Sample Category Title

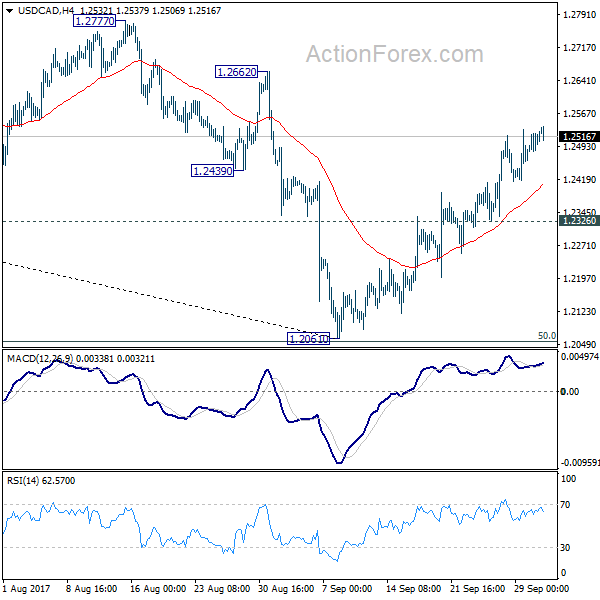

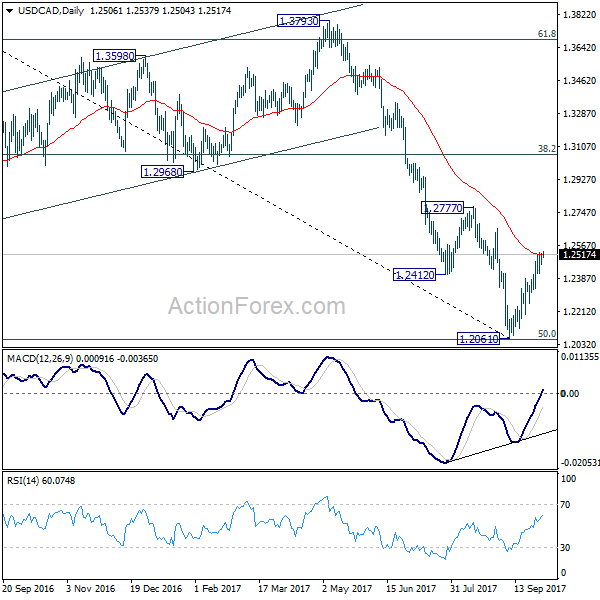

USD/CAD Daily Outlook

Daily Pivots: (S1) 1.2473; (P) 1.2499; (R1) 1.2533; More....

USD/CAD's rebound from 1.2061 is still in progress. Intraday bias remains on the upside for 1.2777 resistance first. As noted before, current development argues that the pair has successfully defended 1.2048 fibonacci level. Decisive break of 1.2777 will target 38.2% retracement of 1.4689 to 1.2061 at 1.3065 next. However, break of 1.2326 will dampen this bullish view and turn bias back to the downside for 1.2061 instead.

In the bigger picture, current development argues that USD/CAD has defended 50% retracement of 0.9406 (2011 low) to 1.4869 (2016 high) at 1.2048. And with 1.2048 intact, we'd favor the case that fall from 1.4689 is a correction. Break of 1.2777 will further affirm this bullish case. That is, larger up trend from 0.9406 is not completed. However, on the other hand, firm break of 1.2048 will indicate that fall from 1.4689 is at least a medium term down trend and should target 61.8% retracement at 1.1424 and below.

RBA Upbeat On Economic Growth, No Rush To Hike Rates

RBA left the cash rate unchanged at 1.5% in September. The accompanying statement contained few changes from the previous one. This perhaps explains the modest drop in Aussie after the release, as the market had expected a more hawkish message. The central bank is upbeat over the economic developments, hinging on the improving non-mining investment. Policymakers also acknowledged the strength in the job market, pointing to the rise in participation rate as well as a number of forward-looking indicators. Comments on the exchange rate were limited, with the central bank reiterating the impact of a strong Aussie on inflation, GDP growth and employment. We expect the central bank to keep the policy rate unchanged until 2H18.

Policymakers retained the view that domestic economy would 'gradually pick up over the coming year'. The members acknowledged that 'non-mining business investment is picking up'. They did not mention the decline in mining investments this month, signaling the negative impact of which has almost dissipated. On the job marker, the RBA noted that it has 'continued to grow strongly over recent months'. It took note that rise in labour force participation as an indication of rising confidence in the employment situation. However, persistently low wage growth should continue for some time.

The central bank did not comment on the decline in AUDUSD (-2.3%) since the last meeting. It only attributed its appreciation since mid-year partly to a lower US dollar It warned that the higher exchange rate would prolong 'subdued' inflation, and weigh down on the outlook for output and employment.

Other than the mild drop in Australian dollar, market reaction of the announcement was muted. IB futures-implied RBA has priced in a 64% chance of a 25bp hike by May, and 100% by August 2018. These bets were similar to those before the announcement. We expect the central bank to keep the policy rate unchanged until 2H18.

Europe Seen Higher After Record Highs In US

European equity markets are expected to open a little higher on Tuesday, buoyed by decent gains in Asia overnight and new record highs in the US on Monday.

AUD Slips as RBA Maintains Neutral Stance

The Reserve Bank of Australia left its cash rate on hold at 1.5% overnight and released a relatively neutral statement alongside it that praised certain elements of the global and domestic economy while once again warning about the detrimental effects of a strong Australian dollar.

The statement gave no indication that the RBA is preparing to raise or cut interest rates any time soon, with upside and downside risks aplenty providing the central bank little incentive to do so. The Aussie dollar fell a little after the release to trade below 0.78 against the dollar, back to levels last seen in mid-July.

Spanish Unemployment and UK Construction eyed

While political distractions will likely continue to tick over in the background – this week's primary focus being the aftermath of the Catalonia referendum – this week is more about the economic data given the sheer volume of numbers being released. Spanish unemployment is up first today, with the data expected to show a second consecutive monthly increase, this time of 21,300. Given the general improvement in the labour market in recent years and the tendency of unemployment to rise at this time of year, I don't think anyone will be too concerned by the data.

Construction becomes the latest sector in the UK to come under the microscope when the PMI survey for September is released this morning. Monday's manufacturing PMI fell a little short of expectations but remained comfortably in growth territory, supported by the weaker pound, despite its recent recovery. The construction PMI is expected to remain unchanged at 51.1, having slipped back here after a summer of much more optimistic readings. The most important of the UK PMIs comes tomorrow though, with the services sector representing more than three quarters of economic output.

Potential Future Fed Chair Makes an Appearance

While there's no US economic data being released today, we will hear from Jerome Powell who currently sits on the board of governors at the FOMC but is also one of the four candidates currently being considered for Chair of Federal Reserve once Janet Yellen's term ends in February.

GBPUSD Short-Term Bearish, Recent Rally At Risk Of Reversal

GBPUSD is increasingly bearish after breaking below the key 1.3400 level and the 2-week decline is threatening to reverse the September rally to 1.3656. The brief consolidation range near the highest levels since June 2016 broke down last week and momentum signals are turning more negative.

The broader market structure looks bullish, showing GBPUSD slowly advanced from the 1.2000 area since the early part of this year. The crossover of the 50-day moving average above the 200-day MA in May gave a bullish signal. It remains to be seen whether the recent drop in prices is just a corrective move of the strong September rally.

GBPUSD is testing fresh 2-week lows and is approaching key support at 1.3200. This level is approximately the mid-point of the recent advance from 1.2773. A break below 1.3200 opens up the way for a drop towards the 50-day MA and to the key 1.3000 level.

Only a rise back above 1.3400 would ease downward pressure and indicate that the 2-week decline from 1.3656 was a corrective move of the broader uptrend.

GBPUSD is expected to remain under pressure in the short-term as momentum signals are shifting. RSI is falling and MACD is reversing its rise. Near term risk is tilted to the downside but the broader bullish picture is still intact as long as the market remains above 1.3200.

Dollar Bulls In Charge On Improved US Economic Outlook, Aussie Down After RBA Policy Meeting

On Tuesday, rising economic prospects in the US kicked the dollar higher to a 1 ½-month high against its major rivals during Asian trading, while a steady monetary policy and an unchanged economic outlook as indicated overnight by RBA policymakers sent the aussie down to a two-month low.

The spot dollar index stretched its uptrend during the Asian session, reaching a fresh 1 ½-month high of 93.92 as confidence in the US economic environment was enhanced after the release of upbeat manufacturing PMI readings on Monday and the Fed retained its hawkish stance on monetary policy. Additional support for the greenback was also found as the US 10-year Treasury yields peaked at a three-month high of 2.371 percent overnight, whereas geopolitical tensions did not escalate despite Trump refusing to start a discussion with North Korea on nuclear issues for the second time.

Dollar/yen rose by 0.20% on the day to 112.96 ahead of the Japanese snap elections later in the month. Meanwhile, the leader of the newly launched Party of Hope and Tokyo's governor, Yuriko Koike, showed reluctance to join the snap elections scheduled for October 22.

Gold stood flat at a two-week low of $1,270 per ounce.

The euro extended losses during the session, breaking marginally the $1.17-key level at $1.1695 as political uncertainties in Spain and Germany were on the rise after a violent independent vote in Spain on Sunday and inconclusive federal elections in Germany on September 24. Investors will now focus on the ECB meeting minutes published on Thursday for any clues on monetary policy moving forward.

The pound posted losses versus the greenback, edging down to $1.3262, weighed by risks revolving Brexit and economic conditions in the nation.

In the first hours of Asian trading, the RBA decided to keep interest rates on hold at a record low of 1.5%. Moreover, the monetary statement did not defer much compared to the one released in September as policymakers reiterated their concerns on a stronger currency, subdued inflation, and wage growth whilst they also stayed cautious on household debt levels. A few hours earlier, August's housing data out of Australia came in lower than expected, adding to losses for the aussie. Building approvals grew by 0.4% m/m compared to an upwardly revised contraction of 1.2% seen in the previous month, missing expectations of a 1.1% growth. Private house approvals declined by 0.6% m/m after rising by 1.0% (revised upwards from 0.0%).

The aussie tumbled to a two-month low of $0.7784 but it managed to climb to 0.7810 before Asian markets close for the day.

The kiwi retreated by 0.35% amid political uncertainty in New Zealand while businesses were more concerned about the country's economic outlook in the next six months, driving the NZIER business confidence index to 5% in the third quarter from the 18% posted in the previous quarter.

In energy markets, oil was trading flat near yesterday's two-week lows. WTI crude stood around $50.40 per barrel and Brent was hovering around $55.88.

Euro Selloff Continues As U.S. 10-Year Yields Hit 3-Month High

The Euro selloff resumed on Tuesday, sending the single currency to $1.17 in Asia trade, the lowest in six weeks. The political risks have been gradually increasing in the past two weeks; it started with the German Federal Election, which led to the surge of the far-right, and now Catalonia’s independence vote. The political risk premium has been reflected in the Spanish-German yield spreads, which widened substantially on Monday. 10-year yield spreads gained eight basis points to trade at their highest levels since early June 2017. Politics has clearly overshadowed the economic improvement in the Eurozone, and this will likely remain the case for the rest of the week. With consumers and business confidence remaining high however, the PMI is continuing to show improvement in the manufacturing and services sector, and the economy is set to expand by 2.2% in 2017.It is these factors that will lead the single currency in the long run.

In contrast, the dollar continued to find support from improving economic data and a rise in yields. The ISM Manufacturing Index hit a 13-year high, supported by new orders and an increase in prices. Hurricanes Harvey and Irma probably disrupted the data a little, but there has been a broad economic improvement strengthening expectations that the Federal Reserve will hike interest rates in December. Looking into the U.S. bond yields, fixed income traders also seem to agree that an interest rate hike is coming soon. After falling to 2.01% on 8 September, U.S. 10-year bond yields have appreciated by more than 330 basis points in just 18 trading days.

Mr. and Mrs. Watanabe like these developments, as they have been waiting for opportunities to increase their carry trades. This is why USDJPY is trading at its highest level since mid-July. However, one should be careful, as the snap election in Japan takes place in just three weeks. Markets so far, are pricing an easy defeat for Shinzo Abe, but given that Tokyo governor Yuriko Koike is becoming more popular, one should hedge his long positions.

In other currency news, the Aussie was the worst performing major currency early Tuesday, after the Reserve Bank of Australia held interest rates at 1.5%. Although Governor Philip Lowe stated that growth in the Australian economy would gradually pick up over the coming year, his warning on the Australian dollar strength drove the selloff. Such comments are always short-lived, and traders need to focus on economic fundamentals. AUDUSD is becoming an attractive long as we approach 0.77, the 50% retracement from the most recent surge (0.7331 – 0.8124).

Aussie Dollar Struggle Continues Vs US Dollar

Key Highlights

- The Aussie Dollar declined recently and broke the 0.7875 support against the US Dollar.

- There are two key bearish trend lines formed with resistance near 0.7820 on the 4-hours chart of AUD/USD.

- RBA made no changes in rates in the recent interest rate decision (Number 2017-21).

- Australia's HIA New Home Sales in August 2017 rose 9.1%, better than the last revised -15.4%.

AUDUSD Technical Analysis

The Aussie Dollar started a major downtrend after failing to remain above 0.8000 against the US Dollar. The AUD/USD pair recently broke a major support area near 0.7875, opening the doors more losses.

The pair is now well below the 100 and 200 simple moving averages (H4) and traded as low as 0.7786. On the upside, there are two key bearish trend lines formed with resistance near 0.7820 on the 4-hours chart.

Considering the recent decline and the price action, there is a chance of AUD/USD correcting by 30-40 pips in the near term. However, there are many hurdles on the upside for buyers near 0.7840 and 0.7860.

Above trend lines, the 50% Fib retracement level of the last decline from the 0.7899 high to 0.7786 low is a major hurdle. Moreover, the broken support at 0.7875 might now act as a barrier for an upside break.

On the downside, a break of the 0.7785 low could take the pair towards the next support at 0.7740.

RBA Interest Rate Decision and HIA New Home Sales

Today, the RBA Interest Rate Decision (Number 2017-21) was announced by the Reserve Bank of Australia. The central bank made no changes in the interest rate from 1.5%.

The statement concluded as:

The low level of interest rates is continuing to support the Australian economy. Taking account of the available information, the Board judged that holding the stance of monetary policy unchanged at this meeting would be consistent with sustainable growth in the economy and achieving the inflation target over time.

Moreover, the HIA New Home Sales figure for August 2017 was released by the Housing Industry Association. The forecast was slated for a minor rise of around 2% in sales compared with the previous month.

However, the result was positive as there was an increase of 9.1% in sales. On the other hand, the last reading was revised down from -3.7% to -15.4%.

The ANZ job advertisements report for August 2017 was also published today by the Australia and New Zealand Banking Group Limited (ANZ). According to the report, there was no increase in the ANZ job advertisements compared with the last revised +2%.

Overall, the AUD/USD pair might correct higher in the short term, but upsides remain capped near the 0.7840-60 levels.

Euro Trades Below 1.1710

The euro has fallen below key weekly technical support against the U.S dollar, after solid economic data from the United States economy provoked another round of buying in the U.S dollar index.

Trading sentiment in the EURUSD pair is expected to remain bearish while political tension in Catalonia worsen, and price-action continues to trade below the euro's 200-week moving average, at 1.1710.

With today's economic calendar in the U.S and Europe remaining fairly light, the U.S dollar index is likely to dictate intraday trading.

The next series of higher time frame closes on the four and eight-hour price-candles around the 1.1710 technical level will be crucial for the EURUSD.

Key intraday technical support below 1.1710 is located at the August monthly low, at 1.1662 and the euro's 100-day moving average, at 1.1654. Below 1.1654, further support is found at 1.1610 and 1.1580.

To the upside, key intraday resistance is located at yesterday daily price-low, at 1.1730 and the euro's calculated daily pivot point, at 1.1748. Above the 1.1748 level, the 1.1770 level is critical former support now turned resistance.

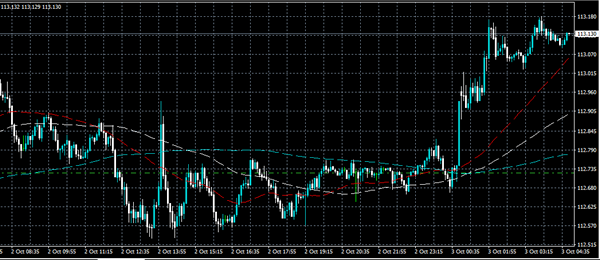

USDJPY Above 113 AS Greenback Soars

The USDJPY pair has moved back above the 113 level, as the U.S dollar index continues to climb higher, after yesterday's United States ISM manufacturing PMI posted its highest reading in six years.

Trading sentiment surrounding the USDJPY pair is increasingly bullish today, with weekly fundamentals and technicals both currently favoring further upside.

Price-action on the USDJPY pair has so far reached 113.18, which is still slightly below the former weekly price-high of 113.25.

A move above the 113.25 level is expected to accelerate buying in the pair, whilst a move below the 112.70 would be technically bearish.

Key intraday resistance on the USDJPY pair is located at 113.25, 113.57 and 113.89. A move above the 113.89 level would likely further buying towards 114.10 and 114.45.

To the downside, key intraday support is found at the former weekly high, at 112.90 and the key 112.70 level. Once below 112.70, further support is found at the pairs weekly pivot point, at 112.41.

.

Tuesday: Calm Before The Storm?

Investors can expect a lighter release schedule on Tuesday as they brace for a more active second half of the week headlined by US jobs data and central bank speeches.

Action begins in Europe at 07:00 GMT with a report on Spain's unemployment situation. The total level of unemployed is expected to rise by 21,300 for September, following an increase of 43,300 the month before.

At 08:30 GMT, CIPS and IHS Markit will produce the monthly construction purchasing managers' index (PMI). The report is expected to show a slight weakness in industry activity for the month of September.

The European Commission's statistical agency will report on producer inflation at 09:00 GMT. The monthly PPI is expected to edge up by 0.1%, translating into a year-over-year gain of 2.3%.

Shifting gears to North America, Federal Open Market Committee (FOMC) member Jerome Powell is scheduled to deliver a speech bright and early at 08:30 GMT. Powell was interviewed by President Trump for the position of Fed Chair, which could become vacant this February.

In policy news, the Reserve Bank of Australia (RBA) kept its trend-setting interest rate at a record low of 1.5% on Tuesday. The decision was widely expected by the financial markets. The Australian central bank has remained on the sidelines of monetary policy since August 2016, when it cut rates for the second time that year.

AUD/USD

A dovish RBA weighed on the Australian dollar Tuesday, as the AUD/USD dipped below 78 cents. The pair was down 0.4% to trade at its lowest level in around seven weeks. The Aussie has declined roughly 300 pips against the US dollar since 20 September. In the meantime, the greenback has regained momentum against a cross-section of its competitors. The short-term outlook is tilted to the downside as a bearish central bank continues to drive away the bulls.

EUR/USD

The euro was back on the defensive Monday, as the US dollar continued to steamroll the competition. The EURU/USD is down more than 100 pips from the Friday high. Prices slipped another 0.2% on Tuesday to trade in the low 1.17 region. The common currency has plunged roughly 400 pips from the 8 September multiyear high. The EUR/USD is testing the 1.1708 daily low from 27 September. On the opposite side of the ledger, resistance is seen at 1.1833.

USD/JPY

The USD/JPY broke above 113.00 on Tuesday, reaching its highest level in three months. The combination of improved risk sentiment and caution ahead of the Japanese general election have triggered heavy volatility in the yen. The USD/JPY has gained 4.5% since 11 September. The bulls are now targeting the critical 114.40 region. This level isn't as far as it appears, given the pair's strongly bullish bias above the 100-day simple moving average (SMA).