Sample Category Title

The US Bond Market Also Received Support From Dovish Comments

Market movers today

In the US, the ISM non-manufacturing index in August is due out today. We believe the fall in July was too big and that it will have recovered some of the lost ground in August . Hence, weest imate the ISM non-manufacturing will come in at 55.0, which is also in line with what the PMI services for August indicates. Tonight at 20:00 CET, the Fed is due to release the Beige Book ahead of the FOMC meeting later this month.

We estimate German factory orders rose 0.4% m/m in July after the big increases in May and June (1.1% and 1.0%, respect ively). With respect to the political development , Angela Merkel still seems on track to secure her fourth term in office, see German Election Monitor No. 1: Next euro area election unlikely to rock the boat, 29 August ).

We expect the Bank of Canada to keep the policy rate unchanged at 0.75% in light of the reduced out look for another Fed hike this year. We still pencil in one 25bp hike in Q4 this year.

In Poland, we expect the central bank to maintain the policy rate at 1.50%.

In Sweden, indust rial and service production data for July are due at 09:30 CET, see page 2.

Selected market news

US Treasuries continue to perform as the crisis in North Korea intensifies and another hurricane is approaching the US mainland. This is also reflected in the equity markets, where the main US indices all fell yesterday. The Asian equity markets have followed the move from the US markets yesterday with falling share prices across the region. The volatility in the markets is increasing as there seems to be a lack of consensus how to deal with North Korea among the US, Russia and China. Most recently, Russian President Put in has rejected more sanct ions against North Korea.

The US bond market also received support from dovish comments by Fed officials Brainard and Kashkari. Neel Kashkari stated that the rate hikes could do real harm against the economy and was against raising rates in March and June. Lael Brainard urged caution in raising rates given the low inflation. The dollar lost versus the euro and the yen on the back of the comments from the officials.

In the front end of the US yield curve, the yield on four-week US T-bills rose at the auction yesterday to the highest level since 2008 as the deadline for raising the US debt ceiling is approaching.

Market Update – Asian Session: Aussie GDP Misses Expectations

Asia Summary

Asian equity markets opened broadly weaker, before falling even lower on uncertainty in US policy and North Korea's latest nuclear test having a chance to reflect for the first time in the US markets after a holiday Monday. AUD held some strength for most of the session before falling to back a slightly weaker level of 0.7990, after Australia Q2 GDP came in slightly lower than expectations. Despite being lower than expectations the 0.8% q/q and 1.8% y/y solidly beat Q1 results. Treasurer Morrison said Expect FY18 budget forecasts to improve if economy stays on current path, a more conservative approach to forecasting has helped the government surpass market expectations and maintain its AAA credit rating.

Offshore yuan continued to climb as the PBOC strengthened the yuan fixing for the 8th consecutive day, making it the longest run since October 2015. A former SAFE official Guan Tao said that China has more leeway to pursue monetary policy goals as yuan’s exchange rate has stabilized this year along with improved forex reserves

Key economic data

(JP) Japan July Labor Cash Earnings Y/Y: -0.3% v +0.5%e; Real Cash Earnings Y/Y: -0.8% v 0.0%e (fastest decline since June 2015)

(AU) AUSTRALIA Q2 GDP Q/Q: 0.8% V 0.9%E; Y/Y: 1.8% V 1.9%E

Speakers and Press

China/Hong Kong

(CN) University of International Business and Economics in Beijing Zhijie: China has more room in monetary policy makes reserve ratio cut an option as yuan depreciation pressure eases

(CN) PBoC Adviser says China should encourage Blockchain technology; China should better regulate virtual currency and there should be stricter supervision for the use of virtual currencies for illegal activities - Chinese Press

(CN) China considering closing North Korea customs post - Chinese press

Korea

(KR) South Korea watching for radiation leak from North Korea test site, so far nothing detected

(KR) South Korea sovereign wealth fund: If a war were to occur on the Korean Peninsula, any impact on the semiconductor industry could be widespread, as South Korean chipmakers supply cellphone and electronics makers globally

(KR) According to analysts North Korea may have as many as 60 nuclear bombs - financial press

Japan

(JP) Former BoJ official/ President of currency think tank Institute for International Monetary Affairs (IIMA)Watanabe: BOJ should stop being obsessed with its 2% inflation target given prices and interest rates around the world remain subdued

Australia

(AU) RBA Gov Lowe: stimulatory policy continues to be appropriate (overnight)

(AU) Australia Treasurer Morrison: Expect FY18 budget forecasts to improve if economy stays on current path

Other\

(US) Fed's Kaplan (moderate, voter):Policy is not as accomodative as some think; Neutral Fed funds rate (FFR) is much closer to 2.25% than it is to 3%

(RU) Russia Energy Min Novak: Confirms OPEC and Russia may extend oil output cap if needed; OPEC deal terms may change after Q1

(SG) Singapore Central Bank (MAS) quarterly survey: Raises Q3 GDP outlook to 3.1% from 2.8%

Asian Equity Indices/Futures (00:00ET)

Nikkei -0.2%, Hang Seng -1.0%; Shanghai Composite -0.3%, ASX200 -0.3%, Kospi -0.4%

Equity Futures: S&P500 -0.0%; Nasdaq100 -0.9%, Dax +0.0%, FTSE100 -0.0%

FX ranges/Commodities/Fixed Income (00:00ET)

EUR 1.1925-1.1903; JPY 108.80-108.51; AUD 0.8021-0.7985; NZD 0.7261-0.7224

Dec Gold -0.1% at $1,343/oz; Oct Crude Oil -0.2% at $48.58/brl; Sept Copper +0.4% at $3.19/lb

(AU) Australia sells A$900M in Nov 2027 bonds, avg yield 2.6125%, bid to cover 3.16x

(CN) China PBoC injects combined CNY40B in 7-day and 28-day reverse repos v skips prior; drains net CNY120B v CNY70B prior (1st injection after 4 consecutive skips, 1st use of 28-day since June 18th)

USD/CNY *(CN) PBOC SETS YUAN REFERENCE RATE AT: 6.5311 V 6.5370 PRIOR (8TH CONSECUTIVE STRONGER SETTING, longest streak since Oct 2015)

(KR) South Korea sells KRW2.4T v KRW2.4T offered in 2-yr monetary stabilization bonds; avg yield 1.69% v 1.74% prior

(CN) China MoF sells upsized 1-yr bonds at 3.4753%; bid-to-cover 1.49x; sells 10-yr bonds at 3.6341% ; bid-to-cover 3.07x

(TH) Thailand sells THB7.0B in 18.8-yr Govt bonds; avg yield 2.8556%; bid-to-cover 3.38x

Equities notable movers

Australia/New Zealand

SXY.AU Canaccord Genuity Raised SXY.AU to Buy from Hold, price target: A$0.36; +20.4%

ACR.AU Reaches mutual agreement with Eli Lilly to terminate licensing agreement for Axiron; -24.5%

Japan

4751.JPCyberAgent Inc, will not be included in Nikkei225; -7%

6098.JPRecruit Holdings to be added to Nikkei225; +6.7%

6502.JP Board was unable to reach a decision on chip sale today – Nikkei; +3.9%

Australian Economic Growth Strengthened In 2Q 2017

For the 24 hours to 23:00 GMT, the AUD rose 0.73% against the USD and closed at 0.8005.

LME Copper prices rose 0.5% or $31.0/MT to $6904.0/MT. Aluminium prices declined 0.6% or $13.5/MT to $2082.0/MT.

In the Asian session, at GMT0300, the pair is trading at 0.7994, with the AUD trading 0.14% lower against the USD from yesterday's close.

Earlier today, data showed that Australia's seasonally adjusted gross domestic product (GDP) advanced by 0.8% QoQ in the second quarter of 2017, boosted by government and consumer spending and compared to a rise of 0.3% in the prior quarter. However, markets had anticipated the nation's GDP to climb 0.9%.

The pair is expected to find support at 0.7952, and a fall through could take it to the next support level of 0.7910. The pair is expected to find its first resistance at 0.8032, and a rise through could take it to the next resistance level of 0.8070.

Looking ahead, investors will closely watch Australia's AiG performance of construction index for August, slated to release overnight. Moreover, the nation's retail sales and trade balance data, both for July, slated to release in the early hours of tomorrow, will be on investors' radar.

The currency pair is showing convergence with its 20 Hr moving average and trading above its 50 Hr moving average.

Euro-Zone’s Services Sector Growth Revised Lower In August, While German Services Sector Activity Notched A 2-Month High In The...

For the 24 hours to 23:00 GMT, the EUR rose 0.21% against the USD and closed at 1.1921.

In economic news, the Euro-zone's final Markit services PMI fell more than initially estimated to a level of 54.7 in August, while the preliminary figures had indicated a drop to a level of 54.9. The PMI had registered a level of 55.4 in the previous month. Moreover, the region's seasonally adjusted retail sales retreated 0.3% on a monthly basis in July, meeting market expectations. In the previous month, retail sales had registered a revised rise of 0.6%.

Separately, growth in Germany's services sector expanded more than initially estimated to a level of 53.5 in August, hitting a two-month high level. The PMI had recorded a reading of 53.1 in the previous month, while the flash print had recorded a rise to a level of 53.4.

The greenback lost ground against a basket of currencies, after a top Federal Reserve (Fed) official expressed caution about further interest rate hikes.

The US Fed Governor, Lael Brainard, urged for caution on raising interest rates further, until there is concrete evidence that inflation is on track to achieve the central bank's target.

Losses in the US Dollar were extended, following downbeat economic data in the US.

Data revealed that the final durable goods orders dropped 6.8% MoM in July, in line with the preliminary print. Market participants had expected for a fall of 2.9%, after registering a gain of 6.4% in the prior month. Further, the nation's factory orders tumbled by the most in nearly three years, after it dropped 3.3% on a monthly basis in July, meeting market consensus. Factory orders had recorded a revised rise of 3.2% in the prior month.

In the Asian session, at GMT0300, the pair is trading at 1.1912, with the EUR trading 0.08% lower against the USD from yesterday's close.

The pair is expected to find support at 1.1873, and a fall through could take it to the next support level of 1.1834. The pair is expected to find its first resistance at 1.1946, and a rise through could take it to the next resistance level of 1.1980.

Going ahead, investors will focus on Germany's Markit construction PMI for August and factory orders data for July, both slated to release in a few hours. Moreover, the US ISM non-manufacturing PMI for August and trade balance data for July, due to release later in the day, will attract a lot of market attention.

The currency pair is showing convergence with its 20 Hr and 50 Hr moving averages.

UK’s Service Sector Growth Slowed To Nearly 1-Year Low Level In August

For the 24 hours to 23:00 GMT, the GBP rose 0.88% against the USD and closed at 1.3041, as investors brushed-off disappointing UK services sector report.

Data indicated that Britain's Markit services PMI declined more-than-expected to a level of 53.2 in August, dipping to an eleven-month low level and suggesting that the nation's services sector, which initially withstood the shock of the Brexit vote, is losing momentum. Markets were anticipating the PMI to fall to a level of 53.5, compared to a reading of 53.8 in the previous month.

In the Asian session, at GMT0300, the pair is trading at 1.3036, with the GBP trading a tad lower against the USD from yesterday's close.

The pair is expected to find support at 1.2949, and a fall through could take it to the next support level of 1.2861. The pair is expected to find its first resistance at 1.3084, and a rise through could take it to the next resistance level of 1.3131.

In absence of any macroeconomic releases in the UK today, investor sentiment will be governed by global macroeconomic news.

The currency pair is trading above its 20 Hr and 50 Hr moving averages.

Japanese Yen Trading On A Weaker Footing This Morning

For the 24 hours to 23:00 GMT, the USD declined 0.98% against the JPY and closed at 108.62.

In the Asian session, at GMT0300, the pair is trading at 108.71, with the USD trading 0.08% higher against the JPY from yesterday’s close.

The pair is expected to find support at 108.29, and a fall through could take it to the next support level of 107.87. The pair is expected to find its first resistance at 109.34, and a rise through could take it to the next resistance level of 109.97.

Moving ahead, market participants will look forward to Japan’s flash leading and coincident indices for July, due to release tomorrow.

The currency pair is trading below its 20 Hr and 50 Hr moving averages.

Swiss Economy Grew Weaker-Than-Expected In 2Q 2017

For the 24 hours to 23:00 GMT, the USD declined 0.46% against the CHF and closed at 0.9539.

Macroeconomic data indicated that Switzerland's seasonally adjusted gross domestic product (GDP) rose less-than-expected by 0.3% on a quarterly basis in the second quarter of 2017, compared to a revised rise of 0.1% in the prior quarter, while markets were anticipating GDP to rise 0.5%. Moreover, the nation's consumer price index (CPI) remained flat on a monthly basis in August, meeting market expectations and compared to a drop of 0.3% in the prior month.

In the Asian session, at GMT0300, the pair is trading at 0.9549, with the USD trading 0.1% higher against the CHF from yesterday's close.

The pair is expected to find support at 0.9517, and a fall through could take it to the next support level of 0.9486. The pair is expected to find its first resistance at 0.9597, and a rise through could take it to the next resistance level of 0.9646.

The currency pair is trading below its 20 Hr and 50 Hr moving averages.

Loonie Trading Lower, Ahead Of BoC’s Interest Rate Decision

For the 24 hours to 23:00 GMT, the USD declined 0.36% against the CAD and closed at 1.2367.

In the Asian session, at GMT0300, the pair is trading at 1.2383, with the USD trading 0.13% higher against the CAD from yesterday's close.

The pair is expected to find support at 1.2343, and a fall through could take it to the next support level of 1.2302. The pair is expected to find its first resistance at 1.2417, and a rise through could take it to the next resistance level of 1.2450.

Ahead in the day, market participants will keep a close watch on Bank of Canada's interest rate decision, scheduled later in the day..

The currency pair is trading above its 20 Hr moving average and showing convergence with its 50 Hr moving average.

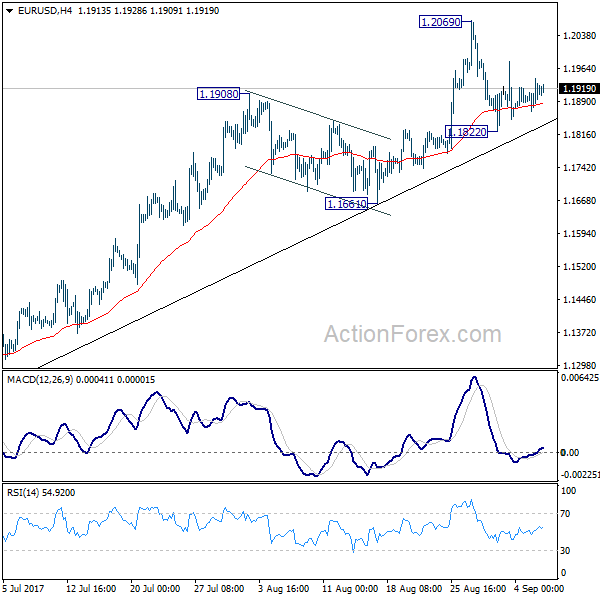

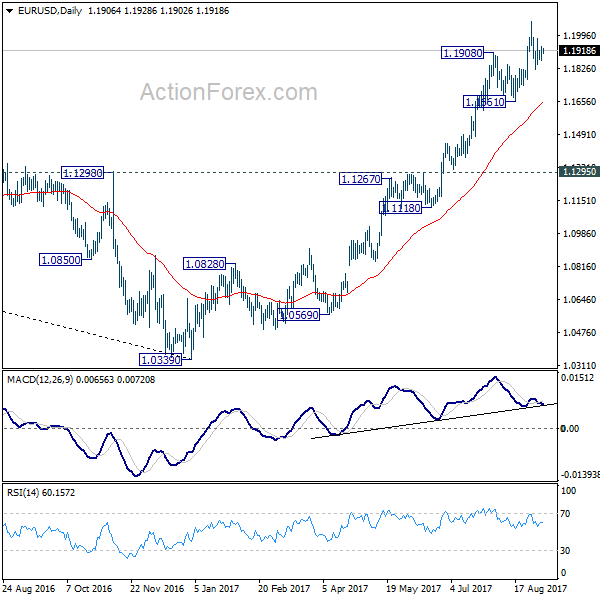

EUR/USD Daily Outlook

Daily Pivots: (S1) 1.1873; (P) 1.1906 (R1) 1.1946; More...

Intraday bias in EUR/USD remains neutral as it's still bounded in consolidation below 1.2069. Below 1.1822 will bring deeper fall. But after all, there is no clear sign of trend reversal yet. Outlook will remain bullish as long as 1.1661 holds. Break of 1.2069 will extend larger rise from 1.0339 to next key fibonacci level at 1.2516. Nonetheless, break of 1.1661 will bring much lengthier consolidation first.

In the bigger picture, an important bottom was formed at 1.0339 on bullish convergence condition in weekly MACD. Sustained trading above 55 month EMA (now at 1.1774) will pave the way to key fibonacci level at 38.2% retracement of 1.6039 (2008 high) to 1.0339 (2017 low) at 1.2516. While rise from 1.0339 is strong, there is no confirmation that it's developing into a long term up trend yet. Hence, we'll be cautious on strong resistance from 1.2516 to limit upside. For now, medium term outlook will remain bullish as long as 1.1295 support holds, in case of pull back.

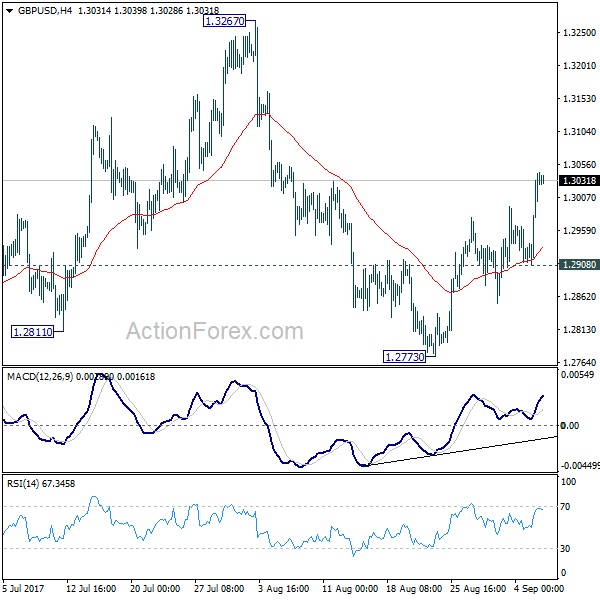

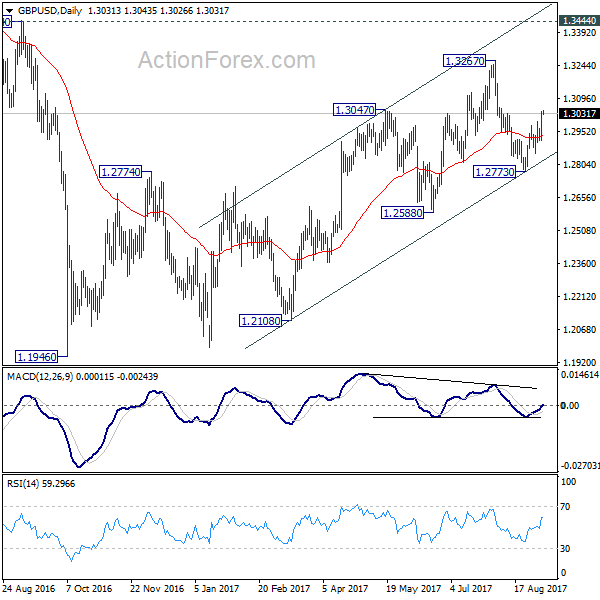

GBP/USD Daily Outlook

Daily Pivots: (S1) 1.2945; (P) 1.2993; (R1) 1.3079; More...

The break of 1.3030 minor resistance argues that pull back from 1.3267 has completed at 1.2773 already. Intraday bias is turned back to the upside for 1.3267 resistance. Break will target 1.3444 key resistance level next. Price actions from 1.1946 are still seen as a corrective pattern. Hence, we'd expect strong resistance from 1.3444 to limit upside to bring larger down trend reversal eventually. On the downside, below 1.2908 minor support will turn bias back to the downside for 1.2773.

In the bigger picture, overall, price actions from 1.1946 medium term low are seen as a corrective pattern. While further rise cannot be ruled out, larger outlook remains bearish as long as 1.3444 key resistance holds. Down trend from 1.7190 (2014 high) is expected to resume later after the correction completes. And break of 1.2588 will indicate that such down trend is resuming.