Sample Category Title

Euro Risks Further Losses

The euro risks further losses against the U.S dollar in Wednesday trading, with sentiment surrounding the euro remaining weak. Buying demand above the 1.1800 level is currently still lacking, after yesterday's steep decline to 1.1754.

Today's key risk event for the EURUSD pair will be the release of the Trump administrations tax reforms, the reaction to the proposed reforms will likely create tremendous volatility in the U.S dollar index.

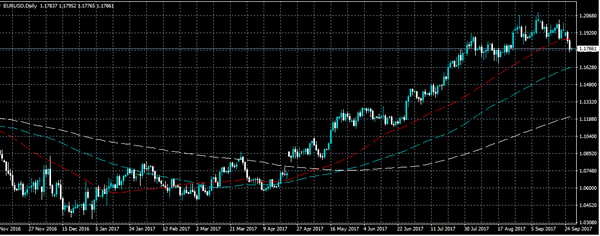

Going forward, the EURUSD pair remains strongly intraday bearish while trading below its 50-day moving average, currently located at 1.1867.

Key intraday technical support is found at 1.1774, 1.1754 and the August 21st price-low, at 1.1731. Below 1.1731, key monthly support is found at the euro's 200-week moving average at 1.1716, and the former monthly price-low, at 1.1662.

To the upside, intraday rallies in the EURUSD pair should find resistance from the daily pivot point, at 1.1804, and the September 9th swing-low, at 1.1838. Above 1.1838, further euro resistance is found at 1.1851 and 1.1867.

.

Economic Data, Monetary Policy Takes Centre Stage On Wednesday

Investors can expect an active session on Wednesday headlined by central bank speeches and high-profile economic data.

In terms of economic data, a pair of consumer confidence reports from France and Italy will be released in the early European session. Both indicators are expected to show no change for September.

The Centre for European Economic Research (ZEW) will report on Switzerland business expectations for the month of September. The monthly report provides a barometer of business health for one of Europe’s most important economies.Italian industrial production data will be released at 09:00 GMT. The report is used to gauge the state of manufacturing in the Eurozone’s third-largest economy.

The biggest data release of the day takes place on the North American circuit. At 8:30 GMT, the US Department of Commerce will issue the latest report on durable goods orders.

Orders for goods meant to last three years or more likely rose 1% in August, according to a median estimate of economists. Durable goods orders plunged 6.8% in June, offsetting large gains the month before.

Excluding transportation equipment, durable goods orders likely rose 0.2%.

The National Association of Realtors’ pending home sales index will also be released at 14:00 GMT. Pending home sales likely fell 0.5% in August, analysts say.

Shifting gears to monetary policy, Bank of Canada (BOC) Governor Stephen Poloz will make the news rounds at 15:45. Poloz heads the only major central bank not named the Federal Reserve to raise interest rates. Investors widely expect the BOC to hike rates for a third time before year’s end.

South of the border, Federal Reserve Bank of St. Louis President James Bullard will deliver a speech at 17:30 GMT. A half hour later, Federal Open Market Committee (FOMC) member Lael Brainard will deliver remarks.

EUR/USD

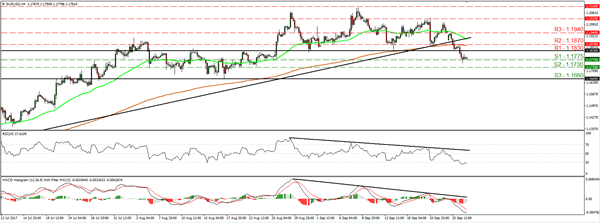

The euro’s correction continued for a second consecutive day on Tuesday, with the EUR/USD falling below 1.1800 for the first time in over a month. The pair was little changed leading into the European session. From a technical perspective, the pair is looking at a possible bearish correction now that price action has fallen below 1.1830. Investors should, therefore, be on the lookout for a broader correction in the short term.

GBP/USD

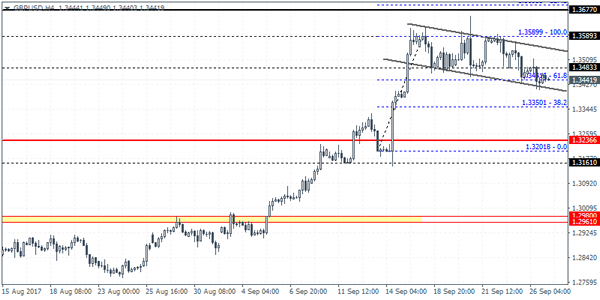

In a sign of exhaustion, the British pound drifted lower on Tuesday to reach an intraday low of 1.3409 US. Cable would later recover to close near the 1.3460 region. Prices were down again in Asian trade. Investors should keep an eye on the 1.3449 level, which corresponds to the 23.6% Fibonacci retracement of the recent bullish uptrend. A break below that level could expose the pair to significant losses over the short term.

USD/CAD

The USD/CAD has consolidated off multiyear lows, with prices currently trading in the mid-1.23 region. However, the short-term picture remains bearish as the BOC eyes further rate adjustments. Oil prices are also trading at multiyear highs (in the case of Brent), which is a strongly bullish sign for the loonie.

Yellen Reveals Little On Policy, Tax Reform In Focus

Fed Chair Yellen revealed almost nothing new on policy yesterday, reiterating that the shortfall in inflation this year remains largely a mystery. The Fed chief maintained a very balanced approach, noting that both very rapid and very gradual rate hikes could weigh on the economy. The reaction in USD was volatile, but limited.

The focus of USD traders now turns to the Trump administration’s highly-anticipated tax plan, which is expected to be unveiled today. According to market chatter, the plan will include a reduction of the corporate tax rate to 20%, from 35% currently. It is also anticipated to contain a one-off repatriation of corporate cash held abroad, at a reduced tax rate. Even though the rate that would be applied is still unclear, the last time this occurred back in 2004, the applicable rate was a mere 5.3%. Coming on top of a potential reduction in corporate taxes, a low repatriation rate could support the US dollar, we think, on speculation that massive amounts of offshore cash will return to the US, thereby raising demand for the currency.

Having said all these, even though an optimistic tax plan could prove positive for the dollar and US equity markets on the announcement, we have to sound a note of caution, as the final version of this plan may look very different than what the administration unveils today. Once the plan is announced, a lengthy negotiating process will begin in Congress, implying that many parameters may be altered in order for lawmakers to vote in favor of it. This suggests lots of headlines, and possibly increased volatility for USD over the next months.

EUR/USD tumbled yesterday, falling below the key support (now turned into resistance) territory of 1.1830 (R1). The break below that barrier confirmed a forthcoming lower low on the 4-hour chart and in our view, it signaled a short-term trend reversal. At the time of writing, the rate is testing the 1.1775 (S1) support line, where a dip could initially aim for our next support of 1.1730 (S2). Another break below that level is possible to carry extensions towards the 1.1660 (S3) zone. A favorable US tax plan today may be the catalyst for more declines.

Will the RBNZ reiterate its exchange rate concerns?

During the early Asian morning Thursday, the RBNZ rate decision will take center stage. The consensus is for the Bank to take no action once again. At its latest gathering, the RBNZ kept the timing of its first planned rate hike unchanged for Q1 2020, and expressed discomfort about the up-until-then strength of the Kiwi. In fact, after the meeting, Governor Wheeler even said that the option of FX intervention is always on the table.

Since that gathering, the only economic developments worth mentioning was a modest slide in the Bank’s 2-year inflation expectations for Q3, and a strong acceleration in GDP for Q2. Perhaps more importantly, the NZD is trading at very similar levels as it was back then. Bearing these in mind, we think that the Bank is unlikely to change its language drastically, and we see the case for policymakers to reiterate their NZD-related concerns. Something like that could extend the latest election-induced pullback in NZD.

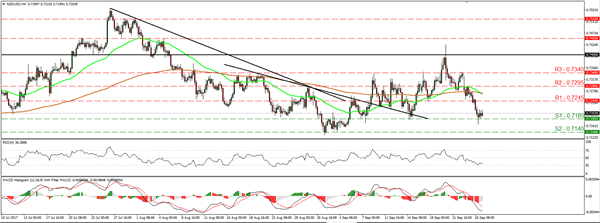

NZD/USD continued tumbling on Tuesday. The pair fell below the support (now turned into resistance) of 0.7245 (R1) and currently it is testing the 0.7185 (S1) support. Taking into account the election outcome over the weekend and the rejection from above 0.7400 last week, we believe that the pair is poised to continue trading south. If RBNZ policymakers reiterate concerns around the Kiwi tonight, the pair could fall below 0.7185 (S1), something that may open the way for our next support of 0.7140 (S2).

As for the rest of today’s highlights:

During the European morning, we get Norway’s AKU unemployment rate for July, as well as Sweden’s consumer and manufacturing confidence indices for September. In the US, durable goods orders for August are due out. The headline rate is expected to have risen following a steep decline in July, while the core rate is expected to have slid, but to have remained within the positive territory. On balance, the market may place more emphasis on a potential decline in the core rate.

We have five speakers on the schedule: Bank of Canada Governor Stephen Poloz, Norges Bank Governor Oystein Olsen, Fed Board Governor Lael Brainard, St. Louis Fed President James Bullard, Minneapolis Fed President Neel Kashkari. We would pay extra attention to Poloz, as he could echo BoC Lane’s concerns about CAD.

EUR/USD

Support: 1.1775 (S1), 1.1730 (S2), 1.1660 (S3)

Resistance: 1.1830 (R1), 1.1870 (R2), 1.1940 (R3)

NZD/USD

Support: 1.1775 (S1), 1.1730 (S2), 1.1660 (S3)

Resistance: 1.1830 (R1), 1.1870 (R2), 1.1940 (R3)

Dollar Stronger On Hawkish Yellen But Eyes On Tax Plans, Kiwi Weak Ahead Of RBNZ Meeting

Fed Chair Janet Yellen, held a hawkish stance on the Fed’s rate path on Tuesday, boosting the dollar to a fresh one-month high against a basket of major currencies. On Wednesday, dollar sentiment is expected to be positive as markets anticipate the Congress to welcome Republicans’ tax plans after Senate Republicans failed again to replace Obamacare. Meanwhile, the focus will be also on the policy meeting held by the Reserve Bank of New Zealand (RBNZ) later today.

The dollar index stood tall at a fresh one-month high of 93.07 on late Tuesday before it edged down to 92.97 in Asia today after Fed Chair Janet Yellen said in Cleveland that interest rates should continue rising gradually despite weakness in inflation. Particularly she commented that “it would be imprudent to keep monetary policy on hold until inflation is back to 2%”.

Today though, the biggest focus will be on Republicans’ tax plans expected to be received positively by Congress after six months of intensive work by six White House members and congressional Republicans. Yesterday, Trump asked both US Republican and Democrat lawmakers to collaborate on a tax framework saying that “it is time for both parties to come together”. This came after Trump team’s efforts to repeal Obamacare on the same day failed for the second time when Senate members from the same team opposed the administration’s healthcare bill.

Sources familiar with the topic said that Trump’s Republicans are due to suggest a new “pass-through” tax rate of 25% on Wednesday from the current 39.6%, while they are also considering asking for corporate income taxes to be cut from 35% to a target range of 18-23%.

Meanwhile, Trump referring to North Korea’s latest threats on Tuesday eased war tensions, saying that a military response is not America’s “preferred option”, but if needed that would be “devastating” for the North Korean regime.

Safe-haven assets weakened after Trump’s words, with dollar/yen rising by 0.35% on the day to 112.62 and dollar/swissie climbing by 0.40% to 0.9725. Gold retreated by 0.12% to $1,291.60 per ounce.

In Paris, the Pro-European centrist French President Emanuel Macron reiterated his vision on higher EU integration, calling for EU members to unify their efforts on defense and immigration and for the eurozone to have its own budget. However, his ambitious ideas might fall on deaf ears as he will struggle to find support from his German counterpart, Angela Merkel, who is considering to build a coalition with Eurosceptic parties. The coalition-building process in Germany might take from weeks to months.

Euro/dollar touched a fresh one-month high, dropping to 1.1756 amid uncertainties around the German political environment.

In other currencies, the kiwi reversed earlier gains made in Asia before Asian markets close, falling to $0.7178. Kiwi traders will also be cautious on the RBNZ policy meeting later today where forecasts are for interest rates to remain steady at a record low of 1.75% until the end of the year.

In other news out of New Zealand, the leader of the First party, Winston Peters, argued that no coalition agreements would be made until final general election votes, which include overseas ballots, are released on October 7.

The aussie was down by 0.47% at $0.7849, pressured by decreasing metal prices including iron ore which is Australia’s main export.

Dollar/loonie was up by 0.33% ahead of the BOC’s Governor Stephen Boloz’s speech later today.

Regarding oil prices, WTI crude jumped by 0.69% to $52.24 per barrel and Brent rose by 0.48% to $58.72 after the API weekly report indicated that US crude inventories declined by 0.761mn barrels in the past week compared to a rise of 3.40mn barrels expected.

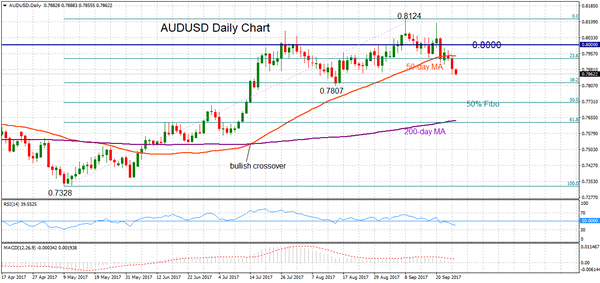

AUDUSD Turns Bearish After Dropping Below 50-Day Moving Average

AUDUSD is turning bearish this week after shifting from a consolidation phase around the key 0.8000 level. After a brief pause, downward momentum resumed once the pair broke below the 50-day moving average at 0.7947. The medium-term bullish trend from May to September is at risk should prices extend lower.

The short-term bias is now bearish based on the RSI dropping below 50 and thereby giving a bearish signal. The first target is the mid-August low at 0.7807. Failure to recover at this support level would increase downward pressure and see prices move towards the 50% Fibonacci retracement level of the uptrend from 0.7328 to 0.8124. This level at 0.7725 is a pivotal level and should AUDUSD break below it then the uptrend from May to September will start to see a reversal and would indicate the medium term bullish trend has ended.

Looking to the upside, there is a resistance area formed by the 23.6% Fibonacci retracement level and the 50-day MA between 0.7934 and 0.7947. A sustained break above these barriers would turn the focus back to the upside. The key psychological level at 0.8000 needs to be broken to see a re-test of the 0.8124 peak, which was the highest level since May 2015. Above this top, AUDUSD would resume the May to September uptrend towards the previous major high at 0.8162 and 0.8294.

A short-term bearish bias is taking shape now but the uptrend from May to September is still intact and the 50-day and 200-day moving averages are still positively aligned. The MACD is still in bullish territory above zero.

Can US Dollar Break 0.9750 Vs Swiss Franc?

Key Highlights

- The US Dollar started an uptrend from the 0.9440 low against the Swiss Franc.

- There is a crucial contracting triangle forming with support at 0.9680 on the 4-hours chart of USD/CHF.

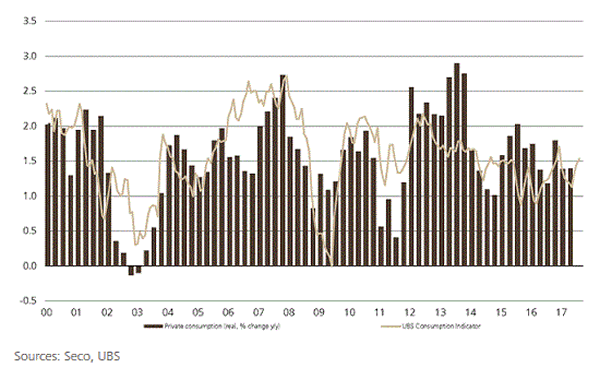

- The UBS Consumption Indicator in Switzerland for August 2017 rose from the last revised 1.46 to 1.53.

- The US Pending Home Sales figure will be released for August 2017, which is forecasted to decline 0.5% (MoM).

USDCHF Technical Analysis

The US Dollar is following a bullish trend and trading well above the 0.9600 support against the Swiss Franc. The USD/CHF pair is facing the next upside challenge near 0.9750, which is a crucial resistance.

Looking at the 4-hours chart of USD/CHF, the pair was rejected twice from the 0.9740-50 resistance levels. The last drop was sharp from 0.9746 to 0.9641. However, a crucial contracting triangle with support at 0.9680 prevented declines.

The pair is once again moving north and already above the 61.8% Fib retracement level of the last decline from the 0.9746 high to 0.9642.

It would be interesting to see if the US Dollar can break 0.9750 this time or not. Another failure would be a strong bearish sign for a reversal towards 0.9600. On the flip side, a break of 0.9750 might call for further gains towards the 0.9800 and 0.9840 levels.

UBS Consumption Indicator

Today in Switzerland, the UBS Consumption Indicator for August 2017 was released. The forecast was slated for a minor rise from the last reading to 1.50.

The actual result was better, as there was a rise in the UBS Consumption Indicator to 1.53. There was a sharp rise in new car registrations and the numbers of hotel stays by Swiss residents.

The report added that:

New car registrations in August boosted the UBS consumption indicator. August saw nearly 6% more new car registrations than the same month last year. The upward trend in overnight hotel stays by Swiss residents also helped. Overnight stays in July increased nearly 3% compared to July 2016.

The overall result was positive, but there was no impact on USD/CHF towards the downside. The pair remains in an uptrend and might soon head towards the 0.9750 level and could even break it.

Economic Releases to Watch Today

US Pending Home Sales for August 2017 (MoM) – Forecast -0.5%, versus -0.8% previous.

US Durable Goods Orders for August 2017 – Forecast +1.0%, versus -6.8% previous

The Market May Require the “Safe Haven” Yen

Despite the correction that took place earlier in September, the Japanese Yen is again strengthening against the USD. The reason is media coverage and investors' growing needs for "safe haven" assets.

Geopolitical situation in Asia is slowly aggravating. There were some comments from North Korea last weekend, which didn't attract investors' attention, but the ones expressed on Monday really made the market nervous. North Korean Ministry of Foreign Affairs perceived Donald Trump's words as the declaration of war. And since the USA has declared a war, North Korean authorities believe that they have every right to accept the challenge. From their point of view, from now on North Korea has the right to shoot down any American strategic aircraft within sight on the Korean territory or even out of sight.

And really, there are some American aircrafts flying not so far after all. Last weekend, they reported on several B-1Bs rather close to the eastern coast of North Korea.

At the same time, we should note that there might be no real military operations: words are words, aggression is aggression, but the very first thoughtless step will cause an entire chain of disastrous consequences, which will be very difficult to settle through peaceful means. This idea can be easily seen in the behavior of the USD/JPY pair: the instrument would return to its highs, unless investors thought otherwise.

At the moment, this is one of the main things that influence the Yen movement. The Japanese fundamental background and news are looking pretty calm during the last September week. The Department of Economic Affairs of Japan says that the country has to work on increasing its economic potential. Japanese authorities would like to see budget surplus in 2018 and say that they're not going to change the sales tax so far, because the country's economy requires some time to become more stable.

If we take a look at the daily chart of the USD/JPY pair, we can see that right now the price is moving inside the descending channel, but is getting closer to the upside border to test or even break it. The key resistance level is close to 113.00. If the instrument breaks it and fixes above, the pair may continue growing to reach the psychologically-crucial level at 120.00. However, this is the mid-term scenario.

The short-term outlook can be better seen at the H1 chart. Here we can see that the pair has finished the ascending impulse and started a new correction with the closest target at 111.35, which is the downside border of the descending channel. The next possible target of this descending movement is close to 110.30. To resume the uptrend, the instrument has to break the resistance level at 112.30. In this case, the price may grow towards its mid-term targets, 113.25 in particular.

XAUUSD Intraday Analysis

XAUUSD (1295.35): The modest rally in gold prices saw a retreat as price fell back to the familiar support zone. Gold prices briefly tested once again the lower end of the support at 1290. However, we can expect to see some near-term upside taking shape once again. A close above 1300 could signal a continuation towards the 1324 - 1320 level. Further gains can be expected only on a breakout above this resistance level with the long-term target at 1345.87.

GBPUSD Intraday Analysis

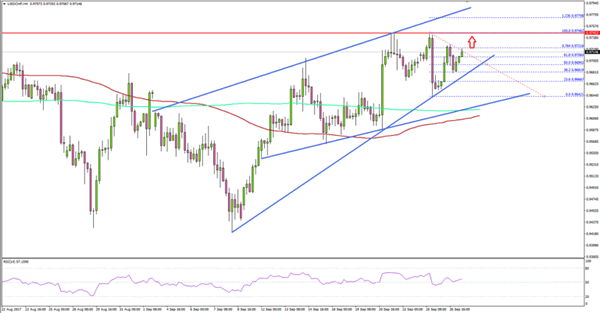

GBPUSD (1.3441): The British pound continues to remain volatile with yesterday's price action closing with a doji pattern. We can expect some downside correction in prices as a result. On the 4-hour chart, the continued consolidation within the bullish flag pattern hints at a possible weakening of this continuation pattern. Price action is sill support in the price zone of 1.3488 - 1.3441. However, a close below this level could signal a correction in the British pound. Lower support level at 1.3236 will be most likely tested as a result.

EURUSD Intraday Analysis

EURUSD (1.1787): The euro continued to post declines against the US dollar yesterday with price action closing below the 1.1822 support level. A break off this support level suggests further decline in prices with the next main support coming into focus at 1.1672. On the 4-hour chart, we can see that the breach of 1.1822 has put the descending triangle pattern into play. However, we can expect some near-term correction back to the broken support level where resistance could now be formed. The downside remains towards the 1.1672 - 1.1688 support level and will mark a short-term correction to the EURUSD rally.