Sample Category Title

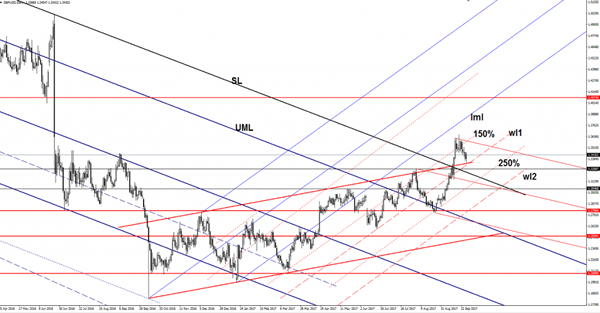

GBP/USD Bounced Back

Price increased in the yesterday's trading session and tries to recover after the last day's drop. GBP/USD stays in the green territory and should climb much higher in the upcoming days. The perspective remains bullish on the Daily chart despite the minor drop.

The pair had come down only to retest some broken levels before will climb much higher. It could move sideways on the short term and could try to recapture more directional energy before will climb towards new highs.

GBP/USD increased significantly in the second part of the day as the USDX plunged on the mixed US data. The USD bulls were disappointed by the Unemployment Claims unexpected increase, the Initial Claims were reported at 272K, above the 269K estimate and much above the 260K in the former reading period.

Price climbed higher and failed to reach and retest the upside line of the ascending channel and the first warning line (wl1) of the ascending pitchfork, signaling that the bulls are still in the game and could take full control again.

Remains to see what will happen tomorrow because the economic calendar is filled with high impact data that could shake the markets.

Price is somehow expected to approach and reach the upper median line (uml) of the red descending pitchfork. A failure to breakout above this level will announce an exhaustion and a potential leg lower.

Dollar Fatigue Sets In

Dollar fatigue sets in

The USD rally has derailed with dollar backpedalling overnight. Perhaps attributable to trader fatigue after this week's frenzied paced sell-off on US bond markets or even a bout of nervous nellie profit-taking. However, the dollar pull-back is more likely a reaction to the fact the hugely anticipated tax reform broadcast has come and gone and the reality check sets in that the road to reform will be a long and winding trek and an extremely bumpy one at that based on the current GOP squabbling.

All eyes will remain on US treasuries for the foreseeable future as this week's ferocious action is unlikely to yield anytime soon given the shifting market narratives.( hawkish fed, tax reform) .However, with market exhaustion setting in, the constant bond curve activity is abating as we enter weeks end and predictably profit taking is setting in.

EURO

Although the EUR has fallen on the back of higher US yields this week, the move has remained tidy as there appears to be a reluctance to sell the EURUSD below 1.1700 as traders believe the long-term investors will eventually have the upper hand and remain buyers in EURUSD dips.

Given the hullabaloo this week over the hawkish shift in the Fed and USD positivity surrounding tax reform, we may be looking at a stronger dollar narrative heading into year-end. However, the EUR needs a distinctive look as the ECB remains the real wild card in the deck. It is possible the more aggressive FED policy tact allows the ECB more wiggle room. So it is conceivable the ECB will sidestep the inflation conundrum, as did the Fed's, and will start to normalise policy soon.This allure should be enough to keep interest in the long EURO trade as dealers will be more than eager to catch the ECB policy shift momentum.

Japanese Yen

Battle lines are developing between election concerns and US yields, but month-end flows may also be distorting the picture. It is hard not to remain supportive of the long USDJPY trade, but the market will get the jitters the tighter the election polls run.

Australian Dollar

USD profit taking ahead of .7800 level ( this was an active short-term target for the AUD bears) has seen the AUDUSD recover off the overnight lows, but the reasons to sell the AUD remain in place.

Iron ore prices look precarious perched as the decline in prices is surely on the cards if the full brunt of Beijing-mandated steel production restriction comes to fruition.

Also, it is evident the RBA would welcome further currency weakness and its careful approach to tightening policy is arguably second only to the BOJ on the dovish scale at this stage.

Its even being bandied around market circles that Aussie may end up being a funding currency as other global central banks gallop towards policy normalisation.

Look for the Aussie sellers to emerge on rallies.

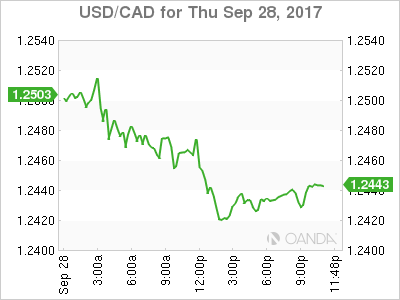

USD/CAD Canadian Dollar Higher As USD Rally Loses Steam

The Canadian dollar appreciated on Thursday versus the US dollar as investors took gains from an earlier greenback rally ahead of the end of September. The loonie traded lower on Wednesday after Bank of Canada (BoC) Governor Stephen Poloz gave a more dovish speech than expected cooling anticipation of an upcoming rate hike. The central bank had surprised the markets in July and once again in September. The Canadian benchmark rate is 1.00 percent after the two 25 basis points hikes, back to its 2015 level.

The USD rally could not be sustained ahead of the end of the week with no upcoming data. The US gross domestic product (GDP) final estimate for the second quarter beat expectations at 3.1 percent leaving investors to wait until next week for another telling economic indicator. Traders took profits on their positions and will reassess the market ahead of US jobs data next week.

NAFTA negotiations made progress as difficult topics were discussed, but so far no clear decisions have been made. The timing of the US Commerce Department 220 percent duty on Bombardier jets has not derailed the talks, but its impact would have been felt within the trade talks. Mexican negotiations have already started to think the late 2017 goal of renegotiating the trade agreement is too optimistic and are now open to the possibility of talks going into 2018. The next round of negotiations will take place in Washington on October 11 through the 15.

The USD/CAD lost 0.278 percent in the last 24 hours. The currency pair is trading at 1.2430 as the boost from the Fed and President Trump’s tax plans was short lived as there were so many details missing. Fed Chair Janet Yellen still sees the best path to be one of gradual rate hikes rather than wait for inflation to pick up. Probabilities of a December rate hike have gone up. The Trump administration is starting its push of tax reforms, but with so much political capital squandered since the beginning of the year.

The loonie mounted a comeback ahead of gross domestic product data on Friday, September 29. Monthly Canadian GDP is expected to come in at 0.1 percent, marketing a slowdown from the impressive pace this year. Last month the GDP grew by 0.3 percent monthly and 4.5 percent annually fuelled by consumer spending. The Bank of Canada (BoC) has stressed that higher rates could impact consumer negatively as household debt has climbed to record levels.

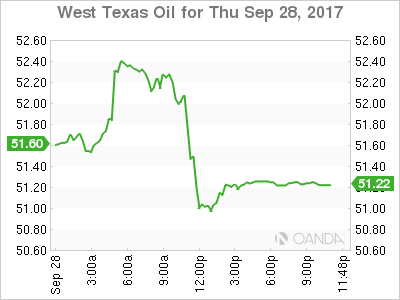

Energy prices lost 1.024 on Thursday. West Texas Intermediate is trading at 51.24 as US oil production rose 9 percent during the last three weeks offsetting reports of stronger forecasted demand and a possible Organization of the Petroleum Exporting Countries (OPEC) cut agreement extension. Saudi Arabia used overproduction as a strategy to grab market share and drive prices lower with the intent to drive the US shale industry into bankruptcy. The strategy backfired as the flexibility of US drillers and low rates made it easier to service the debt and wait for the OPEC to reach an agreement with other major producers.

Oil traders continue to monitor the situation in Northern Iraq. Supply disruptions have been one factor driving prices up in the past, but so far the referendum for independence has not been recognized. Turkey and other allies of Iraq have threatened the Kurdish region with cutting off the access to international markets of their oil if they continue on this path. The potential impact to global supply would be of around 500,000 daily barrels.

Market events to watch this week:

Friday, September 29

4:30am GBP Current Account

8:30am CAD GDP m/m

Is Tax Reform Priced In?

The US dollar struggled to maintain momentum on the heels of the tax announcement as opposition begins to materialize. NZD was the top performer while USD lagged. Japanese CPI is due later. Friday's US core PCE will be key. 5 new charts have been posted to subscribers backing the ongoing DAX30 trade. The chart below is one them.

The greenback has been beaten down for most of the year and finally looks poised for a rebound but the market isn't delivering. The tax proposal gave the dollar a lift Wednesday and sparked a sharp selloff in Treasuries but the momentum faded today.

That was despite a revision higher in Q2 GDP to 3.1% from 3.0%, a small-than-expected good trade deficit and wholesale inventories for August up 1.0% compared to a 0.4% decline expected.

That's all good news but the USD dollar fell around a half-cent across the board. USD/JPY slowly slid to 112.24 from as high as 113.20 in Asian trading. Both EUR/USD and USD/JPY formed minor two-day double bottoms before the turnarounds.

9 months of disappointment for USD bulls is hard to shake off. Friday's critical PCE report will be a major factor in upcoming Fed communication and should be a major dollar story.

The bigger story, however, has to be taxes. The numbers and rates that the administration is floating would be a major dose of stimulus.

The big question regarding tax reform is: What's priced in? Given the healthcare struggles, you would expect some skepticism in the markets but the failure on that front could also help bring Republicans to some sort of compromise.

Perhaps no one wants to bet on Congress and risk another brutal disappointment. We also have to consider the alternative: That a tax cut has already been priced in. Maybe now the market is having doubts because there are so many barriers to a deal, especially with much of the savings going to corporations and high-income earners.

It's tough to believe it's priced in but it's also tough to understand how the dollar can continue to struggle. Perhaps month end flows are skewing the signals. We will watch closely in the week ahead.

In the meantime, Japan is out with a pair of key reports to close the week. Both CPI and employment data are due at 2330 GMT. Even with a rise in CPI to 0.6% (as expected) we struggle to see a shift from the BOJ any time soon.

US GDP Shines, Pound Remains Steady

The British pound has recorded slight gains on Thursday, erasing the losses which marked the Wednesday session. In North American trade, GBP/USD is trading at 1.3430, up 0.31% on the day. On the release front, there were no major British releases. In the US, GDP expanded 3.1%, beating the forecast of 3.0%. Unemployment claims jumped to 272 thousand, higher than the estimate of 269 thousand. On Friday, the US releases Personal Spending and UoM Consumer Sentiment.

The US economy continues to hum in 2017, as Final GDP for the second quarter posted an impressive gain of 3.1%. This figure was revised upwards from the second estimate of 3.0% in August. However, September and third quarter economic numbers could soften, due to the damage caused by hurricanes Harvey and Irma, which caused a slowdown in economic activity. The recent hurricanes have impacted on the labor market, pushing unemployment numbers higher. Still, the labor market remains strong, as underscored by unemployment rolls which have remained below the 300,000 level.

Donald Trump's plans to reform health care appear dead-upon-arrival, so the US president has now set his sights on tax reform, another key campaign platform. On Wednesday, Trump proposed a major overhaul of the US tax code, which includes reducing the corporate tax rate to 20 percent, as well as 25 percent tax rate for small businesses, such as partnerships. Like other Trump proposals, the tax plan was sketchy on details, including how the tax plan would be paid for. With Democrats and some Republicans wary of Trump, it's likely that tax reform will face a stiff battle in Congress.

Gold Steady as Final GDP Edges Above Forecast

Gold has posted slight gains on Thursday. In North American trade, the spot price for an ounce of gold is $1285.21, up 0.27% on the day. Gold prices have steadied, but are still 1.0% lower this week. On the release front, key indicators were mixed. GDP expanded 3.1%, beating the forecast of 3.0%. Unemployment claims jumped to 272 thousand, higher than the estimate of 269 thousand. On Friday, the US releases Personal Spending and UoM Consumer Sentiment.

The US economy continues to perform well, as Final GDP for the second quarter posted an impressive gain of 3.1%. This figure was revised upwards from the second estimate of 3.0% in August. However, September and third quarter economic numbers could soften, due to the damage caused by hurricanes Harvey and Irma, which caused a slowdown in economic activity. The recent hurricanes have impacted on the labor market, pushing unemployment numbers higher. Still, the labor market remains strong, as underscored by unemployment rolls which have remained below the 300,000 level.

President Trump has all but given up on his health care proposals, as the plan lacks enough support from Republican lawmakers. Trump has now set his sights on tax reform, another key campaign promise. On Wednesday, Trump proposed a major overhaul of the US tax code, which includes reducing the corporate tax rate from 40 percent to 20 percent, as well as a 25 percent tax rate for small businesses, such as partnerships. Like other Trump proposals, the tax plan was sketchy on details, including how the tax plan would be paid for. With Democrats and some Republicans wary of Trump's tax agenda, it's likely his that tax reform proposal will face a stiff battle in Congress.

Dollar Retreats Despite US Economy Performing Better than Expected; Pound Reverses Losses after Barnier’s Speech

During European trading, markets pushed the dollar lower as concerns grew over Trump's tax proposals following an initial positive response. The dollar's weakness gave a breather to other majors, with the euro and the pound being the best performers, while the latter gained additional support following encouraging comments made by the EU Brexit negotiator Michel Barnier.

The dollar reversed gains made earlier against a basket of major currencies despite better than expected final GDP growth figures as investors were assessing that Trump's tax cuts proposed yesterday might fail to pass in Congress as they could potentially raise nation's debt levels.

The final US GDP growth rate for the second quarter came in unexpectedly at 3.1% q/q, above the 3.0% expected and the 1.2% seen in the first quarter. August goods trade balance was also a surprise as the deficit declined to $62.94bn while projections were for the deficit to reduce to $65.00bn from $65.10bn.

On the other hand, initial jobless claims during the past week increased by 272,000 versus 260,000 observed two weeks ago and 270,000 anticipated, driving the 4-week average measure to a 16-month high of 277,750.

The dollar index sank to 93.15 after touching a five-week high of 93.47 in the Asian session. Dollar/yen was 0.27% down on the day at 112.51.

In Brussels, the EU Brexit negotiator Michel Barnier and his UK counterpart David Davis held a press conference while in the UK the BOE Governor Mark Carney and the UK Prime Minister, Theresa May, spoke at the 20th independent anniversary of the Bank of England.

Remarks from Barnier provided some support to the pound after he commented that Brexit negotiations, which moved on to the fourth round on Monday, were "useful" and "dynamic" but not sufficient enough for talks to move to trade topics. In addition, he added that it might take "weeks or months" before trade issues come to the table as both sides continue to have different opinions on the Brexit bill and on the role of the European Court of Justice after the divorce.

The BOE's Carney, commenting on Brexit, said that monetary stimulus would be unable to mitigate any negative effects – mainly weaker real incomes – arising from the country's exit from the EU. He added that the only thing the central bank could do is smooth the economic cycle. A few minutes later, PM May gave her own speech but did not address Carney's earlier comments. Instead, she made talk of favoring free markets as the best way to run an economy, saying that "a free market economy is the only sustainable means of increasing living standards of everyone in the country".

The pound gained 0.37% on the day, climbing to $1.3429 ahead of the second quarter's GDP growth readings tomorrow.

The Business and Consumer survey from the European Commission showed that economic sentiment in the Eurozone in September rose more than expected, with the index rising to a 10-year high of 113.0 compared to the forecasted 112.0. Moreover, consumers' confidence in economic activity improved as well, increasing by 0.3 percentage points from -1.5% to -1.2%, while they were also more certain that prices will grow over the next 12 months. Though, tomorrow's CPI readings out of the eurozone will give more clues on the region's inflation path.

Euro/dollar recovered from yesterday's losses, jumping by 0.44% to 1.1792.

Regarding commodities, oil prices touched new highs while gold edged up to $1,283.10 per ounce. Specifically, WTI crude surged by 0.52% to $52.41 per barrel and Brent rose by almost 1% to $58.46 after Turkey threatened on Thursday to impose restrictions on oil trading with Iraq's Kurdistani region.

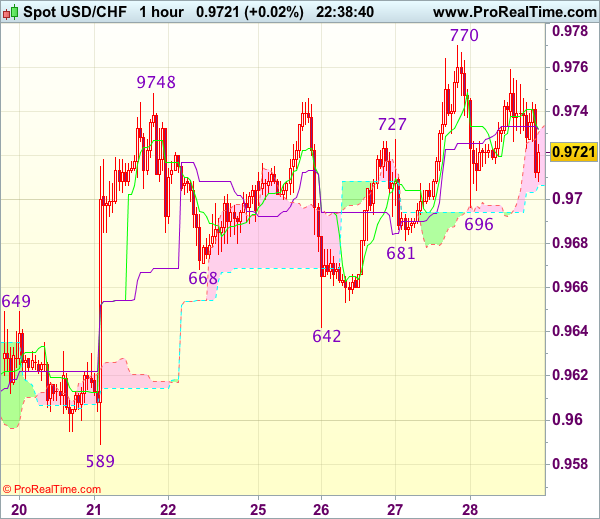

Trade Idea Wrap-up: USD/CHF – Stand aside

USD/CHF - 0.9714

Most recent candlesticks pattern : N/A

Trend : Near term up

Tenkan-Sen level : 0.9731

Kijun-Sen level : 0.9730

Ichimoku cloud top : 0.9732

Ichimoku cloud bottom : 0.9706

New strategy :

Stand aside

Position : -

Target : -

Stop : -

Although the greenback retreated to 0.9696 yesterday, as dollar found support there and rebounded, suggesting another test of resistance at 0.9770-73 cannot be ruled out, however, break there is needed to signal recent upmove has resumed and revive bullishness for the move from 0.9421 low to to extend gain to 0.9800-10 but overbought condition should limit upside to 0.9840-50.

In view of this, would not chase this rise here and would be prudent to stand aside in the meantime. Below said support at 0.9696 would suggest top is possibly formed, bring test of 0.9681 support, break there would add credence to this view, bring correction of recent rise towards support at 0.9642 which is likely to hold on first testing.

Trade Idea Wrap-up: GBP/USD – Buy at 1.3385

GBP/USD - 1.3446

Most recent candlesticks pattern : N/A

Trend : Near term down

Tenkan-Sen level : 1.3399

Kijun-Sen level : 1.3399

Ichimoku cloud top : 1.3451

Ichimoku cloud bottom : 1.3408

Original strategy :

Sell at 1.3500, Target: 1.3380, Stop: 1.3535

Position : -

Target : -

Stop : -

New strategy :

Buy at 1.3385, Target: 1.3485, Stop: 1.3350

Position : -

Target : -

Stop : -

As cable found good support at 1.3343 and has staged a strong rebound, suggesting low is possibly formed there and consolidation with mild upside bias is seen for test of 1.3465-70 (50% Fibonacci retracement of 1.3596-1.3345), however, reckon resistance at 1.3514 would limit upside and price should falter well below resistance at 1.3571, bring another decline later.

In view of this, we are looking to turn long on dips as 1.3380-85 should limit downside. Only below said support at 1.3343 would abort and signal the selloff from 1.3658 top has resumed and extend weakness to previous resistance at 1.3329, then towards 1.3300.

Eurozone Business and Consumer Confidence Surges, USD GDP Grows

Today was a busy day in regards to economic data releases. Gross Domestic Product in the US grew at 3.1% in the second quarter, slightly above the previous forecast. It is the best quarterly growth in almost two years. The economy at its core remained stable as growth in the job market and a booming stock market encouraged households to spend. According to advance economic indicator reports from the US Commerce Department, the trade deficit for US goods narrowed 1.4% and came in at $62.94 billion in August as compared to July. Exports rose 0.2% and goods imports decreased 0.3%. But the Commerce Department also warned that the data may have been affected by Hurricanes Irma and Harvey as ports were closed and caused shipment diversions and delays.

The euro received support after the European Commission earlier today released the economic sentiment indicator, which combines both the business and consumer confidence reports. Economic sentiment rose to 113 in August from 111.9 in July, the highest level its been since June 2007. The strong growth in business confidence implies that the Eurozone economy will be enjoying faster growth in the final months of the year. More confident businesses tend to invest more while households spend more freely. Increases in aggregate confidence will also give the European Central Bank some comfort as it looks to reduce its stimulus program from as early as next year. ECB's economists are also expecting 2.2% economic growth for the region. Inflation data released earlier today suggests that the inflation rate has not moved toward the target in September. Germany's consumer prices rose 1.8% compared to a year earlier and in Spain the rate of inflation slowed to 1.9% from 2% in August.

AUD/USD

AUD/USD is consolidating and trading around last month's low at 0.78072. The pair is trading below the 50- day moving average, which plays a resistance role. The relative strength index is mixed and calls for a bearish movement. As long as the price remains below 0.7887 (yesterday's high) look for further decline to 0.7798 (today's low) and 0.7755. Alternatively, above 0.7887 (yesterday's high) look for 0.7907 (last week's low) and 0.7945.

EUR/USD

EUR/USD rebounded from 1.17162 (this week's low) but the bias remains bullish. The extent of the rebound however should be limited. The downward movement is reinforced by the declining 50 day moving average and the relative strength index is also showing a bearish outlook. So, below 1.18606 (last week's low) look for further downside to 1.17163 (this week's low) and 1.16616 (last month's low). Alternatively, above 1.18606, look for 1.1900 and 1.19360 (this week's high).

NZD/USD

NZDUSD is expected to trade with a bearish outlook as the process of lower highs and lows remains intact. The 50 day moving average and 20 day moving average are still heading downward. So as long as the price remains below 0.72467 (last week's low) look for downside targets at 0.71656 (today's low) and 0.71304 (last month's low). Alternatively, above 0.72467 look for 0.7285 and 0.7305.