Sample Category Title

Elliott Wave View: AUDJPY

AUDJPY Short Term Elliott Wave view suggests that the rally to 90.31 ended Intermediate wave (W). Intermediate wave (X) pullback remains in progress as a double three Elliott Wave structure. Down from 90.31, Minor wave W ended at 88.44 and Minor wave X ended at 89.68. Minor wave Y is unfolding also as a double three Elliott Wave structure. Minute wave ((w)) of Y ended at 88.23 and Minute wave ((x)) of Y is proposed complete at 88.89. Near term, while bounces stay below 9/25 peak at 89.69, expect pair to extend lower towards 87.37 – 87.8` area to complete Intermediate wave (X). Afterwards, pair should resume the rally to a new high or at least bounce in 3 waves. We don’t like selling the proposed pullback.

AUDJPY 1 Hour Elliottwave Chart

Double three ( 7 swings) is the most important pattern in Elliott wave’s new theory. It is also probably the most common pattern in the market these days. Double three is also known as a 7-swing structure. It is a very reliable pattern that gives traders a good opportunity to trade with a well-defined level of risk and target areas. The image below shows what Elliott Wave Double Three looks like. It has labels (W), (X), (Y) and an internal structure of 3-3-3. This means that all 3 legs has corrective sequences. Each (W) and (Y) is formed by 3 wave oscillations and has a structure of A, B, C or W, X, Y of smaller degrees.

Trade Idea : USD/JPY – Stand aside

USD/JPY - 112.59

Most recent candlesticks pattern : N/A

Trend : Up

Tenkan-Sen level : 112.52

Kijun-Sen level : 112.73

Ichimoku cloud top : 112.84

Ichimoku cloud bottom : 112.38

New strategy :

Stand aside

Position : -

Target : -

Stop : -

Despite falling to 112.38 yesterday, lack of follow through selling and the subsequent rebound suggest further consolidation would take place and recovery to 112.85-90 cannot be ruled out, however, price should falter below indicated resistance at 113.26, bring another retreat later, below said support at 112.38 would signal top has been formed at 113.26, bring retracement of recent rise to 112.00, then 111.75-80 but previous support at 111.47 should remain intact.

On the upside, whilst recovery to 112.85-90 cannot be ruled out, reckon said resistance at 113.26 would hold and bring further consolidation. Only a break of said this week’s high at 113.26 would revive bullishness and signal recent upmove has resumed, then further gain to previous resistance at 113.58 would follow but loss of upward momentum should prevent sharp move beyond 113.75-80 and reckon 114.00-10 would remain intact. As near term outlook is mixed, would be prudent to stand aside for now.

Euro Area HICP Figures For September

Market movers today

The final day of the week brings a packed calendar, with several tier-1 releases both globally and in the Scandies. Also, we might get news on the next Riksbank governor. In addition, quarter-end volatility will be a theme today in many markets.

In the Scandies, focus turns to the labour market and retail sales in Norway. Also, in Sweden reports suggest that the next Riksbank governor will be announced today. See Scandi markets on page 2 for more details.

In the euro area, euro area HICP figures for September are set for release. Following yesterday's inflation release in Spain and Germany, we still look for euro area inflation at 1.6% but with the weak service price inflation release in Germany, there is some downside risk to our euro area core inflation forecast of 1.3%. Instead, the increase to 1.6% in September might be driven more by the volatile components energy and food, if similar inflation trends are observed as in Germany. We also get data on German retail sales in August and the German unemployment rate.

In the US, we get the most important release of the week namely PCE inflation for August . We estimate a slight uptick in the monthly increases of both PCE headline and PCE core following the release of the surprisingly high increase in CPI (CPI and PCE numbers tend to follow each other). The monthly increase in the CPI numbers leads us to believe the PCE headline will increase 0.3% m/m (1.5% y/y versus 1.4% in July) and PCE core 0.2% m/m (1.4% y/y versus 1.4% in July). Note that although this relatively strong monthly print in the PCE core does not lead to increases in the yearly rate, this has to do with a very large monthly increase in August 2016. We also get the final University of Michigan consumer confidence. The preliminary number showed a fall compared with August but the index is still at a high level, pointing to solid growth in private consumption. The Chicago manufacturing PMI for September is also due for release.

In the UK, focus turns to Bank of England Governor Mark Carney speaking alongside the final release of second-quarter GDP.

Selected market news

No clear direction on Asian equity markets this morning, despite the move higher in most European and US indices yesterday. Japanese equit ies are trading in the ‘red', amid Japanese inflation moving higher (CPI excluding fresh food at 0.5% y/y). However, there are still no indications of inflation reaching the Bank of Japan's inflation target any time soon , suggesting a continuation of current policy should the forthcoming elections not challenge ‘Abenomics'.

There is still a lot of market focus on a potential tax reform in the US. Meanwhile, we still think the most likely outcome will be a smaller tax reform or no deal at all. We also emphasise that any easier fiscal policy could well be offset by tighter monetary policy . This is so even if uncertainty remains high on what the Fed Board of Governors will look like next year, with President Donald Trump potentially having to nominate five members

Market Update – Asian Session: US Sept Chicago PMI Data And Central Bank Speak In Focus

Asia Summary

Asian equities have traded mixed on today's session. Overall, trading has been fairly quiet amid the batch of data seen out of Japan and South Korea. Looking ahead, Euro Zone Sept Preliminary CPI is due to be released along with the US Sept Chicago PMI data. Central bank speak is also on the agenda with comments expected from the BoE's Carney, ECB's Draghi and Fed's Harker.

China offshore yuan (CNH) money market rates rise sharply ahead of upcoming National Day Golden Week holidays, as Chinese markets will be closed next week.

Key economic data

(AU) AUSTRALIA AUG PRIVATE SECTOR CREDIT M/M: 0.5% V 0.5%E; Y/Y: 5.5% V 5.5%E

(JP) JAPAN AUG NATIONAL CPI Y/Y: 0.7% V 0.6%E; CORE (EX-FRESH FOOD) Y/Y: 0.7% V 0.7%E

(JP) JAPAN SEPT TOKYO CPI Y/Y: 0.5% V 0.6%E; CORE (EX-FRESH FOOD) Y/Y: 0.5% V 0.5%E

(JP) JAPAN AUG PRELIM INDUSTRIAL PRODUCTION M/M: 2.1% V 1.8%E; Y/Y: 5.4% V 5.2%E

(JP) JAPAN AUG JOBLESS RATE: 2.8% V 2.8%E; JOB-TO-APPLICANT RATIO: 1.52 V 1.53E

(JP) JAPAN AUG RETAIL SALES M/M: -1.7% V -0.5%E; RETAIL TRADE Y/Y: 1.7% V 2.5%E

(JP) JAPAN AUG OVERALL HOUSEHOLD SPENDING: 0.6% V 0.9%E

(KR) SOUTH KOREA AUG INDUSTRIAL PRODUCTION M/M: 0.4% V 0.5%E; Y/Y: 2.7% V 1.3%E

(KR) SOUTH KOREA AUG BOP CURRENT ACCOUNT BALANCE: $6.06B V $7.26B PRIOR; GOODS BALANCE: $9.31B V $10.7B PRIOR

(KR) South Korea Aug Cyclical Leading Index: 0.0 v 0.2 prior

(KR) South Korea Oct Business Manufacturing Survey: 79 v 83 prior; Non-Manufacturing Survey: 78 v 78 prior

(NZ) New Zealand Aug Building Permits m/m: 10.2% v 1.7% prior

(NZ) RBNZ 2017 Annual Report: New Zealand's economy and financial system are sound

(UK) UK SEPT GFK CONSUMER CONFIDENCE: -9 V -11E

(UK) UK Sept Lloyds Business Barometer: 23 v 17 prior

Speakers and Press

China

(CN) China Premier Li Keqiang said to stay for another term - HK Press

(CN) China Investment Corp (CIC) said to end Aug with assets over $900B - Chinese Press

(CN) China said to raise fuel prices from Sept 30th

Other

(JP) BoJ Sept Meeting Minutes: One member said more easing is necessary to stimulate demand**Note: At the Sept BoJ meeting, the incoming member Kataoka was the lone dissenter (8 to 1 vote). The official said then that the yield curve control is not enough to meet the inflation target; Also, the official saw a low chance of CPI increasing from 2018.

(JP) Japan Fin Min Aso: Confirms need to delay FY2020 primary balance target ‘a bit'

(KR) South Korea Finance Ministry: Affirms sees 2017 GDP growth at 3%; To continue to monitor global financial markets during 10-day holidays; Uncertainty high ahead of North Korea's party foundation day on Oct 10th.

(KR) South Korea Financial Regulator: Bans all forms of initial coin offerings in the country

Asian Equity Indices/Futures (00:30ET)

Nikkei -0.1%, Hang Seng +0.2%, Shanghai Composite +0.3%%, ASX200 +0.2%, Kospi +0.7%

Equity Futures: S&P500 flat; Nasdaq +0.1% , Dax flat , FTSE100 flat

FX ranges/Commodities/Fixed Income (00:30ET)

EUR 1.1776-1.1791; JPY 112.27-112.69; AUD 0.7839-0.7858; NZD 0.7208-0.7238

Aug Gold -0.1% at 1,287/oz; Aug Crude Oil -0.1% at $51.51/brl; Sept Copper -0.1% at $2.975/lb

GLD SPDR Gold Trust ETF daily holdings flat at 864.7 metric tons

(CN) China PBOC sets yuan reference rate at 6.6369 v 6.6285 prior

(CN) PBOC OMO: SKIPS V INJECTED CNY70B IN 14 AND 28-DAY REVERSE REPOS PRIOR; net drain CNY160B

(AU) Australia sells A$800M in 2028 Bonds, avg yield 2.8913%, bid to cover 5.43x

(NZ) New Zealand sells NZ$150M in 3.5% April 2033 Bonds, avg yield 3.2958%, implied bid to cover 3.33x

Equities notable movers

Australia

Pilbara Minerals, PLS.AU China's Great Wall Motor to give update on plan to buy up to 3.5% stake; +18%

Japan

Yamato Holdings, 9064.JP Some disappointment with medium term outlook; -5.5%

US markets on close: Dow +0.2%, S&P500 +0.1%, Nasdaq flat, Russell +0.3%

Best Sector in S&P500: Real Estate +0.7%

Worst Sector in S&P500: Consumer Discretionary -0.1%

At the close: VIX 9.55 (-0.32 pts); Treasuries: 2-yr 1.459% (-2bps), 10-yr 2.312% (flat), 30-yr 2.871% (+1bp)

US Market Summary

US stocks rallied off of opening lows to end the day about flat, after US GDP and jobless claims data were largely in line with expectations and as Republicans continued to make their case for tax cuts. Treasury yield curves saw steepening trades remain entrenched, with long rates extending modestly higher after a strong 7-year note sale. The Dollar index broke a three-day winning streak but the giveback was benign. The US IPO market heated up with four NASDAQ issues opening for trade including a 50% pop for Roku. Materials and healthcare names were outperformers on the day, while consumer discretionary and industrials lagged slightly.

US Afterhours Movers

ATEN Raises Q3 Rev $59-60M v $55.6Me (prior $53-57M); EVP sales to leave company; +24.8% afterhours

SGH Reports Q4 $0.79 v $0.64e, Rev $223.0M v $211Me; Guides Q1 $0.79-0.83 v $0.68e, Rev $225-240M v $211Me, gross margin 21-22%; +6.7% afterhours

TSN Raises FY17 $5.20-5.30 v $5.09e (prior $4.95-5.05); plans to reduce headcount by ~450 positions; +4.9% afterhours

HLT Files to sell 14.6M shares by holder Blackstone (4.5% of shares outstanding) via GS: -1.4% afterhours

PRTA Reports results from Phase 1b multiple ascending dose study of PRX003 in patients with Psoriasis; Prerequisites were not met; -5.5% afterhours

AUD/USD More Downside In View

Price drops again after the yesterday’s rebound. The pair had come back to retest the median line (ml) of the minor descending pitchfork and now tries to resume the bearish movement. A further drop will be confirmed after a valid breakdown below the 0.7835 static support. The major downside target will be at the WL1, it could also be attracted by the lower median line (lml) of the descending pitchfork.

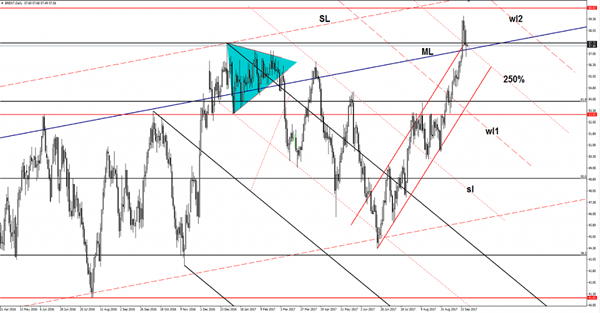

Brent Oil Buying Opportunity?

The pair has dropped a little today and continues to pressure the 250% Fibonacci line (descending dotted line). It could still retest the median line (ML) of the major ascending pitchfork, actually, is attracted by the confluence area formed between the ML and the 250% Fibonacci line. A valid breakdown through the confluence area will accelerate the sell-off, while a rejection will bring us a good opportunity to go long again.

EUR/USD Still In The Green

The currency pair increased in the morning and tries to resume the yesterday’s bullish candle. Has retested an important dynamic support and is somehow expected to climb higher after the corrective phase.

We’ll see what will happen because technically a breakdown was favored after the failure to close above a major resistance area.

The economic calendar is filled with high impact data, so the price will be driven by the fundamental factors today, you should be careful not to suffer a heavy loss.

The German Retail Sales could increase by 0.5%, less versus the 0.6% in the previous reporting period, while the German Unemployment Change could remain in the negative territory, at -5K for the second month in August. Moreover, the CPI Flash Estimate is expected to increase by 1.6%, more versus the 1.5% in the former reading period, while the Core CPI Flash Estimate may increase by 1.2%.

The price failed to break below the confluence area formed at the intersection between the WL4 and the upper median line (uml) of the ascending pitchfork, signaling a rebound. EUR/CHF retested the upper median line (uml) of the minor ascending pitchfork.

A breakdown was somehow expected after the false breakout above the WL3 and above the WL5. We’ll see what will happen in the upcoming days because the failure to reach the median line (ml) of the descending pitchfork announces a bullish momentum towards the upper median line (uml) of this pitchfork.

Dollar Takes Month End Hit Despite Upbeat Data, Quarter-End Profit-Taking In Play?

Greenback Dips Despite Upbeat Data. Even though the most of U.S. data numbers were in the green, underscoring the odds of more Fed tightening moves down the line, the dollar happened to be the worst-performing currency for the day, as investors looked to take profits on the greenback’s rally this week ahead of the end of the quarter.

Aussie Bounces After Steep Fall. The Aussie suffered a steep sell off following proposed changes to both private and corporate tax systems by U.S. president Donald Trump. Having found support at 0.78 the Aussie rallied into the close as profit taking and quarterly position management forced a correction in the USD. Attentions now turn to next Tuesday’s RBA rate announcement and monetary policy statement for further direction and guidance on monetary policy divergence. As we watch key support at 0.78, a break and consolidated close below this threshold could signal a shift in short term ranges.

Loonie Higher as US Dollar Rally Loses Steam. The Canadian dollar gained on its U.S. counterpart, after earlier touching a four-week low, helped by steadier oil prices. The currency pair is trading at 1.2430 as the boost from the Fed and President Trump’s short lived tax plans, mounting a comeback ahead of GDP data later in the day.

Gold Rebounds from 6-Week Low, Silver Bounces Higher as US Dollar Drops. The gold price was up 90 cents to US$1,288.70 an ounce. Gold has rebounded above a six-week low, as the US dollar has turned lower and ushered in short-covering. Bullion was earlier pressured on proposed US tax reforms and strong economic data that supported the case for another US interest rate hike this year. Silver rose to as high as $16.892 and ended with a gain of 0.54%, while copper climbed five cents to US$2.98 a pound.

Oil Dropped Over 1% on Profit Taking, But Retains Grip on Monthly, Quarterly Gains. Oil prices finished lower Thursday, pulling back after hefty month-to-date gains as traders take positions ahead of the conclusion of the third quarter. Crude oil fell 58 cents to US$51.56 per barrel, Brent crude shed 49 cents to $57.41 a barrel ahead of the contract’s expiration at Friday’s finish, natural gas gave back four cents at US$3.02 per MMBtu.

Watch Out Today for:

08:00 am GMT: EUR Unemployment Change (Sep)

09:00 am GMT: EUR Consumer Price Index

12:30 pm GMT: USD Core Personal Consumption Expenditure – Price Index

14:15 pm GMT: EUR ECB President Draghi’s Speech

14:45 pm GMT: GBP BOE’s Governor Carney speech

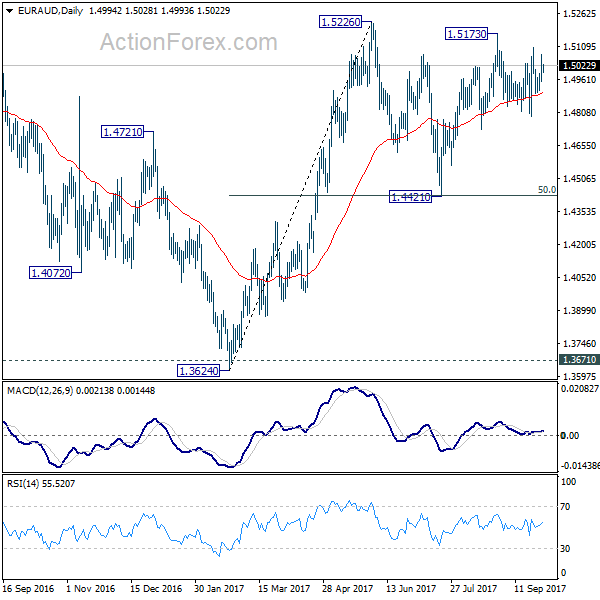

EUR/AUD Daily Outlook

Daily Pivots: (S1) 1.4940; (P) 1.5007; (R1) 1.5065; More....

Intraday bias in EUR/AUD remains neutral as consolidation continues in range of 1.4791/5173. On the upside, break of 1.5173/5226 resistance zone will finally resume larger rise from 1.3624. On the downside, break of 1.4791 support will turn bias to the downside and extend the fall from 1.5173 to retest 1.4421 support.

In the bigger picture, we're holding on to the view that corrective decline from 1.6587 medium term top has completed at 1.3624. Rise from 1.3624 is expected to extend to retest 1.6587. The corrective structure of the price actions from 1.5226 is affirming this view. Above 1.5226 will target a test on 1.6587 key resistance. However, break of 1.4421 support will dampen our view and would drag EUR/AUD lower to retest key support zone around 1.3624.

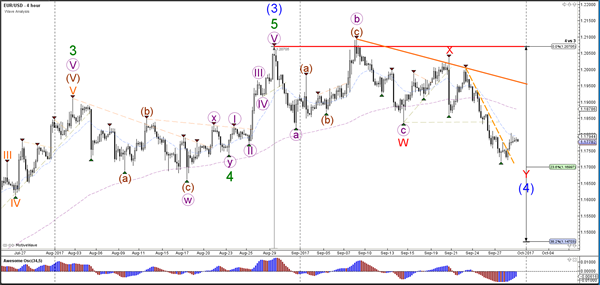

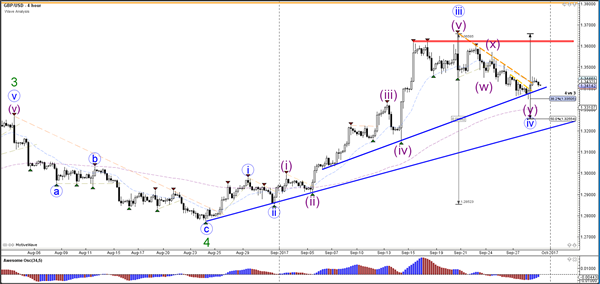

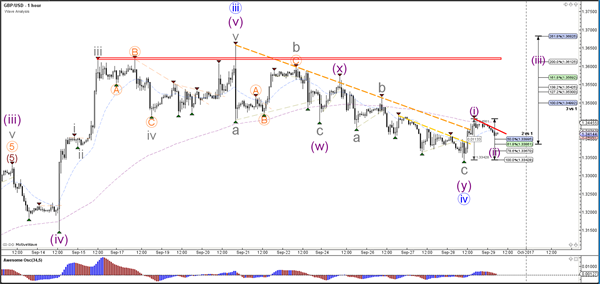

Daily Wave Analysis: EUR/USD, GBP/USD Bounce At Fibonacci Levels And Break Resistance Lines

Currency pair EUR/USD

The EUR/USD bounced at the 23.6% Fibonacci support level of wave 4 (blue). Price broke above the steep trend line (dotted orange) and could be ready to test the resistance levels at 1.1850 at 1.1950. A failure to break these resistance zones could indicate a larger expanded correction within wave 4 (blue).

The EUR/USD broke above 2 resistance trend lines (dotted lines) and could be building either a bullish 123 or ABC wave. Price is now building a small triangle (red/blue lines).

Currency pair GBP/USD

The GBP/USD bounced at the 38.2% Fibonacci level of the potential wave 4 (blue). The Fibonacci levels are acting as a support for a continuation of the uptrend via wave 5.

The GBP/USD has also broken above the resistance trend line (dotted lines) and could be building either a wave 123 or ABC. A new break above resistance (red) could indicate a bullish continuation

Currency pair USD/JPY

The USD/JPY is testing the support trend line (blue). A bounce could indicate the continuation within wave 5 (blue) whereas a break could indicate the end of wave 1 or wave A at the recent high.

The USD/JPY could potentially have completed an ABC (orange) correction within wave 4 (purple) at the 61.8% Fibonacci support level. The support and resistance trend lines will indicate to which direction price will break.