Sample Category Title

Income and Consumption Weakens in August

After a relatively strong start to the third quarter, personal income and spending weakened in August, increasing 0.2 percent and 0.1 percent, respectively. In real terms, spending declined 0.1 percent.

Weaker Income and Consumption

Personal income increased only 0.2 percent in nominal terms while disposable personal income increased 0.1 percent in August. However, real disposable personal income declined 0.1 percent due to higher inflation during the month. Income was particularly weak in August, only increasing $28.6 billion compared to $56.1 billion in July. Compensation of employees increased only $6.2 billion during the month compared to $47.9 billion in July. Particularly, wages and salaries increased only $3.3 billion. Of this, private industry wages and salaries were up $1.3 billion while government wages and salaries increased $2.0 billion. Compare this with an increase of $40.0 billion for private wages and salaries in July and a similar increase of $2.0 billion for government wages and salaries in July.

Personal current transfers increased by $9.6 billion during the month compared to only $5.6 billion in July. The biggest difference within personal current transfers was an increase of $5.2 billion in "other" transfers compared to a decline of $1.1 billion in July. This is, perhaps, a consequence of some of the early effects of the hurricanes affecting Florida and Texas.

Meanwhile, August personal consumption expenditures increased only 0.1 percent in nominal terms after increasing 0.3 percent in July while real personal consumption expenditures also declined 0.1 percent after inching higher, by 0.2 percent, in July. The biggest difference compared to July was a $16.3 billion decline in durable goods consumption, which almost erased the $16.5 billion increase in durable goods consumption in July. On the other hand, services consumption was robust in August, increasing $26.7 billion in August after a $20.7 billion increase the previous month.

GDP Growth Will Probably Downshift in Q3

With the release of personal income and spending for August it is clear that both of these numbers will not contribute to a repeat of the strong performance we saw in GDP during the second quarter of the year. Although we may see a rebound in September, it is probably not going to be enough to override the weakness we saw in August.

Furthermore, although price pressures remained contained during the month, with the PCE price index increasing 0.2 percent in the month while the core PCE inched up only 0.1 percent, the weak performance of both nominal income and consumption growth numbers pushed the real numbers into negative territory, which will put downward pressure on real overall numbers for GDP in Q3.

Thus, even with an expected rebound in the September real consumer spending numbers, we see downside risk to our call for real consumer spending in Q3.

Week Ahead – US Jobs Report and ISM PMIs Eyed as Dollar Rallies Again; RBA Meets

The US dollar just had its most positive week of 2017, driven by firming expectations of a December rate hike. Data out of the US next week will therefore be watched very carefully for further evidence supporting this view. Also coming under the limelight next week is the Reserve Bank of Australia, which meets for a scheduled monetary policy meeting, while Canadian employment figures, ECB meeting minutes, UK PMIs and the Bank of Japan's Tankan survey will too be watched by traders.

RBA expected to hold rates unchanged

The RBA last cut rates back in August 2016 to 1.50% where they've stood since. After some concerns about the strength of the economy in the early part of this year, growth rebounded sharply in the second quarter and all the indications are that this trend continued into the third quarter as the labour market improved and consumption accelerated. However, the RBA has been cautious in signalling that a rate hike may be nearing out of worries that it would trigger a rally in the Australian dollar, which is already up almost 9% against the greenback so far this year. The central bank will likely hold rates and maintain its neutral bias when it meets on Tuesday, while sounding upbeat about the country's growth prospects. Data releases out of Australia next week will also be in focus, including building approvals on Tuesday, and retail sales and trade figures on Thursday, all for August.

Bank of Japan Tankan survey stands out in quiet week for Asian markets

It will be a relatively quiet trading week in Asia in the coming seven days, as the Chinese market will be closed for the entire week for National Day celebrations, while South Korean and Hong Kong markets will also be closed for more than one day next week. This leaves the Bank of Japan's Tankan survey as the main data release out of Asia next week. The Tankan survey for the third quarter is forecast to show improving outlook for large manufacturing and non-manufacturing companies, but business sentiment for smaller firms will likely remain unchanged from the second quarter. Third quarter estimates for capital expenditure are forecast to show slightly higher growth in spending by large firms (from 8% to 8.3%) and a much lesser reduction in spending by smaller firmer than in the previous estimate (from -20.6% to -13.8%).

ECB meeting minutes eyed as QE exit plan still unclear

Economic data out of the Eurozone next week will include the euro area's unemployment rate on Monday, producer prices on Tuesday, retail sales on Wednesday and German industrial orders on Friday. The final September PMI readings for the region by IHS Markit are also due next week but the main focus will likely be on the European Central Bank's account of the September policy meeting. Although the ECB has strongly signalled an announcement on tighter policy at its upcoming October meeting, it has also indicated it is not ready to completely pull the plug on its stimulus program. The September meeting minutes should help provide some additional clarity on policymakers' thinking and what to expect at the next meeting on October 26.

Canadian jobs report awaited amid data-dependent BoC

After not-so-hawkish comments by the Bank of Canada's governor, Stephen Poloz this week, as well as disappointing monthly GPD data, expectations of a third rate by the BoC this year have been somewhat dampened. Next week's Canadian data will likely be scrutinized for further clues as to the timing of the next rate rise. The September employment report is due on Friday and will be followed by the Ivey PMI, also for September. Before that, trade figures will be watched on Thursday. In the meantime, the Canadian dollar has been languishing at one-month lows against its US counterpart, as it catches its breadth from the strong rally seen since May.

UK PMIs unlikely to alter outlook on economy

As the Bank of England prepares to raise interest rates for the first time in a decade, the British economy remains stuck in low gear. The Bank may take little notice of next week's PMI reports from IHS Markit, as it's more concerned about the inflation overshoot and rising household debt. However, they could still have an impact on sterling as they should be a good indication to how the economy performed at the end of the third quarter. The manufacturing PMI, out on Monday, is forecast to ease from 56.9 to 56.4 in September. The construction PMI will follow on Tuesday and is expected to decline from 51.1 to 50.8, while the services PMI, due on Wednesday, is forecast to remain unchanged at 53.2.

Nonfarm payrolls and ISM PMIs to dominate

It will be another packed week for US data, dominated of course by the latest jobs report and the all-important ISM PMIs. The ISM's manufacturing PMI is up first on Monday and is expected to moderate from 58.8 to 57.5 in September. On Wednesday, the ADP's private employment report should provide a glimpse as to what to expect from Friday's official report. Also out on Wednesday is the ISM non-manufacturing PMI, which is forecast to decline from August's 57.5 to 55.8 in September. However, both the manufacturing and non-manufacturing PMI's remain comfortably above the 50-expansion level, suggesting the US economy ended the third quarter on solid footing. August factory orders will follow on Thursday, along with trade data.

On Friday, all eyes will be on the nonfarm payrolls report as investors reassess their positions on the greenback, following the dramatic shift in sentiment for the US currency after the September 19-20 FOMC meeting. Nonfarm payrolls are forecast to rise by just 130k in September as the hurricanes hitting the US east coast likely slowed job creation during the period. The jobless rate is expected to remain steady at 4.4% in September, while average earnings are forecast to pick up pace slightly, from 2.5% to 2.6% year-on-year.

Weekly Market Outlook: CAD Looks Exposed

- RBA to Keep Rates Unchanged - Peter Rosenstreich

- Mario Draghi Does Not Threaten Bitcoin - Yann Quelenn

- CAD Looks Exposed - Peter Rosenstreich

- China Online

FX Market - RBA to Keep Rates Unchanged

We anticipate that the Reserve Bank of Australia (RBA) will leave key interest rate at 1.50% while maintaining its neutral policy stance. On the economic front the economy has expanded in 2Q by a healthy 0.8% q/q, indicating that GDP growth in 2017 will likely hit the higher end of the central banks forecast. The labor markets, which remain a concern for the RBA as unemployment ticked higher in the early part of the year, is now has trending lower. Australia unemployment rates has fallen to a 3-year low at 5.60%. Yet, inflation remains weak as 2Q printed at 1.9% y/y, below the RBA's target range of 2-3%. Concern over the soft inflation outlook was amplified as AUD strengthen, causing policymakers to voice their displeasure over the last two meetings.

The strong currency was seen as a drag on the economy, through higher commodity price but slowed momentum of inflation via imports. The fall in AUD over the last two weeks has not eased the RBA thinking that the currency was the primary risk factor. The RBA need to see a clear trend of AUD weakness before hinting that tighter monetary policy is coming. Higher US treasury yields have affected yield sensitive currencies in the G10 and EM. Pause in the rise of US interest rates has given AUD bulls time to recovery but not much else. In addition renewed weakness in iron ore futures has also hurt AUD. AUDUSD need to close below 0.7807/10 support to establish extension of current correction phase.

Elsewhere, the RBNZ languages around the NZD was slightly less aggressive stating, deprecation"would help" and "increase tradable inflation and deliver more balanced growth." RBNZ left the OCR at 1.75% for the 6th consecutive meeting and seems in no hurry to increase rates. With strong economic developments and monetary tightening that will materialize in late 2017 AUD, EUR and GBP should outperform NZD in the near futures.

Economics - Mario Draghi Does Not Threaten Bitcoin

This was one comment that seems at first sight very bullish for the bitcoin, the most famous digital currency. Earlier last week Mario Draghi, in its statements to the European Parliament's Committee on Economic and Monetary Affairs has mentioned that the European Central Bank has not the mandate to prohibit or regulate Bitcoin. There is now not a single week without at least a mention of the cryptocurrency. Out of this comment, the price has gotten a boost and is back above $4000.

For the time being, it turns out that big institutions are not in a hurry to regulate. Yet, we believe that the power of money creation is one very important power that are not going to be given up. Cryptocurrencies remain unregulated at the moment but, ironically, new derivatives are going to be introduced by next year on the Bitcoin and should, by the way, likely weigh on prices. Story repeats itself and gold price has been driven lower by paper contracts. The ratio between paper and physical is currently higher than 200 according to the latest disclosure from the CME. One can perfectly imagine what impact it may trigger when derivatives are going to be introduced on Bitcoin.

Right now, the Bitcoin price is holding above $4000 and there are consistent upside pressures. The price is likely to rise again. We do not consider that this is a "tulip mania" the bubble name of the hyperinflation that occurred in Netherlands. It is rather another way to store wealth. The debate is still open regarding this question but there is something that we know for sure. The bitcoin price is not in a bubble, there are plenty of upside for the digital currency. It is just a matter of time before we get back above $5000.

Economics - CAD Looks Exposed

Bank of Canada was one of the first Central Banks to honor the thinking that inflation would no longer the primary determinate of interest rate policy. The banks unexpected 25bp hike on 6th September policy meeting, backed up the talk with real action and caught the market short CAD. Since then the pace of the BoC tightening cycle has been hotly debated. A combination of rising US yields and comments by the BoC policymakers stalled the USDCAD downwards trajectory. Whether the short squeeze is a lasting trend or merely a temporary distortion will be based on external events but also Canadian policymakers comments.

Governor Poloz's assertion that their interest rate path is not preordained and data depended, is a common central bank tactic. However, the tone of his speech indicated that a pause is more probably than a follow-up hike in October. Governor Poloz stated there was "is no predetermined path" for rates, policy will be "particularly data dependent" and the BoC will "feel" its way through policy development. Despite nothing new in these comments, Governor Poloz cautious tone suggests a shift from hawkishness and a pause in the BoC tightening cycle after back-to-back hikes. Given the change in language and softening in broader economic data we have penciled the next move in December.

USDCAD has become increasingly sensitive to disappointing economic data indicating the uncertainty around the BoC policy path. Positive USD sentiment, repricing of the Fed policy path and increasingly expectations for US tax reform has given the USD a new lease on life. Given our expectations for higher US rates, US-Canada yields spread is likely to widen benefiting USD. In the mid-term we become more optimistic on Cad but for right now we would remain long USDCAD for a test of 1.26/1.27.

Themes Trading - China Online

Chinese stocks are still reeling from the all-out collapse of local equity markets. Yet while valuations have suffered, the fundamentals remain enticing.

China is undisputedly the largest internet market in the world in terms of its user base, with 620 million users -nearly double that of India and triple that of the USA. Yet the penetration rate is only 45%, compared with 84% for the USA, which means there is significant room for growth. According to Kantar Retail, China has become the world's largest e-commerce market, with sales of $589 billion in 2015. China has developed its own online offering catering to the country's unique culture. Western companies have had a challenging time breaking into the market due to structural and cultural issues. The result has been the incubation of innovative world-class private enterprises. As China shifts from investment- to consumption-led growth, these agile entrepreneurs will also benefit from support and protection from Beijing. With valuations in the single digits, these names offer significant upside potential.

For this theme, we included social media, search engines, retail and B2B commerce, travel and key hardware manufacturers.

Australia & New Zealand Weekly: RBA on hold in October

Week beginning 2 October 2017

- RBA on hold in October: to repeat growth overview from last month.

- Australia: CoreLogic home value index, dwelling approvals, retail sales, trade balance.

- NZ: survey of business opinion.

- China: foreign reserves, FDI.

- Euro Area: ECB minutes, unemployment.

- US: Fed Chair Yellen speaks, nonfarm payrolls.

- Key economic & financial forecasts.

Information contained in this report was current as at 29 September 2017

RBA on hold in October: to repeat growth overview from last month

The Reserve Bank Board meets next week on October 3.

There will be no change to the cash rate. As with recent meetings, the interest will be in the Governor's commentary.

In fact, we don't envisage too much change in the key themes:

- "conditions in the global economy are continuing toimprove".

- "growth in the (Australian) economy will gradually pick upover the coming year".

- "the outlook for non-mining investment has improved".

- "residential construction remains at a high level, but littlefurther growth is expected."

- "slow growth in real wages and high levels of household debtare likely to constrain future growth in spending".

- "the unemployment rate is expected to decline a little overthe next couple of years".

- "stronger conditions in the labour market should see somelift in wages over time".

- "an appreciating exchange rate would be expected to resultin a slower pick-up in economic activity and inflation thancurrently forecast".

- "there are signs that conditions (housing) are easing,especially in Sydney".

- "growth in housing debt has been outpacing the slow growthin household incomes".

- "the Board judged that holding the stance of monetarypolicy unchanged... would be consistent with sustainablegrowth in the economy and achieving the inflation targetover time".

These assessments are consistent with a neutral policy bias.

Markets and many banks expect this bias to change by year's end to a tightening bias.

We expect the cash rate will remain on hold over the course of 2017, 2018 and 2019. We point out that the RBA has a very different growth outlook for the Australian economy and Australia's trading partners than our own. The RBA expects growth in Australia to be 3.25% in 2018 and 3.5% in 2019 (above trend of 2.75%). Westpac expects a below trend pace of 2.5% in both years.

The RBA is also forecasting 2% underlying inflation in 2017 and 2018 (bottom of target band) to be followed by 2.5% in 2019. Underlying inflation is currently running at 1.8% (to June) and the upcoming revised weights (to be applied from the December quarter) are likely to reduce annual underlying inflation by 0.2- 0.3% over the course of 2018. Once these weights are released the Bank might have to reconsider its base case (1.5%-2.5%) for 2018.

While the RBA does not provide detailed forecasts outside growth and inflation, the RBA Governor's likely comments, as set out above, point to a more confident outlook for wages growth; employment; non-mining investment and the residential construction cycle than we are seeing.

A major puzzle for central banks globally has been the limited response of wages to stimulatory monetary policies since the GFC.

Despite these policies in the US; Germany; the UK and Japan driving labour markets to near or full employment, wages have failed to respond. Explanations for this phenomenon have been structural: globalisation; technology; retiring higher paid baby boomers; low productivity growth; an absence of pricing power for employers; low inflation and wage expectations; high risk aversion following the GFC and job insecurity in the face of technology threats.

Consistent with that global theme, wages growth in Australia has also been weak. Australia's wage price index has increased by 1.9% over the last year compared to average growth of 3.5%. The unemployment rate has held in the 5.5%-6.0% range compared to a generally accepted full employment rate in Australia of 5%. Australia had also been raising wages at a faster pace over the last 20 years than other developed countries, exacerbating our lack of competitiveness and further containing our wage growth prospects.

This weak wages performance has lowered annual real income growth to 0.6% while real consumption growth has held around 2.5%. Households will need to protect their fragile savings rate and pressures will emerge on consumer spending. The Reserve Bank seems to recognise this effect, but by assuming faster jobs and wages growth, they are likely to be factoring in faster income growth than we are expecting. Other pressures are impacting households - rising energy prices; record high debt levels and political uncertainty. The latter effect will work through the business sector as businesses restrain employment and investment until political clarity is achieved following the 2019 election. It seems likely that the Bank has a much more optimistic outlook for non-mining investment than we are expecting.

Markets and the RBA may be underestimating the impact on the interest rate sensitive housing market of developments which are unfolding without official rate hikes.

The four majors (90% of the mortgage market) have been raising investor and interest only mortgage rates while applying tighter lending guidelines. House price inflation is slowing and regulators are unlikely to have any patience with a reversal of this trend. We expect that if we did see reversals, the RBA is more likely to embrace a further round of macro-prudential tightening than embark on a new tightening cycle.

To that point, six month annualised house price inflation (CoreLogic data) in Sydney has slowed from 22.4% in January to 4.8% in August. We observed a similar response to macroprudential policies in 2015/16 when six month annualised house price inflation slowed from 25% (July 2015) to -4.4% (April 2016), although rate cuts in 2016 reversed that trend.

Housing activity is also slowing despite a steady cash rate. Other factors, specifically relating to foreign investors, have turned the cycle. High rise building approvals have tumbled by 40% in the last year. This has been particularly due to investment restrictions in China; lending constraints by banks; and sharp increases in state government stamp duties for foreign investors. This downturn is likely to continue for at least a further two years as foreign developers unwind commitments and local developers await more affordable development sites.

While markets are currently captivated by expectations of a coordinated lift in global growth, we are more circumspect with respect to Australia's trading partners. After tightening his grip on power next month, China's leader, Chairman Xi, will focus on risks associated with the credit excesses since the GFC. Tighter credit conditions will slow China's growth rate - we forecast a growth slowdown from 6.7% in 2017 to 6.2% in 2018.

Bill Evans, Chief Economist

New Zealand: Week ahead & Data Wrap

Behind closed doors

Post-election negotiations between the major political parties mean that the form of the next Government - and hence the mix of economic policy - won't be known to the public for another couple of weeks. Meanwhile, the Reserve Bank largely stuck to its lines in this week's OCR review, but hinted at a more substantial change to its forecasts in the November Monetary Policy Statement.

As expected, New Zealand's general election delivered no clear outcome. Neither the incumbent centre-right National Party, nor the centre-left bloc of the Labour and Green Parties, has the numbers to form a government. This leaves the centrist and nationalist NZ First Party in a monarch-maker position.

NZ First leader Winston Peters has said that he won't be making any decisions before 7 October, when the special vote count is expected to be announced. Special votes include late enrolments and people voting outside their electorates (including university students). These votes tend to skew left; in the last few elections, National have lost a seat and the Greens have gained a seat once the special votes are incorporated. The high number of special votes this time (about 15% of the total) means that National may even lose a second seat to Labour or the Greens. Such an outcome would not change the balance of power, but it might make a Labour/Green/NZ First agreement less vulnerable, as it would give them more than the oneseat majority that the current voting results suggest.

With negotiations going on behind closed doors, we won't have confirmation of the form of the next Government for another couple of weeks at least. For the record, we view a National/NZ First deal as the more likely outcome, in part because a two-way combination is likely to prove more workable than a three-way one.

A National/NZ First government would have fewer implications for our economic forecasts, but we can already identify a few policy areas where changes are likely to be on the table:

Immigration: A key NZ First policy platform is to tighten immigration restrictions - Peters has stated he would prefer net immigration of 10,000 per annum, compared to over 70,000 per annum presently. Net immigration has already started to fall, and we are already forecasting that it will drop to 20,000 by the end of 2020. If some policy change prompted us to forecast a steeper decline in net immigration, we would also consider reducing our GDP growth forecast.

House prices: We suspect that the housing market would initially react positively to a National/NZ First Government - that is, turnover would pick up and prices would be higher than otherwise. It's true that tighter limits on immigration would reduce expected future demand for housing. But we think that this effect would be outweighed by a 'relief rally', given the potential impact on house prices that Labour's proposed tax changes might have had.

Beyond the near term, though, financial factors such as interest rates and macroprudential lending restrictions will once again hold sway over house prices. There have been some small reductions in mortgage rates in recent weeks as bank funding conditions have improved. But without a more substantial fall in mortgage rates, we think the housing market will turn subdued again over the course of next year.

Monetary policy: NZ First favours changing the Reserve Bank Act with an eye to generating a more exporter-friendly exchange rate. National favours the status quo of inflation targeting, and is unlikely to give any ground on that. However, NZ First's presence in government does make some sort of change at the Reserve Bank more likely - for example, a change from the present single-decision maker structure to a committee for monetary policy decisions.

Fiscal policy: NZ First's policies are expensive, and it has not signed up to any budget responsibility agreement. In the first instance we would expect that policy concessions to NZ First, such as its various regional development priorities, could be managed within the Government's existing budget. However, the direction of risk on fiscal policy is that this Government will hew towards smaller surpluses and more debt than otherwise.

It's unclear what impact this policy mix would have on inflation pressures and the Official Cash Rate. However, longer-term interest rates may rise slightly if projections for fiscal surpluses are lowered and for public debt are raised.

Turning to the Reserve Bank itself, this week's OCR Review was much as we expected. The OCR was left unchanged at 1.75%, and the press release retained much of the language of previous statements, including the bottom line: "Monetary policy will remain accommodative for a considerable period. Numerous uncertainties remain and policy may need to adjust accordingly."

However, there were some notable changes in the details, the most important being a downgrade to the RBNZ's growth outlook. The RBNZ said that "growth is projected to maintain its current pace going forward." This is clearly weaker than the RBNZ's previous statement that "growth is expected to improve going forward." Construction activity has been weaker than expected in recent quarters, something that has also prompted us to revise down our GDP growth forecasts. The RBNZ also no longer describes population growth as "strong", which may be a veiled acknowledgement of the recent slowdown in net migration.

These comments suggest that the economic forecasts published in the November MPS could be meaningfully different from those in the August MPS. If the most recent quarterly GDP outturn were repeated each quarter, the annual percentage change in GDP would reach 3.2% by June 2018. That compares to the RBNZ's forecast of 3.8% growth in August. Slower growth implies a slower return to potential output, less inflation pressure, and a lower interest rate path than otherwise.

Weaker growth could be offset to some degree by a lower exchange rate, which has been lower than was assumed in the August MPS. If the decline in the currency persists, the RBNZ would be able to leave its OCR guidance unchanged. But if the exchange rate fails to fall by enough, the RBNZ may have to downgrade its OCR outlook.

Data previews

Aus Sep CoreLogic home value index

Oct 3, Last: 0.1%, WBC f/c: 0.2%

- The overhauled CoreLogic measures provide a much morereliable guide to price changes. Whereas previously it wouldtake 3-6mths and/or multiple measures to confirm a marketshift, the new series appear to give clear signals on a monthto month basis. As such, and with the CoreLogic estimatesalready provided much earlier than other measures, we willnow be treating these as the 'benchmark' for Australianhouse prices and reporting/previewing on a more regularbasis.

- The index showed a 0.1% gain in Aug, the 3mth annualisedpace slowing abruptly to just 2.5% from 10.2% in May.The daily index points to a similarly subdued 0.2% gain inSep. Note that Aug and Sep are seasonal highs for pricessuggesting 'underlying' moves are likely small negatives.

Aus Aug dwelling approvals

Oct 3, Last: -1.7%, WBC f/c: 2.0%

Mkt f/c: 1.0%, Range: -3.0% to 3.0%

- Dwelling approvals dipped 1.7% in July, but were coming offan 11.7% jump in June. Approvals are still down 13.9% vs theirhigh a year ago but over recent months have shown signsof stabilisation for high rise and firming across non high risesegments.

- Construction-related housing finance approvals suggestthe lift in non high rise activity gathered steam through themiddle of the year, annual growth lifting above 10%. Whilewe expect high rise approvals to take another leg lower, astrong lift in the considerably bigger non high rise segmentis expected to dominate in the Aug month, producing a 2%rise in approvals overall. Potentially large offsetting movesmake the estimate more uncertain than usual.

Aus RBA policy announcement

Oct 3, Last: 1.50%, WBC f/c: 1.50%

Mkt f/c: 1.50%, Range: 1.50% to 1.50%

- The RBA is certain to leave rates unchanged again atits October meeting. The Bank has left the cash rateunchanged since August last year.

- Over the past year, economic growth has been patchy(albeit with a lift in momentum recently), annual coreinflation is below the target band, there is still significantslack in the labour market, notwithstanding the recent jobssurge, and wages growth is at historic lows.

- With a number of these trends likely to persist, we expectrates to remain on hold throughout 2017 and 2018. However,market pricing is for two rate hikes in 2018.

- The 2018 outlook is critical to the rates debate. The RBA'scentral case forecast is for growth to accelerate to beabove trend in 2018 and into 2019. We are less convinced,expecting growth to slow to below trend in 2018. See page2 for a more detailed discussion.

Aus Aug retail trade

Oct 5, Last: flat, WBC f/c: 0.2%

Mkt f/c: 0.3%, Range: -0.3% to 0.6%

- The August retail report shapes up as a particularlyimportant one for gauging the consumer. Retail sales havestalled through June-July suggesting the Q2 reboundfrom a weather affected Q1 has faded quickly and that'underlying' conditions remain weak. The August update willgive a clearer indication of just how weak.

- Consumer sentiment remained soft in August with financesagain under pressure and consumer caution elevated. Whilethe labour market has seen solid job gains, weak wagesgrowth and structural shifts are seeing a muted impacton incomes. Business surveys also point to weaker retailconditions through July-August although spending on 'nonretail' consumer services still appears to be buoyant. Overallthat suggests a disappointing gain. We expect retail sales tobe up just 0.2% in the month.

Aus Aug trade balance, AUDbn

Oct 5, Last: 0.46, WBC f/c: 0.5

Mkt f/c: 0.9, Range: 0.1 to 1.5

- Australia's trade balance has been in surplus in eight of thepast nine months.

- For August, we expect the trade surplus to remainunchanged at $0.5bn.

- Export earnings are expected to be little changed, -0.2%,reflecting the balance of countervailing forces. The mainplus, the iron ore spot price rose to US$76/t, up from $67.Against that are lower volumes for coal and LNG, as well asa sharp pull-back in rural commodity prices.

- The import bill declines by an anticipated 0.3%, as pricesfall in association with the stronger currency. The Australiandollar made further gains in the month, increasing by 1.6%to 79US¢ and up 0.6% on a TWI weighted basis.

NZ Q3 Survey of Business Opinion

Oct 3, General Business Situation - last: +17.8

- Through the first half of the year, the Quarterly Survey ofBusiness Opinion pointed towards firmness in economicactivity. However, confidence has taken a bit of a knockrecently, with uncertainty around the general electionclouding the outlook. We expect that this will put adampener on the September confidence report, surveyingfor which was conducted in the run up to the election.

- Looking through election related volatility, we'll be keepinga close eye on a number of the survey's key activitygauges. In particular, we'll be watching how activity in theconstruction sector is shaping up, and any headwinds theindustry is highlighting. This sector has been a key driver ofgrowth in recent years. However, we're now seeing growingsigns that momentum in the construction activity is fading.

US Sep employment report

Oct 6, nonfarm payrolls, last 156k, WBC 100k

Oct 6, unemployment rate, last 4.4%, WBC 4.4%

- August nonfarm payrolls surprised to the downside, withonly 156k new jobs created in the month and a cumulative41k in downward revisions to June and July. The BLSreported that Hurricane Harvey had no discernable impacton employment in the month.

- September is likely to be a different story, with manyworkers in affected areas forced to stay away. However,continued robust job growth across the rest of the nationshould beget a moderate positive outcome overall. Notethat weather-affected prints can be subject to materialrevisions. Hence it is best to focus on 3 and 6 monthaverages, both of which continue to show strength.

- Household employment is less affected by the weather, soexpect the unemployment rate to remain unchanged at 4.4%.

Weekly Focus: Strong Economy, Low Rates

Market movers ahead

- In the US, we believe ISM manufacturing data released on Monday is likely to increase to an even higher level in line with regional PMIs.

- Next week's US labour market rep ort will, in our view, be strongly affected by Sep tember's hurricanes and will not reflect underlying labour market strength.

- In the euro area, we expect the unemployment rate to continue to decline but we still observe slack in the labour market due to a lack of productivity growth, low inflation expectations and a still high share of involuntary part-timers.

- At the UK Conservative Party Conference, we expect Theresa May to deliver a speech on Brexit underlining that the UK is leaving the single market and the customs union.

- We expect Chinese manufacturing PMI to decline, due among other things to changing seasonal patterns.

- In Norway, we expect housing prices to continue to decline, as a sharp rise in the number of properties on the market, especially in Oslo, will probably put a damper on prices.

Global macro and market themes

- The natural rate of interest is key to understanding monetary policy setting in the long run, while the Phillips curve has explanatory power in the short term.

- The Bank of England's M ark Carney argues that structural factors continue to weigh on the natural rate but that it is increasing everywhere due to the global recovery.

- While we still expect long-term yields to increase, as central banks have turned more hawkish, there is a limit to how high they can move due to the low natural rate.

Dollar Reverses Losses after Chicago PMI Beat; Pound Slips as GDP Growth Disappoints

In a relatively busy data session, investors turned their attention back to the economic calendar, while concerns over Trump's tax proposals continued to weigh on the markets. Disappointing US inflation readings had a moderate impact on the dollar as markets were optimistic that the Fed would deliver another rate hike in December after Fed Chair, Janet Yellen, supported on Tuesday a gradual rate hike despite the weakness in inflation. The pound was the worst performer following weaker GDP growth readings.

The core PCE price index which is the Fed's preferred inflation measure added losses to the dollar on Friday after September's estimates appeared weaker than anticipated. While forecasts for the annual rate stood at August's mark of 1.4%, the index edged down by 0.1 percentage points to 1.3%, a level last seen in November 2015.

On the other hand, the Chicago PMI for the aforementioned month shot up to 65.2, approaching the 3-year highs reached in June and surpassing sharply the forecast of 58.5. This offset the dollar's earlier losses, pushing its index up to 93.21.

Dollar/yen pared half of yesterday's losses, jumping 0.22% on the day to 112.56.

According to the Office for National Statistics the final annual GDP growth for the UK missed the expectations of 1.7%, falling by 0.5 percentage points to 1.5% in the second quarter and touching the lowest growth since 2013 due to a weaker service sector in July. However, the quarterly basis figure remained unrevised at 0.3%, slightly up from the 0.2% reported in the first quarter.

Household savings ratio stuck at historically low levels in the second quarter at 5.4% despite the agency upwardly revising the previous mark of 1.7% to 3.8% due to errors in calculations.

Despite the fifth-largest economy growing slowly, the data might not change the BOE's intentions to raise rates soon. The Bank of England's Governor, Mark Carney, speaking on BBC radio on Friday reiterated that interest rates are likely to move upwards in "the relatively near term" but to a "limited extend" if the economy maintains its current performance. Yet, he did not confirm whether this would emerge at the November's MPC meeting.

The pound, however, failed to gain on Carney's remarks, falling to $1.3354 before rebounding to $1.3408. Euro/pound changed hands at a one-week high of 0.8841.

Initial Eurozone CPI readings for the month of September were just a shy lower than the forecast, hinting for a gradual removal of monetary stimulus. Headline inflation stood flat at 1.5% y/y, while analysts anticipated prices to pick up by 1.6%. Excluding food and energy items, the core equivalent was unchanged at 1.3%, whereas analysts projected for prices to grow at August's rate of 1.2%. A day earlier, ECB chief economist Peter Praet argued that the ECB will discuss recalibration and not termination of the asset purchase program.

In other data out of the Eurozone, German unemployment fell surprisingly to a record low of 5.6% in September in contrast to retail sales which came in disappointing.

Euro/dollar breached above 1.1800 key level, trading higher by 0.25% on the day at 1.1810.

After four months of increases, the monthly Canadian GDP growth numbers in July indicated that the economy neither expanded or contracted, driving dollar/loonie up by 0.30% to 1. 2463.This was below the 0.1% expected and the 0.3% reported in June.

EUR/USD On The Run

The currency pair increased significantly today and resumed the yesterday's bullish candle. The today's increase will invalidate the Wednesday's breakdown, that's why we may have another bullish momentum in the upcoming days. Price is trading in the green and tries to climb much higher as the dollar index dropped further today.

The USDX is trading in the red and is under selling pressure on the short term again. The index has found strong resistance and 93.68, much below the 93.81 static resistance and now goes down and could retest the 92.49 horizontal support before will try to climb higher again.

The Euro increased despite some poor Euro-zone data, the German Retail Sales dropped by 0.4%, even if the traders have expected to see a 0.5% growth. Moreover, the Euro-zone CPI Flash Estimate increased only by 1.5%, less versus the 1.6% estimate, while the Core CPI Flash Estimate surged only by 1.1%, less versus the 1.2% estimate.

Price failed to stabilize below the median line (ML) of the minor black ascending pitchfork and below the median line (ml) of the minor descending pitchfork. A retest of the ML will confirm a further increase in the upcoming period, the next target will be at the upper median line (uml) of the descending pitchfork.

The pair is trapped within the 1.2041 horizontal resistance and the 1.1711 static support, could move in range between these levels in the upcoming period after the failure to approach and reach the median line (ML) of the major ascending pitchfork.

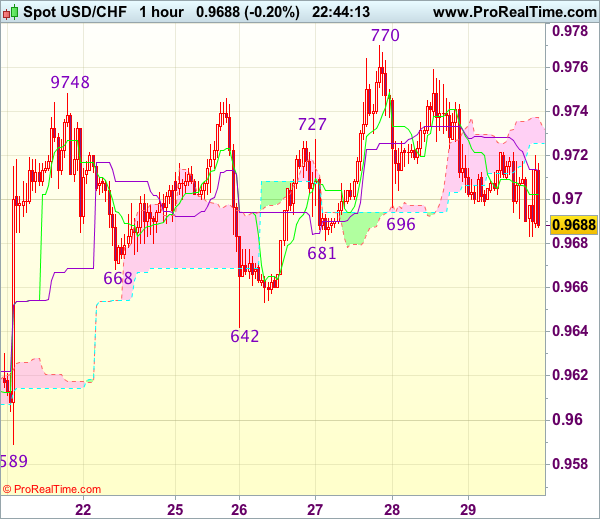

USD/CHF Another False Breakout

Price failed to stay above the second warning line and now could drop deeper in the upcoming days. USD/CHF is somehow expected to drop in the upcoming days after the failure to make new highs and to jump above the 0.9771 previous high. The failure to reach and retest the upper median line (uml) of the descending pitchfork could send the rate very fast towards the median line (ml) of the descending pitchfork.

GBP/JPY Further Drop In The Cards

The GBP/JPY is trading in the red on the short term, could drop further after the false breakout above the 151.66 horizontal resistance. You can see that has come back to retest the mentioned resistance and now goes down. The first downside target will be at the 150% Fibonacci line, a breakdown below it will open the door for more declines.

Trade Idea Wrap-Up: USD/CHF – Sell at 0.9705

Due to holidays, next update will be posted on Oct 9.

USD/CHF - 0.9677

Most recent candlesticks pattern : N/A

Trend : Near term up

Tenkan-Sen level : 0.9696

Kijun-Sen level : 0.9707

Ichimoku cloud top : 0.9737

Ichimoku cloud bottom : 0.9726

New strategy :

Sell at 0.9705, Target: 0.9605, Stop: 0.9740

Position : -

Target : -

Stop : -

The greenback continued meeting resistance around 0.9720 and has slipped again in NY morning, suggesting top has possibly been formed at 0.9770 earlier this week and downside bias is seen for test of support at 0.9642, however, break there is needed to add credence to this view and extend fall to 0.9620, then towards previous support at 0.9589 which is likely to hold from here.

In view of this, we are looking to sell dollar on recovery as 0.9700-05 should limit upside and bring another decline later. Above 0.9720-25 would suggest an intra-day low is formed, bring rebound to 0.9750 but still reckon strong resistance at 0.9770-73 would hold from here.