Sample Category Title

Dollar Falls To 32-Month Low, Rivals Hit Fresh Highs

It was another difficult session for the US dollar as numerous factors including political issues, disappointing economic numbers, and dangerous natural phenomena weighed heavily on the currency driving it to a 31-month low. Consequently, the dollar’s weakness boosted other majors and helped them reach new highs.

The dollar fell to low levels not seen since the beginning of 2015 during the Asian trading hours as the country is preparing to welcome another powerful Hurricane named Irma in Florida, hopes for another rate hike soon are fading while North Korean fears are increasing.

On Friday, New York Fed President William Dudley, an influential member of the rate-setting committee, was less hawkish than previous times, saying that inflation is expected to reach the Fed’s 2% target over the medium-term, while he added that data in the following six months will clarify whether the weakness in inflation is attributed to temporary factors. Moreover, as other fed members supported recently, he argued that interest rates should increase gradually given that inflation will rebound. A day before, the Cleveland Fed President Loretta Mester, who is a voting member of the committee in 2018, supported the above view as well, stating that a gradual pace rate hikes will prevent the economy from overheating as political and fiscal uncertainties keep business optimism subdued.

Meanwhile, Trump claimed yesterday that it is not “inevitable” that the North Korean story will end up with a war but he retained that a military response to North Korean ongoing nuclear programs is still an option.

The dollar index dropped to a 32-month low of 90.96 during the Asian session but managed to climb to 91.15 later on, down 0.51% on the day.

Dollar/yen hit a fresh 10-month low at 107.61 before it edged up to 107.84.

At the same time, GDP growth figures out of Japan came in lower in the second quarter than the preliminary numbers published earlier. The Japanese economy expanded by 0.6% q/q, below the 1% estimated initially and 0.7% forecasted. The actual number for the first quarter was at 0.3%. On a yearly basis, GDP growth fell to 2.5% compared to the preliminary mark of 4.0% and the forecast of 2.9%, while the figure stood at 1% in the previous quarter.

Dollar/swissie stretched down by 0.60% to more than a two-year low of 0.9419.

Euro/dollar surged to a 32-month high of 1.2091 in the session, following the widely expected ECB decision on Thursday to keep its rates unchanged at 0% and deposit rates at -0.4%. However, the ECB Chief Mario Draghi’s’ softer language about the strengthening euro was the main driver of the currency. Draghi did not give hints about whether the central bank will intervene in markets to weaken the common currency while he highlighted that the decision on potential policy tapering will be probably announced in October.

The aussie jumped to a 23-month high of $0.8124 on the back of a buoyant dollar although Chinese data released early today disappointed analysts.

China’s Trade surplus in August narrowed from 46.73bn yuan to 41.99bn yuan while expectations were for a surplus equal to 48.60bn yuan. Exports rose by 5.5% compared to 7.2% observed in July, while analysts expected the figure to increase by 6%. On the other hand, imports increased by 13.3% above the 10.0% expected and 11.0% seen in July.

Australia released home loans data for the month of July. Home loans grew by 2.9%, more than twice the 1.2% seen in June and 1% projected.

Looking at oil markets, oil prices were mixed after the weekly report of the Energy Information Administration which showed that US crude oil inventories rose unexpectedly for the first time after 9 weeks by 4.580mn barrels. This arose as the disastrous tropical storm Harvey reduced the demand for crude oil which is the primary input at refineries. Gasoline inventories which are the first products of the refining process dropped by 1.085mn barrels.

WTI crude oil was down by 0.04% on the day at $49.07 per barrel, while London based Brent was up by 0.35% at $49.06 per barrel.

Regarding gold, the precious yellow metal jumped by 0.32% to $1353.10 an ounce, reaching a 25-month high.

Hurricane Harvey Impacts US Unemployment

The US Department of Labor released Initial Jobless Claims (Sep 1) on Thursday that showed the impact Hurricane Harvey has had on US unemployment. Initial claims for state unemployment benefits increased 62,000 to a seasonally adjusted 298,000 for the week ended Sept. 2, the biggest jump in more than 2 years. With Harvey causing heavy flooding, which disrupted Oil & Natural Gas production, resulting in the temporary closure of Gulf Coast Refineries, Texas saw an increase in Americans seeking unemployment benefits. With Hurricane Irma expected to make landfall in the US on Saturday, markets are concerned what devastation Irma may cause in a region only now starting to get back on its feet.

The ECB Rates decision was no surprise to the markets, keeping rates unchanged, on Thursday. However, ECB President Draghi commented that the ECB was looking at how to wind down its €60 billion a month buying program, indicating the decision will be made in October. With no foreseeable end to Eurozone stimulus, Eurozone Bonds were bought, along with EURUSD which surged higher, reaching a high on the day of 1.20593.

The US Energy Information Administration released data on Thursday that showed US Crude Inventories increased by 4.58M last week – the most since March. With a large number of refineries inoperable, because of Hurricane Harvey, the markets were expecting a buildup in inventories. These inventories should reduce as Gulf Coast refineries are coming back online, but the impending arrival of Hurricane Irma could slow, or potentially stop, this progress. Federal Reserve Bank of New York President Dudley is the latest US central banker to present his views, ahead of a policy-setting meeting later this month.

Dudley reiterated the need to continue raising rates while conceding that the Fed may have to rethink its inflation model.

EURUSD continued strengthening overnight following ECB President Draghi’s comments. Currently, EURUSD is 0.5% higher trading around 1.2085 – levels not seen since late 2014.

USDJPY has weakened 0.6% overnight to currently trade around 107.70 – last seen in October 2016.

GBPUSD continues to improve on overall USD weakness. Currently, GBPUSD is trading around 1.3140.

Gold reached levels not seen for over a year, on concerns that there may be another North Korean missile launch over the weekend. Currently, Gold is trading around $1,356.

WTI initially slipped on the back of the inventories report, but has recovered 0.3% overnight to currently trade around $49.55pb.

At 9:30 BST, the Bank of England will release Consumer Inflation Expectations. A somewhat subjective release, as it is based on consumer’s expectation as to how much price of goods and services are likely to change during the next 12 months. Previously the release was 2.8%.

At 9:30 BST, Reserve Bank of Australia Governor Lowe is scheduled to make a speech. Markets will be looking for any clues as to changes in Australian economic policy.

At 13:30, Statistics Canada will release the Canadian Unemployment rate for August. With the recent surprise rate hike by the Bank of Canada, the markets will be looking to see any change from the previous unemployment rate of 6.3% and how this may underscore economic growth. More so, will be the Net

Change in Employment, that is released at the same time, with consensus calling for an increase to 19K, which could see CAD bulls if the release comes in higher.

EURUSD Analysis: Surges As Draghi Speaks

In result of announcement of the EU Minimum Bid Rate as well as the subsequent Mario Draghi press conference, the Euro expectedly broke to the top and appreciated against the Greenback by 1%. Today, two scenarios might happen. First, once the markets will calm down the buck might make an attempt to recover, thus dragging the pair back to the weekly R1 at 1.2013. But most likely the currency rate will continue the surge towards the monthly R1 at 1.2099. If this target will be reached, the will be another two options. Either the pair will make a rebound from the upper trend-line of a medium-term ascending channel, or it will continue to soar in a junior ascending channel towards the northern boundary of a long-term formation.

GBPUSD Analysis: Tries To Reach 1.3158

An upside momentum provided by the junior ascending channel in conjunction with release of information on the Halifax HPI as well as Mario Draghi speech helped the Pound to break through the upper trend-line of a senior descending channel.

On the one hand, the pair has all chances to continue the surge towards the weekly RR3 at 1.3158. On the other hand, the further direction will very depend on release of data on the UK Manufacturing Production.

If the numbers will be negative, the pair might slip back until a combined support set up by the weekly R2 at 1.3077 and the approaching 55-hour SMA.

USDJPY Analysis: Falls From Senior Channel

Even though a release of information on the Japanese GDP was worse than analysts anticipated, the last day of the week the currency pair started in a sharp downfall. To certain extent, this breakout from a dominant descending channel was triggered by a combined resistance level set up by the weekly and monthly S1 as well as the 55- and 100-hour SMAs. As a result, the next two likely targets for the pair will be the weekly and monthly S2 at 107.33 and 106.98. But starting from the next week, the buck most probably will try to restore some of the lost positions.

However, there is a need to take into account that development of this currency pair will quite strongly depend on geological situation surrounding North Korea.

XAUUSD Analysis: Jumps Above 1,352.00

As it was expected, most of the previous trading day the yellow metal spent in an advance against the buck. On the one hand, this movement was triggered by a combined support created by the 55- and 100-hour SMAs. On the other hand, there is also a need to take into account a pressure from the lower trend-line of a rising wedge, which was moving along the above technical indicators. For this reason, today the pair is expected to make a rebound from the upper trend-line of this long -term formation and, starting from next week, resume the fall towards the monthly R1 at 1,348.36. However, there is a need to carefully monitor development of the North Korean crisis, as its further escalation might continue to stir interest in the gold.

USD/CAD: Building Permits

A stronger-than-anticipated drop in Canadian building permits contributed to further decline in the USD/CAD exchange rate. The Greenback weakened against the Canadian Dollar by 0.020% to continue trading lower in the 1.216-1.218 area.

Statistic Canada released its monthly report showing the value of building permits within the country dropped 3.5% in July, exceeding expectations for a modest 1.5% decline. The fall was sparked by fewer intentions for commercial projects, while residential construction decreased for the first time in the three-month period. The latest figures suggested that construction activity is likely to soften in the following months, as almost all categories marked a decline in the reported period.

EUR/USD: ECB Minimum Bid Rate, Press Conference

EUR/USD revealed muted reaction on the ECB rate announcement ahead of the Central Bank's policy statement. However, the first half an hour of the Mario Draghi speech put the European single currency 72 pips higher against the US dollar, while the further course of press conference managed to keep the Euro above the 1.2000 level.

The ECB President Mario Draghi noted that volatility in the Euro exchange rate was a source of unclarity, causing the necessity to monitor the FX rate impact on price stability being very important for inflation targets and growth. Mr. Draghi stated that underlying inflation trends had improved, but continued to be relatively subdued, while confidence surrounding the future economic growth remained strong.

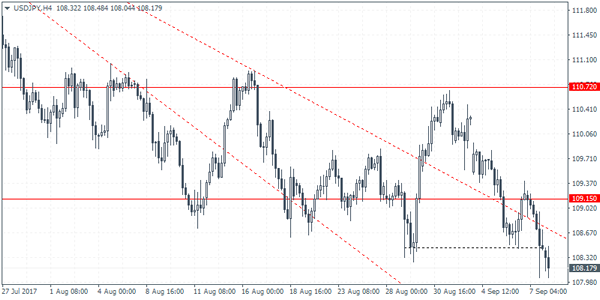

USDJPY Intraday Analysis

USDJPY (108.17): USDJPY slipped to 108.26 marking the lower end of the support zone that has been established. This potentially means that the US dollar could be posting further losses on a daily close below this level. The double bottom pattern that initially formed has been breached and exposes the downside in the currency pair. The next main support is at 108.00 level with major resistance likely to be established at 109.15.

GBPUSD Intraday Analysis

GBPUSD (1.3128): The British pound has managed to post gains as price action rallied above the 1.3033 resistance level. Currently, GBPUSD is testing the trend line break out level which could still offer some near term resistance. The current extension above 1.3033 weakens the potential head and shoulders pattern. If support is established at 1.3033, then the GBPUSD could be seen posting stronger gains in the near term.