Sample Category Title

Autos and Oil Led to a July Pause in Canadian GDP

After notching up eight straight months of gains, the Canadian economy took a pause in July, as GDP was effectively unchanged on a month-on-month basis.

Unsurprisingly, only 11 of the 20 major industry groups saw output expand in July, representing roughly 52% of output - the smallest share since October of last year.

The goods producing sector held things back, pulling back 0.5% after four consecutive monthly expansions. Weakness was relatively widespread, as mining and quarrying contracted 1.2%, due largely to weakness in ¬oil and gas extraction. Construction activity fell 0.5% on weakness in the residential sector, while manufacturing output was down 0.4% on the back of motor vehicle manufacturing. As was noted in the manufacturing sales report earlier this month, this pullback appears to be the result of more significant than normal retooling activity at major auto plants in July.

Services remained the 'Steady Eddie' of the Canadian economy, expanding 0.2% in their 16th straight month of growth. Wholesale trade led the way, up 2.0% on broad-based strength. It was a more mixed story across the other major service sectors.

Key Implications

Well that isn't terribly encouraging. A softer report was to be expected given the impact of auto sector retooling, but in the event, July GDP still disappointed as the pullback in the oil and gas sector added to a generally weak month of activity for goods producing industries. The decline was big enough to outweigh growth in the service sector - which saw its 16th month of growth - its longest run since 2006.

With some of the weakness down to one-off factors, a resumption of growth in August appears to be a reasonable assumption. However, with growth tracking 2.2%, effectively in line with our Quarterly Economic Forecast for the third quarter, it appears that the red-hot growth seen in the first half of the year is likely behind us.

Like the other July economic data, today's report only partially reflects the impact of Bank of Canada tightening, and so is likely to be discounted by policymakers. But, when taken together with Poloz's more cautious tone this week, the case for additional monetary tightening in the very near-term does look somewhat weaker.

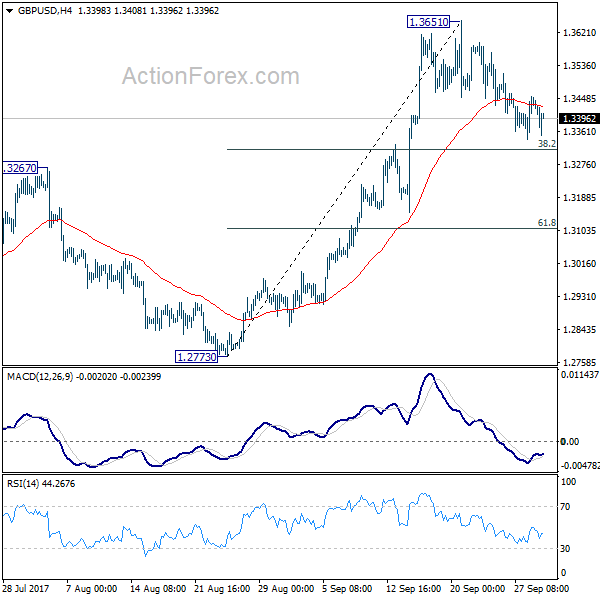

GBPUSD Tests Support on GDP Revision

The British pound has moved below the 1.3400 level against the U.S dollar during the European trading session, hitting 1.3353, after the United Kingdom's second quarter annual gross domestic product figure was revised lower to just 1.3 percent.

Intraday trading sentiment surrounding the GBPUSD pair is currently bearish, with the pair risking further losses while price-action remains beneath the 1.3400 level.

Despite the GBPUSD pairs sharp decline after today's negative economic news, solid buying interest from lower levels is still present, with price-action starting to recover bullish momentum.

Furthermore, the GBPUSD pair has so far created a bullish higher daily price low, with buyers coming in just above yesterday's weekly low, at 1.3443.

Key intraday technical resistance is now found at 1.3400 and the daily pivot point, at 1.3413. Above the 1.3413 level, the pair may find a buying surge towards 1.3443 and 1.3504.

To the downside, a higher time-frame price-close beneath the pairs 200-week moving average, at 1.3363 should trigger further intraday losses towards 1.3343 and 1.3300.

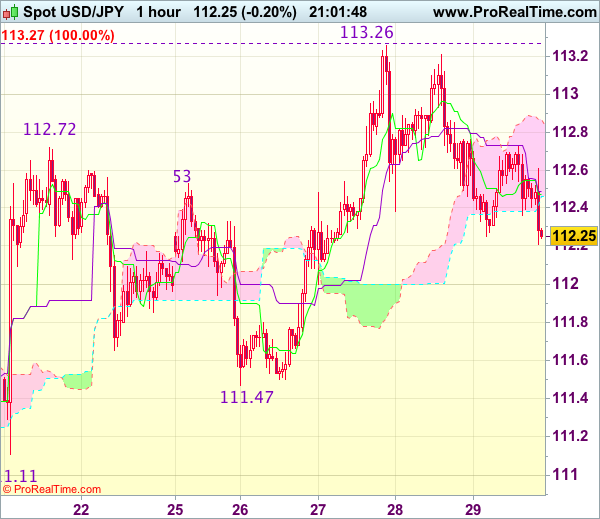

USDJPY Intraday Bearish Below 112.71

The U.S dollar has moved lower against the Japanese Yen, as the greenback retraces to key support, and investors seek further details from the Trump administrations proposed tax reforms.

Today's intraday trading sentiment surrounding the USDJPY is currently bearish, as buying momentum wanes, and the pair fails to trade back above the former weekly price-high, located at the 112.71 level.

With a lack of economic data on the U.S docket, the focus during the U.S session will turn to end of month price-flows and the weekly price close on the USDJPY pair.

Last week the USDJPY closed price above its 200-week moving average, at 111.69, for the first time in 8-weeks. Traders will pay close attention to a bullish, second consecutive weekly price closes above the pairs 200-week MA.

To the downside, key intraday technical resistance is found at the current daily price-low, at 112.27 and the pairs weekly pivot point, at 111.90. Below 111.90, the pair fast approached its 200-week and 200-day moving averages, at 111.69 and 111.46.

Intraday resistance is clearly defined for the USDJPY pair, at 112.71, once above the former weekly high, further bullishness may be seen towards 113.00 and 113.25.

Trade Idea Update: USD/JPY – Stand aside

USD/JPY - 112.32

New strategy :

Stand aside

Position : -

Target : -

Stop : -

Despite falling to 112.38 yesterday, lack of follow through selling suggests further consolidation would take place and recovery to 112.75-80 cannot be ruled out, however, price should falter below indicated resistance at 113.26, bring another retreat later, below 112.20 would signal top has been formed at 113.26, bring retracement of recent rise to 112.00, then 111.75-80 but previous support at 111.47 should remain intact.

On the upside, whilst recovery to 112.75-80 cannot be ruled out, reckon said resistance at 113.26 would hold and bring further consolidation. Only a break of said this week’s high at 113.26 would revive bullishness and signal recent upmove has resumed, then further gain to previous resistance at 113.58 would follow but loss of upward momentum should prevent sharp move beyond 113.75-80 and reckon 114.00-10 would remain intact. As near term outlook is mixed, would be prudent to stand aside for now.

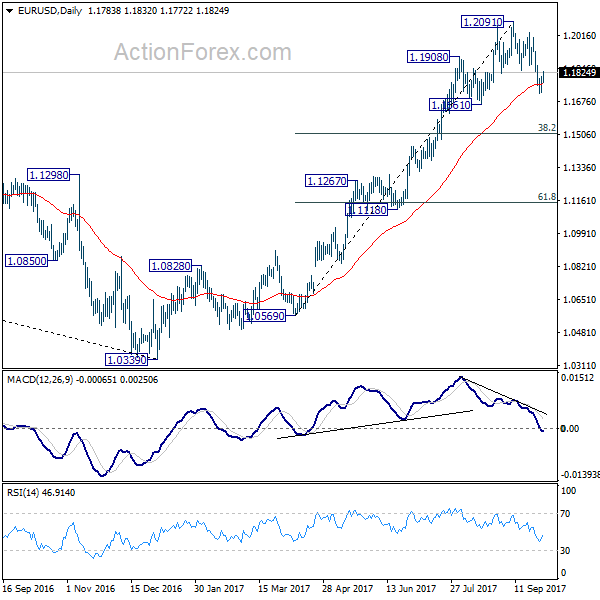

EUR/USD Mid-Day Outlook

Daily Pivots: (S1) 1.1736; (P) 1.1770 (R1) 1.1820; More...

Intraday bias in EUR/USD remains neutral for the moment and some sideway trading could be seen above 1.1716 temporary low. Deeper fall is expected as long as 1.2029 resistance holds. Decline from 1.2091 is seen as correcting whole rise from 1.0569. Below 1.1716 will target 1.1661 support and then 38.2% retracement of 1.0569 to 1.2091 at 1.1510, where we're expecting support to bring rebound.

In the bigger picture, rise from medium term bottom at 1.0339 is still in progress for 38.2% retracement of 1.6039 (2008 high) to 1.0339 (2017 low) at 1.2516. However, it should be noted that there is no confirmation of trend reversal yet. That is, such rebound from 1.0399 could be a correction. And the long term fall from 1.6039 (2008 high) could resume. Hence, we'd be cautious on strong resistance from 1.2516 to limit upside. But after all, break of 1.1661 is needed to indicate medium term topping. Otherwise, outlook will remain bullish in case of pull back.

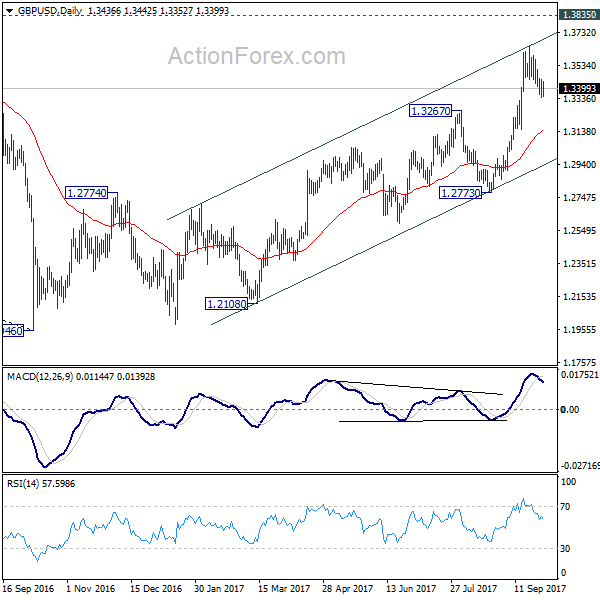

GBP/USD Mid-Day Outlook

Daily Pivots: (S1) 1.3370; (P) 1.3413; (R1) 1.3483; More....

No change in GBP/USD's outlook. Correction from 1.3651 could extend. But we'd continue to expect strong support from 38.2% retracement of 1.2773 to 1.3651 at 1.3316 to contain downside and bring rally resumption. Break of 1.3651 will turn bias back to the upside for 1.3835 support turned resistance next. Break there will target 55 month EMA (now at 1.4405).

In the bigger picture, current development argues that the long term trend in GBP/USD has reversed. That is, a key bottom was formed back in 1.1946 on bullish convergence condition in monthly MACD. Current rise from 1.1946 will target 38.2% retracement of 2.1161 (2007 high) to 1.1946 (2016 low) at 1.5466 next. In any case, medium term outlook will now stay bull

USD/JPY Mid-Day Outlook

Daily Pivots: (S1) 111.99; (P) 112.59; (R1) 112.94; More...

Outlook is unchanged in USD/JPY even though it continues to lose upside momentum. But still, with 111.46 minor support intact, further rise is expected. Sustained break of medium term channel resistance will argue that correction from 118.65 is already completed with three waves down to 107.31. Break of 114.49 will confirm this bullish case and target a test on 118.65 next. On the downside, however, break of 111.46 will suggest rejection from the channel resistance and turn bias back to the downside.

In the bigger picture, rise from 98.97 (2016 low) is seen as the second leg of the corrective pattern from 125.85 (2015 high). It's unclear whether this this second leg has completed at 118.65 or not. But medium term outlook will be mildly bearish as long as 114.49 resistance holds. And, there is prospect of breaking 98.97 ahead. Meanwhile, break of 114.49 will bring retest of 125.85 high. But even in that case, we don't expect a break there on first attempt.

US: Spending Down and Inflation Soft in August, as Data Distorted by Hurricanes

Personal income rose 0.2% in August, in line with expectations, but from a downwardly revised 0.3% increase in July. Controlling for inflation and taxes, real disposable personal income edged down 0.1% in the month.

Personal consumption rose by 0.1% in nominal terms (in line with the consensus). In real terms spending fell 0.1%. By component, real spending on durable goods saw the biggest decline, falling 1.0%. Nondurable goods also fell 0.2%, while services edged up 0.1%.

The PCE price deflator rose 0.2% month-on-month (below consensus for 0.3%), while the core PCE deflator ticked up just 0.1%. Year-on-year, PCE inflation was up 1.4%, while the core rate decelerated to 1.3%.

Key Implications

The consumer appears to have lost some momentum after a strong second quarter. However, we have to take this report with a grain of salt given the distortionary impact of Hurricane Harvey. The negative impact could continue through September, before spending gets a lift as rebuilding begins. So, it will be a few months before we get a clear read on the state of household spending.

Having said that the broader outlook for U.S. consumers remains positive. With few signs of a slowdown in the pace of job growth and increasing evidence of accelerating wage growth, household spending should continue to support demand growth.

The continued deceleration in inflation (as measured by the price deflator for personal consumption) is notable. Core pries in particular did not show any of the acceleration recorded in the CPI measure in August. While Chair Yellen noted this week that the Fed does not have to see inflation reach 2.0% before raising interest rates, she was also at a loss to fully explain its recent weakness. Signs that inflation is deteriorating further casts some doubt on the Fed's plans for a December hike.

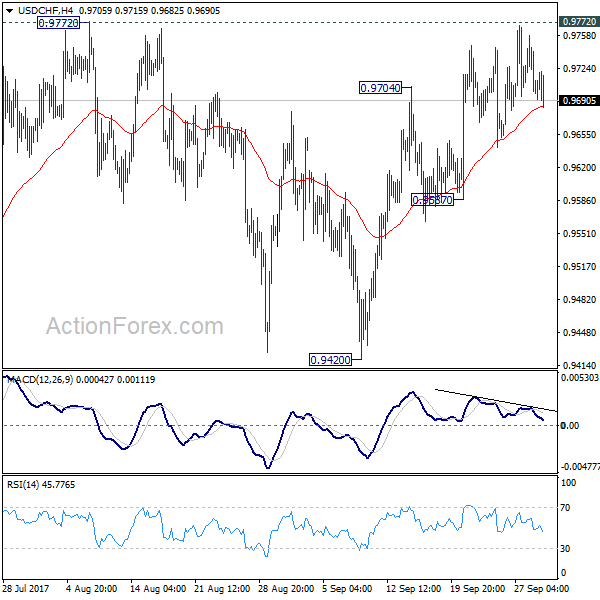

USD/CHF Mid-Day Outlook

Daily Pivots: (S1) 0.9679; (P) 0.9718; (R1) 0.9740; More....

USD/CHF continues to gyrate lower today but overall outlook is unchanged. On the upside, decisive break of 0.9772 key resistance will suggest that whole down trend form 1.0342 has completed. In that case, near term outlook will be turned bullish for 0.9860/1.0099 resistance zone. Nonetheless, with 0.9772 resistance intact, outlook remains bearish. Below 0.9587 minor support will turn bias back to the downside for retesting 0.9420 low.

In the bigger picture, focus remains on whether 0.9443 key support (2016 low) could be taken out firmly as down trend from 1.0342 extends. There are various interpretation of the price actions. But in any case, medium term outlook will stay bearish as long as 0.9772 resistance holds. Current down trend could extend to 38.2% retracement of 0.7065 (2011 low) to 1.0342 (2016 high) at 0.9090. However, break of 0.9772 will indicate that USD/CHF has successfully defended 0.9443 again and turn outlook bullish for 1.0099 resistance.

Dollar Pullback Continues as Inflation Reading Missed Expectations

Dollar weakens pare gains as markets are heading to weekly close. In particular, Swiss Franc has overtaken Dollar's place as the strongest one for the week. Economic data from US are providing little boost for the greenback. Instead, tamer than expected inflation is weighing mildly on Dollar. And traders should be taking profit at quarter end, and ahead of next week's employment data. Meanwhile, some more time is needed to reassess the impact of US President Donald Trump's tax plan, before traders take a more decisive stance. US personal income rose 0.2% in August, spending rose 0.1%, in line with consensus. Headline PCE was unchanged at 1.4% yoy while core CPI slowed to 1.3% yoy. Both were below expectations. From Canada, GDP rose 0.0% in July, below expectation of 0.1% mom. IPPI rose 0.3% while RMPI rose 1.0% mom in August.

BoE Carney affirms rate hike in "relatively near term"

BoE Governor Mark Carney said in a BBC radio interview that "if the economy continues on the track that it's been on, and all indications are that it is, in the relatively near term we can expect that interest rates would increase somewhat." That is affirming to the view that BoE will hike in the next MPC meeting in November. Carney also noted that there is a "speed limit" for UK's growth. Brexit will be as immigration slows and investment in capacity being held off, the economy will not be able to grow as fast as before, without pushing up inflation. And, "if the speed limit has slowed and we're in a position where we've used up a lot of the capacity in this economy ... it means that we should be thinking about, and we are open about this, we're thinking about taking our foot a bit off the accelerator."

Released from UK, Q2 GDP growth was finalized at 0.3% qoq, 1.5% yoy. Current account deficit widened to GBP -16.9b in Q2. Mortgage approvals dropped to 67k in August. M4 money supply rose 0.9% mom in August. Index of services rose 0.5% 3mo3m in July. Gfk consumer sentiment improved to -9 in September.

Macron won Merkel backing on EU reforms

In Eurozone, German Chancellor Angel Merkel hailed French President Emmanuel Macron's proposals on EU reforms. She said that Macron's ideas could be the foundation for an "intense" Franco-German cooperation on the future of Europe. And, Merkel noted that "as far as the proposals were concerned, there was a high level of agreement between German and France. We must still discuss the details, but I am of the firm conviction that Europe can't just stay still but must continue to develop." Meanwhile, Macron said after an EU summit dinner that "we're all convinced Europe must move ahead faster and stronger, for more sovereignty, more unity and more democracy."

Released from Eurozone, CPI was unchanged at 1.5% yoy in September, below expectation. Core CPI dropped to 1.1% yoy in September, below expectation of 1.2%. German unemployment dropped -23k in September. German unemployment rate dropped to 5.6%, hitting the lowest level since the data series began in January 1992. German retail sales dropped -0.4% mom in August. Also from Europe, Swiss KOF leading indicate rose to 105.8 in September.

One BoJ member called for expanding stimulus

Summary of opinions in the September BoJ meeting showed that one policymaker called for expanding monetary stimulus. Meanwhile, all other nine-members were in consensus to maintain the current program. The dovish member was quoted saying that "it's necessary to stimulate demand further with additional monetary easing to achieve and stabilize inflation at the BOJ's target, given a scheduled sales tax hike in October 2019." The dissenting member was not named in the summary, but it's rather clear that the meeting statement showed newcomer Goushi Kataoka dissented last time. And Kataoka is widely known as a dove that advocates aggressive easing. The summary also showed concerns over escalating tensions between US and North Korea. One member was quoted saying that "if geopolitical risks heighten further, the BOJ must be ready to consider taking necessary policy adjustments to prevent deflationary mindset from re-emerging."

Released from Japan, National CPI core accelerated to 0.7% yoy in August, up from 0.5% yoy. Tokyo CPI core rose to 0.5% yoy, up from 0.4% yoy. Unemployment rate was unchanged at 2.8%, household spending rose 0.6% yoy, retail sales rose 1.7% yoy, industrial production rose 2.1% mom. Housing starts dropped -20% yoy in August.

USD/CHF Mid-Day Outlook

Daily Pivots: (S1) 0.9679; (P) 0.9718; (R1) 0.9740; More....

USD/CHF continues to gyrate lower today but overall outlook is unchanged. On the upside, decisive break of 0.9772 key resistance will suggest that whole down trend form 1.0342 has completed. In that case, near term outlook will be turned bullish for 0.9860/1.0099 resistance zone. Nonetheless, with 0.9772 resistance intact, outlook remains bearish. Below 0.9587 minor support will turn bias back to the downside for retesting 0.9420 low.

In the bigger picture, focus remains on whether 0.9443 key support (2016 low) could be taken out firmly as down trend from 1.0342 extends. There are various interpretation of the price actions. But in any case, medium term outlook will stay bearish as long as 0.9772 resistance holds. Current down trend could extend to 38.2% retracement of 0.7065 (2011 low) to 1.0342 (2016 high) at 0.9090. However, break of 0.9772 will indicate that USD/CHF has successfully defended 0.9443 again and turn outlook bullish for 1.0099 resistance.

Economic Indicators Update

| GMT | Ccy | Events | Actual | Forecast | Previous | Revised |

|---|---|---|---|---|---|---|

| 21:45 | NZD | Building Permits M/M Aug | 10.20% | -0.70% | -1.70% | |

| 23:01 | GBP | GfK Consumer Confidence Sep | -9 | -11 | -10 | |

| 23:30 | JPY | Unemployment Rate Aug | 2.80% | 2.80% | 2.80% | |

| 23:30 | JPY | Household Spending Y/Y Aug | 0.60% | 0.90% | -0.20% | |

| 23:30 | JPY | National CPI Core Y/Y Aug | 0.70% | 0.70% | 0.50% | |

| 23:30 | JPY | Tokyo CPI Core Y/Y Sep | 0.50% | 0.50% | 0.40% | |

| 23:50 | JPY | BOJ Summary of Opinions Sept.20-21 Meeting | ||||

| 23:50 | JPY | Retail Trade Y/Y Aug | 1.70% | 2.40% | 1.90% | 1.80% |

| 23:50 | JPY | Industrial Production M/M Aug P | 2.10% | 1.80% | -0.80% | |

| 05:00 | JPY | Housing Starts Y/Y Aug | -2.00% | 0.60% | -2.30% | |

| 06:00 | EUR | German Retail Sales M/M Aug | -0.40% | 0.50% | -1.20% | -0.60% |

| 07:00 | CHF | KOF Leading Indicator Sep | 105.8 | 105.5 | 104.1 | 104.2 |

| 07:55 | EUR | German Unemployment Change Sep | -23K | -5K | -5K | -6K |

| 07:55 | EUR | German Unemployment Rate Sep | 5.60% | 5.70% | 5.70% | |

| 08:30 | GBP | Current Account (GBP) Q2 | -23.2B | -15.8B | -16.9B | |

| 08:30 | GBP | Mortgage Approvals Aug | 67K | 67K | 69K | |

| 08:30 | GBP | M4 Money Supply M/M Aug | 0.90% | 0.20% | 0.50% | |

| 08:30 | GBP | GDP Q/Q Q2 F | 0.30% | 0.30% | 0.30% | |

| 08:30 | GBP | GDP Y/Y Q2 F | 1.50% | 1.70% | 1.70% | |

| 08:30 | GBP | Index of Services 3M/3M Jul | 0.50% | 0.70% | 0.50% | |

| 09:00 | EUR | Eurozone CPI Estimate Y/Y Sep | 1.50% | 1.60% | 1.50% | |

| 09:00 | EUR | Eurozone CPI - Core Y/Y Sep A | 1.10% | 1.20% | 1.20% | |

| 12:30 | CAD | GDP M/M Jul | 0.00% | 0.10% | 0.30% | |

| 12:30 | CAD | Industrial Product Price M/M Aug | 0.30% | 0.50% | -1.50% | -1.60% |

| 12:30 | CAD | Raw Materials Price Index M/M Aug | 1.00% | 0.30% | -0.60% | -0.90% |

| 12:30 | USD | Personal Income Aug | 0.20% | 0.20% | 0.40% | 0.30% |

| 12:30 | USD | Personal Spending Aug | 0.10% | 0.10% | 0.30% | |

| 12:30 | USD | PCE Deflator M/M Aug | 0.20% | 0.30% | 0.10% | |

| 12:30 | USD | PCE Deflator Y/Y Aug | 1.40% | 1.50% | 1.40% | |

| 12:30 | USD | PCE Core M/M Aug | 0.10% | 0.20% | 0.10% | |

| 12:30 | USD | PCE Core Y/Y Aug | 1.30% | 1.40% | 1.40% | |

| 13:45 | USD | Chicago PMI Sep | 58.7 | 58.9 | ||

| 14:00 | USD | U. of Michigan Confidence Sep F | 95.3 | 95.3 |