Sample Category Title

Euro Quiet As Eurozone CPI Estimate Within Expectations

The euro is almost unchanged in the Friday session. Currently, EUR/USD is trading at 1.1797, up 0.09% on the day. On the release front, Eurozone CPI Flash Estimate was unchanged at 1.5%, just shy of the forecast of 1.6%. German numbers were mixed. Retail Sales declined 0.4%, well off the forecast of +0.5%. There was better news from the labor market, as unemployment rolls dropped by 23 thousand, much stronger than the estimate of a decline of 5 thousand. In the US, there are two key indicators – Personal Spending and UoM Consumer Sentiment. Both indicators are expected to soften, with estimates of 0.1% and 95.3, respectively.

The markets continue to digest the results of the German election earlier this week. President Angela Merkel won a fourth mandate from the voters, but her election win is being called a ‘hollow victory’, as Merkel’s CDU slipped badly and won just 33% of the seats in parliament. The CUD will have to negotiate with smaller parties in order to make a coalition government. The most likely coalition is the CDU, the pro-business FDP and the Greens. This is uncharted political territory, as Germany hasn’t had a 3-party coalition since the 1950s. Merkel, an experienced and astute politician, hasn’t wasted any time, and has already appointed her former finance minister, Wolfgang Schaeuble to president of parliament. This move clears the path for the FDP to join, as the party has insisted on the finance portfolio. The FDP is fiscally hawkish and against Germany continuing to finance weaker eurozone members, such as Greece. If the FDP does take part in the government, Merkel may have to shift away from her pan-European vision of a more closely integrated eurozone.

The US economy continues to perform well, as Final GDP for the second quarter posted an impressive gain of 3.1%. This figure was revised upwards from the second estimate of 3.0% in August. However, September and third quarter economic numbers could soften, due to the damage caused by hurricanes Harvey and Irma, which caused a slowdown in economic activity. The recent hurricanes have impacted on the labor market, pushing unemployment numbers higher. Still, the labor market remains strong, as underscored by unemployment rolls which have remained below the 300,000 level.

President Trump has all but given up on his health care proposal, as the plan lacks enough support from Republican lawmakers. Trump has now set his sights on tax reform, another key campaign promise. On Wednesday, Trump proposed a major overhaul of the US tax code, which includes reducing the corporate tax rate from 35 percent to 20 percent, as well as a 25 percent tax rate for small businesses, such as partnerships. Like other Trump proposals, the tax plan was sketchy on details, including how the tax plan would be paid for. With Democrats and some Republicans wary of Trump’s tax agenda, it’s likely his that tax reform proposal will face a stiff battle in Congress.

Strategy: Natural Rate Key To Understand Central Banks

Today's key points

- While the Phillips curve theory is important to understanding monetary policy setting in the short run, the natural rate is key to understanding monetary policy setting in the long run.

- The BoE's Mark Carney argues that structural factors continue to weigh on the natural rate but that it is increasing everywhere due to the global recovery.

- While we still expect long-term yields to increase as central banks have turned more hawkish, there is a limit to how high they can move due to the low natural rate

We have had several important central bank speeches over the past couple of weeks revealing how the major central banks are thinking at the moment. As the speeches have been quite theoretical, we have gained more information about how they see monetary policy not only in the short run but also in the long run, which may have interesting market implications – more on that later. In particular, we think Bank of England Governor Mark Carney's speech on 18 September was quite interesting as he (among other things) touched upon the natural rate (simply put, it is the rate which should prevail in ‘equilibrium' when the output gap is closed and growth is on trend). While the Phillips curve theory (stating that the tighter labour market will push up wages and hence inflation) is still important to understand monetary policy setting in the short run, the natural rate is key to understanding the monetary policy setting in the long run.

Carney argues that although structural factors continue to weigh down on the natural rate, it is likely increasing everywhere due to the global recovery, not least since business investments are picking up again after they declined on the back of the hard landing in China and the oil price shock beginning in 2014. Business confidence has continued higher in recent months, signalling accelerating business investment growth, see chart to the right. When looking at the economic data, it is also difficult to be very concerned, as the global economy seems in a good shape and there are not many risk factors out there at the moment – this also partly explains why we have not seen any big market corrections, as we discussed in last week's strategy piece. Looking at some of the recent data releases: US core capex orders continued higher in August, euro area economic confidence is at its highest since the crisis and PMIs are high – all good news. The strong economic cycle and low risks mean we are still positive on equities.

If Carney is right that the natural rate is increasing, it means that a constant monetary policy is becoming more accommodative, something Carney and ECB President Mario Draghi both mentioned before the summer holiday, see also Strategy: Central banks consider leaving the party, 30 June. Theory suggests the stance of monetary policy should be measured by the so-called real policy rate gap, which is the difference between the actual real policy rate and the natural rate and not just by the current level of the nominal policy rate. If the natural rate increases and the actual real policy rate remains unchanged, the gap increases and monetary policy becomes more accommodative. This likely also explains why the Bank of England now seems on its way to delivering a November hike, in particular now that UK CPI inflation remains high and unemployment rate is below the BoE's NAIRU estimate. One problem is, however, that the natural rate is unobservable, so we cannot know for sure.

Fed Chair Yellen also contributed to this debate during her press conference after the recent FOMC meeting and in her speech on Tuesday. Not surprisingly, she repeated she still believes in the Phillips curve and thus it is still appropriate to tighten monetary policy gradually. However, she also said that US monetary policy is close to neutral right now, (see chart below), meaning that the Fed should not hike much further, before monetary policy is neither expansionary nor contractionary. The reason why the Fed expects more than a few hikes is because Yellen also expects the natural rate is increasing, which the level of the Fed's longer-run median ‘dot' also shows. However, the Fed has consistently revised down its projection for the natural rate and did it once more at the recent meeting from 3% to 2.75% (in nominal terms), so the question is of course whether the Fed is once again too optimistic.

A lot of theory but what does all this mean for markets? The strong economy not only means we are positive on equities, but also that central banks are gradually turning more hawkish, which explains why we expect yields to increase, see also Yield Outlook, 15 September. However, given the natural rate will remain low even if it is increasing, there is a limit to how high yields can move and it is difficult to see the longer-end of the curve trading at the same levels as before the crisis even when monetary policy is normalised. Thus, we expect a flattening of the UST curve for the 2Y10Y on a 12M horizon, as the short end is pushed higher by Fed hikes and structural factors are weighing down on the long end. In the euro area, we expect a steeper EUR curve next year, as the ECB maintains a tight grip on the short end of the curve, while the 10Y segment of the curve is pushed higher by US yields and a market slowly pricing in an end to the QE programme/tapering in 2018. However, when the ECB begins to hike rates, perhaps some time in 2019, we may see the flattening again, as structural factors also put a cap on longterm yields in the euro area.

US Futures Higher | Dollar Index Bounces Back Up | Illegal Referendum In Spain Under Focus | Gold Could...

Tightening of the Fed momentary policy started to play its role

President Trump's tax reform could hang up in negotiations

Illegal referendum taking place over in Spain

Smart money is actually busy in hedging their risk while the gold price drops

The US futures are trading higher as the dollar index makes its sudden comeback. This is despite the fact that there is a higher probability that President Trump's tax reform could hang up in negotiations or that we could see an extremely watered down version. Nonetheless, the month of September has brought good news for the US equity markets as president Trump announced the initial framework on tax reforms. The US markets are set to close the month at a new record high. The US dollar index has been under pressure pretty much this year however, with the announcement of the tax reforms, the trend for the currency has reversed because investors do see the currency improving due to the better economic growth.

The tightening of the momentary policy by the Fed has also started to play its role and the dollar is looking much firmer on the back of this. Having said that, the prospects of another rate hike for this year aren't that solid yet, as we do think that the chances of another rate hike for this year are still fifty percent.

Unlike the US equity market, the performance of the FTSE 100 index has been lacklustre this year. Thanks to the strength of the currency which is having a major impact. After falling sharply last year, the rebound in the currency is dragging the index lower. The British pound is set to post its best monthly performance against the mighty dollar and also three consecutive quarters of gain. Later today, we will also see the UK Q2 GDP reading. No surprise is expected here and the forecast is for 0.3%. The business investments are expected to remain under the influence of the Brexit woes and the forecast is for 0%.

The event which is going to gain an enormous amount of attention over the weekend is the illegal referendum taking place over in Spain. Catalonia will stage an illegal referendum and a yes vote would depend on the country's crisis. The potential impact would be on the country's bonds unless the county's PM manages to stop the vote. The Spanish equity markets had outperformed the European peers so far this year but the recent illegal referendum situation has taken the toll on the IBEX index.

Over in the US, we expect a lot of noise in the personal spending and income data. The numbers would show a lot of distortion due to the influence of the recent hurricanes. We expect the spending number to drop and the core PCE deflator may not show any change.

The recent rise in the oil prices should provide some sort of tailwind for the upcoming CPI data for the Eurozone. The forecast is for 1.6% while the previous reading was at 1.5%.

Gold

As for the precious metal, the strength in the dollar is pushing the price lower. However, it is important to pay attention to the holdings of the biggest gold exchange holding fund. It clearly shows that smart money is actually busy in hedging their risk while the gold price drops. The 30-day volatility index for the gold price has also surged and this provides an evidence that the shining metal could bounce soon. The near-term support is at 1266.

Technical Outlook: AUDUSD Is Consolidating Above Daily Cloud Base, Near-Term Bias Remains Negative

The pair is holding bullish stance as Thursday's pullback was contained by rising daily Tenkan-sen (112.20) and action remains also underpinned by 10/200 Golden cross (112.00). Bulls look for close above dented 112.80 target to confirm bullish continuation through Thu/Wed peaks at 113.20/25) towards targets at 113.57/114.00 and possible extension towards key barrier at 114.49 (11 July high. Downside should be ideally protected by rising Tenkan-sen , but extended dips towards daily cloud top (111.54) cannot be ruled out. Daily cloud continues to underpin the action after the price surged through the cloud and downside attempts being repeatedly contained by cloud top. The pair is also on track for the third straight bullish weekly close and above weekly cloud that supports broader bullish structure.

Res: 112.80, 113.25, 113.57, 113.68

Sup: 112.00, 112.00, 111.54, 111.36

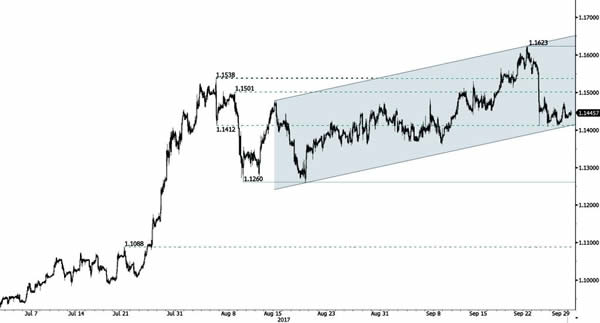

EUR/CHF Ready To Bounce Back

EUR/CHF is riding within uptrend channel. Buying pressures are still strong. Strong resistance is now given at 1.1623 (22/09/2017 high). Expected to bounce back within uptrend channel.

In the longer term, the technical structure has reversed. Strong resistance is given at 1.20 (level before the unpeg). Yet, the ECB's QE programme is likely to cause persistent selling pressures on the euro, which should weigh on EUR/CHF. Supports can be found at 1.0184 (28/01/2015 low) and 1.0082 (27/01/2015 low).

CRUDE OIL Holding Above $50

Crude oil is edging higher above the $50 level. Key support is given at 45.40 (17/08/2017 high). Strong resistance found at 52.43 (26/09/2017) has been broken. Expected to show another leg higher.

In the long-term, crude oil has recovered after its sharp decline last year. However, we consider that further weakness are very likely. Strong support lies at 35.24 (05/04/2016) while resistance can now be found at 55.24 (03/01/2017 high).

SILVER Monitoring Support At 16.58

Silver has reversed and has broken uptrend channel by breaking support implied by its lower bound. Strong resistance is given at 18.65 (17/04/2017 high) while support can be found at 16.58 (15/08/2017 high). Expected to show further bearish move.

In the long-term, the trend is rater negative. Further downsides are very likely. Resistance is located at 25.11 (28/08/2013 high). Strong support can be found at 11.75 (20/04/2009).

GOLD Bearish Consolidation Within Mediumterm Uptrend Channel

Gold has weakened again below 1300. Hourly support is now given at 1277 (intraday low). Hourly resistance is located at 1357 (08/09/2016). Stronger support lies at 1204 (10/07/2017 high). Expected to show further bearish move.

In the long-term, the technical structure suggests that there is a growing upside momentum. A break of 1392 (17/03/2014) is necessary ton confirm it, A major support can be found at 1045 (05/02/2010 low).

BITCOIN Bearish Consolidation Within Uptrend Momentum

Bitcoin has taken a dive after strong interest over the summer. The digital currency has set up a new support at 2975 (22/08/2017 low). Sell walls around $4000 have been broken. Key resistance can be located at 4921 (01/09/2017 high). The road is wide open for further shortterm consolidation.

In the long-term, the digital currency has had an exponential growth. There are decent likelihood that the asset will reach $10'000.

EUR/GBP Consolidating

EUR/GBP is trading sideways. Yet, the pair is facing selling pressures. As long as prices remain below the resistance at 0.8899 (19/09/2017 low), the short-term technical structure is biased to the downside. Hourly support is given at 0.8746 (27/09/2017). Resistance lies at 0.8899 (19/09/2017 high).

In the long-term, the pair has largely recovered from recent lows in 2015. The technical structure suggests a growing upside momentum. The pair is trading above from its 200 DMA. Strong resistance can be found at 0.9500 (psychological level).