Sample Category Title

Elliott Wave Analysis: Nikkei 225 And GBPJPY Correlation

Stock markets in Asia were lower after North Korea accuses Trump of declaring war. We have seen Nikkei turning lower, but mostly likely only into wave C of 4) which may send price to the upside soon, into wave 5) towards 20600. At the same time we can expect higher xxx/jpy pairs because of tight positive correlation.

Nikkei 225, 1H

We are looking at GBPJPY which is also in a wave c of 4 but it may retest 149.70 low before turning up. However rise above 151.85 would suggest that wave 5 is already underway.

GBPJPY, 1H

Market Update – European Session: European Indices Reverse Early Losses Digesting Recent News Flow

Notes/Observations

European Indices trade slightly higher, reversing earlier losses in lackluster session despite tensions growing in the far east

Merkel looks to build coalition after German election

Nestle affirms 2020 growth targets at investor day

Overnight

Asia:

Geopolitical tensions continue to grow as North Korean Foreign Min said Pres Trump's comments over the weekend amount to declaration of war, noting North Korea has the right to shoot down US bombers even if they're not in North Korean airspace.

South Korea FSC announced financial reforms for retail customers, including changes to interest rates on overdue loan payments.

The yuan declined to the lowest level against its currency basket in nearly 4-weeks as the PBOC weakens the daily fix

Europe:

Merkel looks to build coalition being open to talks with all of Germany's mainstream parliamentary parties

Americas

(US) Fed's Kashkari (dove, voter): Do not see signs of economy overheating; do not see inflation taking off no need to tap breaks; Fed should not be under any pressure to raise rates

(US) Fed's Dudley (dove, FOMC voter): Reiterates expect further gradual tightening of US monetary policy; economy has grown steadily.

Economic data

(FR) FRANCE SEPT BUSINESS CONFIDENCE: 109 V 110E; MANUFACTURING CONFIDENCE: 110 V 111E

(DE) GERMANY AUG IMPORT PRICE INDEX M/M: 0.0% V 0.1%E; Y/Y: 2.1% V 2.1%E

(UK) AUG BBA LOANS FOR HOUSE PURCHASES: 41.8K V 41.7KE

(SE) Sweden Aug PPI M/M: -0.8% v +0.6% prior; Y/Y: 3.8% v 5.7% prior

Fixed Income Issuance:

(IT) Italy Debt Agency (Tesoror) sells total €1.5B v €1.0-1.5B indicated range in I/L 2022 and 2032 Bonds (BTPei)

(IT)ITALY DEBT AGENCY (TESORO) SELLS €1.5B VS. €1.0-1.5B INDICATED RANGE IN ZERO COUPON MAY 2019 CTZ BONDS; AVG YIELD: -0.22% V -0.139% PRIOR; BID-TO-COVER: 2.0X V 1.68X PRIOR

SPEAKERS/FIXED INCOME/FX/COMMODITIES/ERRATUM

Equities

Indices [Stoxx50 +0.1% at 3,543, FTSE +0.2% at 7,290, DAX +0.2% at 12,624, CAC-40 +0.1% at 5,273, IBEX-35 flat at 10,213, FTSE MIB +0.4% at 22,474, SMI +0.1% at 9,150, S&P 500 Futures -1.0%]

Market Focal Points/Key Themes: European stocks opened slightly lower, but drifted higher as the session progressed; geopolitical risks continue to weigh on sentiment, though haven flows were reduced; energy stocks supported by a bump in oil prices over Kurdistan referendum; attention moving to Fed Chair Yellen's speech after market close; upcoming earnings releases in the US session include Carnival and Darden

Equities

Consumer discretionary: Card Factory CARD.UK -0.7% (results), Deutsche Wohnen DWN.DE +3.1% (bond issue), Nestle NESN.CH +1.0% (investor day comments), Salvatore Ferragamo SFER.IT +2.2%(analyst action)

Financials: AA AA.UK -9.5% (results)

Industrials: Aurubis NDA.DE -4.6% (Analyst action), Duro Felguera MDF.ES -6.6% (under investigation), Fincantieri FCT.IT +0.9% (STX deal), Kone KNEBV.FI +0.1% (launches strategy), Norske Skogindustrier NSG.NO +31.7% (recapitalization plan), ThyssenKrupp TKA.DE +0.6(capital raise)

Healthcare: Pharming PHARM.NL +7.1% (partnership)

Technology: Infineon IFX.DE -0.1% (analyst action)

Telecom: Kinepolis KIN.BE +3.8% (analyst action)

Utilities: United Utilities UU.UK -0.7% (trading update)

Speakers

(IT) Italy Fin Min Padoan: It is a critical time for Europe at the moment; Sees much better outlook for Italian Economy- TV interview

Currencies

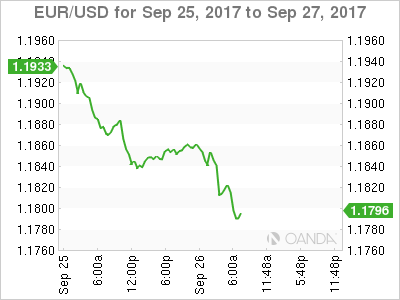

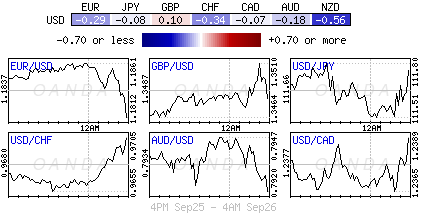

EUR/USD continues its downtrend on continued concerns over following the German Elections, Support lies at 1.1810 area.

Fixed Income

Bund futures trade at 161.79 down 16 ticks following the as expectations grow for a stronger safe-haven role following the German elections. Continued downside targets 161.03 while upside resistance stands initially at 162.07, followed by 163.27.

Gilt futures trade at 124.03 down 19 ticks as markets price a 78 percent chance of a Bank of England rate rise in November. Continued downside eyeing 123.26. Upside targets 124.90 then 125.24.

Tuesday’s liquidity report showed Monday’s excess liquidity fell to €1.723T from €1.743T and use of the marginal lending facility dropped to €114M from €122M.

Corporate issuance saw $6.1B come to market via 6 issuers headlined by DNB Bank $1.75B 2-part offering and Nissan $2.0B 4-part senior unsecured note offering

Looking Ahead

05.30 (UK) Weekly John Lewis LFL sales data

05:30 (ZA) South Africa Q2 Non-Farm Payrolls Q/Q: No est v-0.5% prior; Y/Y: No est v -0.6% prior

07:00 (BR) Brazil Sept FGV Construction Costs M/M: 0.3%e v 0.4% prior

07:45 (US) Weekly Goldman Economist Chain Store Sales

08:05 (UK) Baltic Dry Bulk Index

08:55 (US) Weekly Redbook Sales

09:00 (US) July S&P / Case-Shiller 20-City M/M: 0.20%e v 0.11% prior; Y/Y: 5.70%e v 5.65% prior; House Price Index (HPI): No est v 200.54 prior

09:00 (US) July S&P / Case-Shiller Case-Shiller (overall) HPI Y/Y: No est v 5.77% prior, House Price Index (HPI): No est v 192.6 prior

09:00 (EU) Weekly ECB Forex Reserves: € v € prior

09:00 (MX) Mexico Aug Unemployment Rate (seasonally adj): 3.2%e v 3.2% prior

09:30 (BR) Brazil Aug Current Account: No est v -$3.4B prior; Foreign Direct Investment (FDI): No est v $4.1B prior

10:00 (US) Consumer Confidence: 120.0e v 122.9 prior

10:00 (US) Aug New Home Sales: 588Ke v 571K prior

10:00 (US) Sept Richmond Fed Manufacturing Index: 13e v 14 prior

Daily Technical Analysis: NZD/USD Bearish Slope Marks The Downtrend

The NZD/USD, popular 'Kiwi' is in a zig-zag downtrend aiming for D L5/ W L5 camarilla levels. The POC zone 0.7285-0,7305 (D H4, 61.8, bearish order block, channel top) could reject the price should it retrace within the zone. Targets are 0.7187 and 0.7147. Also, watch for 38.2 X cross - 0.7255 that could also reject the price towards D L5 and W L5.

W L3 - Weekly Camarilla Pivot (Weekly Interim Support)

W H3 - Weekly Camarilla Pivot (Weekly Interim Resistance)

W H4 - Weekly Camarilla Pivot (Strong Weekly Resistance)

D H4 - Daily Camarilla Pivot (Very Strong Daily Resistance)

D L3 – Daily Camarilla Pivot (Daily Support)

D L4 – Daily H4 Camarilla (Very Strong Daily Support)

POC - Point Of Confluence (The zone where we expect price to react aka entry zone)

EURUSD – Continues To Push Lower On Bearishness

EURUSD - With the pair weakening on Monday and following through lower during Tuesday trading session, further bearishness is expected in the days ahead. Resistance comes in at 1.1850 level with a cut through here opening the door for more upside towards the 1.1900 level. Further up, resistance lies at the 1.1950 level where a break will expose the 1.2000 level. Conversely, support lies at the 1.1750 level where a violation will aim at the 1.1700 level. A break of here will aim at the 1.1650 level. Below here will open the door for more weakness towards the 1.1600. All in all, EURUSD faces further corrective weakness threats

Markets Seek Fed’s Guidance

Tuesday September 26: Five things the markets are talking about

Ahead of the U.S open, markets are stabilizing as investors digest a host of catalysts from N. Korean war threats and central-bank policy to tailwinds for oil and the aftermath of the German election.

For Tuesday, investors are waiting for fresh signals about U.S monetary policy outlook. Yesterday saw two opposing views from Fed members on inflation.

New York's Dudley expressed confidence that fading one-off effects and a weaker dollar would help inflation trend back to +2%, and deserves the gradual withdrawal of monetary stimulus.

In the opposing camp was Chicago Fed President Evans expressing concerns that the shortfall in price pressures may be more “structural rather than temporary.'

The debate continues on today, with Fed Governor Brainard (10:30 am EDT) and Chair Janet Yellen (12:45 EDT) set to give speeches while Cleveland Fed President Loretta Mester moderates a panel.

1. Global stocks trade with little direction

In Japan overnight, the Nikkei average edged lower as tech shares declined, tracking their U.S counterparts yesterday, while worries over N. Korea weakened risk appetite. The Nikkei ended -0.3% lower, while the broader Topix traded unchanged.

Down-under, Australia's S&P/ASX 200 Index lost -0.2%, while South Korea's Kospi index fell -0.3%.

In Hong Kong, the Hang Seng Index added +0.1% after slumping -1.4% Monday as Chinese property developers tumbled on fresh mainland home curbs.

In China, stocks inch up after three days of losses. The blue-chip CSI300 index rose +0.1%, while the Shanghai Composite Index added +0.1%.

Note: Do not expect Chinese authorities to tolerate any violent moves ahead of the key Communist Party Congress next month. Maintaining market stability is of “extreme importance,' and is a political task.

In Europe, regional indices trade slightly higher, reversing earlier losses in a lackluster session despite tensions growing in the Far East. Energy stocks are being supported by a bump in oil prices over Kurdistan referendum (see below). Attention now moves to Fed Chair Yellen's speech.

U.S stocks are set to open in the ‘red' (-1%).

Indices: Stoxx50 +0.1% at 3,543, FTSE +0.2% at 7,290, DAX +0.2% at 12,624, CAC-40 +0.1% at 5,273, IBEX-35 flat at 10,213, FTSE MIB +0.4% at 22,474, SMI +0.1% at 9,150, S&P 500 Futures -1.0%

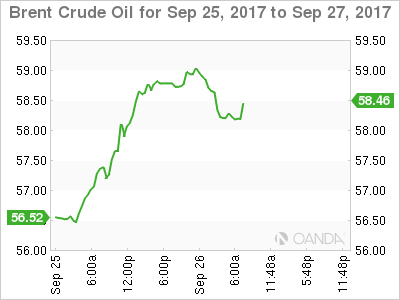

2. Oil at two-year high on Turkey threat, gold stable

Brent oil prices hover near their two-year high, supported by Turkey's threat to cut crude exports from Iraq's Kurdistan region as well as signs that market rebalancing is accelerating.

President Erdogan has threatened to cut off the pipeline that carries +600k barrels of crude per day from northern Iraq to the Turkish port of Ceyhan, intensifying pressure on the Kurdish autonomous region over its independence referendum.

The loss of this supply, combined with the -1.8m bpd of supply cuts by OPEC is raising concerns of tighter supply.

Brent crude futures have slipped -17c to +$58.85 a barrel (+34% higher from this years lows), while U.S crude WTI futures have eased -10c to +$52.12 a barrel, after hitting a five-month high of +$52.43 a barrel.

Note: The crude ‘bears' remain sceptical about further price gains due to higher oil output from the U.S. The EIA said that production from wells in shale formations would rise for a 10th month in a row in October.

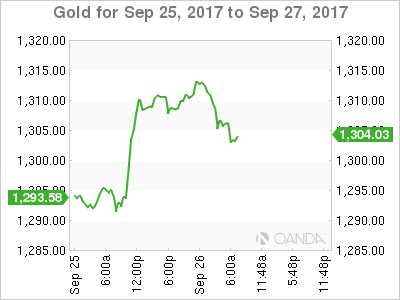

Gold is trading steady after hitting its one-week highs Monday, supported by safe-haven demand amidst lingering tensions over the Korean peninsula. Spot gold is unchanged at +$1,310.01 per ounce. It gained +1.3% in yesterdays session.

3. Euro yields steady after biggest drop in seven-weeks

Europe's benchmark bond yield are trading steady ahead of the U.S open as the market waits for Fed speeches that may provide some clues to tighten U.S monetary conditions.

The yield on Germany's 10-year Bund fell -6 bps to +0.41% yesterday after an unexpectedly weak election result for Chancellor Merkel's CDU party and N. Korea accused the U.S of having declared war.

Note: Many believe that the U.S fixed income market is behind the Treasury curve and are underpricing ‘hawkish' signals from Fed officials. The curve should be flatter if the Fed was in a tightening cycle.

According to CME's FedWatch tool, money markets point to a +70% chance of a hike in December, but only a +20% chance of a further hike in March 2018. The yields on 10-year Treasuries have advanced less than +1 bps to +2.22%.

In the U.K, the 10-year Gilt yield has climbed +1 bps to +1.346%.

4. EUR under geopolitical pressure

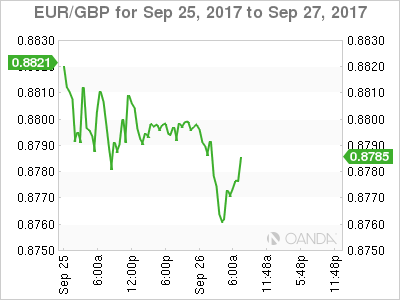

Ahead of the U.S open, the EUR has fallen to a fresh one-month low of €1.1797 outright and to a 10-week low of €0.8758 against the pound, continuing yesterday's losses after German elections reignited concerns about European political uncertainty.

A percentage of the market is concerned that Angela Merkel's CDU party will have to form a potentially tricky three-way coalition with the liberal FDP and the Greens, as well as the degree of support for the far-right AfD.

Note: With the populist AFD party winning the third largest number of votes, fears that nationalism has returned to Europe are forcing some investors to stop seeing the EUR as a “political haven'.

EUR ‘bears' are targeting €1.1625 as strong support, as they see little reason in terms of economic fundamentals for it to move much lower.

5. Bank of Japan (BoJ) monetary policy minutes

The July minutes showed that BoJ policymakers should stick with their current policy framework and had reason to be optimistic about consumer prices because measures of inflation expectations have stopped falling.

Note: The BoJ held rates steady, but pushed back the timing of its inflation target for the sixth-time since QE began.

A few members argued Japan's jobless rate and output gap needed to improve to reach the BoJ's +2% inflation target. The central bank expects to reach the target inflation sometime in the fiscal year ending in March 2020.

Note: As expected late yesterday, Japan's PM Abe called for a snap election. According to Moody's credit rating agency, the Japanese elections are unlikely to have implications for sovereign rating. “A refreshed mandate for reform would be considered a credit positive.'

Fed Speakers Eyed As Safe Havens Pare Gains

- EUR remains under pressure after German election;

- Safe havens pare gains as US labels declaration of war “absurd”;

- Fed officials provide distraction from political and geopolitical headlines.

It's been a steady start to trading on Tuesday, with political uncertainty and geopolitical risk once again weighing on risk appetite.

Coalition talks in Germany and New Zealand following elections over the weekend will likely lead to some uncertainty in the near-term which is weighing on the kiwi but having less of a negative impact on German-related assets. Bund yields fell slightly in the immediate aftermath of the election while the euro has fallen back towards 1.18 against the dollar but it's important to note that both had made significant gains prior to this and the latter in particular was looking a little overstretched.

Rather than being a source of negativity for the euro, I think traders are seeing the election as an opportunity to lock in some profits which is triggering a small but arguably necessary correction. With 1.18 now coming under pressure, I think further downside could be on the cards in the near-term, with 1.1660 being the next test to the downside potentially more to come. A correction would provide the EBC the opportunity to announce tapering next month with the currency trading at more comfortable levels.

We saw some safe haven flows on Monday after it was claimed that US President Donald Trump had declared war on North Korea with his comments over the weekend. Foreign Minister Ri Yong-ho made this statement in New York which immediately triggered moves towards traditional safe havens such as Gold, although these moves have already been partially reversed today. The US immediately rejected these claims and branded them absurd which has possibly helped alleviate any concerns although it's clear that the rhetoric between the two countries is intensifying.

This underlying risk will remain in the markets, leaving them vulnerable to these bouts of sudden safe haven flows, until we start to see signs of a diplomatic solution being found. Something that doesn't look like it's coming any time soon with the leaders of both countries clearly more intent on appearing dominant than finding a solution.

Politics and geopolitics aside, we will get some economic data from the US today and also hear from a number of Federal Reserve officials. Chair Janet Yellen is clearly the most notable of the Fed speakers today but we'll also hear from Charles Evans, Loretta Mester, Lael Brainard and Raphael Bostic which should make it an interesting day for the dollar and US yields, particularly as the central bank stood by expectations of one more rate hike at its meeting this month. CB consumer confidence and new home sales data will also accompany these appearances.

CRUDE OIL Buying Demand

.

Crude oil is edging higher above the $50 level. Key support is given at 45.40 (17/08/2017 high). Strong resistance found at 50.43 (31/07/2017) has been broken. Expected to show another leg higher.

In the long-term, crude oil has recovered after its sharp decline last year. However, we consider that further weakness are very likely. Strong support lies at 35.24 (05/04/2016) while resistance can now be found at 55.24 (03/01/2017 high).

SILVER Consolidation

Silver has reversed and has broken uptrend channel by breaking support implied by its lower bound. Strong resistance is given at 18.65 (17/04/2017 high) while support can be found at 16.58 (15/08/2017 high). Expected to show further bearish move.

In the long-term, the trend is rater negative. Further downsides are very likely. Resistance is located at 25.11 (28/08/2013 high). Strong support can be found at 11.75 (20/04/2009).

GOLD Bullish Breakout

Gold has pushed above 1300. Hourly support is now given at 1288 (21/08/2017 low). Hourly resistance is located at 1357 (08/09/2016). Stronger support lies at 1204 (10/07/2017 high). Expected to show further bearish move.

In the long-term, the technical structure suggests that there is a growing upside momentum. A break of 1392 (17/03/2014) is necessary ton confirm it, A major support can be found at 1045 (05/02/2010 low).

BITCOIN Ready For Further Decline

Bitcoin has taken a dive after strong interest over the summer. The digital currency has set up a new support at 2975 (22/08/2017 low). Hourly resistance is given at 4121 (18/09/2017 low). Key resistance can be located at 4921 (01/09/2017 high). The road is wide open for further shortterm decline.

In the long-term, the digital currency has had an exponential growth. There are decent likelihood that the asset will reach $10'000.