Sample Category Title

Market Update – European Session: BOE Dove Vlieghe Ruffles Hawkish Feathers

Notes/Observations

Risk aversion sentiment fails to hold following another North Korea missile as ongoing tensionon Korean Peninsula would not lead to any actual military action

BOE dove Vlieghe ruffles hawkish feathers to move in-line with recent BOE statement

Small explosion reported on London Underground Train; being treated as terror event

Overnight

Asia:

North Korea fires a missile from Pyongyang towards the east, missile passes over Japan

Japan PM Abe: North Korea launch is absolutely unacceptable; international community must send clear message to North Korea over provocative actions; requested emergency UN meeting; North Korea has to be shown there is no bright future for it if it continues down this path; UN sanctions need to be firmly and fully implemented

South Korea President Moon: Dialogue with North Korea is impossible at this point. Will not sit idle on North Korea provocation. South Korea has power to ‘pulverize’ should North Korea provoke

South Korea Military said to have conducted ‘firing drill’ in which it fired missile in a test into the sea, coinciding with North Korea's missile launch

US Sec of State Tillerson: China and Russia must indicate their intolerance for these reckless missile launches by taking direct actions of their own

Europe:

ECB's Weidmann (Germany): ECB should not miss the precise time to normalize policy. Reiterated General Council view that monetary policy to remain exceptionally easy after QE. ECB should ease up on the gas, but not brake hard

Germany Fin Min Schaeuble: ECB must prepare exit from policy very cautiously to prevent markets from overreacting. ECB extraordinary monetary policy with low interest rates and bond purchases (QE) was necessary to overcome economic crisis

Americas:

Bank of Canada Wilkins: Not ideal to give markets full plan on rates, every rate decision is 'live'. Only moving rates when everyone expects it would not lead to good policy outcomes.

UN Security Council to meet at 3 pm EDT on Friday, Sept 15thregarding the most recent North Korea missile test

Economic data

(NO) Norway Aug Trade Balance (NOK): 12.4B v 14.3B prior

(CN) China Aug New Yuan Loans (CNY): 1.09T v 950.0Be

(CN) China Aug Aggregate Financing (CNY): 1.48T v 1.280Te

(CN) China Aug M2 Money Supply Y/Y: 8.9% v 9.1%e; M1 Money Supply Y/Y: 14.0% v 14.8%e; M0 Money Supply Y/Y: 6.5% v 6.0%e

(IT) Italy July General Government Debt: €2.300T (record high) v €2.281T prior

(EU) Euro Zone July Trade Balance (Seasonally Adj): €18.6B v €20.3Be; Trade Balance NSA(unadj): €23.2B v 26.6B prior

(EU) Euro Zone Q2 Labour Costs Y/Y: 1.8% v 1.4% prior

Fixed Income Issuance:

(ZA) South Africa sold total ZAR800M vs. ZAR800M indicated in I/L 2029, 2038 and 2050 bonds

SPEAKERS/FIXED INCOME/FX/COMMODITIES/ERRATUM

Equities

Indices [Stoxx600 -0.1% at 381.6, FTSE -0.7% at 7247, DAX flat at 12536, CAC-40 flat at 5225, IBEX-35 -0.2% at 10341, FTSE MIB flat at 22274, SMI -0.4% at 9040, S&P 500 Futures -0.1%]

Market Focal Points/Key Themes:

European Indices trade mostly lower being led lower once again by the FTSE 100 which trades lower by over half a percent following on from the steep drop yesterday as hawkish commentary from BoE Dove Vlieghe which pushed Sterling up a further 80 pips.

On the corporate front AB Science and Santhera Pharma trade sharply lower following negative opinions from the CHMP, whilst H&M trades higher on a better Autumn outlook. Pub Chain JD Weatherspoons outperforms after Full year results and current trading.

Equities

Consumer discretionary [H&M [HMB] +2.4% (Prelim Q3), JD Weatherspoon [JDW.UK] +9.7% (Earnings), Sthree [STHR.UK] +1.4% (Earnings)]

Industrials: [DX Group [DX.UK] -12% (Cuts outlook due to incorrect accounting practice)]

Technology: [ DIGIA [DIGIA.FI] -7.2% (Cuts outlook)]

Healthcare: [UCB [UCB.BE] +1.3% (UCB's newest antiepileptic drug approved by FDA ), Santhera Pharmaceuticals [SANN.CH] -54% (Negative CHMP opinion), Bavarian Nordic -50% (Independent data monitoring committee recommends discontinuation of Bavarian Nordic's Phase 3 study of PROSTVAC in metastatic prostate cancer), AB Science -13% (CHMP has adopted negative opinion for masitinib marketing authorization in indolent systemic mastocytosis after reassessment)]

Speakers

BOE’s Vlieghe (dove): Might need to adjust BOE interest rate in the coming months (in-line with MPC majority). Time for a rate hike was approaching; slack being eroded, wage pressure gently growing. Still a risk that Brexit would have a biggest effect on economy

ECB’s Lautenschlaeger (Germany): Conditions are all in place for inflation to reach a stable trend towards our goal: below, but close to, 2% in the medium term. Accommodation still needed to help bring inflation back to stable trend towards target. Must help markets get idea on how QE exit will look like

IMF's Lipton: Risks that Ukraine could go backwards in terms of IMF program

North Korea Foreign Ministry official: Latest missile launch is a normal part of strengthening the nuclear deterrent

China govt official reiterated urge to find peaceful and political solution for Korean Peninsula. To continue to strictly implement UN resolution and opposes North Korean violations of UN resolution

Currencies

GBP/USD continued to build upon recent gains in the aftermath of the BOE rate decision and policy statement. BoE sent a very hawkish message with the majority of members agreeing that some withdrawal of monetary stimulus is likely to be appropriate over the coming months. The market probability for a November hike is now just over 50%. GBP/USDstrengthened to above 1.35 level as BOE dove Vlieghe turned hawkish

JPY currency (Yen) off session best level despite another missile launch from North Korea on Friday. Dealers note that current thinking of markets is the ongoing tension on Korean Peninsula would not lead to any actual military action

Fixed Income

Bund futures trade at 161.74 up 10 ticks, with technical levels remaining in focus. Continued downside targets 161.42 while upside resistance stands initially at 162.07, followed by 163.27.

Gilt futures trade at 125.59 down 37 ticks continuing to underperform following yesterday’s BOE rate decision, which prompted a sharp repricing of UK rate expectations after breaking below the 126.53 support level. Continued downside eyeing 124.91. Upside targets 127.90 then 128.24.

Friday’s liquidity report showed Thursday’s excess liquidity fell to €1.766T from €1.786T and use of the marginal lending facility rose to €115M from €107M.

Corporate issuance saw $7.9B come to market via 6 issuers headlined Bank of Nova Scotia $1.4B 2-part senior unsecure note offering and BP Capital Markets $3B 4-part senior unsecured note offering. For the week ending Sep 13th IG Funds reported high-yield outflows of $95.5M v inflows of $641M in the prior week.

Looking Ahead

(BE) Belgium Debt Agency (BDA) announces size of upcoming OLO auction

06:00 (IE) Ireland Q2 GDP Q/Q: +1.3%e v -2.6% prior; Y/Y: No est v 6.1% prior

06:00 (IE) Ireland Q2 Current Account Balance: No est v €8.6B prior

06:00 (UK) DMO to sell combined £4.5B in 1-month, 3-month and 6-month Bills on Fri, Sept 15th (£1.5B, £1.0B and £2.0B respectively)

06:30 (RU) Russia Central Bank (CBR) Interest Rate Decision: Expected to cut 1-Week Auction Rate by 50bps to 8.50%

06:45 (US) Daily Libor Fixing

07:00 (IL) Israel Aug CPI M/M: +0.3%e v -0.1% prior; Y/Y: -0.1%e v -0.7% prior

07:30 (IN) India Weekly Forex Reserves

08:00 (IS) Iceland Aug Unemployment Rate: No est v 3.4% prior

08:00 (DE) German Chancellor Merkel with France PM Philippe in Berlin

08:00 (ES) Spain Debt Agency (Tesoro) announces upcoming issuance

08:00 (IN) India announces upcoming Bill auction (held on Wed)

08:05 (UK) Baltic Dry Bulk Index

08:30 (US) Sept Empire Manufacturing: 18.0e v 25.2 prior

08:30 (US) Aug Advance Retail Sales M/M: 0.1%e v 0.6% prior; Retail Sales Ex Auto M/M: 0.5%e v 0.5% prior; Retail Sales Ex Auto and Gas: 0.3%e v 0.5% prior; Retail Sales Control Group: 0.2%e v 0.6% prior

09:00 (CA) Canada Aug Existing Home Sales M/M: No est v -2.1% prior

09:00 (BE) Belgium July Trade Balance: No est v €0.1M prior

09/15/2017 09/16 (RU) Russia Aug Industrial Production Y/Y: No est v 1.1% prior

09:15 (US) Aug Industrial Production M/M: 0.1%e v 0.2% prior; Capacity Utilization: 76.8%e v 76.7% prior; Manufacturing Production Y/Y: +0.4%e v -0.1% prior

10:00 (US) Sept Preliminary University of Michigan Confidence: 95.0e v 96.8 prior

10:00 (US) July Business Inventories: 0.2%e v 0.5% prior

11:00 (CO) Colombia July Industrial Production Y/Y: +4.1%e v -1.9% prior

11:00 (CO) Colombia July Retail Sales Y/Y: 2.8%e v 1.0% prior

11:00 (EU) Potential sovereign ratings

(AT) Austria Sovereign Debt to be rated by S&P

(CY) Cyprus Sovereign Debt to be rated by S&P

(DK) Denmark Sovereign Debt to be rated by S&P

(FI) Finland Sovereign Debt to be rated by S&P

(IE) Ireland Sovereign Debt to be rated by Moody's

(LX) Luxembourg Sovereign Debt to be rated by S&P

(NG) Nigeria Sovereign Debt to be rated by S&P

(PT) Portugal Sovereign Debt to be rated by S&P

(RU) Russia Sovereign Debt to be rated by S&P

13:00 (US) Weekly Baker Hughes Rig Count data

14:00 (CO) Colombia Central Bank Aug Minutes

(CO) Colombia Aug Consumer Confidence: -6.0e v -9.5 prior

(PE) Peru July Economic Activity (Monthly GDP) Y/Y: 2.7%e v 3.6% prior

(PE) Peru Aug Unemployment Rate: 6.9%e v 7.1% prior

Technical Outlook: EURGBP Surges Below Daily Cloud On Fresh Hawkish Comments From BoE

The pair extends steep descend into sixth straight day, with strong bearish acceleration on Thu/Fri, being boosted by hawkish comments from BoE yesterday and hawkish shift of former most dovish MPC member, who advocated for rate hike in coming months, in today’s comments.

Bears surged through rising daily cloud and generated additional bearish signal, as further extension below cloud dented weekly Kijun-sen support (0.8809) and hit fresh two-month low at 0.8793.

Higher low of 14 July at 0.8742 and weekly cloud top at 0.8699 (also Fibo 61.8% of larger 0.8312/0.9306 rally) are coming in focus.

The pair on track for very strong bearish weekly close (the biggest one-week loss since early Feb 2013), which will also mark the third consecutive weekly close in red and further weigh on pair’s short-term action.

Res: 0.8864, 0.8906, 0.8957, 0.9011

Sup: 0.8793, 0.8742, 0.8699, 0.8640

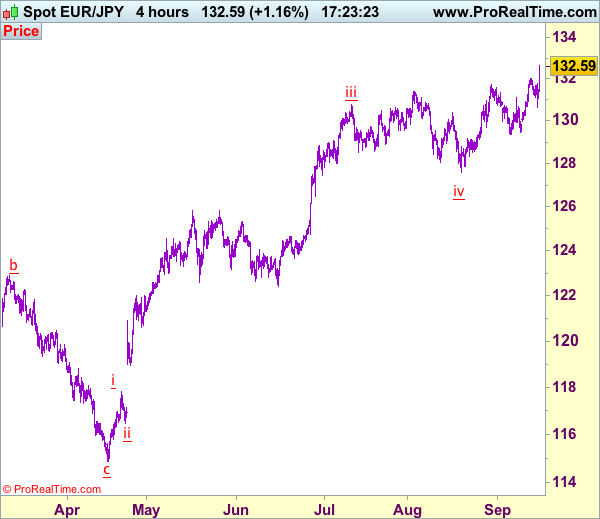

Trade Idea: EUR/JPY – Buy at 132.20

EUR/JPY - 132.79

Original strategy:

Exit long entered at 131.35,

Position: - Long at 131.35

Target: -

Stop: -

New strategy :

Buy at 132.20, Target: 134.20, Stop: 131.60

Position: -

Target: -

Stop:-

Although the single currency slipped to as low as 130.62, as renewed buying interest emerged there and euro has rallied above resistance t 132.01 today, reviving our bullishness and signal recent upmove is still in progress, hence further gain to 133.00-10, then 133.50-60 would be seen, however, near term overbought condition should prevent sharp move beyond 134.00-10 and reckon 134.50-60 would hold from here, risk from there has increased for a retreat later.

In view of this, we are looking to reinstate long on pullback as 132.20 should limit downside and previous resistance at 132.01 (should turn into support) and bring another rise later. Below 131.60-70 would defer and risk retreat to 131.00-10 but said support at 130.62 should remain intact, bring another rise later.

Our latest preferred count is that wave (ii) is ABC-X-ABC which ended at 123.33 and wave (iii) is unfolding with wave iii ended at 100.77, followed by wave iv at 111.57 and wave v as well as the wave (iii) has ended at 97.04, followed by wave (iv) at 111.43 and wave (v) has ended at 94.12 which is also the end of the larger degree v, this also implied the major wave (C) has also ended there, hence major correction has commenced from there with (A) leg unfolding in its lower degree wave c which has possibly ended at 145.69. Under this count, A-B-C wave (B) has commenced with A leg ended at 136.23, wave B at 143.79 and wave C has possibly ended at 149.79.

Our larger degree count is that the decline from 139.26 is wave (C) and is sub-divided into a diagonal triangle i-ii-iii-iv-v with wave i - 105.44, wave ii- 123.33, wave iii - 97.03, wave iv - 111.43, followed by the final wave v as well as the end of wave (C) at 94.12, this also mark the bottom of larger degree wave B. Under this count, major rise in wave C has commenced as an impulsive wave with minor wave III ended at 145.69, wave V is still in progress for further gain to 150.00. Having said that, this so-called wave V could well be the first leg of larger degree 5-waver wave C and this wave C should bring at least a retest of wave A top at 169.97 (July 2008).

Euro Steady Ahead Of U.S. Retail Sales

The euro has edged higher in the Friday session. Currently, the pair is trading at 1.1945, up 0.27% on the day. On the release front, the eurozone trade surplus, which narrowed to EUR 18.6 billion in July, well short of the estimate of EUR 20.1 billion. This marked the smallest trade surplus since February. In the US, it's a busy day, so we could see some movement from EUR/USD. Today's highlights are Retail Sales and Core Retail Sales. As well, the US will release the Empire State Manufacturing Index and UoM Consumer Sentiment.

The German economy continues to impress. Unemployment levels remain low, growth is steady, and the country even has a budget surplus. However, analysts are divided on the extent of the momentum. The German Economy Ministry is predicting that the economy could slow in the second half of 2017, and is holding to its forecast of 1.5% growth this year. The BDI Group is projecting an expansion of just above 2.0%, while the International Monetary Fund has pegged growth at 1.8% for 2017. Strong German growth in the second half would be good news for the streaking euro.

Germany will hold a federal election on September 24, and Angela Merkel is widely expected to win her fourth term as prime minister. French President Emmanuel Macron, a staunch supporter of a unified Europe, is hoping to work with Merkel and reform the eurozone. Macron's proposal includes a eurozone finance minister who would be in charge of a eurozone budget. Macron's call for greater cooperation is linked to Britain's exit from the EU, which could lead to divisions among the remaining 27 members in the bloc. However, the French ambitious plan will need Germany's support before it can become a reality. Will Germany embrace the idea? Angela Merkel's has indicated that she is open to the idea, but on Wednesday, Jean-Claude Juckner, head of the European Commission, dismissed the plan, saying he favored a finance minister for the EU but was against a separate eurozone budget and finance minister. Even if the plan is not adopted, we can expect a Macron-Merkel alliance to take steps which will strengthen Franco-German ties and further unify the eurozone.

Bitcoin Could Drop Below 3000 | European Markets & US Futures Noiseless | North Korea’s Action Reflective In Gold

The typical risk-off trade did come into play

It would be a mistake to undermine the geopolitical tensions

The sterling-dollar pair is in no mood in giving up its gains from yesterday

North Korea took no time to show its reaction to the new sanctions imposed on the country by the U.N. It was largely expected that North Korea would take that path. And here you are again, North Korea fired a missile which passed over northern Japan and fell in the sea. The typical risk-off trade did come into play but traders are getting more used to these sorts of provocations. Although, I would argue that these threats should not be taken light-heartedly. They can get out of hand much quicker than anyone can anticipate, and if appropriate risk measures are not in place, the situation would look immensely vile.

President Trump has demanded a direct action from China. The Japanese prime minister has made it clear that the "fire and fury" statement only isn't going to resolve the situation. Therefore, it would be a mistake in our opinion to undermine the geopolitical tensions. This situation is like an elastic band which is being stretched on both ends and if it continues like this, it would be only a matter of time before it breaks.

European markets and US futures are trading lower but noiseless during the early hours of trading. This quietness in the market could change rapidly if we have any serious action by Russia or China (which President Trump has requested). However, the chances of that taking place are minuscule.

For Sterling, the message was clear, tightening is coming and the market is underestimating this fact. But we have heard this song over and over again. However, something has changed and the market has started to price that in. The BOE seems serious this time and it is likely that it would tighten the belt. The sterling-dollar pair is in no mood in giving up its gains from yesterday, in fact, it is building on them and broke the 1.34 resistance today. Only a bad string of economic data could dial back the interest rate hike or some sort of other monetary policy action. The MPC member Vlieghe will be speaking later today and his comments could bring some swing for the currency and the possibility of a tailspin move cannot be ignored

Bitcoin is extending its losses after finding some peace. The cryptocurrency is suffering its longest streak of losses in a year thanks to the Chinese regulator's news. The gap from the 7th August is very much a target now and we do think it is highly likely, that the price fills up that gap first before any possible meaningful bounce. The next support is between 3000 and 2877.

Technical Outlook: Cable Surges Above 1.3500 On Hawkish Comments From Previously Most Dovish MPC Member

Sterling surged above target at 1.3473 and psychological 1.3500 barrier, hitting the highest levels since June 2016 after receiving fresh boost on hawkish comments from BoE MPC member Vlieghe.

Gertjan Vlieghe was previously seen as the most dovish member of the committee, but his today's comments were seen as hawkish steer.

He said that the BoE might need to raise interest rates in the coming months, echoing Thursday's comments from BoE. Vlieghe shifted his stance from further patience ahead of rate hike action to push for faster action of BoE in coming months.

British pound which already maintained strong bullish sentiment from yesterday's BoE's statement and extended rally to the levels last seen over two years ago.

Cable is on track for the second straight bullish weekly close, with close above weekly cloud to generate another strong bullish signal for extension towards next target at 1.3835 (29 Feb low/Fibo 61.8% of 1.5016/1.1930 descend).

Corrective actions on overbought studies could be anticipated in coming sessions.

Res: 1.3550, 1.3574, 1.3600, 1.3646

Sup: 1.3500, 1.3473, 1.3381, 1.3328

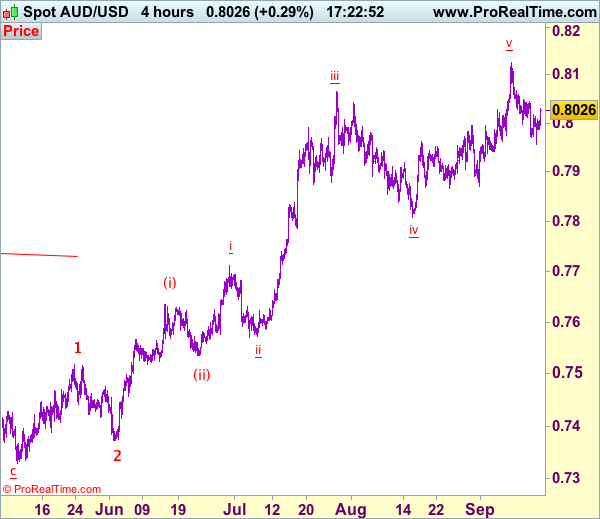

Trade Idea: AUD/USD – Sell at 0.8090

AUD/USD – 0.8024

Original strategy:

Sell at 0.8090, Target: 0.7900, Stop: 0.8150

Position: -

Target: -

Stop:-

New strategy :

Sell at 0.8090, Target: 0.7900, Stop: 0.8150

Position: -

Target: -

Stop:-

As aussie found support at 0.7956 yesterday and has rebounded, suggesting consolidation would be seen and corrective bounce to 0.8040-45 is likely, however, as top has been formed at 0.8125, upside should be limited to 0.8090 and bring retreat later, below said support at 0.7956 would add credence to this view, bring retracement of recent rise to 0.7920-25 and later 0.7890-00 but support at 0.7867-71 should remain intact.

In view of this, we are looking to sell aussie on recovery as 0.8090-00 should limit upside. Above said resistance at 0.8125 would (last week’s high) would extend recent upmove in wave v of (iii) to 0.8150, then towards 0.8200, however, loss of upward momentum should prevent sharp move beyond 0.8225-30 and price should falter below 0.8250-60, risk from there is seen for a retreat later.

On the 4-hour chart, the move from 0.8066 is the wave 5 with i: 0.8860, ii: 0.8315, wave iii is an extended move ended at 1.0183, iv: 0.9706 and wave v has ended at 1.1081 (also the top of entire wave 5). The subsequent selloff is the major correction which is unfolding as ABC-X-ABC and 2nd A leg has ended at 0.8848, followed by a-b-c wave B which ended at 0.9758, hence, 2nd C wave is now in progress and indicated downside target at 0.7000 and 0.6950 had been met, so further fall to 0.6710-20 cannot be ruled out.

Daily Technical Analysis: EURUSD, GBPUSD, USDJPY, USDCHF

EURUSD

The EURUSD attempted to push lower yesterday bottomed at 1.1837 but closed higher at 1.1918. The bias is bullish in nearest term testing 1.2000 region. Immediate support is seen around 1.1870. A clear break below that area could lead price to neutral zone in nearest term retesting 1.1823 key support area which remains a good place to buy with a tight stop loss as a clear break and daily/weekly close below that area could trigger further bearish correction testing 1.1700 – 1.1600 region next week. Overall I remain bullish and still prefer to buy on dips with nearest target seen at 1.2175 area.

GBPUSD

The GBPUSD had a strong bullish momentum yesterday topped at 1.3405 after bounced off 1.3150 support area and the EMA 200 as you can see on my H1 chart below . The bias is bullish in nearest term testing 1.3500 area. Immediate support is seen around 1.3330. A clear break below that area could lead price to neutral zone in nearest term testing 1.3265 region but overall I am bullish on this pair and any downside pullback should be seen as a good opportunity to buy.

USDJPY

The USDJPY attempted to push higher yesterday slipped above 111.00 key resistance but whipsawed to the downside and closed lower at 110.21 and hit 109.54 earlier today in Asian session. We have a bearish pin bar formation as you can see on my H4 chart below suggests a bearish view. The bias is bearish in nearest term testing 109.25/00 area. Immediate resistance is seen around 110.50. A clear break above that area could lead price to neutral zone in nearest term retesting 111.00 key resistance area. As long as stay below 111.00, my H4 chart bias remains bearish. Overall I remain neutral.

USDCHF

The USDCHF attempted to push higher yesterday slipped above 0.9700 resistance area but whipsawed to the downside and closed lower at 0.9628, formed a bearish pin bar formation as you can see on my daily chart below. The bias is bearish in nearest term testing 0.9585 area. Immediate resistance is seen around 0.9700. A clear break above that area could lead price to neutral zone in nearest term as direction would become unclear. On the downside, a clear break and daily/weekly close below 0.9585 would retest 0.9450 key support area next week.

Daily Technical Analysis: USD/JPY Possible Breakout Above 110.78

Equities have been holding strong this week and USD/JPY has seen a recovery from its lows making a diving board pattern/V shaped reversal. At this point it stands at the important levels 110.70 and if we see a momentum break of 110.78 it could proceed towards 111.22-30 zone. In the case of profit taking (It's Friday) pay attention to 110.10-20 zone (historical gap support, 38.2, channel bottom, EMA89) as the POC could again spike the price towards 110.78 and above.

W L3 - Weekly Camarilla Pivot (Weekly Interim Support)

W H3 - Weekly Camarilla Pivot (Weekly Interim Resistance)

W H4 - Weekly Camarilla Pivot (Strong Weekly Resistance)

D H4 - Daily Camarilla Pivot (Very Strong Daily Resistance)

D L3 – Daily Camarilla Pivot (Daily Support)

D L4 – Daily H4 Camarilla (Very Strong Daily Support)

POC - Point Of Confluence (The zone where we expect price to react aka entry zone)

USD Rally Stalls Ahead Of FOMC Meeting, CBR Expected To Cut Rates

USD recovery was short-lived ahead of next week FOMC meeting

The US dollar got a fresh boost yesterday after the release of better-than-expected inflation report. The headline CPI gained 1.9%y/y, against median forecast of 1.8%, up from 1.7% in July. The core gauge also beat expectations of 1.6% by rising 1.7%y/y. This upside surprise may have renewed expectations of an upcoming tightening move from the Fed. However, many clouds remain on the horizon.

First of all, real average weekly earnings grew only 0.9%y/y, down from 1.1% in the previous month, suggesting that the significant recovery of real wage growth that started at the beginning of the year may have come to an end, which is definitely not of good omen for the Fed normalization cycle.

Second, hurricanes Harvey and Irma have substantially blurred the Fed’s vision by distorting the economic data. Unfortunately, it will take months for the dust to settle down, which could prompt the Fed to act with caution. New York fed President Dudley mentioned this point as he argued that the hurricanes could affect temporarily the timing of the next rate hike.

The dollar recovery was short-lived as the greenback reversed gains against most of its peers. The single currency rose 0.13% to $1.1940. Commodity currencies were also better bid with the AUD, NZD and CAD rising 0.25%, 0.66% and 0.16%, respectively. We believe investors will remain cautious ahead of next Wednesday FOMC meeting as there is a growing sentiment that the Fed will play for time, once again.

Russia: Markets strongly expect a rate cut

The Central Bank of Russia will decide about its key rate today. There is a significant likelihood that the central bank lower its key rate to 8.5%. In July, the CBR decided to remain on hold, markets expectations for a rate cut are now strong.

There are a major reason for that, it has been a while that Russian inflation is on its way lower. Consumer prices have increased 1.7% year-to-date. Annualized figure is 3.3% below the central bank expectations. The central bank has now some room to act to normalize its monetary policy.

Currency-wise, the ruble is trading at the highest levels for the last two years against the dollar at 52 ruble for one single dollar note. It is important to remember that before 2013, the USDRUB was trading around 30. We consider that the CBR is willing to strengthen the currency by lowering its key rate. Today’s event should not appear as a non-event but as a remainder of benefiting from the likely strengthening of the Russian currency over the medium-term.