Sample Category Title

USDJPY: Vulnerable On Loss Of Upside Pressure

USDJPY - The pair closed lower on Thursday leaving risk on further downside on the cards. On the downside, support comes in at the 112.00 level where a break if seen will aim at the 111.50 level. A cut through here will turn focus to the 111.00 level and possibly lower towards the 110.50 level. On the upside, resistance resides at the 113.00 level. Further out, we envisage a possible move towards the 113.50 level. Further out, resistance resides at the 114.00 level with a turn above here aiming at the 114.50 level. On the whole, USDJPY now faces further bear pressure.

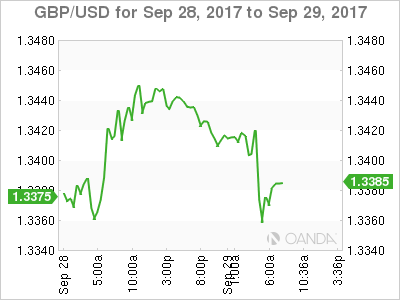

Pound Dips as UK Current Account Deficit Ballons

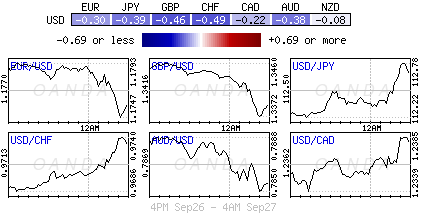

The British pound has recorded losses on Friday, erasing the gains which marked the Thursday session. Currently, GBP/USD is trading at 1.3389, down 0.39% on the day. On the release front, it's a busy day, with multiple releases in the both the UK and US. The UK's current account deficit widened significantly in the second quarter, climbing to GBP 23.2 billion. This was much higher than the forecast of GBP 15.8 billion. Britain's GDP expanded 0.35% in the second quarter, matching the estimate. In the US, Personal Spending XX

The negotiations between Britain and the European Union over the terms of Britain's withdrawal from the EU have been tortuous until now, with little progress to report after several rounds of negotiations. Key sticking points include the amount that Britain will pay upon leaving, whether the European High Court will have jurisdiction over EU citizens living in Britain, and the border with Ireland. British Prime Minister May has been keen to discuss trade relations with the continent, but the Europeans have insisted on first making progress on the other issues. However, the tone of the talks has improved recently, as Prime Minister May's conciliatory speech in Florence was received positively in Europe, although large gaps still remain between the two sides.

The US economy received strong marks on its report card for Q2, as Final GDP posted an impressive gain of 3.1%. This figure was revised upwards from the second estimate of 3.0% in August. The strong reading is being taken with some caution, however, as third quarter economic numbers could soften, due to the tremendous damage caused by hurricanes Harvey and Irma, which caused a slowdown in economic activity. The recent hurricanes have also impacted on the labor market, pushing unemployment numbers higher. Still, the US labor market remains strong, as underscored by unemployment rolls which have remained below the 300,000 level.

Donald Trump hasn't had any luck with his health care plan, which barely passed in the House of Representatives and appears doomed in the Senate, despite a Republican majority in both houses. The US president has now set his sights on tax reform, another key campaign platform. On Wednesday, Trump proposed a major overhaul of the US tax code, which includes reducing the corporate tax rate from 35 percent to 20 percent, as well as 25 percent tax rate for small businesses, such as partnerships. Like other Trump proposals, the tax plan was sketchy on details, including how the tax plan would be paid for. With Democrats and some Republicans wary of Trump, it's likely that tax reform will face a stiff battle in Congress.

Trumps Reflation Trade On Hold

Friday September 29: Five things the markets are talking about

This week has been one of the strongest this year for the mighty dollar against G10 currency pairs in particular. The month of September is looking to close out the first monthly gain for the ‘buck' in seven-months, backed by investors weighing up the prospects for U.S tax cuts and the possibility of another Fed hike before year-end.

Trump's proposed tax plan, currently lacks detail, leaving capital markets somewhat in the dark on what areas would be prioritized by the administration. It's this lack of context that seems to have persuaded a number of investors to consider putting Trumps ‘reflation' trade on hold.

Nevertheless, with fed fund futures odds of further tightening stateside this year hovering atop of +70%, continues to provide some underlying support for equities and sovereign yields. Investors prefer to shy away from owning gold, which remains on track to close out September as its worst month this year.

Data on tap today, stateside; the U.S Commerce Department reports personal income and spending data for August (08:30 am EDT). Investors are likely to see some distortions related to Hurricanes Harvey and Irma, while north of the border, Canada releases its GDP numbers.

1. Stocks in the black

A weaker yen (¥112.48) has managed to underpin Japanese equities in September. Overnight, the Nikkei share average ended almost flat, down -0.03%, but managed to post its biggest monthly gain this year as investors rebuild positions they were scaled back on geopolitical concerns. The broader Topix was down -0.08%, but ended the month up +3.5%.

In Hong Kong, stocks ended higher on Friday, but the benchmark index has closed out September with its first monthly loss in 2017, an indication that the market's upward momentum may be slowing amid worries over U.S monetary tightening and a China economic slowdown. The Hang Seng index rose +0.5%, but posted a -1.5% loss on the month and reduce 2017 gains to +25%. The China Enterprises Index gained +0.3%. For the month, it was up +0.2%, and for the quarter, the gauge gained +8.6%.

In China, stocks were higher, supported by hopes of further reforms to the mainland's state-owned enterprises. The blue-chip CSI300 index rose +0.4%, while the Shanghai Composite Index gained +0.3%.

Note: China now begins its weeklong National Day holiday.

In Europe, stocks remain in the black; the FTSE 100 Index has jumped +0.5% to the highest in almost two-weeks, while the DAX Index has gained +0.2%, hitting the highest in three-months with its fifth consecutive advance. Spanish stocks are underperforming leading into the weekend with expected (illegal) referendum vote in Catalonia.

U.S stocks are set to open little changed.

Indices: Stoxx50 +0.2% at 3,567, FTSE +0.5% at 7,361, DAX +0.2% at 12,732, CAC-40 flat at 5,292, IBEX-35 -0.4% at 10,292, FTSE MIB flat at 22,591, SMI +0.2% at 9,128, S&P 500 Futures -0.05%

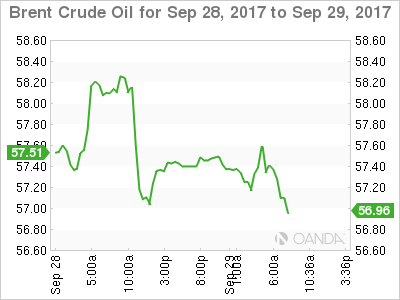

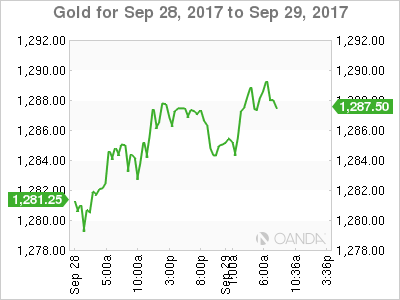

2. Oil mixed but set for weekly gain, gold has a losing month

Ahead of the U.S open, oil prices are mixed, but both Brent and U.S crude are set to record another weekly gain as investors bet that efforts to cut a global glut are working.

Brent crude oil is up +1c to +$57.42 a barrel, heading for a fifth weekly climb and a nearly a +10% gain on the month, while U.S crude (WTI) is down -8c at $51.48 a barrel at 0641 GMT, after earlier rising slightly. Still, the contract is heading for a fourth consecutively weekly gain and is on track for a 9 percent advance this month.

Support has been found from OPEC and non-OPEC producers have indicated they will stick with output cuts to limit supply. The crude ‘bulls' are also getting support from Turkey's threats to cut off a pipeline from the Kurdish region of Iraq after a referendum where Kurds voted overwhelmingly in favour of independence.

Note: The Kurdish region exports about +500k bpd through a pipeline that runs through Turkey to the Mediterranean Sea.

Gold is trading little changed amid pressure from a stronger U.S dollar. The yellow metal is heading for its biggest monthly fall this year amid rising prospects of a U.S rate hike in December. Spot gold is unchanged at +$1,286.96 per ounce and is on track to register a -2.5%this month.

3. Yields end the week on a high

The prospect of higher U.S debt levels and expectations for another Fed hike has sent 10-year U.S Treasury yields to their highest since mid-July, with the 2-10 year yield curve steepening to its highest in a month.

This week's selloff saw yields jump +19 bps, the most since Trump's U.S election victory last November. Overnight, the yield on U.S 10-year notes has fallen less than -1 bps to +2.31%.

Comments this week from Fed Chair Janet Yellen that the U.S central bank needs “to continue with gradual rate hikes” have cemented expectations for policy tightening by year-end.

Note: U.S two-year notes are the most sensitive to overnight rates – yields have backed up to a nine-year high of +1.49% in anticipation of a rate rise in December.

Elsewhere, Germany's 10-year Bund yield has dipped -2 bps to +0.46%, while the U.K's 10-year Gilt yield has decreased -2 bps to +1.33%.

4. Sterling falls on higher Q2 U.K deficit

Ahead of the U.S open, Sterling (£1.3381) has been trading under pressure after data this morning showed that the U.K Q2 deficit came in much higher than expected at -£23.2B. The market was forecasting a deficit of -£16.1B. U.K Q2 GDP growth was unrevised at +0.3% q/q.

Note: The U.K. current account position alone is not enough of a reason to be bearish the pound, however, it's a risk that leaves the UK dependent on ‘the kindness of strangers' according to the BoE to fund its twin deficits.

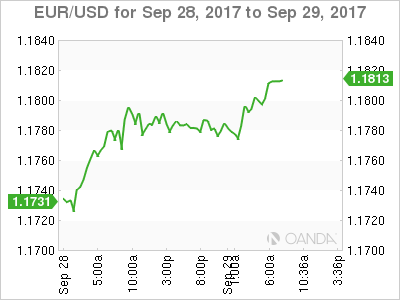

Elsewhere, the EUR (€1.1811) is off its overnight highs after weaker preliminary CPI data (see below), nevertheless, the range remains relatively tight with little volume. Investors are starting to question in what form President Trump's tax reform will get through Congress. The potential of a delay and/or watering down of the plans is expected to limit the USD appreciation potential.

5. Eurozone inflation below expectations

Data this morning showed that the eurozone's annual rate of inflation was unchanged at +1.5% this month, below the consensus forecast for a pickup to +1.6%.

That leaves it well below the ECB's target of just under +2%. Digging deeper, the core rate of inflation fell to +1.1% from +1.2%, its lowest level since June, and a number that should leave Euro policy makers a tad concerned, but are unlikely to inspire a major rethink at the ECB.

Risks In Catalonia Build

All eyes on Spain

While the German elections (still a non-issue) continues to dominate Europe conversation, events in Spain are about to heat up. Where this story takes markets, confounds and worries this strategy desk. The Catalonia referendum on Independence is plan to take place on Sunday 1st October. The Sunday vote will ask Catalans if they would support a separate state from Spain. Based on the 1978 'unity' agreement the Spanish constitutional court has ruled the referendum illegal. The regional government remains committed holding a vote while Spain central government has increase efforts to eliminate any trace of a referendum including confiscating by force ballet boxes, shutting down social media site and detaining regional political figures. Markets are betting that the efforts by the Central government to stymie representative results will delegitimize any Sunday ballot. Yet these efforts by the Central Government in our view will most likely backfire as the Catalonian that do find a way to vote (eliminating balancing vote of opponents of independence) in a board majority vote for succession. A similar pattern witnessed in the 'non-binding' referendum in 2014. To defuse tensions, there has been signals from both sides that discussion for a calmer resolution are on the table. Offers to the Catalan government of a new financial constitution will address a primary point of contention. But overall we have the feeling passions are running high, were suggestions of future talks will not appease the Catalonians. Markets are not pricing in any risk for Sunday as short-term EURUSD implied volatility are actually lower then longer term. We would be wary of hold spec positions over the weekend as truly all things are possible in Barcelona.

CHF strengthens against Catalonian vote backdrop

The Helvetic currency has lost two figures since the start of the week going from 1.16CHF to 1.14CHF. Some Swiss economic indicators came in better. The UBS Consumption indicator has risen in August from 1.38 to 1.53. This morning the KOF Leading Indicator, an indicator trying to predict the future of the Swiss economy, has also risen.

Economic indicators are showing good optimism on the Swiss economy and markets tends to also adjust their optimism on the single currency which explains, in our view, the current decline in the EURCHF.

The EURCHF is also largely driven in the short-term on European political issues. The Catalonian vote is definitely a thorn in the side of the European Union which tend to be above nations. We believe that the right for self-determination will become a key issue in the Future of the European Union and as a result will continue weighing on the single currency. On top of that, we also consider that markets are still overly optimistic regarding the future tightening of the ECB.

In the short-term, we should nonetheless see the euro rising again the CHF as there are decent likelihood that Madrid invalidates the Catalonian vote.

Market Update – European Session: Sterling Suffers As UK Q2 GDP Y/Y Revised Lower. Eurozone Inflation Misses Forecasts

Notes/Observations

UK FTSE rises on weaker cable after UK Q2 GDP was revised lower

EU flash CPI comes short of expectations, while French CPI was a slight beat and Italy misses

German jobless rates hits new record low in Sep

Overnight

Asia:

Raft of data out of Japan, prelim Industrial Production, National CPI comes ahead of expectations while Retail Sales, Household spending misses and Jobless rate comes inline.

BoJ Sept Meeting Minutes: One member said more easing is necessary to stimulate demand**Note: At the Sept BoJ meeting, the incoming member Kataoka was the lone dissenter (8 to 1 vote). The official said then that the yield curve control is not enough to meet the inflation target; Also, the official saw a low chance of CPI increasing from 2018.

Europe:

UK Q2 Final GDP Y/Y revised lower to 1.5% from 1.7% prior, Cable falls Gilts rise

Eurozone prelim CPI comes in softer then forecast, Core CPI misses estimates and falls m/m

French CPI comes in slightly firmer then forecasts, Italy CPI misses

German Unemployment rate at fresh record low at 5.6%

ECBs Praet Economic recovery is not yet translating into higher inflation; ECB has to take economic improvement into account

Economic data

(UK) Q2 FINAL GDP Q/Q: 0.3% V 0.3%E; Y/Y: 1.5% V 1.7%E

(EU) EURO ZONE SEPT ADVANCE CPI ESTIMATE Y/Y: 1.5% V 1.6%E; CPI CORE Y/Y: 1.1% V 1.2%E

(UK) AUG NET CONSUMER CREDIT: £1.6B V £1.4BE; NET LENDING: £3.6B V £3.6BE

(UK) Q2 CURRENT ACCOUNT: -£23.2B V -£15.9BE

(DE) GERMANY SEPT UNEMPLOYMENT CHANGE: -23K V -5KE; UNEMPLOYMENT RATE: 5.6% (record low) V 5.7%E

(FR) FRANCE SEPT PRELIMINARY CPI M/M: -0.1% V -0.2%E; Y/Y: 1.0% V 1.0%E

(FR) FRANCE AUG CONSUMER SPENDING M/M: -0.3% V 0.2%E; Y/Y: 1.2% V 1.7%E

(IT) ITALY SEPT PRELIMINARY CPI (NIC INCLUDING TOBACCO) M/M: -0.3% V -0.2%E; Y/Y: 1.1% V 1.3%E

(DE) GERMANY AUG RETAIL SALES M/M: -0.4% V +0.5%E; Y/Y: 2.8% V 3.2%E

(UK) SEPT NATIONWIDE HOUSE PRICE INDEX M/M: 0.2% V 0.1%E; Y/Y: 2.0% V 1.9%E

(CH) SWISS SEPT KOF LEADING INDICATOR: 105.8 V 105.5E

Fixed Income Issuance:

Non seen

SPEAKERS/FIXED INCOME/FX/COMMODITIES/ERRATUM

Equities

Indices [Stoxx50 +0.2% at 3,567, FTSE +0.5% at 7,361, DAX +0.2% at 12,732, CAC-40 flat at 5,292, IBEX-35 -0.4% at 10,292, FTSE MIB flat at 22,591, SMI +0.2% at 9,128, S&P 500 Futures -0.05%]

Market Focal Points/Key Themes: European stocks opened higher and maintained momentum; oil slightly higher, but not supporting energy stocks much; Spanish stocks underperforming leading into the weekend with expected vote in Catalonia; Israel closed for holiday; attention turning to personal income and spending data as well as PCE deflator from the US, to be released later in the session; upcoming earnings in the US session include Marine Products and City Holding; reminder that next week both South Korea and China markets to be closed for holidays

Equities

Consumer discretionary: Vivendi EX.FR +0.7% (analyst action), Volkswagen VOW3.DE -1.6% (increases impairment)

Energy: Electricite de France EDF.FR -2.3(analyst action), Lundin Petroleum LUPE.SE -1.1% (dry well), Rubis RUI.FR +1.9% (analyst action)

Financials: Beazley Group BEZ.UK +3.2 (trading update), Fonciere Des Regions FDR.FR +1.9% (analyst action)

Industrials: Advanced Metallurgical Group AMG.NL +8.2% (operations update), Carillion CLLN.UK -11.3% (results)

Materials: Covestro 1COC.DE +0.6% (Bayer sell stake) - Telecom: Telecom Italia TIT.IT -0.8% (new CEO)

Speakers

(EU) EU's Juncker: Not in favour of a Euro budget; Sees EU reform program stretching through next 7 years

(EU) EU's Tusk: To present schedule for reform of EU in two weeks; EU needs to take step by step approach with EU reform - speaking ahead of Summit in Estonia

(EU) ECB's Nouy (SSM Chief): Banking union headed in right direction

(CN) China Banking Regulator (CBRC): China to prevent fast rise in household leverage ratio

(UK) PM May: We are making progress on citizen's rights negotiations

(IT) Italy PM Gentiloni: EU reforms must boost economic growth

Currencies

GBPUSD trades lower after Q2 GDP was revised lower y/y, trading down to 1.3363. EURGBP rises to 0.8815 a 4 day high.

EURUSD trades slightly lower after weaker prelim CPI, the range remains narrow in quiet trade

(IN) India INR currency (rupee) off session lows on suspected dollar sales by RBI - dealers

Fixed Income

Bund futures trade at 161.20 up 28 ticks as euro are inflation data came in weaker than expected. Continued downside targets 160.25 while upside resistance stands initially at 162.07, followed by 163.27.

Gilt futures trade at 124.00 up 18 ticks after UK second quarter final GDP YoY was revised down to 1.5%. Continued downside eyeing 123.06. Upside targets 124.90 then 125.24.

Friday's liquidity report showed Thursday's excess liquidity fell to €1.712T from €1.723T and use of the marginal lending facility dropped to €48M from €131M.

Corporate issuance saw $2.2B come to market via 2 issuers headlined by Canadian Imperial Bank $1.75B 2-part senior notes offering. Which brings weekly issuance to $20.4B.

For the week ending Sep 27th Lipper US fund flows reported IG Funds net inflows of $1.19B bringing YTD inflows to $92.5B, High Yield funds reported net inflows of $432.6M bringing YTD outflows to $7.98B.

Looking Ahead

05:30 (SL) Sri Lanka Sept CPI Y/Y: No est v 6.0% prior

06:00 (IT) Italy Aug PPI M/M: No est v 0.0% prior; Y/Y: No est v 0.9% prior

06:00 (PT) Portugal Aug Industrial Production M/M: No est v 2.0% prior; Y/Y: No est v 6.4% prior

07:30 (IN) India Weekly Forex Reserves

08:00 (BR) Brazil Aug National Unemployment Rate: 12.7%e v 12.8% prior

08:00 (CL) Chile Aug Total Copper Production: No est v 473.5K tons prior

08:00 (CL) Chile Aug Manufacturing Production Y/Y: 1.8%e v 2.6% prior; Industrial Production Y/Y: 3.3%e v 3.3% prior

08:00 (CL) Chile Aug Unemployment Rate: 6.8%e v 6.9% prior

08:00 (PL) Poland Sept Preliminary CPI M/M: 0.2%e v -0.1% prior; Y/Y: 2.0%e v 1.8% prior

08:00 (ZA) South Africa Aug South Africa Budget Balance (ZAR): No est v -92.2B prior

08:00 (ZA) South Africa Aug Trade Balance (ZAR): 2.1Be v 9.0B prior

08:05 (UK) Baltic Dry Bulk Index

08:30 (CA) Canada July GDP M/M: 0.1%e v 0.3% prior; Y/Y: 3.9%e v 4.3% prior

08:30 (CA) Canada Aug Industrial Product Price M/M: 0.5%e v -1.5% prior; Raw Materials Price Index M/M: 0.3%e v -0.6% prior

08:30 (US) Aug PCE Core M/M: 0.2%e v 0.1% prior; Y/Y: 1.4%e v 1.4% prior

08:30 (US) Aug PCE Deflator M/M: 0.3%e v 0.1% prior; Y/Y: 1.5%e v 1.4% prior

08:30 (US) Aug Personal Income: 0.3%e v 0.4% prior; Personal Spending: 0.2%e v 0.3% prior

09:00 (RU) Russia Q2 Final Current Account: No est v -$0.3B prelim

09:30 (BR) Brazil Aug Primary Budget Balance: No est v -16.1B prior; Nominal Budget Balance: No est v -44.6B prior

09:45 (US) Sept Chicago Purchasing Manager: 58.7e v 58.9 prior

10:00 (MX) Mexico Aug Net Outstanding Loans: No est v 3.823T prior

10:00 (US) Sept Final University of Michigan Confidence: 95.3e v 95.3 prelim

11:00 (CO) Colombia Aug Exports: No est v $3.1B prior

11:00 (CO) Colombia Aug National Unemployment Rate: No est v 9.7% prior; Urban Unemployment Rate: No est v 11.3% prior

12:00 (US) USDA World Agricultural Supply and Demand Estimate (WASDE) Crop Report

13:00 (US) Weekly Baker Hughes Rig Count data

15:30 (MX) Mexico Aug YTD Budget Balance (MXN): No est v 119.3B prior

GBP/JPY Lower Trend Line Broken

Following worse than expected GDP data, the popular “Dragon” – GBP/JPY has broken both he lower trend line and progressive channel. A subsequent pullback within the POC zone (D H3, Upper trend line, ATR pivot, EMA89) 151.15-30 could reject the price towards 150.50 zone again. However if we don’t see any pullback a sustained break or 4h close below D L4 150.38 should target 149.87 and 149.60. The final ATR projection is 149.36 but that might happen only on strong profit taking. For bears to dominate the price should stay below 150.60.

Dollar Smiles While Sterling Scowls

Sterling's price action this week can be described as messy, as rocky Brexit negotiations between the United Kingdom and Brussels, left investors on edge.

Sentiment towards the Pound was already fragile amid the uncertainty,and reports released on Friday, showing a downward revision of Britain's annual growth rate,put more pressure on the currency. Economic growth in the United Kingdom rose by just 1.5% annually in the second quarter of 2017, which was down from an earlier estimate of 1.7%. This was the slowest annual growth since 2013 and continues to suggest that Britain is struggling to shake offthe Brexit blues. With Brexit uncertainty and soft economic data weighing on sentiment, it will be interesting to see how the BoE responds duringNovember's policy meeting.

BoE's Mark Carney was in the spotlight yesterday, as he delivered the opening remarks at the Bank of England's conference, celebrating 20 years of independence. Investors who were betting on Carney to reinforce the BoE's hawkish stance were left empty-handed, after the central banker sounded somewhat cautious. What mildly excited sellers, were statements that the BoE could not be expected to nullify the likely hit to the UK economy, as a result of Brexit. With Carney informing markets that the central bank will do everything it can to support the fragile UK economy as it tackles Brexit, market players may be forced to re-evaluate the likelihood of higher UK interest rates. It should be kept in mind that Brexit has dished out bucket loads of uncertainty, and this has the ability to obstruct the central bank's efforts to take action.

Sterling/Dollar remains under pressure on the daily charts below 1.3500. Sustained weakness under this level should open a path lower towards 1.3350. A weekly close below 1.3350 may signal a further decline towards 1.3150.

Dollar set for best weekly gain in 2017

It has certainly been a positive trading week for the Greenback, as hawkish comments from Fed officials and renewed optimism over Trump's tax reforms, stimulated buying sentimenttowards the currency.

Dollar bulls were revitalised this week, after Yellen emphasized the need for gradual rate hikes. Trump's tax reform blueprint, which he says will be the largest tax cutin the history of U.S., also gave a boost to sentiment towards the U.S. economy. With U.S. economic growth for the second quarter revised higher at 3.1%, the ingredients for the Fed to raise U.S. interest rates in December are falling into place.

From a technical standpoint, the Dollar Index is turning increasingly bullish on the daily charts. Although the Dollar extended losses against a basket of currencies on Friday, on the back of profit taking, buyers still remain in control above 92.50. While optimism over the U.S. economy is likely to keep prices buoyed, a catalyst may be needed to jolt the index back above 93.50. This could come in the form of a solid U.S. jobs report next week.

Euro rises on positive economic fundamentals

Euro bulls were active on Friday, after data released in the previous session showed that Eurozone economic confidence hit its highest level in more than 10 years, in September.

While the Euro may edge higher in the short term amid the positivity, political uncertainty in Europe is likely to create headwinds for bulls down the road. As we head into the final trading quarter of 2017, the EURUSD could be instore for a rough and rocky ride. With the Dollar regaining its mojo amid rising rate hike expectations and the Euro finding support from QE taper expectations, bulls and bears are gearing for a tough tug of war.

From a technical standpoint, the EURUSD is under pressure on the daily charts. Previous support around 1.1850 could transform into a dynamic resistance that encourages a further decline towards 1.1680. Repeated weakness below this price should signal an end to the weekly bullish trend, with the next level of interest at 1.1500.

Commodity spotlight – Gold

Gold tumbled to its lowest level since Augustduring Thursday's trading session, and headed for the biggest monthly decline this year, as optimism over Trump's tax reforms boosted the U.S. Dollar.

The downside was complimented by firmly hawkish comments from Janet Yellen earlier in the week, which reinforced expectations of a U.S. interest rate hike in December. With the Dollar likely to appreciate further, amid rate hike expectations and optimism over tax reforms, Gold remains vulnerable to further losses. Although the yellow metal has edged slightly higher during Friday's trading session, bears remain in control under $1300 with breakdown below $1280, opening a path towards $1267.

Technical Outlook: WTI Oil – Mixed Near-Term Signals But Overall Bulls Remain Intact

WTI Oil remains in red on Friday, but near-term price action stays above initial supports at $51.16/09 (rising 10 SMA / Tenkan-sen).

Oil hit fresh multi-month high at $52.84 on Thursday, but was unable to hold gains and fell back, ending Thursday’s trading in red.

Near-term picture is mixed as the price trying to find direction after double-Doji on Tue/Wed which signaled strong indecision and possible stall of steep three-week rally.

Technical outlook remains bullish and sees scope for fresh upside after consolidation phase, which should be ideally contained above 10SMA / Tenkan-sen.

Fundamentals are also supportive as efforts from oil producers to cut global oversupply are giving results and outlook for oil demand is improving.

WTI contract is on track for the fourth consecutive strong bullish weekly close and ends the month in green, which is bullish signal.

Weekly close above cracked $51.95 barrier (Fibo 76.4% of $55.01/$42.04 Feb-June descend) is needed to generate further signal for advance towards $53.74 target (12 Apr high).

Conversely, Friday’s close below 10SMA / Tenkan-sen supports would be negative signal for deeper pullback towards psychological $50.00 support (also Fibo 382% of $45.57/$52.84 ascend).

Res: 51.75, 52.41, 52.84, 53.00

Sup: 51.32, 51.08, 50.38, 50.00

Will Inflation Data Heighten Or Calm Fed Fears?

- US inflation, income and spending numbers key as Fed uncertainty grows;

- Sterling slides as Q2 GDP is revised lower;

- IBEX lower as caution grows ahead of Catalonia referendum.

US equity markets are expected to open relatively unchanged from Thursday as we await the release of some important inflation data, as well as other key US economic metrics.

The inflation data clearly stands out today as, despite it coming a couple of weeks after the CPI numbers for the same month, it is the Federal Reserve’s preferred measure of inflation as comes as policy makers appear uncertain about the correct approach to interest rates. The central bank recently claimed that it still intends to raise rates one more time this year with support among policy makers for such a move actually increasing and yet, the tone coming from officials themselves suggests there’s a serious lack of conviction.

Concerns about inflation not progressing towards target are clearly increasing among some of the more dovish policy makers at the Fed and another weak reading today won’t help matters. Should we see some improvement, as is expected with the PCE price index seen rising to 1.5% from 1.4%, it may be just enough to get one more rate hike over the line in December, assuming of course that it doesn’t reverse course again over the next couple of months.

Personal income and spending figures will also be released alongside the inflation data, both of which are also important metrics as it offers some insight into possible future inflationary trends and economic performance. It’s no secret that the US economy is driven by the consumer so higher incomes and spending should make the Fed’s job that much easier. The UoM consumer sentiment survey should also provide some insight into this.

The pound has come under some pressure on Friday having previously been on a great run on the anticipation that the Bank of England will raise interest rates this year. Softer GDP data for the second quarter of 1.5%, down from previous estimates of 1.7%, triggered the slide in the pound, which was already looking a little vulnerable following recent moves. While the downside looks limited as long as the BoE follows through on rate hike plans, a sustained move above 1.36 against the dollar also looks a little far-fetched on the possibility of one hike and very gradual hikes thereafter.

Interestingly, the IBEX is the only major European index trading in the red this morning as we head into a weekend in which Catalonia is planning an illegal independence referendum. While the outcome of the referendum, should it go ahead, is unlikely to change anything in the near-term, if at all, there is clearly a little caution about what the outcome will do to investor sentiment in the region and whether it could trigger a series of events that ultimately leads to it gaining independence. As it is, I don’t see much threat from this weekend’s referendum and there’s a good chance that efforts to stop it from Madrid will be successful.

DAX Climbs To 3-Month High, German Data Mixed

The DAX index continues to post gains this week. In the Friday session, DAX is trading at 12,736.25, up 0.40% on the day. On the release front, Eurozone CPI Flash Estimate was unchanged at 1.5%, just shy of the forecast of 1.6%. German numbers were a mix. Retail Sales declined 0.4%, well off the forecast of +0.5%. There was better news from the labor market, as unemployment rolls dropped by 23 thousand, much stronger than the estimate of a decline of 5 thousand.

Despite the uncertainty surrounding the German election, German stock markets continue to point upwards. The DAX is poised for another winning week, and has climbed an impressive 5.3 percent in September. Although German retail sales have recorded two straight declines, the markets remain confident in the strength of the German economy, which has showed robust growth in 2017 and is a key factor in stronger economic conditions in the eurozone, in particular stronger growth and lower unemployment. As for the election, President Angela Merkel isn’t wasting any time, and has appointed her former finance minister, Wolfgang Schaeuble as president of parliament. This move clears the path for the FDP to join a Merkel government, as the party has insisted on the finance portfolio. The FDP is fiscally hawkish and staunchly against Germany continuing to finance weaker eurozone members, such as Greece. If the FDP does take part in the government, Merkel may have to shift away from her pan-European vision of a more closely integrated eurozone.

The US economy continues to perform hum, as Final GDP for the second quarter posted an impressive gain of 3.1%. This figure was revised upwards from the second estimate of 3.0% in August. However, September and third quarter economic numbers could soften, due to the damage caused by hurricanes Harvey and Irma, which caused a slowdown in economic activity. The recent hurricanes have impacted on the labor market, pushing unemployment numbers higher. Still, the labor market remains strong, as underscored by unemployment rolls which have remained below the 300,000 level.

President Trump has all but given up on his health care proposal, as the plan lacks enough support from Republican lawmakers. Trump has now set his sights on tax reform, another key campaign promise. On Wednesday, Trump proposed a major overhaul of the US tax code, which includes reducing the corporate tax rate from 35 percent to 20 percent, as well as a 25 percent tax rate for small businesses, such as partnerships. Like other Trump proposals, the tax plan was sketchy on details, including how the tax plan would be paid for. With Democrats and some Republicans wary of Trump’s tax agenda, it’s likely his that tax reform proposal will face a stiff battle in Congress.