Sample Category Title

Elliott Wave View: EURUSD In A Flat Correction

EURUSD Short Term Elliott Wave view suggests that the decline from 9/8 peak is unfolding as an expanded Flat Elliott Wave structure. Down from 9/8 high (1.2094), Intermediate wave (A) ended at 1.1837 and Intermediate wave (B) ended at 1.2034. Intermediate wave (C) is in progress as 5 waves. Minor wave 1 of (C) ended at 1.186, and bounce to 1.2 ended Minor wave 2 of (C). Down from there, Minor wave 3 of (C) ended at 1.1716, and bounce to 1.1832 ended Minor wave 4 of (C). Minor wave 5 of (C) remains in progress and can reach as low as 1.16207. This area will also complete Primary wave ((W)) and end cycle from 9/8 peak. Afterwards, pair should bounce within Primary wave ((X)) to correct cycle from 9/8 peak in 3, 7, or 11 swing before turning lower again.

Alternatively, if pair extends below 1.16207, then the entire move lower from 9/8 high could be labelled as 5 waves impulse. In this case, the current decline will only end Intermediate wave (3). Then pair should bounce in Intermediate wave (4) before the decline resumes again.

EURUSD 1 Hour Elliott Wave Chart

Expanded Flat is a 3 waves corrective pattern, and the inner subdivision is labeled as A,B,C with 3,3,5 structure. That means waves A and B are always corrective structures i.e. could be WXY, WXYXZ, Zigzag or any 3 waves corrective pattern. Wave C is either 5 waves impulse or ending diagonal pattern. In the graphic below, we can see what Expanded Flat structure looks like. Inner structure has ABC labeling, where wave B can complete below or above the starting point of wave A. Wave C should complete below the end point of wave A (usually at 1.236-1.618 fibonacci extension A related to B).

Forex: Upbeat Data Boosts USD

On Monday, the US Institute for Supply Management (ISM) released data showing the index of national factory activity surged to a reading of 60.8 in September, the highest reading since May 2004, from 58.8 in August. The gains appear to be attributive to the re-build, following the devastation caused by Hurricanes Harvey & Irma, with gains in new orders and raw material prices. Further data released on Monday indicated a rebound in Construction Spending in August, which will further harden expectations the Fed will raise rates in December.

With higher than expected construction spending in August, and the surge in factory activity in September, the Atlanta Federal Reserve’s GDP Now forecast model is indicating that the US economy is on target to grow at 2.7% annualized in Q3. The previous forecast, on September 29th, had suggested a 2.3% growth rate.

Eurozone data released on Monday showed factories, in the eurozone, having their strongest month for over 12-months. However, whilst such data would normally see a rise in EUR, the violence marred independence vote in Spain’s Catalonia region has created concern in the markets with the political risk this could cause to the European Community. Spain now faces its biggest constitutional crisis in decades, as reports suggest that over 90% of voters have chosen to “leave” Spain. Investors will be keenly watching the Spanish Governments response and if this could lead to a “decoupling” of Catalonia.

As expected, the Reserve Bank of Australia left interest rates unchanged at 1.5% earlier today.

EURUSD continued its recent downward trend, falling 0.4% on Monday and continuing lower in early Tuesday trading. Currently, EURUSD is trading around 1.1720.

USDJPY is relatively unchanged overnight, currently trading around 112.95.

GBPUSD continues to move lower with the uncertainty surrounding Brexit negotiations and Prime Minister Theresa May’s apparent lack of party support. Currently, GBPUSD is trading around 1.3265.

After dropping 0.35% on Monday, Gold has retraced slightly in early Tuesday trading to currently trade around $1.272.

WTI suffered a near 2.5% loss on Tuesday on oversupply fears. Currently, WTI is trading around $50.65.

Major economic data releases for today:

At 09:30 BST, the UK Chartered Institute of Purchasing & Supply and Markit Economics will release UK PMI Construction for September. Consensus is calling for a reading of 50.8, slightly worse than the previous release of 51.1, which is very close to the 50 level that would suggest stagnation. A reading of

50.8 underlines the uncertain economic outlook facing the UK and the difficulty the Bank of England has in gauging economic growth. A release considerably different from consensus will see GBP experience high volatility.

At 9:00 BST, Eurostat will release Eurozone PPI (YoY) for August. The forecast is for a higher reading of 2.3% (previously 2.0%). A reading of 2.3% or above could see EUR strengthen and add further impetus for the ECB to reign in stimulus and possibly look at raising interest rates.

Currencies: Dollar Tries To Break ST Top

Sunrise Market Commentary

- Rates: Sentiment-driven trading

Today's eco calendar is empty suggesting sentiment-driven trading (currently negative core bonds) with many investors potentially side-lined in the run-up to key US eco releases later this week. The sell-off in Spanish assets could slow as Catalonia seems to favour dialogue instead of unilaterally declaring independence. - Currencies: Dollar tries to break ST top

The dollar extended its gradual rebound yesterday even as the gains were not impressive. Still, the US currency is nearing recent highs against a series of currencies including the euro and the yen. The eco calendar is thin today, but a further rise in US yields might help the dollar to clear these hurdles.

The Sunrise Headlines

- Wall Street (+0.5%) began the fourth quarter with a quartet of closing highs as upbeat data helped boost optimism on the health of the US economy. Asian risk sentiment is somewhat more mixed overnight with China still closed.

- The Reserve Bank of Australia leaves interest rate unchanged at record low 1.5% for 14th month, having previously said it doesn't need to follow global peers that are tightening policy. AUD/USD tests 0.78 support.

- The Catalan government said it wanted to avoid a 'traumatic split' from Spain and appealed to the EU to help mediate with Madrid in signs it was holding back from an early declaration of independence.

- Relatively calm market conditions could encourage the European Central Bank to extend its asset purchase scheme for a relatively longer period but with reduced monthly spending, ECB chief economist Praet said.

- Dallas Fed Kaplan sounded a cautious note, saying officials should 'look hard' at whether taking action in December is warranted. Minneapolis Fed Kashkari argued that the Fed's own actions, not transitory factors, are responsible for weak inflation.

- The Bavarian sister party (CSU) of German Chancellor Merkel's CDU has said her conservative bloc must agree policies on immigration, pensions and healthcare before opening coalition negotiations with two other parties.

- Today's eco calendar is extremely thin with only US car sales

Currencies: Dollar Tries To Break ST Top

Dollar extends gradual rebound

Yesterday, the dollar traded with a cautiously positive bias as global investors extended last week's reflation trade. At the same time, the euro faced some headwinds from the uncertainty on Catalonia. The USD rebound lost momentum in the afternoon trade despite a very strong ISM manufacturing. Still the US currency finished the session with modest gains. EUR/USD finished the session at 1.1733 (from 1.1814). USD/JPY closed the session at 112.77 (from 112.51). US equities set again new records, but were no big help for the dollar.

Overnight, Asian equities ex-Australia join the positive sentiment from WS. The dollar also receives a better bid supported by strong equities and a minor rise in US yields. USD/JPY rebounded north of 113. EUR/USD dropped to a new correction low and trades in the low 1.17 area. The Reserve Bank of Australia as expected left its policy rate unchanged at 1.5%. The policy statement brought no new information, but repeats that a stronger Aussie dollar weighs on inflation, growth and employment. The Aussie dollar declined after the RBA statement and trades around 0.78.

Today, EMU eco reports are limited to the August PPI (producer prices). It is no market mover, as most national PPI data have already been released. US car sales are expected to have rebounded in September after a sharp dip in August. That's good news for the economy, but markets usually ignore the car sales report.

The dollar rallied last week, as chances on a December Fed rate hike have risen and as the US government stepped up its efforts to put the tax reform on the rails. Both factors propelled US yields and the dollar, but the dollar rebound ran into resistance at the end of last week. It apparently needs good eco news and higher US yields. Yesterday's USD performance was mildly positive, but the pair near the recent highs against several other currencies including the euro and the yen. A positive risk sentiment and a rise in US yields may be needed to support the USD rebound today.

From a technical point of view EUR/USD hovered in a consolidation pattern between 1.1823 and 1.2070, but broke below last week. There was some hesitation in the USD rebound at the end of last week, but EUR/USD closed below the 1.1823 previous range bottom. The rise in US yields is needed to support the USD rebound. Next support in EUR/USD comes in at 1.1662, while 1.1423 marks the 38% retracement from the 2017 rally. The day-to-day momentum in USD/JPY is constructive, but for and important part due to yen weakness. However, USD sentiment is currently also improving. USD/JPY regained 110.67/95 (previous resistance), a short-term positive. The 114.49 correction top is the next important resistance. .

EUR/USD correction lower continues

EUR/GBP

EUR/GBP bottom to become more solid? .

Yesterday, sterling declined against an overall stronger dollar, but also against the single currency. The latter was under slight pressure from the independence vote in Catalonia. Sterling declined after the slightly softer than expected UK manufacturing PMI (55.9). The political bickering on the Brexit strategy between Foreign Secretary Boris Johnson and PM May also weighed on the UK currency. EUR/GBP rebounded to the 0.8868 area and finished the session at 0.8838. The daily losses in cable were substantial as sterling softness coincided with dollar strenght. The pair closed the day at 1.3276 (from 1.3398 on Friday).

Today, the eco calendar only contains the UK construction PMI. A stabilisation at expected. Investors will also keep an eye at the annual conference of the Conservative party in Manchester. The party is divided on the Brexit strategy and PM May's leadership is contested. However, we expect PM May to stay in charge for now. The noise on Brexit might be a modest negative for sterling. Over the previous days, sterling lost some momentum. Sterling may extend its correction against the dollar. A further decline of EUR/USD may be a hurdle for sustained EUR/GBP gains. Even so, a more solid floor is building in EUR/GBP.

EUR/GBP made an impressive uptrend from April to set a MT top at 0.9307 late August. UK price data amended the dynamics and hawkish BoE comments reinforced a sterling rebound. Medium term, we maintain a EUR/GBP buy-on-dips approach as we expect the mix of euro strength and sterling softness to persist. However, the prospect of (limited) withdrawal of BOE stimulus puts a solid floor for sterling ST term. We look how far the current correction goes. EUR/GBP nears support at 0.8743 and 0.8652, which is difficult to break. We look to buy EUR/GBP on dips

EUR/GBP: downside support becomes more solid?

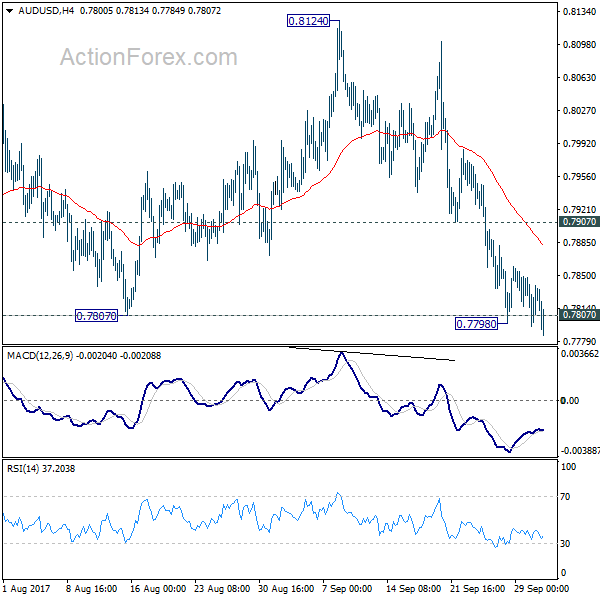

AUD/USD Daily Outlook

Daily Pivots: (S1) 0.7798; (P) 0.7823; (R1) 0.7850; More...

AUD/USD breaches 0.7798 again today but there is no follow through selling below 0.7807 near term support. Intraday bias remains neutral first. As noted before, considering bearish divergence condition in daily MACD, firm break of 0.7807 support will indicate near term reversal. Outlook will then be turned bearish for 55 week EMA (now at 0.7674) first. Meanwhile, rebound from 0.7807 will retain bullishness. Above 0.7907 minor resistance will turn bias back to the upside for retesting 0.8124 high.

In the bigger picture, rise from 0.6826 medium term bottom is seen as corrective pattern. In case of further rally, strong resistance should be seen at 38.2% retracement of 1.1079 to 0.6826 at 0.8451 to limit upside. Meanwhile, firm break of 0.7807 is the first signal that such correction is focused. Break of 0.7328 will bring retest of 0.6826 low.

Dollar Strengthens as US Equities Hit Records Again, Aussie Mildly Lower after RBA

US equities surged to new record highs overnight on solid manufacturing data and dollar followed by gaining broadly in Asian session today. DOW jumped 152.51 points or 0.68% to close at 22557.6. S&P 500 rose 9.76 pts or 0.39% to end at 25.29.12. NASDAQ also gained 20.76 pts or 0.32% to 6516.72. 10 year yield was steady, though, failing to take out last week's high at 2.344 but still rose 0.011 to 2.337. While the greenback is clearly stronger against European majors, it's strength against commodity currencies is less apparent. Aussie dips mildly after RBA left interest rates unchanged. But no follow through selling is seen yet below 0.78 handle.

Fed Kashkari prefer Fed to stand pat

Minneapolis Fed President Neel Kashkari, a know dove, criticized that Fed's monetary accommodation over the past few years is "likely an important factor driving inflation expectations lower". And he preferred not to hike interest rates again until core PCE hitting 2% yoy, a large drop in headline unemployment rate signalling using up of remaining labor slack, or surprise increase in inflation expectations. The latest FOMC rate projections suggest that Fed is still on course for another hike in December, and three more next year. Fed fund futures are pricing in 77.8% chance of a December hike.

ECB Praet markets allow ECB to slow down assess purchase

ECB chief economist Peter Praet said yesterday that in more normal market conditions investors may become "more patient" and be "better able to evaluate the stimulus that can be expected to come from a purchase plan that is to be executed over a more extended time interval." On the other hand, in highly uncertain conditions, "front loading the accumulation of a given stock of purchases more forcefully signals the central bank's commitment to inject the degree of accommodation necessary to support the recovery." With relatively calm markets now, ECB could opt for extending the asset purchase program with reduced monthly purchase for a longer period of time.

RBA left rate unchanged at 1.50% as expected

RBA left interest rate unchanged at 1.50% today as widely expected. In the accompanying statement, RBA Governor Philip Lowe noted that recent data are "consistent with the Bank's expectation that growth in the Australian economy will gradually pick up over the coming year." Also, "a large pipeline of infrastructure investment" will also be " supporting the outlook". However, "wage growth remains low" and "is likely to continue for a while yet". RBA only warned that appreciation in the exchange rate "would be expected to result in a slower pick-up in economic activity and inflation than currently forecast."

On the data front

Australia building approvals rose 0.0% mom in August. Japan consumer confidence improved to 43.9 in September, monetary base rose 15.6% yoy. UK construction PMI and Eurozone PPI are the main features in European session.

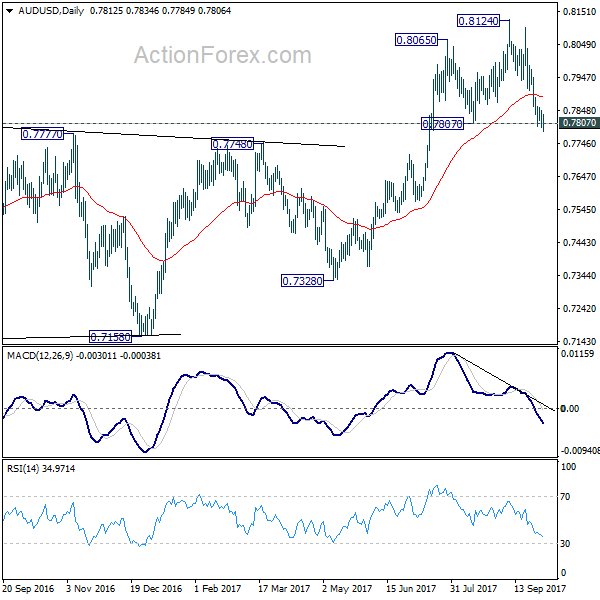

AUD/USD Daily Outlook

Daily Pivots: (S1) 0.7798; (P) 0.7823; (R1) 0.7850; More...

AUD/USD breaches 0.7798 again today but there is no follow through selling below 0.7807 near term support. Intraday bias remains neutral first. As noted before, considering bearish divergence condition in daily MACD, firm break of 0.7807 support will indicate near term reversal. Outlook will then be turned bearish for 55 week EMA (now at 0.7674) first. Meanwhile, rebound from 0.7807 will retain bullishness. Above 0.7907 minor resistance will turn bias back to the upside for retesting 0.8124 high.

In the bigger picture, rise from 0.6826 medium term bottom is seen as corrective pattern. In case of further rally, strong resistance should be seen at 38.2% retracement of 1.1079 to 0.6826 at 0.8451 to limit upside. Meanwhile, firm break of 0.7807 is the first signal that such correction is focused. Break of 0.7328 will bring retest of 0.6826 low.

Economic Indicators Update

| GMT | Ccy | Events | Actual | Forecast | Previous | Revised |

|---|---|---|---|---|---|---|

| 23:50 | JPY | Monetary Base Y/Y Sep | 15.60% | 16.30% | 16.30% | |

| 0:30 | AUD | Building Approvals M/M Aug | 0.00% | 1.00% | -1.70% | -1.20% |

| 3:30 | AUD | RBA Rate Decision | 1.50% | 1.50% | 1.50% | |

| 5:00 | JPY | Consumer Confidence Sep | 43.9 | 43.5 | 43.3 | |

| 8:30 | GBP | Construction PMI Sep | 51.1 | 51.1 | ||

| 9:00 | EUR | Eurozone PPI M/M Aug | 0.10% | 0.00% | ||

| 9:00 | EUR | Eurozone PPI Y/Y Aug | 2.30% | 2.00% |

NZD/USD Accelerates The Sell-Off

The NZD/USD drops further on the short term and is almost to hit the fifth warning line (wl5) of the ascending pitchfork. I’ve said in the previous week that the rate should take out the warning line (wl5) if will reach it. Technically, it should drop further after the retest of the sliding line (sl).

USD/CAD Breakout Expected

USD/CAD increases further on the short term and is almost to hit the upper median line (uml) of the descending pitchfork. Technically, it should take this out if will reach it. A valid breakout will confirm an increase at least till will reach the 1.2678 and the median line (ML) of the major descending pitchfork.

USD/CHF At New Highs

The currency pair increased further and resumed the upside movement. Is trading in the green and looks poised to take out a major resistance level. USD/CHF increases further as the USDX resumed the yesterday's impressive bullish candle. The USDX has managed to jump above the 93.68 previous high and now is trading above the 93.81 horizontal resistance. A valid breakout will confirm a larger rebound in the upcoming weeks and a USD dominance.

The USDX is expected to increase further as the Federal Reserve is expected to hike the rate in December.

The USD/CHF will be driven by the technical factors today, the US is to release only the Total Vehicle Sales indicator, which is expected to increase from 16.1M to 16.9M, but remains to see if will have any impact.

Price is pressuring the upper median line (uml) of the descending pitchfork. Has jumped above this dynamic resistance, but remains to see if will really have a valid breakout. USD/CHF has managed to come back above the up sloping red line, signaling that the bulls are very strong on the short term.

I've drawn an ascending pitchfork to catch a larger upside movement, you can see that the median line (ml) represents a very strong resistance level, it was rejected several times in the last weeks. Price could increase further even if will stay under this dynamic resistance.

RBA Keeps Interest Rate On Hold At 1.5%

For the 24 hours to 23:00 GMT, the AUD rose 0.12% against the USD and closed at 0.7834.

LME Copper prices declined 0.5% or $30.0/MT to $6455.0/MT. Aluminium prices declined 2.1% or $43.5/MT to $2067.0/MT.

In the Asian session, at GMT0300, the pair is trading at 0.7815, with the AUD trading 0.24% lower against the USD from yesterday's close.

Earlier today, the Reserve Bank of Australia (RBA) kept key interest rate unchanged at a record low 1.5%, as widely expected. In a post-meeting statement, Governor Philip Lowe highlighted that unemployment rate in Australia was unlikely to fall quickly while adding sluggish wages was going to be a problem for some time. He also stated that the impact of a stronger Australian Dollar is expected to contribute to continued subdued price pressures in the economy.

Overnight data indicated that Australia's seasonally adjusted building approvals rebounded 0.4% MoM in August, less than market consensus for a gain of 1.0%. In the previous month, building approvals had recorded a revised drop of 1.2%. Moreover, the nation's new home sales rebounded by 9.1% on a monthly basis in August. In the prior month, new home sales had registered a revised drop of 15.4%.

The pair is expected to find support at 0.7794, and a fall through could take it to the next support level of 0.7773. The pair is expected to find its first resistance at 0.7838, and a rise through could take it to the next resistance level of 0.7861.

Going forward, Australia's AiG performance of service index for September, slated to release in overnight, will be on investors' radar.

The currency pair is showing convergence with its 20 Hr moving average and trading below its 50 Hr moving average.

Euro-Zone’s Unemployment Rate Surprisingly Remained Steady In August

For the 24 hours to 23:00 GMT, the EUR declined 0.31% against the USD and closed at 1.1738.

Meanwhile, data indicated that the Euro-zone's unemployment rate unexpectedly remained steady at an eight-year low of 9.1% in August, while markets had anticipated for a drop to 9.0%.

Moreover, the region's final Markit manufacturing PMI was revised lower to a level of 58.1 in September, compared to a preliminary print indicating an advance to a level of 58.2. However, the PMI remained at a nearly seven-year high level. In the previous month, the PMI had registered a reading of 57.4.

Separately, Germany's manufacturing sector expanded to a level of 60.6 in September, confirming the flash estimate. In the previous month, the PMI had registered a level of 59.3.

The greenback gained ground against a basket of major currencies, following a pair of upbeat US economic reports.

The US ISM manufacturing activity index surprised with an unexpected rise to a level of 60.8 in September, accelerating at its fastest pace in more than thirteen years, amid a sharp rise in new orders and raw material prices. Markets had expected the index to fall to a level of 58.1, after recording a reading of 58.8 in the prior month. Further, the nation's construction spending rebounded more-than-anticipated by 0.5% on a monthly basis in August, following a revised drop of 1.2% in the prior month. Markets had expected construction spending to climb 0.4%.

In other economic news, final print of Markit manufacturing PMI was revised higher to a level of 53.1 in September from a preliminary print indicating a rise to a level of 53.0. The PMI had registered a level of 52.8 in the previous month.

In the Asian session, at GMT0300, the pair is trading at 1.1713, with the EUR trading 0.21% lower against the USD from yesterday's close.

The pair is expected to find support at 1.1683, and a fall through could take it to the next support level of 1.1654. The pair is expected to find its first resistance at 1.1761, and a rise through could take it to the next resistance level of 1.1810.

Going forward, market participants will closely monitor the Euro-zone's producer price index for August, slated to release in a few hours.

The currency pair is trading below its 20 Hr and 50 Hr moving averages.