Sample Category Title

European Indices Trade Higher as Rising Bond Yields Lift the Financial Sector

**Notes/Observations**

- German inflation flat to slightly higher, while Spanish inflation beats expectations

- BoE Carney comments soften Cable as the BoE will aim to achieve CPI goal in smooth way

- Higher Bond yields push financials higher

Overnight

Asia:

- RBNZ left rates unchanged as expected, noting that weaker currency is best for dealing with tradables inflation

- Hong Kong property names were weaker on another Chinese city adding property curves.

- Japan PM Abe dissolved lower house to make way for snap elections announced for 22nd Oct

- Toshiba sale of chip finally signed to Bain led consortium for ¥2T

Europe:

- German regional CPI reading largely flat to slightly higher m/m; Spanish prelim CPI comes in stronger

- Slight weakness in Cable as BoE Gov Carney says will aim to achieve CPI goal in smooth way, will support economy though Brexit adjustment; cannot prevent weaker real income growth likely to accompany Brexit

- German Economic Institutes Fall Forecast: Raises 2017 GDP +1.9% (prior 1.5%); 2018 GDP 2.0% (prior 1.8%) as speculated; notes In this environment, the ECB should prepare for the exit from its very expansive monetary policy and in particular from its unconventional measures.

- Swedish Retail giant H&M reports results which missed estimates, shares fall over 5%

Americas

- US President Trump proposes US tax overhaul in line with speculation; doubts remain over deficit following proposed tax cuts

Economic data

- (DE) GERMANY SEPT CPI NORTH RHINE WESTPHALIA M/M: 0.1% V 0.1% PRIOR; Y/Y: 1.9% V 1.9% PRIOR

- (DE) GERMANY SEPT CPI SAXONY M/M: 0.2% V 0.2% PRIOR; Y/Y: 2.0% V 1.9% PRIOR

- (DE) Germany Sept CPI Brandenburg M/M: 0.2% v 0.1% prior; Y/Y: 1.6% v 1.8% prior

- (DE) Germany Sept CPI Bavaria M/M: 0.2% v 0.2% prior; Y/Y: 1.8% v 1.8% prior

- (DE) Germany Sept CPI Hesse M/M: 0.3% v 0.0% prior; Y/Y: 2.1% v 1.8% prior

- (EU) EURO ZONE SEPT BUSINESS CLIMATE INDICATOR: 1.34 V 1.12E; FINAL CONSUMER CONFIDENCE: -1.2 V -1.2E

- Economic Confidence: 113.0 v 112.0e

- (ES) SPAIN SEPT PRELIMINARY CPI M/M: 0.2% V 0.1%E; Y/Y: 1.8%E V 1.6%E

- (DE) GERMANY OCT GFK CONSUMER CONFIDENCE: 10.8 V 11.0E

- (ES) Spain Aug Adjusted Retail Sales Y/Y: 1.6% v 2.0%e; Retail Sales (unadj): 1.7% v 0.7% prior

- **Fixed Income Issuance:

- (IT) ITALY DEBT AGENCY (TESORO) SELLS TOTAL €4.5B VS. €3.5-4.5B INDICATED IN 5-YEAR AND 10-YEAR BTP BONDS

SPEAKERS/FIXED INCOME/FX/COMMODITIES/ERRATUM

**Equities**

Indices [Stoxx600 +0.1% at 385.8, FTSE +0.1% at 7319, DAX +0.4% at 12701 , CAC-40 +0.2% at 5293 , IBEX-35 +0.3% at 10399 , FTSE MIB +0.1% at 22653, SMI +0.2% at 9117 , S&P 500 Futures flat]

Market Focal Points/Key Themes: European stocks opened slightly higher and remained in the same direction as the session; financials supported by bank shares moving higher on bond yields; materials stocks pulled own by commodity prices, including oil to impact energy stocks; plethora of speakers kept macro attention; upcoming earnings in the US session include Accenture and Blackberry

Equities

- Consumer discretionary: Applus APPS.ES -2.6% (acquisition), Hennes & Mauritz HMB.SE -5.1% (results), Orpea ORP.FR -2.3 (analyst action), TUI TUI.UK -1.1% (results)

- Consumer staples: Imperial Brands IMB.UK -2.6% (trading update)

- Financials: Ageas AGS.BE -1.4% (analyst action), Coface COFA.FR +3.9% (results), Mapfre MAP.ES -2.1% (analyst action)

- Industrials: Balfour Beatty BBY.UK +4.3% (analyst action), Flughafen Zurich FHZN.CH +2.1% (analyst action), Hapag-Lloyd HLAG.DE +0.3% (capital increase)

- Healthcare: Abivax ABVX.FR +8.9% (positive study results), Bavarian Nordic BAVA.DK +3.2% (contract)

- Technology: Agfa Gevaert AGFB.BE +6.8% (analyst action), Dassault Systems DSY.FR +0.3%(acquisition), Rocket Internet RKET.DE +5.6% (asset sale, results)

- Utilities: Direct Energie DIREN.FR -5.5% (results)

Speakers

- (UK) Bank of England (BOE) Gov Carney: Will aim to achieve CPI goal in smooth way; Will support economy through Brexit adjustment - speaks at conf in London

- (FI) ECB's Liikanen (Finland): ECB inflation target is symmetrical; forward guidance now permanent tool of ECB policy

- (EE) ECB's Hansson (Estonia): Rates to remain low at least until QE is continuing ; Euro FX rate is still close to historic average

- (EU) ECB's Praet (Belgium): We want sustainable inflation not due to seasonal data - speaks in Berlin

- (EU) EU's Moscovici: EU has made major progress on banking union - comments from Stockholm -German Economic institute "In this environment, the ECB should prepare for the exit from its very expansive monetary policy and in particular from its unconventional measures; ECB should in short term announce tapering of Bond-buying programme from beginning of next year if economic conditions remain favorable

- (SE) Sweden Central Bank (Riksbank) Gov Ingves: monetary policy needs to remain expansionary - comment from Parliament

- (UK) PM May: Never any disagreement about aim of BOE policy - BOE conf

- Much work to do to restore UK finances to health

- (JP) Japan Gov Koike: wants to study phasing out Japan nuclear power by 2030

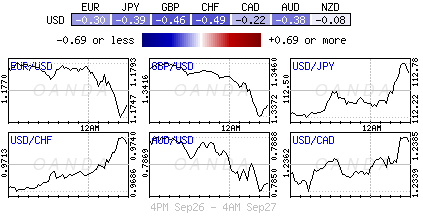

Currencies

- GBPUSD fell after soothing comments from BoE Gov Carney, as the pair finds support at 1.3345. Resistance stands just below 1.34

Fixed Income

- Bund futures trade at 160.63 down 31 as the global duration slide continues, Treasuries fueled losses in large volumes. Continued downside targets 160.25 while upside resistance stands initially at 162.07, followed by 163.27.

- Gilt futures trade at 123.45 down 22 ticks as the markets focus on BOE Gov Carney and PM May's comments at the BOE conference. Continued downside eyeing 123.06. Upside targets 124.90 then 125.24.

- Thursday's liquidity report showed Tuesday's excess liquidity fell to €1.723T from €1.725T and use of the marginal lending facility rose to €131M from €49M.

- Corporate issuance saw $5.5B come to market via 3 issuers headlined by Credit Agricole $1.5B senior notes and EQT $3.5B 4-part senior unsecured note offering

Looking Ahead

- 05:30 (ZA) South Africa Aug PPI M/M: 0.3%e v 0.5% prior; Y/Y: 4.1%e v 3.6% prior

- 07:00 (BR) Brazil Sept FGV Inflation IGPM M/M: 0.5%e v 0.1% prior; Y/Y: -1.5%e v -1.7% prior

- 08:00 (DE) Germany Sept Preliminary CPI M/M: 0.1%e v 0.1% prior; Y/Y: 1.8%e v 1.8% prior

- 08:05 (UK) Baltic Dry Bulk Index

- 08:30 (US) Aug Advance Goods Trade Balance: -$65.1B v -$63.9B prior

- 08:30 (US) Q2 Final GDP Annualized (3rd reading) Q/Q: 3.2%e v 3.0% prelim; Personal Consumption: 3.3%e v 3.3% prelim

- 08:30 (US) Q2 Final GDP Price Index: 1.0%e v 1.0% prelim; Core PCE Q/Q: 0.9%e v 0.9% prelim

- 08:30 (US) Initial Jobless Claims: No est v K prior; Continuing Claims: No est v M prior

- 08:30 (US) Weekly USDA Net Export Sales

- 08:30 (US) Aug Preliminary Wholesale Inventories M/M: 0.4%e v 0.6% prior

- 09:00 (RU) Russia Gold and Forex Reserve w/e Sept 22nd: No est v $ prior

- 10:30 (US) Weekly EIA Natural Gas Inventories

- 11:00 (US) Sept Kansas City Fed Manufacturing Activity: 14e v 16 prior

- 14:00 (MX) Mexico Central Bank (Banxico) Interest Rate Decision: Expected to leave Overnight Rate unchanged at 7.00%

- 15:00 (AR) Argentina Aug Industrial Production Y/Y: No est v 5.9% prior

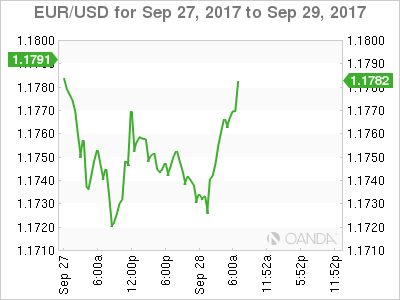

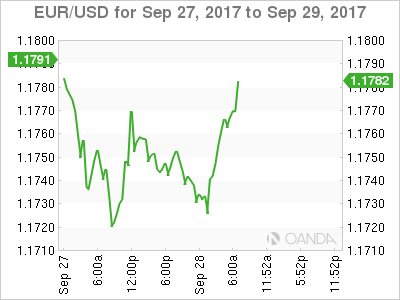

EURUSD Starts to Recover

The EURUSD pair has started to recover yesterday's losses during the European trading session, after traders failed to push price below its key 200-week moving average, whilst the U.S dollar index pulled back from five-week trading highs.

After three days of heavy trading losses, the intraday sentiment surrounding the euro currency is currently neutral, ahead of German inflation data, with sellers and buyers currently battling around the 1.1770 region.

Earlier, the EURUSD pair found intraday support from the 1.1720 level, which further encouraged euro buying interest as the sellers failed to push-price below the former daily price-low.

A move above the 1.1800 level should help lift sentiment surrounding the pair, whilst a move below 1.1720 should encourage selling towards 1.1660.

Key intraday support for the EURUSD pair is found at the pairs 50-hour moving average, at 1.1764, and the pairs daily pivot, at 1.1751. Below the daily pivot, the 1.1720 and 1.1716 levels become critical intraday support.

Key intraday resistance is located at 1.1780 and the key 1.1800 level. Once above the 1.1800 level, the pairs 100-hour moving average offers strong intraday resistance, at 1.1833.

USDJPY Slips Below Key Support

The USDJPY pair has slipped below the support, at 112.71, with today's pullback driven by a move lower in the U.S dollar index and a bearish double-top pattern formation, on the lower time-frame price-charts.

On an intraday basis, the sentiment surrounding the USDJPY pair is bearish below the 112.71 level, with a deeper technical pullback expected while trading below this key support level.

Traders will now look to the U.S trading session, where we see the release of the latest revision of second quarter United States Gross domestic product.

The U.S dollar index is also likely to dominate the intraday trend on the USDJPY pair, especially the 93.00 level on the U.S dollar index and the index's key 200-week moving average, at 92.82.

Key intraday technical support is found at the pairs 50-hour moving average, at 112.60, and the recent pullback low, at 112.38. Below 112.38, further support is found at 112.20 and the USDJPY weekly pivot, at 111.90.

To the upside, key intraday resistance is found at 112.70-79, with further technical resistance above 112.79 located at 113.02, 113.25 and 113.57.

CAC Unchanged Ahead of French Consumer Spending, Inflation Reports

The CAC index is unchanged in the Thursday session. Currently, the index is at 5,283.75, up 0.03% on the day. There are no French or eurozone indicators on the schedule. On Friday, France releases Consumer Spending and Preliminary CPI.

French President Emmanuel Macron wants to further integrate the eurozone, and has proposed that the bloc should have its own budget and finance minister. On Tuesday, Macron went as far as proposing that Germany and French completely integrate their markets and corporate rules by 2024. However, Macron may find serious resistance to his plan in post-election Germany, where a weakened Angela Merkel will have her work cut out cobbling together a coalition. Merkel made a first move by appointing her former finance minister, Wolfgang Schaeuble as president of parliament. This astute move clears the path for the pro- business FDP party, which has insisted on the powerful finance portfolio, to join a coalition with Merkel. The FDP is fiscally hawkish and is strongly opposed to Germany continuing to finance weaker eurozone members, such as Greece. If the FDP does take part in the government, Merkel may have to shift away from her pan-European vision, which could ice Macron's proposal to further integrate the eurozone.

On Tuesday, German industrial giant Siemens AG announced that it would merge rail operations with Alstom SA, a French train manufacturer. The merger is aimed as a response to growing competition in the rail transport sector, particularly from the Chinese state-owned railroad, CRRC. The merger still needs to be approved by regulators, but is already being hailed as an important deal which will strengthen economic ties between France and Germany and will help Europe compete on the global stage. French finance minister finance minister Bruno Le Maire has said that he will ensure the deal, which still must be approved by regulators, does not result in any job losses at Alstrom.

Trump Tax Plan Sends Dollar, Bond Yields Higher

Thursday September 28: Five things the markets are talking about

The Trump reflation trade is coming back in vogue with a bit more details on the U.S tax plans.

The dollar and global sovereign yields have rallied after President Trump yesterday proposed the biggest shake-up of the U.S tax system in thirty-years and strong U.S data further supports the case for another Fed rate hike later this year.

Nevertheless, investors should expect the proposed bill to face an uphill battle in congress with Trump's own Republican Party divided over it and Democrats hostile as critiques suggest the plan favours businesses and the rich and could add trillions of dollars to the U.S deficit.

Today's U.S data on GDP and personal spending (08:30 am EDT) should provide further clues as to the potential Fed policy path.

1. Stocks mixed signals

Global equities trade mixed as investors began to assess the implications of the much-anticipated U.S tax proposal.

In Japan, stocks rebounded overnight after Wall Street gained and the dollar rallied against the yen (¥112.81) on hopes that President Trump may be making progress on his tax plan. The Nikkei gained +0.5%, while the broader Topix rallied +0.7%.

Note: Japan's PM Abe dissolved lower house to make way for snap elections announced for Oct. 22

In Hong Kong, stocks fell, mirroring weakness in some other Asian markets, as investors worried about a possible slowdown in China await Q3 economic data. The Hang Seng index ended down -0.8%, while the China Enterprises Index lost -1.5%.

In China, equities were little changed as investors await Q3 data and counted down to a weeklong National Day holiday starting on Sunday. The blue-chip CSI300 index was unchanged, while the Shanghai Composite Index was down -0.2%.

Note: Mixed August data have raised concerns that China economic recovery could be losing steam.

In Europe, regional indices are trading mostly higher as rising bond yields lift the financial sector, materials stocks are being pulled own by commodity prices, including oil which is impacting energy stocks.

U.S stocks are set to open little changed.

Indices: Stoxx600 +0.1% at 385.8, FTSE +0.1% at 7319, DAX +0.4% at 12701, CAC-40 +0.2% at 5293, IBEX-35 +0.3% at 10399 , FTSE MIB +0.1% at 22653, SMI +0.2% at 9117 , S&P 500 Futures flat

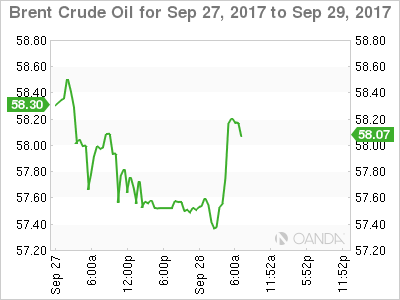

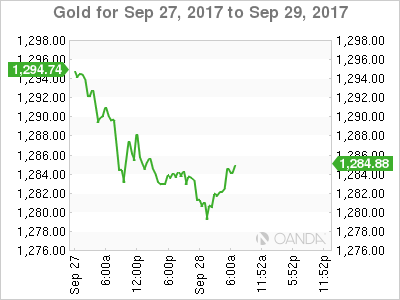

2. Oil steadies as North Iraq, Kurdish pipeline stays open, gold melts

Oil prices trade steady, taking a breather after gains spurred by rising tension in northern Iraq following Kurdistan region's vote for independence in a referendum.

Brent crude oil is unchanged at +$57.90 a barrel. On Tuesday, it hit a two-year high print of +$59.49 after Monday's referendum vote prompted Turkey to threaten to close the region's oil pipeline, before pulling back.

U.S. light crude is +5c higher at $52.19 after rising +26c yesterday to just below a five-month high.

U.S. crude prices found some support from a surprise fall in U.S stocks. Crude inventories fell -1.8m barrels last week according to the U.S. Energy Department, versus forecasts for a +3.4m build.

Note: The crude ‘bears' remain sceptical about further price gains due to higher oil output from the U.S. The EIA said that production from wells in shale formations would rise for a 10th month in a row in October.

Gold fell to a new one-month low overnight as the ‘big' dollar rallied on expectations of a U.S interest rate hike in December. Spot gold is down -0.2% at +$1,278.36 per ounce, as strong U.S economic data took sheen off the precious metal.

3. A global bond rout deepens

The prospect of higher U.S debt levels and expectations for another Fed hike has sent 10-year Treasury yields to their highest since mid-July, with the 2-10 year yield curve steepening to its highest in a month.

Comments this week from Fed Chair Janet Yellen that the U.S central bank needs 'to continue with gradual rate hikes' have cemented expectations for policy tightening by year-end.

Note: U.S two-year notes are the most sensitive to overnight rates – yields have backed up to a nine-year high of +1.49% in anticipation of a rate rise in December.

The yield on U.S 10's has gained +3 bps to +2.34%, the highest in more than two months. In Germany, 10-year Bund yields increased +3 bps to +0.49%, the highest in almost two months, while the U.K's 10-year Gilt yield has climbed +1 bps to +1.398%, the highest in eight months.

4. Dollar gets a lift from Tax cuts, and Fed expectations

Expectations that the Fed will continue to raise interest rates and the prospect of U.S tax reform has boosted the dollar across the board. Are its gains short lived?

The EUR (€1.1764), GBP (£1.3373), and CAD (CA$1.2478) are all trading higher from their worst levels seen overnight, as too is yen (¥112.82) with the dollar after having hit a three-month high of ¥113.26 yesterday.

EUR ‘bears' continue to see a potential risk of the single unit falling as low as €1.15 if investors remain worried about German politics and optimism about the U.S.

Note: After Sunday's German elections, worries have resurfaced about the rising populism in the eurozone, and about whether Chancellor Merkel and French President Macron will be able to strike a deal on deeper eurozone financial integration.

Down under, the Reserve Bank of New Zealand (RBNZ) left rates unchanged as expected yesterday, noting that weaker currency ((NZ$0.7186) is best for dealing with 'tradable inflation.'

5. Eurozone business, consumer confidence surges

Data this morning showed that the EC's Economic Sentiment Indicator for September was stronger than expected, rising to 113.0 from 111.9, compared with a consensus forecast of 112.0.

It's the highest level since June 2007, and included Germany, France, Italy and Spain. The rise is a fresh sign that the economy has grown in Q3 at roughly the pace it did in Q2, and suggest that the region is poised for robust end to the year.

The data would also suggest that businesses and households are not that concerned about the prospect of a reduction in ECB stimulus sometime soon.

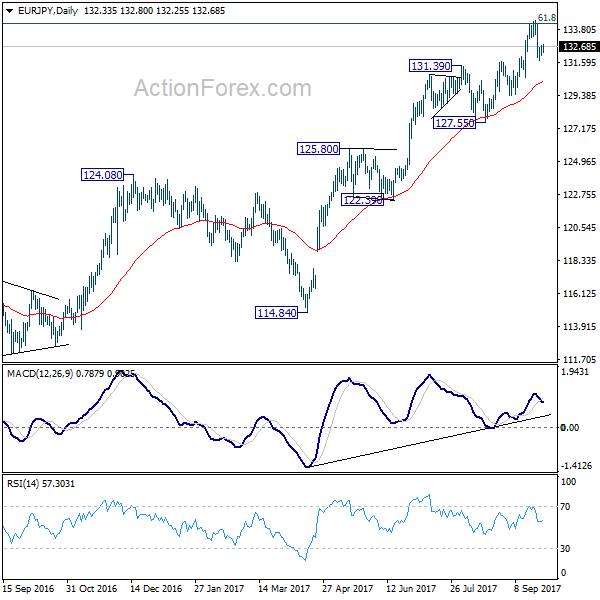

EUR/JPY Daily Outlook

Daily Pivots: (S1) 132.13; (P) 132.43; (R1) 132.79; More...

Intraday bias in EUR/JPY remains neutral as corrective trading from 134.39 is still in progress. Outlook stays bullish as long as 131.69 support holds. Above 133.02 minor resistance will turn bias back to the upside. Sustained break of 134.20 fibonacci level will extend larger up trend to 141.04 resistance next. However, break of 131.69 will be an early sigh of medium term reversal and will target 127.55 key support level instead.

In the bigger picture, current rise from 109.03 is seen as at the same degree as the down trend from 149.76 (2014 high) to 109.03 (2016 low). 61.8% retracement of 149.76 to 109.03 at 134.20 is already met. Sustained break there will pave the way to key long term resistance zone at 141.04/149.76. On the downside, break of 127.55 support is needed to be the first signal of medium term reversal. Otherwise, outlook will remain bullish.

GBP/JPY Daily Outlook

Daily Pivots: (S1) 150.48; (P) 151.04; (R1) 151.56; More

No change in GBP/JPY's outlook. Correction from 152.82 could extend lower. But downside is expected to be contained by 38.2% retracement of 141.17 to 152.82 at 148.36 to bring rally resumption. Break of 152.82 will extend the larger rise from 122.36 to 61.8% projection of 122.36 to 148.42 from 139.29 at 155.39 next.

In the bigger picture, medium term rebound from 122.36 is in progress. Firm break of 38.2% retracement of 196.85 to 122.36 at 150.43 will carry long term bullish implications. In that case, GBP/JPY could target 61.8% retracement at 167.78. For now, the bullish scenario is preferred as long as 139.29 support holds.

CRUDE OIL Consolidating Below 52

Crude Oil is edging higher above the $50 level. Key support is given at 45.40 (17/08/2017 high). Strong resistance found at 52.43 (26/09/2017) has been broken. Expected to show another leg higher.

In the long-term, crude oil has recovered after its sharp decline last year. However, we consider that further weakness are very likely. Strong support lies at 35.24 (05/04/2016) while resistance can now be found at 55.24 (03/01/2017 high).

SILVER Monitoring Support At 16.58

Silver has reversed and has broken uptrend channel by breaking support implied by its lower bound. Strong resistance is given at 18.65 (17/04/2017 high) while support can be found at 16.58 (15/08/2017 high). Expected to show further bearish move.

In the long-term, the trend is rater negative. Further downsides are very likely. Resistance is located at 25.11 (28/08/2013 high). Strong support can be found at 11.75 (20/04/2009).

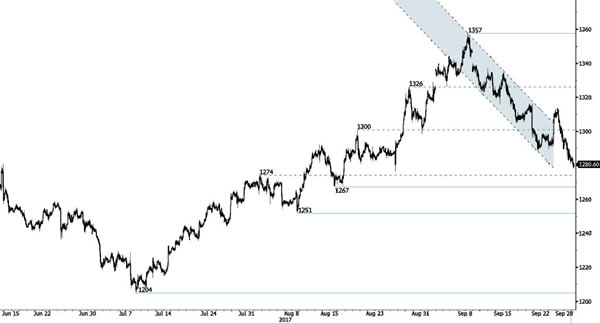

GOLD Long-Term Bearish Consolidation

Gold has weakened again below 1300. Hourly support is now given at 1277 (intraday low). Hourly resistance is located at 1357 (08/09/2016). Stronger support lies at 1204 (10/07/2017 high). Expected to show further bearish move.

In the long-term, the technical structure suggests that there is a growing upside momentum. A break of 1392 (17/03/2014) is necessary ton confirm it, A major support can be found at 1045 (05/02/2010 low).