Sample Category Title

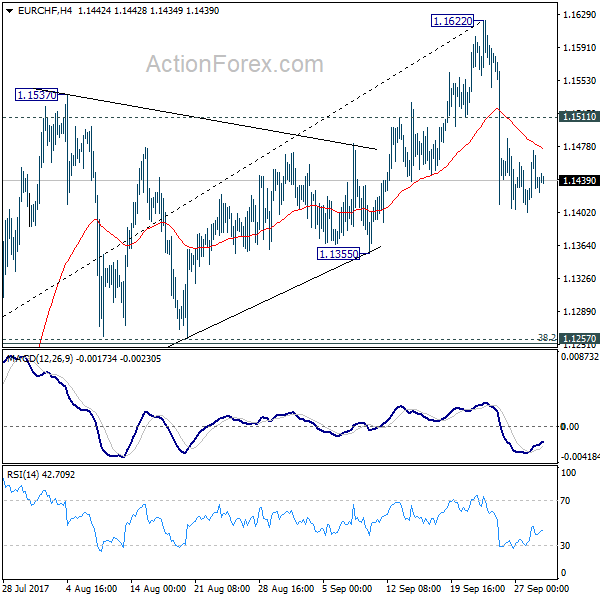

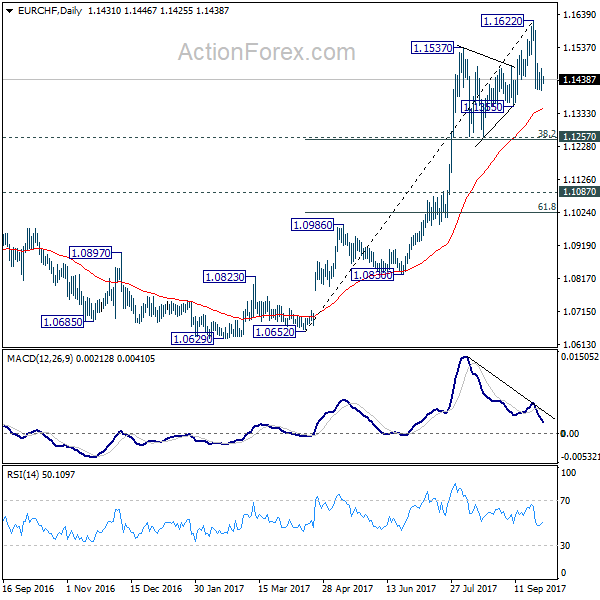

EUR/CHF Daily Outlook

Daily Pivots: (S1) 1.1404; (P) 1.1439; (R1) 1.1467; More...

No change in EUR/CHF's outlook. With 1.1511 minor resistance, correction from 1.1622 short term top is expected extend through 1.1355 support. Strong support is expected from 1.1257 (38.2% retracement of 1.0652 to 1.1622 at 1.1251) to bring rebound. On the upside, break of 1.1511 minor resistance will suggest that the pull back is completed and bring retest of 1.1622.

In the bigger picture, long term rise from SNB spike low back in 2015 is still in progress. EUR/CHF should now be heading back to prior SNB imposed floor at 1.2000. For now, this will be the favored case as long as 1.1198 resistance turned support holds.

Aussie Dollar Trading Lower This Morning

For the 24 hours to 23:00 GMT, the AUD declined 0.06% against the USD and closed at 0.7849.

LME Copper prices declined 0.3% or $21.0/MT to $6405.0/MT. Aluminium prices declined 0.7% or $14.5/MT to $2102.5/MT.

In the Asian session, at GMT0300, the pair is trading at 0.7841, with the AUD trading 0.1% lower against the USD from yesterday’s close.

Early morning data indicated that Australia’s private sector credit advanced 0.5% on a monthly basis in August, compared to a similar rise in the previous month.

The pair is expected to find support at 0.7807, and a fall through could take it to the next support level of 0.7774. The pair is expected to find its first resistance at 0.7867, and a rise through could take it to the next resistance level of 0.7894.

The currency pair is showing convergence with its 20 Hr and 50 Hr moving averages.

Euro-Zone’s Economic Sentiment At A More Than A Decade High Level In September

For the 24 hours to 23:00 GMT, the EUR rose 0.31% against the USD and closed at 1.1781, after data indicated that the Euro-zone's final consumer confidence index climbed to a sixteen-year high level of -1.2 in September, confirming the preliminary print and following a level of -1.5 in the prior month.

Further, the region's economic confidence index jumped to a more than ten-year high level of 113.0 in September, indicating that businesses and households are growing more upbeat about the region's growth prospects. The index had recorded a reading of 111.9 in the previous month, while markets were expecting for a rise to a level of 112.0.

Separately, Germany's flash consumer price index (CPI) rose 1.8% YoY in September, at par with market expectations and following a similar rise in the prior month. On the other hand, the nation's GfK consumer confidence index registered an unexpected drop to a level of 10.8 in October, defying market consensus for an increase to a level of 11.0 and following a level of 10.9 in the prior month.

In the US, data indicated that the final annualised gross domestic product (GDP) was revised higher to 3.1% in the second quarter of 2017, accelerating at its quickest pace in more than two years, while the preliminary figures had indicated an expansion of 3.0%. The nation's GDP had posted a revised advance of 1.2% in the previous quarter. Further, the nation's preliminary wholesale inventories recorded a rise of 1.0% on a monthly basis in August, beating market expectations for an advance of 0.4%. In the previous month, wholesale inventories had climbed 0.6%.

Other economic data showed that advance goods trade deficit in the US surprisingly narrowed to a level of $62.9 billion in August, after reporting a revised deficit of $63.9 billion in the previous month, while investors had envisaged the trade deficit to expand to a level of $65.1 billion. On the contrary, the nation's initial jobless claims climbed more-than anticipated to a level of 272.0K in the week ended 23 September, compared to a revised level of 260.0K in the prior week, while markets had anticipated for an advance to a level of 270.0K.

In the Asian session, at GMT0300, the pair is trading at 1.1779, with the EUR trading slightly lower against the USD from yesterday's close.

The pair is expected to find support at 1.1732, and a fall through could take it to the next support level of 1.1685. The pair is expected to find its first resistance at 1.1815, and a rise through could take it to the next resistance level of 1.1851.

Going ahead, investors will focus on the Euro-zone's flash inflation numbers for September along with Germany's unemployment rate for September and retail sales for August, all slated to release in a few hours. Later today, traders would eye the US personal income as well as spending data for August and the final Michigan consumer confidence index for September.

The currency pair is showing convergence with its 20 Hr moving average and trading above its 50 Hr moving average.

BoE Can’t Be Expected To Nullify Brexit Hit: Mark Carney

For the 24 hours to 23:00 GMT, the GBP rose 0.27% against the USD and closed at 1.3434, after Brexit officials confirmed that “considerable progress” is finally being made in the fourth round of Brexit negotiations.

Yesterday, the Bank of England (BoE) Governor, Mark Carney, indicated that the central bank has limited tools to mitigate economic damage caused by Brexit, although it could influence how that hit is spread across Britain. He further added that the BoE will continue to assess and express its independent assessment of the risks associated with Brexit.

In the Asian session, at GMT0300, the pair is trading at 1.3411, with the GBP trading 0.17% lower against the USD from yesterday's close.

Overnight data showed that the nation's GfK consumer confidence index unexpectedly climbed to a four-month high level of -9.0 in September, confounding market consensus for a drop to a level of -11.0. In the prior month, the index had registered a level of -10.0.

The pair is expected to find support at 1.3351, and a fall through could take it to the next support level of 1.3291. The pair is expected to find its first resistance at 1.3463, and a rise through could take it to the next resistance level of 1.3515.

Ahead in the day, market participants will focus on UK's final 2Q GDP as well as net consumer credit and mortgage approvals data, both for August.

The currency pair is trading below its 20 Hr moving average and showing convergence with its 50 Hr moving average.

Japan’s Consumer Price Inflation Advanced Better-Than-Expected In August

For the 24 hours to 23:00 GMT, the USD declined 0.42% against the JPY and closed at 112.39.

In the Asian session, at GMT0300, the pair is trading at 112.67, with the USD trading 0.25% higher against the JPY from yesterday's close.

Overnight data revealed that Japan's national consumer price index (CPI) rose 0.7% on an annual basis in August, surpassing market consensus for a gain of 0.6%. The CPI had climbed 0.4% in the prior month. Further, the nation's unemployment rate remained steady at 2.8% in August, meeting market expectations. Moreover, the nation's preliminary industrial production rebounded more-than-anticipated by 2.1% on a monthly basis in August, compared to market expectations for an advance of 1.8%. In the previous month, industrial production had recorded a drop of 0.8%.

In other economic news, Japan's retail trade registered a more-than-expected drop of 1.7% in August, while markets had envisaged for a fall of 0.5% and following a rise of 1.1% in the previous month. On the contrary, the nation's large retailers' sales rebounded 0.6% in August, compared to a fall of 0.2% in the prior month, while markets were expecting for an advance of 0.3%.

Separately, the Bank of Japan's (BoJ) summary of opinions report showed that one policymaker urged for expanding monetary stimulus at the central bank's September meeting, while most officials remained in favour of maintaining the current stimulus programme, as the bank was far from achieving the 2.0% inflation target.

The pair is expected to find support at 112.22, and a fall through could take it to the next support level of 111.76. The pair is expected to find its first resistance at 113.17, and a rise through could take it to the next resistance level of 113.66.

The currency pair is showing convergence with its 20 Hr moving average and trading below its 50 Hr moving average

Swiss Franc Trading On A Weaker Footing In The Morning Session

For the 24 hours to 23:00 GMT, the USD declined 0.16% against the CHF and closed at 0.9705.

In the Asian session, at GMT0300, the pair is trading at 0.9718, with the USD trading 0.13% higher against the CHF from yesterday’s close.

The pair is expected to find support at 0.9691, and a fall through could take it to the next support level of 0.9664. The pair is expected to find its first resistance at 0.9752, and a rise through could take it to the next resistance level of 0.9786.

Moving ahead, traders will eye Switzerland’s KOF leading indicator data for September, due to release in a few hours.

The currency pair is showing convergence with its 20 Hr moving average and trading below its 50 Hr moving average.

Loonie Reverses Its Gains, Ahead Of Canada’s GDP Data

For the 24 hours to 23:00 GMT, the USD declined 0.34% against the CAD and closed at 1.2435.

In the Asian session, at GMT0300, the pair is trading at 1.2443, with the USD trading 0.06% higher against the CAD from yesterday's close.

The pair is expected to find support at 1.2400, and a fall through could take it to the next support level of 1.2358. The pair is expected to find its first resistance at 1.2502, and a rise through could take it to the next resistance level of 1.2562.

This afternoon will bring a crucial Canadian release, namely the GDP data for July.

The currency pair is trading below its 20 Hr moving average and showing convergence with its 50 Hr moving average.

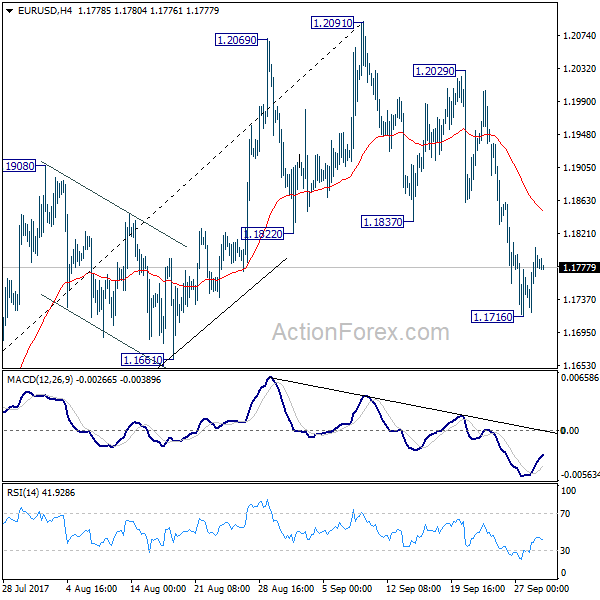

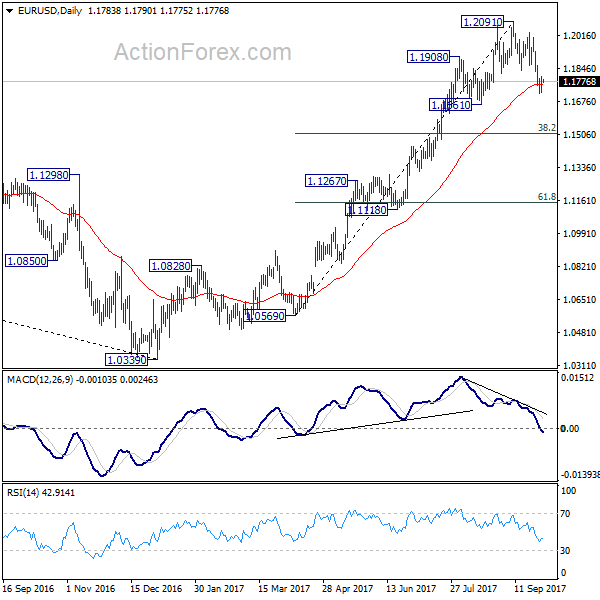

EUR/USD Daily Outlook

Daily Pivots: (S1) 1.1736; (P) 1.1770 (R1) 1.1820; More...

Intraday bias in EUR/USD remains neutral for the moment and some sideway trading could be seen above 1.1716 temporary low. Deeper fall is expected as long as 1.2029 resistance holds. Decline from 1.2091 is seen as correcting whole rise from 1.0569. Below 1.1716 will target 1.1661 support and then 38.2% retracement of 1.0569 to 1.2091 at 1.1510, where we're expecting support to bring rebound.

In the bigger picture, rise from medium term bottom at 1.0339 is still in progress for 38.2% retracement of 1.6039 (2008 high) to 1.0339 (2017 low) at 1.2516. However, it should be noted that there is no confirmation of trend reversal yet. That is, such rebound from 1.0399 could be a correction. And the long term fall from 1.6039 (2008 high) could resume. Hence, we'd be cautious on strong resistance from 1.2516 to limit upside. But after all, break of 1.1661 is needed to indicate medium term topping. Otherwise, outlook will remain bullish in case of pull back.

European Open Briefing: Equity Markets Across The Asia-Pacific Region Were Mostly Higher

Global Markets:

- Asian stock markets: Nikkei dropped 0.09 %, Shanghai Composite up 0.27 %, Hang Seng gained 0.23 %, ASX 200 rose 0.29 %

- Commodities: Gold at $1288.52 (-0.01 %), Silver at $16.87 (0.17 %), WTI Oil at $51.48 (-0.16 %), Brent Oil at $57.16 (+0.02 %)

- Rates: US 10-year yield at 2.31, UK 10-year yield at 1.37, German 10-year yield at 0.47

News & Data:

- (AUD) Private Sector Credit m/m 0.5 % vs 0.5 % expected

- (EUR) German Prelim CPI m/m 0.1 % vs 0.1 % expected

- (EUR) Spanish Flash CPI y/y 1.8 % vs 1.8 % expected

- (USD) Final GDP q/q 3.1 % vs 3.0 % expected

- (USD) Unemployment Claims 272 K vs 269 K expected

- (USD) Natural Gas Storage 58 B vs 77 B expected

- White House battles critics over tax plan as lawmakers prepare to act- RTRS

Markets Update:

Equity markets across the Asia-Pacific region were mostly higher on the final trading day of what's been a strong quarter. Most countries' stock indexes are set to end the month higher, with solid earnings and broadly positive risk sentiment outweighing the region's geopolitical concerns, in particular the escalation of tensions between North Korea and the U.S.

USDJPY had an active session early on Friday. Price is currently seen trading at 112.61 as the Yen lost 0.2 percent against the US Dollar. The pair printed a small high again after a period of consolidation earlier in the session. Today's session saw a big amount of data hit from Japan along with the 'Summary of Opinions' from the Bank of Japan September meeting. Price was

EURUSD is currently seen trading at 1.1780 as the Euro advanced 0.4 percent against the US Dollar. Price had earlier reached highs of 1.8000 in previous sessions before losing some of its gains. The dollar index, which tracks the dollar against a basket of currencies rose 0.1 percent and is currently valued at 93.21.

AUDUSD is down from the session highs of 0.7850 and is currently seen trading around 0.7840, mainly due to price of iron ore declining once Chinese market opened. Australia's 10-year bond yield declined about three basis points to 2.83 percent. Australian markets were a bit quiet as it is a holiday in Melbourne today and will be a holiday in Sydney on Monday. Likewise, the NZDUSD is seen trading at 0.7210 down close to 30 pips from the session highs of around 0.7240.

Upcoming Events:

- Tentative - (GBP) MPC Member Broadbent Speaks

- 06:00 GMT - (EUR) German Retail Sales m/m

- 07:00 GMT - (CHF) KOF Economic Barometer

- 08:30 GMT - (GBP) Current Account

- 08:30 GMT - (GBP) Final GDP q/q

- 08:30 GMT - (GBP) Net Lending to Individuals m/m

- 09:00 GMT - (EUR) CPI Flash Estimate y/y

- 09:00 GMT - (EUR) Core CPI Flash Estimate y/y

- 12:30 GMT - (CAD) GDP m/m

- 12:30 GMT - (CAD) RMPI m/m

- 12:30 GMT - (USD) Core PCE Price Index m/m

- 12:30 GMT - (USD) Personal Spending m/m

- 13:45 GMT - (USD) Chicago PMI

- 14:00 GMT - (USD) Revised UoM Consumer Sentiment

- 14:15 GMT - (EUR) ECB President Draghi Speaks

- 14:45 GMT - (GBP) BOE Gov Carney Speaks

- 15:00 GMT - (USD) FOMC Member Harker Speaks

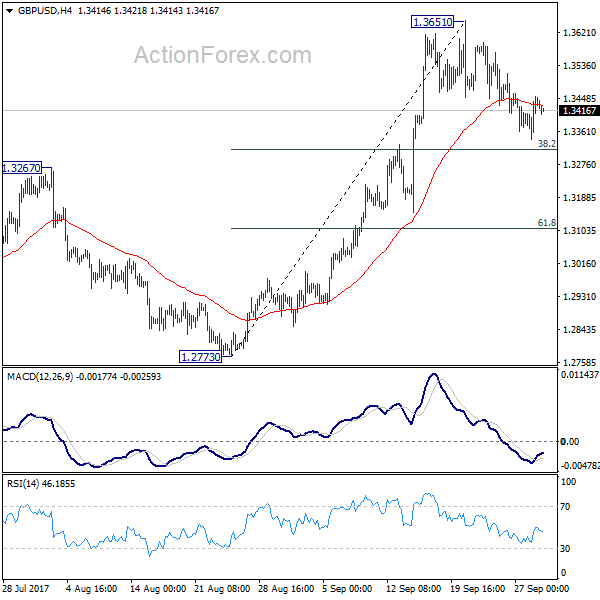

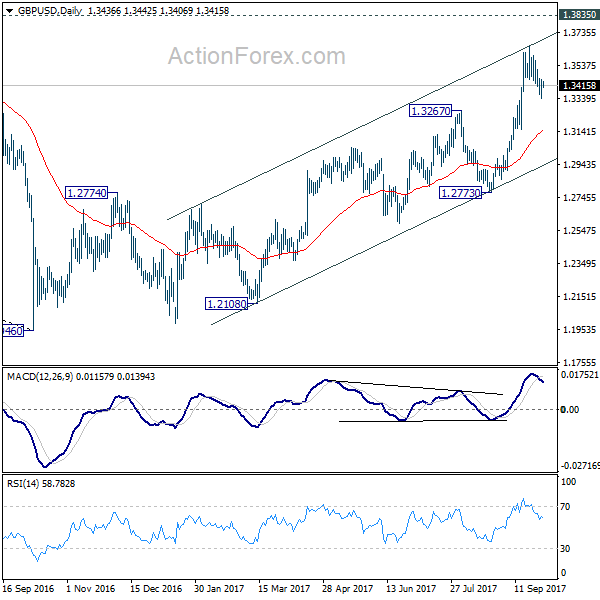

GBP/USD Daily Outlook

Daily Pivots: (S1) 1.3370; (P) 1.3413; (R1) 1.3483; More....

No change in GBP/USD's outlook. Correction from 1.3651 could extend. But we'd continue to expect strong support from 38.2% retracement of 1.2773 to 1.3651 at 1.3316 to contain downside and bring rally resumption. Break of 1.3651 will turn bias back to the upside for 1.3835 support turned resistance next. Break there will target 55 month EMA (now at 1.4405).

In the bigger picture, current development argues that the long term trend in GBP/USD has reversed. That is, a key bottom was formed back in 1.1946 on bullish convergence condition in monthly MACD. Current rise from 1.1946 will target 38.2% retracement of 2.1161 (2007 high) to 1.1946 (2016 low) at 1.5466 next. In any case, medium term outlook will now stay bull