Sample Category Title

Gold Drops to 4-Week Low on Strong Durable Goods Report

Gold has posted losses on Wednesday, continuing the downward trend move which marked the Tuesday session. In North American trade, the spot price for an ounce of gold is $1285.39, down 0.58% on the day. Gold has now slipped 1.9 percent since Tuesday, and is currently trading at its lowest level since August 25. On the release front, key indicators were mixed. Durable Good Orders sparkled with a 1.7% gain, well above the estimate of 1.0%. Core Durable Goods slowed to 0.2%, matching the estimate. Pending Home Sales was unexpectedly soft, posting a decline of 2.5%, compared to an estimate of -0.5%. The US will release two key events – Final GDP and unemployment claims.

What can we expect from the Federal Reserve with regard to interest rate policy? Fed policymakers remain divided on the hot issue of a third and final rate hike in 2017. Fed Chair Janet Yellen waded into the rate debate on Tuesday, as she sent out a surprisingly hawkish message to the markets. Yellen said that she favored gradual rate increases, and voiced confidence that inflation levels would move higher. She added that if the Federal Reserve did not continue to raise rates, the red-hot labor market could become overheated, potentially causing a recession. Yellen appeared to echo sentiments voiced by New York Fed President William Dudley, who made a strong case for raising rates on Monday. Dudley cited a soft US dollar and strong global growth as reasons why inflation would increase and also translate into stronger wage growth. Dudley said he expects inflation to reach the Fed's target of 2 percent in the "medium term", and predicted that the Fed would continue to gradually remove monetary accommodation. However, Chicago Fed President Charles Evans sent out a very different message, calling on the Fed to avoid another rate hike until wage and inflation levels moved higher. Evans said that inflation, which is running at around 1.4 percent, is too low, and wants to see "clear signs" that prices are moving higher before the Fed presses the rate trigger. For their part, the markets are more confident in a December move – the CME Group has pegged the odds of a December raise at 81%, while the odds were mired below 50% just a few weeks ago.

At last week's policy meeting, the Fed stayed on the sidelines and maintained the benchmark rate at 1.25%. There was dramatic news, however, as the Fed made its long-awaited announcement that it would reduce its $4.2 trillion balance sheet by $50 billion/mth, starting in October. Commenting on the decision to taper the balance sheet, FOMC member John Williams said last week that he did not "anticipate any sudden or large effects on rates or spreads", but acknowledged that the Fed could not predict how the markets would react, and policymakers would have to monitor market reaction to the reduction in the balance sheet. The reduction in the balance sheet can be viewed as a mini-rate hike, so if the Fed sticks to its plan of monthly tapers, the US dollar could gain ground against its major rivals.

UK Retail Sales Report Sparkles, but Pound Dips

The British pound continues to head lower this week, and has posted losses in the Wednesday session. In North American trade, GBP/USD is trading at 1.3407, down 0.38% on the day. On the release front, British CBI Realized Sales soared with a reading of 42, crushing the estimate of 6 points. In the US, data was mixed. Durable Good Orders sparkled with a 1.7% gain, well above the estimate of 1.0%. Core Durable Goods slowed to 0.2%, matching the estimate. Pending Home Sales was unexpectedly soft, posting a decline of 2.5%, compared to an estimate of -0.5%. On Thursday, BoE Governor Mark Carney will speak at a BoE conference in London. The US will release two key events – Final GDP and unemployment claims.

Federal Reserve policymakers remain divided on the hot issue of another rate hike in 2017. Fed Chair Janet Yellen waded into the rate debate on Tuesday, as she sent out a surprisingly hawkish message to the markets. Yellen said that she favored gradual rate increases, and voiced confidence that inflation levels would move higher. She added that if the Federal Reserve did not continue to raise rates, the red-hot labor market could become overheated, potentially causing a recession. On Monday, New York Fed President William Dudley also made a strong case to raise rates. Dudley cited a soft US dollar and strong global growth as reasons why inflation would increase and also translate into stronger wage growth. Dudley said he expects inflation to reach the Fed's target of 2 percent in the "medium term", and predicted that the Fed would continue to gradually remove monetary accommodation. However, Chicago Fed President Charles Evans sent out a very different message, calling on the Fed to avoid another rate hike until wage and inflation levels moved higher. Evans said that inflation, which is running at around 1.4%, is too low, and wants to see "clear signs" that prices are moving higher before the Fed presses the rate trigger. For their part, the markets are more confident in a December move – the CME Group has pegged the odds of a December raise at 81%, while the odds were mired below 50% just a few weeks ago.

The Brexit saga continues, as negotiations between Britain and the European Union have been testy and tense, with little headway on a range of issues that must be resolved as part of the divorce process. Given this background, it was no surprise that European Council President Donald Tusk acknowledged on Tuesday that the two sides had not made enough progress to move to trade discussions. The May government is eager to discuss trade relations with Europe in a post-Brexit era, but the EU has conditioned trade talks on "sufficient progress" being made regarding the amount of Britain's bill to leave the EU, the legal status of EU citizens living in the UK and the border between the UK and Ireland. The two sides remain far apart on these key issues, so it appears that the May government will have little choice but to move closer to the European position before it can talk trade. Adding to the uncertainty, the British government itself is divided on its Brexit policy. Hawkish cabinet members, such as foreign secretary Boris Johnston, have consistently put forward a harder line towards the Europeans than has Prime Minister May, and it's difficult to see how negotiations can move forward before the May gets her own house in order.

Dollar Rallies on Hopes of Tax Reforms; Eyes on RBNZ

Hawkish remarks by Fed Chair Yellen on Tuesday continued supporting the dollar against its major rivals during European trading as markets were more confident now that the Fed would deliver another rate hike in December. Investors were also cautious to hear whether the US tax overhaul plan announced later today would be Trump's first major legislative achievement since his election, a day after his proposals to repeal Obamacare failed to pass yet again.

The dollar index breached again the 93 key level during the European session, last trading at 93.23, as the odds for a third-rate hike to be delivered in December rose to more than 80% today compared to approximately 40% a month ago after the Fed Chair, Janet Yellen, said in Cleveland on Tuesday that rates should rise gradually despite the weakness in inflation.

Investors were also optimistic about the US tax reforms expected to be announced by Trump's administration and Republicans in Congress today at 1920GMT. After a multi-month process of preparing the tax outline, Republicans are said to propose for pass-through tax rates to drop to 25% from the current 39.6% and corporate tax rates to decrease from 35% to 20%. According to rumors though, details on how these tax cuts would be delivered without increasing the federal deficit would be limited.

Moreover, US durable goods orders for the month of August recovered after a sharp fall in the previous month, rising by 1.7% m/m, more than the forecast of 1.0%. The core equivalent measure came in as projected at 0.2%, below the 0.8% recorded in July (upwardly revised from 0.5%).

Regarding August's US pending home sales, those declined steeply by 2.6% m/m, posting the biggest fall since February. Expectations were for the figures to decline by 0.5% after a 0.8% fall in July. On Thursday, readings on final US growth rates for the second quarter will be also released.

Since North Korea did not proceed with any provocative actions after Trump's latest comments, demand for safe-haven assets eased further. Dollar/yen surged to a 2 ½-month high of 113.22, while dollar/swissie advanced to a near 4-month high of 0.9755. In other safe-haven assets, yields on US 2-year treasuries reached the highest level since October 2008 and gold dipped to a one-month low of $1,283.68 per ounce.

The euro bottomed to a near 6-week low of $1.1723 as political stability is put to question in Germany after Sunday's federal elections and as the dollar continued strengthening. In other news, the ECB's bank supervisor Danièle Nouy argued that Europe's banking sector may likely need to shrink as it has grown significantly.

The pound retreated to a two-week low of $1.3394, while the key event this week for the pound will be the BOE Governor Mark Carney's speech on Thursday.

In New Zealand, RBNZ policymakers are scheduled to gather later today to decide on interest rates, which are projected to remain steady at a record low of 1.75% until the end of the year. The kiwi was moving sideways during the session near a 3-week low of $0.7200 as political uncertainty is weighing on the currency, with the leader of the opposition party saying that coalition agreements will not be made until October 7.

The aussie extended its losses for the third day reaching a six-week low of $0.7835 on the back of a stronger dollar and decreasing metal prices.

In Canada, the BOC Governor Stephen Poloz will release a report on the country's economic conditions and hold a news conference at 1545GMT. Traders will be eager to hear whether the BOC is willing to continue tightening its monetary policy after two consecutive rate hikes. Dollar/loonie was up by 0.29% on the day at 1.2380.

In energy markets, oil prices hit lower despite the EIA report showing that US crude oil inventories declined by 1.846mn barrels the past week while analysts anticipated oil inventories to increase by 3.422m barrels. Gasoline inventories, though, rose by 1.107m barrels instead of falling by 0.921m as expected. Gasoline production was also up by 0.062m barrels. On the day, WTI crude traded 0.4% lower at $51.64 per barrel, while Brent was 1.1% down at $57.80.

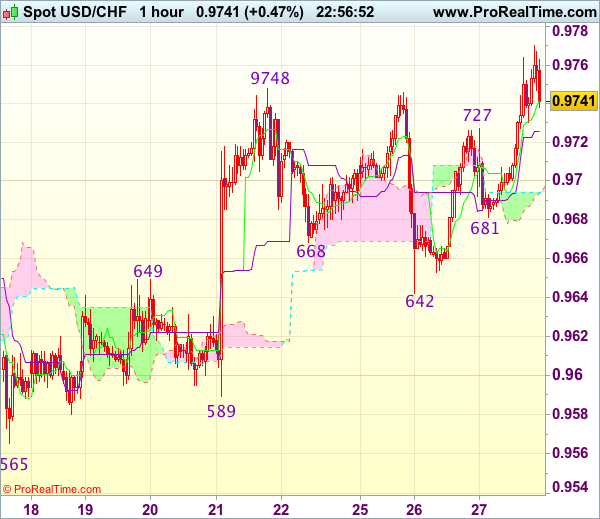

Trade Idea Wrap-up: USD/CHF – Hold long entered at 0.9685

USD/CHF - 0.9745

Most recent candlesticks pattern : N/A

Trend : Near term up

Tenkan-Sen level : 0.9749

Kijun-Sen level : 0.9726

Ichimoku cloud top : 0.9695

Ichimoku cloud bottom : 0.9694

Original strategy :

Bought at 0.9685, Target: 0.9785, Stop: 0.9710

Position : - Long at 0.9685

Target : - 0.9785

Stop : - 0.9710

New strategy :

Hold long entered at 0.9685, Target: 0.9785, Stop: 0.9710

Position : - Long at 0.9685

Target : - 0.9785

Stop : - 0.9710

As the greenback did find renewed buying interest at 0.9681 (we recommended to buy at 0.9685 and a long position was entered) and has rallied in line with our bullish expectation, retaining our upside bias for recent upmove from 0.9421 low to to extend gain to 0.9773 resistance, however, break of this level is needed to bring further rise towards 0.9800-10 which is likely to hold from here due to near term overbought condition.

In view of this, we are holding on to our long position entered at 0.9685. Only below said support at 0.9681 would abort and signal top is formed instead, bring correction of recent rise towards support at 0.9642 which is likely to hold on first testing.

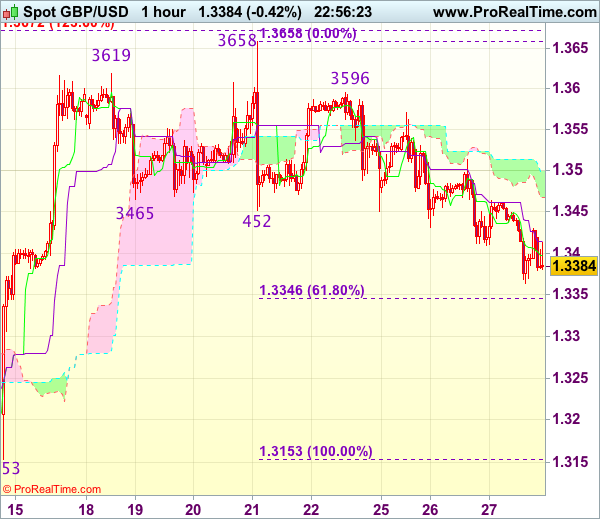

Trade Idea Wrap-up: GBP/USD – Sell at 1.3500

GBP/USD - 1.3404

Most recent candlesticks pattern : N/A

Trend : Up

Tenkan-Sen level : 1.3397

Kijun-Sen level : 1.3414

Ichimoku cloud top : 1.3500

Ichimoku cloud bottom : 1.3467

Original strategy :

Sell at 1.3500, Target: 1.3380, Stop: 1.3535

Position : -

Target : -

Stop : -

New strategy :

Sell at 1.3500, Target: 1.3380, Stop: 1.3535

Position : -

Target : -

Stop : -

As cable has rebounded after falling to 1.3364 earlier today, suggesting minor consolidation above this level would be seen and corrective bounce to 1.3455-60 cannot be ruled out, however, reckon upside would be limited to 1.3500 and bring another decline later, below said support at 1.3364 would extend recent decline from 1.3658 top to 1.3345-50 (61.8% Fibonacci retracement of 1.3153-1.3658) and possibly towards previous resistance at 1.3329.

In view of this, would not chase this fall here and would be prudent to sell cable on further recovery as 1.3500 should hold. Above resistance at 1.3514 would defer and risk a stronger rebound to 1.3535-40 but resistance at 1.3571 should remain intact.

Core Capital Goods Orders Pick Up the Pace in August

August durable goods orders rose 1.7 percent, in part due to another strong month for aircraft. Core orders, however, rose 0.9 percent and suggest solid equipment spending in the second half of the year.

Ear Protection Area: Aircraft Still Noisy

Durable goods orders suggest that the manufacturing sector continues to gain momentum. New orders rose 1.7 percent in August, beating market expectations for a 1.0 percent gain. The increase follows two particularly choppy months where aircraft orders led to more than a six percent jump in June that was immediately unwound in July. The noise was dialed down somewhat in August, but 33 new orders from Boeing led to a 44 percent rise in the value to aircraft orders over the month.

Outside of aircraft, gains were more modest. Orders for vehicles and parts snapped a two month string of declines and rose 1.5 percent. We are just now coming out of the summer shutdown season, in which the timing and length of stoppages have become more varied in recent years. Therefore, we are cautious to read too much into the August gain, particularly as auto sales have struggled over the past year. Orders for new vehicles and parts have largely moved sideways over the past year and are up only 0.9 percent from last August.

Positive Momentum Heading into the End of the Year

Excluding transportation, orders rose 0.2 percent. That was in line with expectations, but the increase came on the heels of an upward revision to July. The real strength in today's report, however, lies in new orders for nondefense capital goods ex-aircraft. This measure of "core" orders rose 0.9 percent (also on the heels of a modest upward revision to July). Some of that strength can be traced to machinery and primary metals, but orders for communications equipment rose an impressive 4.0 percent last month.

Core orders are now running at an average annualized pace of 6.4 percent over the past three months, similar to the pace registered early in the year. Momentum looks to have carried forward in September. The regional purchasing managers' indices released thus far this month have all improved, with new orders expanding at a faster clip according to the New York, Philadelphia, Richmond and Dallas Fed manufacturing surveys.

Shipments Point to Another Good Quarter for Equipment

Shipments of durable goods edged up 0.3 percent in August despite a pullback in the aircraft industry. While aircraft is excluded from our preferred measure of core orders due to the long lead time, shipments for the industry are still useful in gauging the strength of current outlays for equipment in the GDP report. Non-defense capital goods shipments are up at a 9.2 percent annualized pace thus far in the third quarter. That sits well with our call for another solid quarter of equipment spending. We currently have penciled in a 6.9 percent rise in equipment spending for the current quarter, while the strength of core orders is pointing to a similarly strong rise in the fourth quarter.

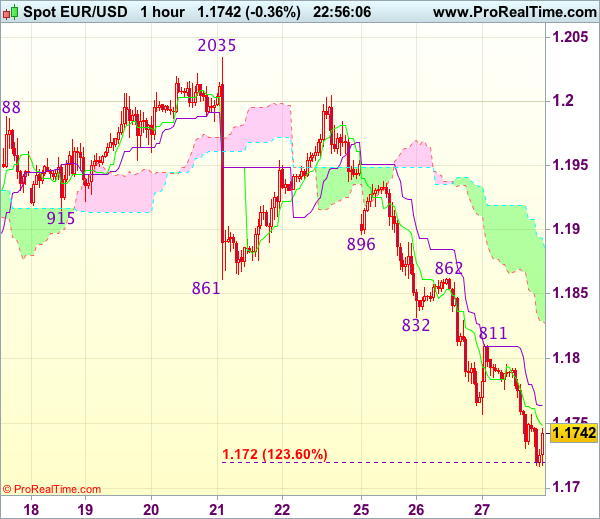

Trade Idea Wrap-up: EUR/USD – Sell at 1.1810

EUR/USD - 1.1739

Most recent candlesticks pattern : N/A

Trend : Down

Tenkan-Sen level : 1.1739

Kijun-Sen level : 1.1764

Ichimoku cloud top : 1.1882

Ichimoku cloud bottom : 1.1827

Original strategy :

Sell at 1.1830, Target: 1.1720, Stop: 1.1865

Position : -

Target : -

Stop : -

New strategy :

Sell at 1.1830, Target: 1.1720, Stop: 1.1865

Position : -

Target : -

Stop : -

As the single currency has fallen again after brief recovery to 1.1811, adding credence to our bearish view that the decline from .2093 top is still in progress and downside bias remains for further weakness to 1.1720 (1.236 times projection of 1.2093-1.1838 measuring from 1.2035), then 1.1700, however, loss of downward momentum should prevent sharp fall below previous support at 1.1662 and bring rebound later.

In view of this, we are looking to sell euro on recovery, above the Kijun-Sen (now at 1.1764) would bring recovery to said resistance at 1.1811, however, previous support at 1.1832-38 (now resistance) should hold and bring another decline later. Above resistance at 1.1862 would abort and signal low is formed instead, bring a stronger rebound to 1.1896 (another previous support).

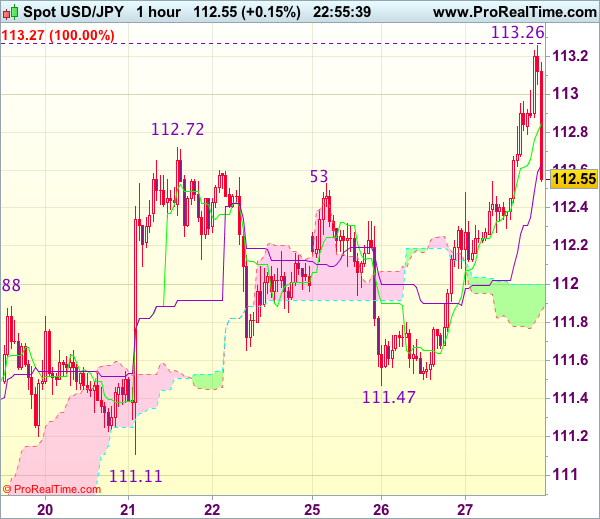

Trade Idea Wrap-up: USD/JPY – Exit long entered at 112.65

USD/JPY - 112.65

Most recent candlesticks pattern : N/A

Trend : Up

Tenkan-Sen level : 112.85

Kijun-Sen level : 112.63

Ichimoku cloud top : 112.00

Ichimoku cloud bottom : 111.86

Original strategy :

Bought at 112.65, Target: 113.65, Stop: 112.30

Position : - Long at 112.65

Target : - 113.65

Stop : - 112.30

New strategy :

Exit long entered at 112.65,

Position : - Long at 112.65

Target : -

Stop : -

Although the greenback rose to as high as 113.26, the subsequent sharp retreat suggests consolidation below this level would be seen, risk of further weakness to 112.20-35 cannot be ruled out, however, reckon the upper Kumo (now at 112.00) would limit downside and bring rebound later. Only below 111.75-80 would confirm top has been formed at 113.26, bring correction to 111.60 but support at 111.47 should remain intact.

In view of this, would be prudent to exit long entered at 112.65 and stand aside for now. Above 113.00 would bring retest of 113.26 but only break there would signal recent upmove has once again resumed and extend headway to previous resistance at 113.58.

Dollar Accelerates after Yellen Comments and Durable Goods

Yesterday the US dollar traded higher against the euro as the German election results continued to shake trader sentiment. A weaker than expected performance of Angela Merkel's conservative party suggests that Europe could face political turbulence in the future. Over the last two days the euro fell 1.4% against the US dollar.

On Tuesday, economic data showed the impact of hurricanes Irma and Harvey. According to the US state commerce department, new house sales declined 3.4% in August, which is the lowest level since December 2016. Consumer confidence also slipped to 119.8 in September as compared to 120.4 in August.

Recent data released today showed that the demand for US factory goods rebounded in August which is pointing to a continued increase in business investment. Orders of durable goods increased 1.7% in August versus the 1.0% expected and as compared to -6.8% in the previous month. Core durable goods orders rose 0.2% as expected.

Demand for the US dollar also increased and strengthened after comments from Janet Yellen. The Chair of the Federal Reserve said in her recent speech that the central bank has to increase the interest rate gradually as it would be unwise to put the monetary policy on hold until inflation is back to 2.0%. She also said that there would be the risk that the labor market could be overheated without further increases in the interest rate over time, which is expected to create inflationary problems that might be difficult to overcome without triggering a recession.

Many investors are looking for any update on a US tax plan that could revamp the stock market. Republicans are expected to release a blue print for tax reform later today that is expected to include a wide range of tax cuts for individuals and businesses, according to speculations. Any signals regarding the tax cut could accelerates the increase in small cap company's share prices, which tend to gain more benefit from tax reductions and generate more revenue domestically.

EURUSD

EURUSD is under pressure as it has been capped by a bearish trend line since September 22. Yesterday's high at 1.18609 is playing a resistance role. The relative strength index lacks upward momentum. As long as 1.18609 (yesterday's high) is resistance, look for a new decline towards 1.16616 (last month's low) and 1.1620. Alternatively, above 1.18609 look for 1.19360 (this week's high) and 1.20306 (last week's high).

USDJPY

USDJPY is expected to continue to trade its upside movement. The dollar is supported by the recent increase in durable goods order and yesterday's comments from Ms. Yellen. Technically the pair is trading above the 50 day moving average and 20 day moving average, which confirms the bullish outlook. the relative strength index is also above its neutrality area at 50 and lacks downward momentum. As long as the pair is trading above 112.16 (today's low) look for further advancement to 112.50 and 112.80. Alternatively, below 112.16 look for 111.50 (yesterday's low) and 111.00.

EURGBP

EURGBP is capped by the declining trend line. The 50 day moving average is also in decline, which suggests a break below today's high is highly possible. As long as the pair is trading below 0.8800 (yesterday's high) bearish acceleration towards 0.8730 and 0.8675 is likely. Alternatively, above 0.8800 (yesterday's high) look for 0. 8830 and 0.8898 (last week's high).

Yen Drops to 10-Week Low as US Durable Goods Shine

USD/JPY has posted gains on Wednesday, continuing the upward movement we saw on Tuesday. In North American trade, the pair is trading at 112.81, up 0.54% on the day. On the release front, BoJ Governor Haruhiko Kuroda will speak at a conference in Tokyo. In the US, Durable Good Orders sparkled with a 1.7% gain, well above the estimate of 1.0%. Core Durable Goods slowed to 0.2%, matching the estimate. Pending Home Sales was unexpectedly soft, posting a decline of 2.5%, compared to an estimate of -0.5%. On Thursday, the US will publish Final GDP and unemployment claims.

The BoJ is stubbornly sticking with its ultra-accommodative policy, and this was reiterated in the minutes of the Bank's August policy meeting. Most policymakers remained in favor of continuing present policy, and expressed optimism that inflation levels would move higher. Is there a real basis to this positive sentiment. Inflation remains well short of the BoJ target of just below 2 percent, and in its most recent forecast, the BoJ said that this target would not be met until 2020. Still, the BoJ has so far rejected calls to lower its inflation target, so it's unlikely that the Bank will taper its radical stimulus program anytime soon.

For some time, the markets have been looking for guidance from Fed Chair Janet Yellen regarding interest rate policy. Yellen did not disappoint, as she sent out a surprisingly hawkish message on Tuesday, strengthening the US dollar. Yellen said that she favored gradual rate increases, and voiced confidence that inflation levels would move higher. She added that if the Federal Reserve did not continue to raise rates, the red-hot labor market could become overheated, potentially causing a recession. At the same time, her Fed colleagues remain split on a December rate hike. On Monday, New York Fed President William Dudley made a strong case to raise rates. Dudley cited a soft US dollar and strong global growth as reasons why inflation would increase and also translate into stronger wage growth. Dudley said he expects inflation to reach the Fed's target of 2 percent in the "medium term", and predicted that the Fed would continue to gradually remove monetary accommodation. However, Chicago Fed President Charles Evans sent out a very different message, calling on the Fed to avoid another rate hike until wage and inflation levels moved higher. Evans said that inflation, which is running at around 1.4%, is too low, and wants to see "clear signs" that prices are moving higher before the Fed presses the rate trigger. For their part, the markets are more confident in a December move – the CME Group has pegged the odds of a December raise at 81%, while the odds were mired below 50% just a few weeks ago.