61.30 and WTI at 54.45, both near the highs of the New York.

That said, we sound a note of caution in Asia this morning as both contract's daily relative strength indexes (RSI) have moved in to strongly overbought territory. Given the pace of the move and the generally bullish tone in the market, both contracts could be vulnerable to a short-term downward correction. The RSI has been an excellent indicator of these sorts of corrections in 2017.

Both crude contracts have continued to rally in Asia, spurred on by the news that Saudi Arabia will raise prices to two-year highs to Asian customers, and with OPEC compliance rising to 92.0%.

Brent Crude has edged 30 cents higher in early trade to 61.85 having earlier touched 62.00 with little to no technical resistance of note past this level. Support is at 60.50 and 60.00 with a break of that level signalling a deeper correction is possible to the 58.00 area.

WTI has raced 40 cents higher to 54.85 having touched 55.10 earlier in the session. A break of this level clears the road to around 56.00. A daily close above 54.70 is significant as WTI would finally have broken its long-term resistance zone between 53.50 and 54.70. Conversely, a break of 53.50 would signal a correction to at least 52.50 and possibly 52.00.

DAX Jumps On Strong Corporate Earnings

The DAX has posted considerable gains in the Wednesday session. Currently, the DAX is at 13,442.00, up 1.61% on the day. On the release front, there are no eurozone or German indicators on the schedule. Today’s highlight is the Federal Reserve rate statement. On Thursday, Germany publishes Final Manufacturing and PMI and unemployment change, and the eurozone releases Final Manufacturing PMI.

The DAX has posted strong gains on Wednesday, after positive corporate earnings releases. Most companies on the DAX are showing gains, including BMW (1.56%), Daimler (1.92%), Infineon (3.43%) and Volkswagen (2.55%). The DAX continues to set record highs, and has climbed 3.2% since October 23. German stock markets have also been buoyed by strong German numbers, and with the economy expected to record a healthy fourth quarter, the DAX rally could continue.

In Germany, retail sales rebounded in impressive fashion, gaining 0.5% after two straight declines. On an annualized basis, retail sales gained 4.1%, indicative of strong consumer spending. Germany Preliminary CPI edged down to 0.0%, shy of the forecast of 0.1%. This follows two consecutive readings of 0.1% and points to continuing low inflation in an otherwise robust economy.

After months of speculation, the ECB announced last week that it will begin tapering its asset purchase program, from EUR 60 billion/mth to EUR 30 billion/mth. The program, which was scheduled to end in December, has been extended to April 2018. However, ECB President Mario Draghi added a dovish twist to the move, stating that the program would remain open-ended. This provides the cautious ECB with the ability to keep the program in place beyond April without causing strong movement in the currency and stock markets. The euro has reacted sharply to ECB moves (or lack of a move) in the past, and Draghi would like to minimize the ECB’s involvement in market movement.

CRUDE OIL Strong Bullish Momentum

Crude oil has surged. Strong resistance given at 52.86 (28/09/2017) has been broken. The commodity is monitoring 1-year high. Expected to show continued increase.

In the long-term, crude oil has recovered after its sharp decline last year. However, we consider that further weakness are very likely. For the time being the pair lies in an upside momentum. Strong support lies at 35.24 (05/04/2016) while resistance can now be found at 55.24 (03/01/2017 high).

SILVER Continued Decline Within Downtrend Channel

Silver is again grinding lower. Hourly support can be found at 16.60 (27/10/2017 low). Hourly resistance is given at 17.46 (13/10/2017 high). Additional support can be found at 16.13 (06/10/2017 low).

In the long-term, the trend is rater negative. Further downsides are very likely. Resistance is located at 25.11 (28/08/2013 high). Strong support can be found at 11.75 (20/04/2009).