Sample Category Title

GBP/USD Mid-Day Outlook

Daily Pivots: (S1) 1.3193; (P) 1.3245; (R1) 1.3334; More...

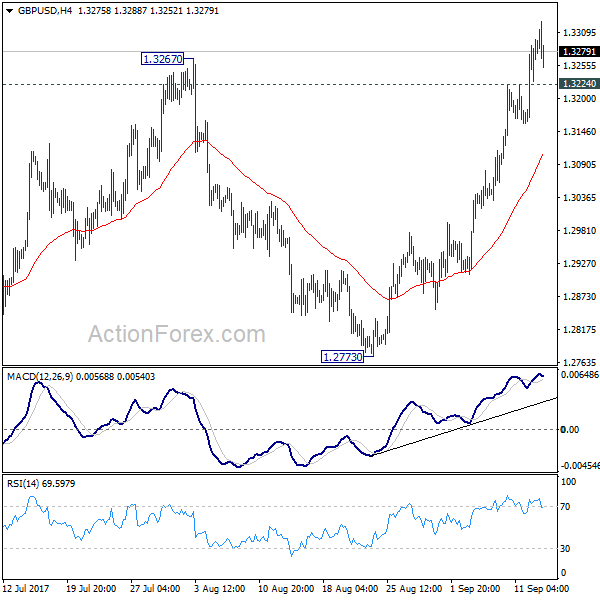

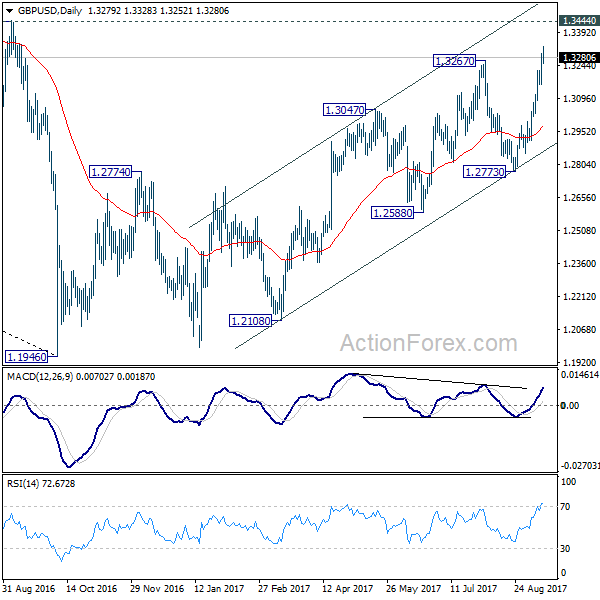

GBP/USD lost momentum after hitting 1.3328 and retreated. But with 1.3224 minor support intact, intraday bias stays on the upside. Current rally is expected to target 1.3444 key resistance next. At this point, we'd maintain that price actions from 1.1946 are still seen as a corrective pattern. Hence, we'd expect strong resistance from 1.3444 to limit upside to bring larger down trend reversal eventually. On the downside below, 1.3224 minor support will turn intraday bias neutral again. However, firm break of 1.3444 will carry larger bullish implication and target 1.3835/5016 resistance first zone first.

In the bigger picture, overall, price actions from 1.1946 medium term low are seen as a corrective pattern. While further rise cannot be ruled out, larger outlook remains bearish as long as 1.3444 key resistance holds. Down trend from 1.7190 (2014 high) is expected to resume later after the correction completes. And break of 1.2773 support will be the first sign that such down trend is resuming. However, considering bullish convergence condition in monthly MACD, firm break of 1.3444 will argue that whole down trend from 2.1161 (2007) has completed. And stronger rise would be seen back to 38.2% retracement of 2.1161 to 1.1946 at 1.5466.

UK Unemployment Dropped to 42 Year Low, But Wage Growth Missed Expectation, Sterling Rally Lost Momentum

Sterling's rally lost some momentum today after job data showed weaker than expected wage growth. Nonetheless, the Pound is still trading in firm tone as markets await tomorrow's BoE rate decision. Dollar also weakens mildly after producer inflation data missed expectation. On the other hand, Canadian and Aussie are trading generally higher today. Gold is trying to regain some from after this week's sharp pull back. But it's yet to break above 1340 handle yet. WTI is back above 48.50 as recent corrective trading extends. There is no sign of momentum for a break through 50 handle yet. Released from US, headline PPI jumped to 2.4% yoy in August but missed expectation of 2.5% yoy. PPI core Rose to 2.0% yoy but also missed expectation of 2.1% yoy.

Treasury Mnuchin: Yellen is being consider by there are a lot others too

US Treasury Secretary Steven Mnuchin said that Fed Chair Janet Yellen is "obviously quite talented" and she's "being considered" as the next Fed Chair after her term expires early next year. However, Mnuchin also noted that " there's a lot of great people that we've been meeting with and considering as well." He declined to comment on front runner White House economic advisor Gary Cohn, nor Cohn's relationship with President Donald Trump. Meanwhile, Mnuchin also reiterated that Trump's administration is still working on getting the tax reform passed this year. There are talks that the corporate tax rates would be reduced from the current 35% to as low as 15%, or somewhere in between. Mnuchin just noted that the final level would put businesses at a "very competitive level" with other countries.

UK unemployment rate dropped to 42 year low

UK employment rate dropped to 4.3% in the three months to July. That's the lowest level in 42 years since 1975. However, wage growth was disappointing. Average weekly earnings rose 2.1% 3moy only, below consensus of 2.3% 3moy. Jobless claims dropped -2.8k in August, better than expectation of 0.6k rise. Focus will turn to tomorrow's BoE announcement. We expect the BOE to vote 7-2 to leave the Bank rate unchanged at 0.25% and the asset purchase at 435B pound. Despite overshooting of inflation, most members would remain cautious and cite slow economic growth and Brexit uncertainty as reasons for keeping the monetary policy accommodative. However, the MPC is expected to adopt a more hawkish tone and strengthen the warning of a weak sterling. The new deputy governor Dave Ramsden would be voting for the first time. He is perceived as a dove amidst his warning of dire consequences after Brexit. He is expected to vote to maintain the status quo in the first 9-member MPC meeting since May. More in BOE To Maintain Status Quo With New Comer On Dovish Side.

Brexit negotiations delayed for a week to Sep 25

The next round of Brexit negotiation between EU and UK is originally scheduled for next week, starting September 18. But it's now be postponed by a week to September 25 to "allow more time for consultation". In a statement, UK said that "both sides settled on the date after discussions between senior officials in recognition that more time for consultation would give negotiators the flexibility to make progress in the September round." The decision came just a week after European Parliament's chief Brexit negotiator Guy Verhofstadt said UK Prime Minister Theresa May was preparing to make an "important intervention... in the coming days".

EC Juncker: Wind is back in Europe's sails

European Commission President Jean-Claude Juncker delivered optimism is his State of the Union speech. He told the European Parliament that "the wind is back in Europe's sails." And, "now we have a window of opportunity, but it will not stay open for ever. Let us make the most of the moment: catch the wind in our sails." Meanwhile, he is pushing for a Minister of Economy and Finance, who should be the chair of all Eurozone finance ministers and be accountable to the European Parliament. And the minister will be in charge of issues not only for the Eurozone, but for all European Union countries. The key responsibility is on deeper economic and financial integration. This is an idea proposed by France and supported by Germany.

ECB Vice Constancio: Non-standard measures to stay

ECB Vice President Vitor Constancio expressed his confidence to hit its mandate eventually, "by keeping a sufficient degree of monetary policy accommodation". He also noted that "non-standard measures are going to be part of our toolkit for some time to come, and some of them might even be deemed standard measures at some point." And, the central bank will "continue using forward guidance to some extent" But Constancio maintained his criticism on it and noted that it's an "imperfect tool", as "one of the various non-standard measures that we can activate when deemed necessary".

Released fro Eurozone, industrial production rose 0.1% mom in July. Employment rose 0.4% qoq in Q2. Germany CPI was finalized at 1.8% yoy in August. Elsewhere, Swiss PPI rose 0.3% mom, 0.6% yoy in August.

Japan PMI Abe offer no hint on who's the next BoJ head

In Japan, Prime Minister Shinzo Abe declined to comment on who would succeed BoJ Governor Haruhiko Kuroda after his five year terms ends in April next year. And, Abe didn't comment on whether Kuroda's term would be renewed. But he hailed that Kuroda's massive monetary stimulus has boosted employment and "created a situation where Japan was no longer in deflation." Abe emphasized that it's important to hit the 2% target and "stabilizes at that level". And, "the government expects the BOJ to continue efforts to meet the target." Meanwhile, Abe said he's still on track to raise sales tax from 8% to 10% in October 2019.

Japan BSI large manufacturing rose to 9.4 in Q3, domestic CGPI rose 0.0% in August.

North Korea pledged to "redouble effort"

North Korea issued an official response to the fresh sanctions approved by United Nations Security Council earlier this week. The foreign ministry condemned the sanctions as "another illegal and evil" one as "piloted by the US. It said in a statement that it aimed at "completely suffocating its state and people through full-scale economic blockade". And it "served as an occasion for the DPRK to verify that the road it chose to go down was absolutely right." North Korea pledged to "redouble the efforts to increase its strength to safeguard the country's sovereignty and right to existence." The country's ambassador to the UN, Han Tae Song, also said yesterday that the country is "ready to use a form of ultimate means". And, "the forthcoming measures ... will make the U.S. suffer the greatest pain it ever experienced in its history."

GBP/USD Mid-Day Outlook

Daily Pivots: (S1) 1.3193; (P) 1.3245; (R1) 1.3334; More...

GBP/USD lost momentum after hitting 1.3328 and retreated. But with 1.3224 minor support intact, intraday bias stays on the upside. Current rally is expected to target 1.3444 key resistance next. At this point, we'd maintain that price actions from 1.1946 are still seen as a corrective pattern. Hence, we'd expect strong resistance from 1.3444 to limit upside to bring larger down trend reversal eventually. On the downside below, 1.3224 minor support will turn intraday bias neutral again. However, firm break of 1.3444 will carry larger bullish implication and target 1.3835/5016 resistance first zone first.

In the bigger picture, overall, price actions from 1.1946 medium term low are seen as a corrective pattern. While further rise cannot be ruled out, larger outlook remains bearish as long as 1.3444 key resistance holds. Down trend from 1.7190 (2014 high) is expected to resume later after the correction completes. And break of 1.2773 support will be the first sign that such down trend is resuming. However, considering bullish convergence condition in monthly MACD, firm break of 1.3444 will argue that whole down trend from 2.1161 (2007) has completed. And stronger rise would be seen back to 38.2% retracement of 2.1161 to 1.1946 at 1.5466.

Economic Indicators Update

| GMT | Ccy | Events | Actual | Forecast | Previous | Revised |

|---|---|---|---|---|---|---|

| 23:50 | JPY | BSI Large Manufacturing Q/Q Q3 | 9.4 | -2.8 | -2.9 | |

| 23:50 | JPY | Domestic CGPI M/M Aug | 0.00% | 0.10% | 0.30% | |

| 00:30 | AUD | Westpac Consumer Confidence Sep | 2.50% | -1.20% | ||

| 06:00 | EUR | German CPI M/M Aug F | 0.10% | 0.10% | 0.10% | |

| 06:00 | EUR | German CPI Y/Y Aug F | 1.80% | 1.80% | 1.80% | |

| 07:15 | CHF | Producer & Import Prices M/M Aug | 0.30% | 0.20% | 0.00% | |

| 07:15 | CHF | Producer & Import Prices Y/Y Aug | 0.60% | 0.40% | -0.10% | |

| 08:30 | GBP | Jobless Claims Change Aug | -2.8K | 0.6K | -4.2K | |

| 08:30 | GBP | Claimant Count Rate Aug | 2.30% | 2.30% | ||

| 08:30 | GBP | ILO Unemployment Rate 3M Jul | 4.30% | 4.40% | 4.40% | |

| 08:30 | GBP | Average Weekly Earnings 3M/Y Jul | 2.10% | 2.30% | 2.10% | |

| 09:00 | EUR | Eurozone Industrial Production M/M Jul | 0.10% | 0.10% | -0.60% | |

| 09:00 | EUR | Eurozone Employment Q/Q Q2 | 0.40% | 0.30% | 0.40% | 0.50% |

| 12:30 | USD | PPI M/M Aug | 0.20% | 0.30% | -0.10% | |

| 12:30 | USD | PPI Y/Y Aug | 2.40% | 2.50% | 1.90% | |

| 12:30 | USD | PPI Core M/M Aug | 0.10% | 0.20% | -0.10% | |

| 12:30 | USD | PPI Core Y/Y Aug | 2.00% | 2.10% | 1.80% | |

| 14:30 | USD | Crude Oil Inventories | 4.1M | 4.6M | ||

| 18:00 | USD | Monthly Budget Statement Aug | -124.3B | -42.9B |

Crude Oil Targets Further Upside Pressure Towards 49.39 Zone

CRUDE OIL: The commodity is building up on its Tuesday gains as it eyes it key resistance residing at 49.39 zone. On the downside, support resides at the 48.00 level where a break will expose the 47.50 level. A cut through here will set the stage for a run at the 47.00 level. Further down, support resides at the 46.50 level. On the upside, resistance resides at the 49.00 level. Further out, resistance comes in at the 49.50 level. A break above here will aim at the 50.00 level and then the 50.00 level followed by the 50.50 level. Its daily RSI is bullish and pointing higher suggesting further strength. All in all, CRUDE OIL remains biased to the upside nearer term.

EUR/JPY Hovers Below A Major Resistance

EUR/JPY has managed to increase as much as 132.00 in the morning, but failed to stay near the today's high and now is trading in the red again. Price reached a very strong dynamic resistance, so the current drop is understandable. A minor decrease will appear if the Nikkei stock index will drop in the upcoming days.

The Yen has increased versus all its rivals as the JP225 has found temporary resistance and now is going down, but this could be only a temporary decrease. JP225 decrease is natural after the impressive rally and after the breakout above the 19700 horizontal resistance. Nikkei could come down to retest the broken levels before will resume the upside movement.

The Nikkei's next upside target will be at the 20058 static resistance, a further increase will punish the Yen, which should drop versus all its rivals.

Price has retested the outside sliding line (SL), but failed to reach the median line (ml) of the black ascending pitchfork. Only a valid breakout above the mentioned levels will confirm a further increase. Is trapped within the inside sliding line and the outside sliding line, so we'll have a fresh trading signal once the rate will escape from this chart pattern.

The current rebound was expected after the failure to retest the inside sliding line (SL) and the upper median line (uml) if the minor descending pitchfork. Technically, it could climb much higher because the Nikkei stock index is expected to resume the rebound.

EUR/USD Increases Ahead The US Data

EUR/USD resumed the yesterday's bullish candle and now is trying to retest the upper median line (uml) of the minor ascending pitchfork. Could be attracted by the confluence area formed at the intersection between the upper median line (uml) and the upper median line (uml) of the descending pitchfork.

A rejection from the mentioned resistance levels will send the rate down again, an important downside target will be at the confluence area formed by the median line (ml) of the descending pitchfork with the median line (ml) of the ascending pitchfork.

USD/CAD Bounced Back

The USD/CAD has managed to increase a little in the yesterday's session, but failed once again to reach the median line (ml) of the minor ascending pitchfork. So the current minor decrease is natural, could retest the lower median line (lml) of the ascending pitchfork, a rejection from there will send the rate much higher on the short term. Is trading near the 1.2150 level, but you should be careful because the US data could bring a high volatility.

GBPUSD Falls After Mixed Data

The British pound has fallen below the 1.3300 handle, moving towards the 1.3250 level against the U.S dollar, after UK economic data showed employment continues to rise, while domestic wage growth remains stagnant.

Earlier, the GBPUSD pair moved to 1.3328, which marked a new 2017 yearly price high, and the highest level for sterling since September 8th, 2016.

Going forward, the GBPUSD pair remains bullish on an intraday basis, whilst trading above its calculated daily pivot point, located at 1.3252.

Key upside technical resistance is now located at the former monthly price high, at 1.3268, and the former daily high, at 1.3298. Above 1.3298, further resistance is found at 1.3328 and 1.3348.

To the downside, intraday GBPUSD technical support is located at 1.3252 and 1.3228. Below the 1.3228 level, a deeper sell-off may take place towards 1.3190 and 1.3159.

EURUSD Rejected at 100 Hour Moving Average

The EURUSD pair has found strong intraday technical resistance just below the psychological 1.2000 level, trading to 1.1995, which represents the single currencies 100-hour moving average.

Price-action is currently trading around the 1.1970, as the euro searches for direction, in narrow range-bound conditions, between the 1.1960 to 1.1995 region.

The EURUSD pair remains neutral on an intraday basis, but strongly bullish in the medium and long-term, as traders await the release of high impact United States economic data.

To the upside, key technical resistance is located at the weekly pivot point, at 1.1999, and the key 1.2030 level. Above the 1.2030 level, further resistance is located at 1.2069 and 1.2092.

To the downside, key technical support is located at the daily pivot point, at 1.1957 and the current weekly price low, at 1.1926.

Below the 1.1926 level, key EURUSD technical support is located at 1.1890 and the monthly time frame, 50 period moving average, at 1.1872.

Market Update – European Session: Disappointing UK Wage Data Undermines Hawkish BOE Sentiment

Notes/Observations

UK July wage data hints that recent pick-up in CPI is yet to be sustainable; personal consumption might remain subdued and thus keep BOE’s hands tied for some time ahead

Overnight

Asia:

Japan PM Abe: No dialogue with North Korea without denuclearization. To work together with the international community to apply maximum pressure, so that North Korea commits to perfect, verifiable and irreversible denuclearization. Completely trust Bank of Japan (BOJ) Gov Kuroda; want to continue accelerating Abenomics with gov and BOJ together

RBA's Harper: Domestic economic growth is too weak to justify a rate hike; economy operating below its potential. AUD currency gains being driven by weaker USD;

Europe:

EU and UK said to have decided on one-week postponement of next round of Brexit talk. The 4th round of talks now expected to begin on Sept 25th. The delay will give negotiators flexibility to make progress in September round. Some cited that political matters forced the delay in UK as PM May planned a major Brexit speech later in Sept

PM May's Conservatives wins vote to ensure govt has majority at committee stage and is granted more control in lawmaking process. House of Commons votes 320-301 in favor of govt motion

Americas:

President Trump: New UN North Korea sanctions are another very small step; sanctions are 'nothing compared to what ultimately will have to happen'

President Trump warned China to get tough on North Korea and reduce trade and financial transactions or it will target Chinese banks

Energy:

Weekly API Oil Inventories: Crude: +6.2M v +2.8M prior

Economic data

(DE) Germany Aug Final CPI M/M: 0.1% v 0.1%e; Y/Y: 1.8% v 1.8%e

(DE) Germany Aug Final CPI EU Harmonized M/M: 0.2% v 0.2%e; Y/Y: 1.8% v 1.8%e

(DE) Germany Aug Wholesale Prices M/M: +0.3 v -0.1% prior; Y/Y: 3.2% v 2.2% prior

(ES) Spain Aug Final CPI M/M: 0.2% v 0.2%e; Y/Y: 1.6% v 1.6%e

(ES) Spain Aug Final CPI EU Harmonized M/M: 0.2% v 0.2%e ; Y/Y: 2.0% v 2.0%e

(ES) Spain Aug CPI Core M/M: +0.2% v -0.7% prior; Y/Y: 1.2% v 1.4% prior

(EU) Euro Zone Q2 Employment Q/Q: 0.4% v 0.5% prior; Y/Y: 1.6% v 1.6% prior

(CH) Swiss Aug Producer & Import Prices M/M: 0.3% v 0.2%e; Y/Y: 0.6% v 0.4%e

(SE) Sweden Q2 Final GDP Q/Q: 1.3% v 1.7%e; Y/Y: 3.1% v 4.0%e

(UK) July Average Weekly Earnings 3M/Y: % v 2.3%e; Weekly Earnings Ex Bonus 3M/Y: % v 2.2%e

(UK) Aug Jobless Claims Change: -2.8K v -2.9K prior; Claimant Count Rate: 2.3% v 2.3% prior

(UK) July ILO Unemployment Rate: 4.3% v 4.4%e (lowest level since 1975)

Fixed Income Issuance:

(IN) India sold total INR160B vs. INR160B indicated in 3-month and 12-month Bills

(DK) Denmark sold total DKK1.22B in 3-month and 6-month bills

(EU) ECB allotted $35M in 7-day USD Liquidity Tender at fixed 1.66% vs 85M prior

(SE) Sweden sold SEK10B vs. SEK10B indicated in 6-month Bills; Avg Yield: -0.7044% v -0.7339% prior; bid-to-cover: 1.40x v 1.66x prior

SPEAKERS/FIXED INCOME/FX/COMMODITIES/ERRATUM

Equities

Indices [Stoxx600 -0.3% at 380.1, FTSE -0.5% at 7361, DAX flat at 12520, CAC-40 -0.1% at 5206, IBEX-35 flat at 10331, FTSE MIB +0.1% at 22258, SMI -0.3% at 9031, S&P 500 Futures -0.1%]

Market Focal Points/Key Themes:

European indices trade mixed this morning with the majority of Indices little changed with the exception of the FTSE 100 which trades 0.5% lower, weighed by a stronger Sterling.

Strong results from Sequana sees shares trade sharply higher, while Dunelm trades higher after an encouraging start to the year. Covestro shares are higher after Bayer further diluted its stake, on the other hand Richemont Shares trade lower despite posting better then expected 5 Month Revenue numbers.

In the US shares of Apple will be in focus after releasing the new Iphone 8 and X.

Looking ahead, the main US earnings for the day is Cracker Barrel.

Equities

Consumer discretionary [Halford [HFD.UK] +1% (Names new CEO). Dunelm [DNLM.UK] +8% (Earnings), Richemont [CFR.CH] -1.4% (5M Sales)]

Industrials: [Sequna [SEQ.FR] +9% (Earnings), Skanska [SAKB.SE] -1.1% (CEO Steps down), Norske Skog [NSG.NO] -56% (Citi accelerates repayment of secured senior notes)]

Healthcare: [Covestro [1COV.DE] +2.7%, Bayer [BAYN.DE] -0.6% (Bayer cuts stake in covestro to 31.5% from 40.9% prior), Quantum Pharma [QP.UK] +20% (Acquired by Clinigen)]

Real Estate: [Galliford Try {GFRD.UK] +1.8% (Earnings)]

Speakers

EU’s Juncker State of the Union address noted that the European economy and confidence were rebounding. Euro Area must have a European Monetary Fund and its own Finance Minister. ESM should gradually become the European IMF; commission to make proposals in December

Germany Fin Min Schaeuble reiterated view that ECB’s extraordinary monetary policy not sustainable over long term; time to start exit from easy policy. He did ECB chief Draghi and basically confident in ECB’s policy course

Denmark Central Bank Q3 review raised its GDP growth forecast for 2017 thru 2019 period. Raised 2017 GDP growth from 1.6% to 2.3; 2018 GDP growth from 1.6% to 1.8% and 2019 GDP growth from 1.6% to 1.7%. It noted that fiscal policy should not stimulate demand further, but rather contribute to ensuring that growth does not overstretch capacity

IEA Monthly Oil Report noted that global oil surplus was beginning to shrink due to stronger-than-expected European and U.S. demand growth, as well as production declines in OPEC and non-OPEC countries. Raised 2017 global oil demand growth forecast from 1.5M bpd to 1.6M bpd. OPEC August oil production at 32.67M bpd vs. 32.84M bpd prior which was the 1st decline in 5 months.

Kuwait Oil Min Almarzooq reiterated that producers should comply with output cuts. Committee to consider all options including more production cuts. OPEC could hold a March meeting on production cut extension. Nigeria to join production cuts once oil output hits 1.8M bpd (**Note: In-line with Saudi comments)

Venezuela Oil Min Del Pino: Opec and Non-OPEC not close to any deal on cuts. Venezuela current production at 2.0M bpd. US actions on country to impact oil investment

Currencies

GBP/USD continued to build upon gains ahead of Thursday’s BOE rate decision. The pair was at a fresh 1-year high above the 1.3325 level. The recent CPI data has brought forward expectations for a Bank of England interest-rate increase. BOE Statement in Aug did note that Policy could be tightened by somewhat greater extent than market expectations if economy met forecasts (QIR saw the 1st rate hike in Q3 2018. The release of UK July wage data hinted that recent pick-up in CPI is yet to be sustainable and caused the GBP currency to move off its best level of the session. The wage data foreshadowed that personal consumption might remain subdued and thus keep BOE’s hands tied for some time ahead

EUR/SEK pair was higher after Sweden 2Q GDP was revised down from preliminary reading.EUR/SEK at 9.5420 just ahead of the NY morning.

Fixed Income

Bund futures trade at 161.81 down 11 ticks and still near the 2-month lows. Continued downside targets 161.42 while upside resistance stands initially at 163.27.

Gilt futures trade at 127.42 up 23 ticks extending their gains as wage data misses. Continued downside eyeing 127.25, then 126.88. Upside targets 128.90 then 129.24.

Wednesday’s liquidity report showed Tuesday’s excess liquidity rose to €1.769T from €1.766T and use of the marginal lending facility fell to €118M from €275M.

Corporate issuance saw $8.9B come to market via 10 issuers headlined Metropolitan Life $1.75B 3-part FA backed note offering and Union Pacific $1B in a 2part senior unsecured note offering

Looking Ahead

(IT) Italy Debt Agency (Tesoro) to sell €6.5-8.0B in 2020, 2024 and 2036 BTP Bonds

05:30 (DE) Germany to sell €3.0B in 0.5% Aug 2027 Bunds

05:30 (UK) DMO to sell £2.5B in 1.25% July 2027 Gilts

05:30 (PT) Portugal Debt Agency (IGCB) to sell €1.0B in 4.125% Apr 2027 OT bonds

(CZ) Czech Republic to sell 2027 and 2036 bonds

06:00 (IL) Israel Aug Trade Balance: No est v -$1.6B prior

06:00 (ZA) South Africa Q3 BER Business Confidence: No est v 29.0 prior

06:00 (RU) Russia to sell combined RUB40B in OFZ 2024 and 2027 bonds

06:30 (IS) Iceland to sell Bills

06:45 (US) Daily Libor Fixing

07:00 (US) MBA Mortgage Applications w/e Sept 8th: No est v +3.3% prior

07:00 (ZA) South Africa July Retail Sales M/M: 0.0%e v 0.2% prior; Y/Y: 2.5%e v 2.9% prior

07:30 (CL) Chile Central Bank's Traders Survey

08:00 (PL) Poland July Current Account: -€0.8Be v -€0.9B prior; Trade Balance: -€0.5Be v -€0.2B prior; Exports: €15.3Be v €16.6B prior; Imports: 15.9Be v €16.9B prior

08:00 (BR) Brazil July IBGE Services Sector Volume Y/Y: -2.4%e v -3.0% prior

08:05 (UK) Baltic Dry Bulk Index

08:30 (US) Aug PPI Final Demand M/M: +0.3%e v -0.1% prior; Y/Y: 2.5%e v 1.9% prior

08:30 (US) Aug PPI Ex Food and Energy M/M: +0.2%e v -0.1% prior; Y/Y: 2.1%e v 1.8% prior

08:30 (US) Aug PPI Ex Food, Energy, Trade M/M: 0.1%e v 0.0% prior; Y/Y: No est v 1.9% prior

08:30 (CA) Canada Aug Teranet/National Bank HPI M/M: No est v 2.0% prior; Y/Y: No est v 14.2% prior, House Price Index: No est v 220.75 prior

09:50 (UK) BOE to buy £1.125B in in APF Gilt purchase operation (over 7-15 years)

10:30 (US) Weekly DOE Crude Oil Inventories

10:30 (SE) Sweden Central Bank (Riksbank) Dep Gov Ohlsson

12:00 (CA) Canada to sell 30-Year Real Return Bonds

13:00 (US) Treasury to sell $12B in 30-Year Bonds Reopening

13:00 (BE) ECB’s Preat (Belgium , chief Economist) in Frankfurt

14:00 (US) Aug Monthly Budget Statement: -$130.5Be v -$42.9B prior

DAX Unchanged As German Inflation Reports Within Expectations

The DAX is showing little movement in the Wednesday session. Currently, the DAX is trading at 12,528.75, up 0.03% on the day. On the release front, German Final CPI posted a small gain of 0.1%, matching the estimate. German WPI gained 0.3%, above the forecast of 0.1%. Eurozone data met expectations, with Employment Change gaining 0.4% and Industrial Production posting a gain of 0.1%.

Germany has enjoyed robust growth in 2017 and has helped lift the entire eurozone economy. Still, the country finds itself grappling with stubbornly low inflation, which has also been a chronic problem in the US, Japan and throughout the Eurozone. German Final CPI, the primary gauge of consumer inflation, slowed to 0.1% in September, down from 0.4% in the August release. German WPI rebounded with a gain of 0.3%, after failing to post a gain for three consecutive months. On the employment front, there was positive news as Eurozone Employment posted a second straight gain of 0.4%. This reflects stronger employment numbers in the eurozone, as stronger economic conditions have improved the labor market and pushed unemployment rates lower.

There's no arguing that the German economy hasn't missed a beat in the first half of 2017, but analysts are divided on how the extent of the momentum. The German Economy Ministry is predicting that the economy could slow in the second half of 2017, and is holding to its forecast of 1.5% growth this year. The BDI Group is projecting an expansion of just above 2.0%, while the International Monetary Fund has pegged growth at 1.8% for 2017. Strong growth in the second half would be good news for the Eurozone and should be bullish for European stock markets.