Sample Category Title

USD/CHF Daily Outlook

Daily Pivots: (S1) 0.9520; (P) 0.9566; (R1) 0.9599; More....

Intraday bias in USD/CHF remains neutral for the moment. On the downside, break of 0.9537 minor support will turn bias back to the downside for retesting 0.9427 first. Break of 0.9427 will resume whole decline from 1.3042. Meanwhile, considering it's close to to 0.9443 key support, consolidation from 0.9427 might extend further. But still, break of 0.9772 resistance is needed to confirm near term reversal. Otherwise, outlook stays bearish for another decline.

In the bigger picture, current development suggests that 0.9443 key support (2016 low) could be taken out firmly as down trend form 1.0342 extends. There are various interpretation of the price actions. But in any case, medium term outlook will stay bearish as long as 0.9772 resistance holds. Current down trend could extend to 38.2% retracement of 0.7065 (2011 low) to 1.0342 (2016 high) at 0.9090. However, break of 0.9772 will indicate that USD/CHF has successfully defended 0.9443 again and turn outlook bullish for 1.0099 resistance.

USD/JPY Daily Outlook

Daily Pivots: (S1) 108.34; (P) 109.09; (R1) 109.54; More...

No change in USD/JPY's outlook. Intraday bias remains on the downside for 108.12/26 support zone. Decisive break there will resume the whole corrective decline from 118.65. Next target will be 61.8% retracement of 98.97 to 118.65 at 106.48. In any case, outlook will remain cautiously bearish as long as 110.94 resistance holds.

In the bigger picture, the corrective structure of the fall from 118.65 suggests that rise from 98.97 is not completed yet. Break of 118.65 will target a test on 125.85 high. At this point, it's uncertain whether rise from 98.97 is resuming the long term up trend from 75.56, or it's a leg in the consolidation from 125.85. Hence, we'll be cautious on topping as it approaches 125.85. If fall from 118.65 extends lower, downside should be contained by 61.8% retracement of 98.97 to 118.65 at 106.48 and bring rebound.

AUD/USD Daily Outlook

Daily Pivots: (S1) 0.7949; (P) 0.7989; (R1) 0.8035; More...

Intraday bias in AUD/USD remains neutral as it's staying in consolidation from 0.8065. In case of another fall, downside should be contained by 0.7785 cluster support (38.2% retracement of 0.7328 to 0.8065 at 0.7783) to bring rebound. On the upside, break of 0.8065 will resume the medium term rise and target 100% projection of 0.6826 to 0.7833 from 0.7328 at 0.8335.

In the bigger picture, rise from 0.6826 medium term bottom is still in progress. At this point, there is no confirmation of trend reversal yet and we'll continue to treat such rebound as a corrective pattern. But in any case, break of 55 month EMA (now at 0.8087) will target 38.2% retracement of 1.1079 to 0.6826 at 0.8451. Break of 0.7328 support is needed to confirm completion of the rebound. Otherwise, further rise is now in favor.

Dollar Talked Down By Dovish Fed Officials, Canadian Dollar Awaits BoC for Guidance

Dollar is trading as the weakest major currency for the week. Dovish comments from Fed officials are weighing on the greenback. Also stocks and yield played catch up after holding and suffered notable lost. DOW closed down -1.07% at 21753.31. 10 year yield dropped through last week's low, losing -0.087 to close at 2.070. 2.0 handle is starting to look vulnerable as recent decline extends.

Japanese Yen is trading as the strongest major currency for the week on mild risk aversion. USD/JPY, despite the selloff, is holding above last week's low at 108.26 so far. More notable move is seen in EUR/JPY, which drops through 129.65 minor support, which suggests more near term weakness. But that was mainly due to Euro's softness ahead of ECB meeting. That can also be seen in EUR/GBP which is extending near term fall from 0.9305.

In other markets, Gold turned into consolidation after hitting 1349.7 and is yet to take out 1350 handle firmly. WTI crude oil jumped to as high as 48.98 so far. But strength in oil is not transferred to Canadian Dollar yet as BoC rate announce looms.

Past Fed hike could have hurt the economy

Minneapolis Fed President Neel Kashkari, a known dove, warned that "it's very possible that our rate hikes over the past 18 months are leading to slower job growth, leaving more people on the sidelines, leading to lower wage growth, and leading to lower inflation and inflation expectations." And, these "premature rat hikes" are "not free". He criticized that Fed might be making "one of two fundamental mistakes". Firstly, Fed is "overestimating how tight the labor market is". secondly, Fed "allowed inflation expectations to drift lower".

Dallas Fed President Robert Kaplan while hurricane Harvey was a "significant" event, it doesn't change his view on the timing about unwinding Fed's USD 4.5T balance sheet. He maintain that Fed should start it "as soon as possible". But regarding another rate hike, Kaplan said that "I actually believe we should be patient here". Fed Governor Lael Brainard also said that Fed should be " cautious about tightening policy further until we are confident inflation is on track to achieve our target." She also noted that "there is a high premium on guiding inflation back up to target so as to retain space to buffer adverse shocks with conventional policy." And she emphasized that " it is important to be clear that we would be comfortable with inflation moving modestly above our target for a time."

Sufficient progress unlikely for Brexit negotiation before October

In UK, Brexit Secretary David Davis told the parliament that UK and EU continues to have "significant differences" over the divorce bill. And two sides have "very different legal stances" on the amount. Davis also said that "time pressure as a pressure point to put up against Britain". But he warned that it is "a pressure tactic to make us pay". Sabine Weyand, EU's deputy Brexit negotiator, told the Bundestag that she doesn't seen the chance of making sufficient progress for EU leaders to give a go to move on to trade agreement in October. The fourth round of talk is scheduled to being on September 18.

A draft document on UK's plan for post-Brexit immigration system was leaked to the Guardian and published. The proposals in the document are to be endorsed by ministers and subject to negotiation with EU. But it's also triggered much controversies as some believed that it targets low skilled EU migrants. Some MPs reacted furiously to the document as criticized it as a "mean and cynical approach". Chair of the home affairs select committee Yvette Copper said the document "seems to contradicts the home secretary's decision just over a month ago". Meanwhile, German MEP Elmar Brok, who's one of European Parliament's Brexit officials, warned that the proposal will " increase the lack of credibility and deepen mistrust". It would make it even harder to reach agreement on divorce by October.

BoC to stand pat and wait for October

The focus today is on the BoC meeting. Recent strong dataflow from Canada has raised bets for a rate hike this month. Real GDP growth accelerated to 4.5% in 2Q17, form 3.7% in the prior quarter. The improvement was significantly better than expected. However, inflation has stayed way below target. It would also be prudent for BoC to be more cautious over tightening the monetary policy as NAFTA talks remain highly uncertain. We expect policymakers to keep the policy rate unchanged at 0.75%, while a rate hike would be implemented in October. The surprisingly strong second quarter GDP growth would also lead the central bank to upgrade its economic forecasts at the October meeting.

Elsewhere

Japan labor cash earnings dropped -0.3% yoy in July. Australia GDP grew 0.8% qoq in Q2, in line with expectation. German factory orders and Eurozone retail PMI will be release in European session. Canada labor productivity and trade balance will be featured in US session. US will release trade balance, ISM services and Fed's Beige Book economic report.

USD/CAD Daily Outlook

Daily Pivots: (S1) 1.2333; (P) 1.2375; (R1) 1.2415; More....

USD/CAD is losing some downside momentum as seen in 4 hour MACD. But still, with 1.2490 minor resistance intact, intraday bias stays on the downside. Current decline from 1.3793 (and 1.4689) is expected to continue and target next long term fibonacci level at 1.2048. On the upside, above 1.2490 will turn focus back to 1.2662. Break there will be the first sign of near term reversal.

In the bigger picture, price actions from 1.4689 medium term top are seen as a correction pattern. Such corrective fall is expected to extend to 50% retracement of 0.9406 to 1.4869 at 1.2048. At this point, we'd look for strong support from there to contain downside and bring rebound. Break of 1.2777 resistance will indicate reversal and turn outlook bullish for 1.3793 key resistance. However, sustained break of 1.2048 will carry larger bearish implications and bring deeper decline.

Economic Indicators Update

| GMT | Ccy | Events | Actual | Forecast | Previous | Revised |

|---|---|---|---|---|---|---|

| 0:00 | JPY | Labor Cash Earnings Y/Y Jul | -0.30% | 0.50% | -0.40% | |

| 1:30 | AUD | GDP Q/Q Q2 | 0.80% | 0.80% | 0.30% | |

| 6:00 | EUR | German Factory Orders M/M Jul | 0.20% | 1.00% | ||

| 8:10 | EUR | Eurozone Retail PMI Aug | 51 | |||

| 12:30 | CAD | Labor Productivity Q/Q Q2 | 1.40% | |||

| 12:30 | CAD | International Merchandise Trade (CAD) Jul | -3.8B | -3.6B | ||

| 12:30 | USD | Trade Balance Jul | -44.6B | -43.6B | ||

| 13:45 | USD | US Services PMI Aug F | 56.9 | 56.9 | ||

| 14:00 | CAD | BoC Rate Decision | 0.75% | 0.75% | ||

| 14:00 | USD | ISM Services/Non-Manufacturing Composite Aug | 55.5 | 53.9 | ||

| 18:00 | USD | Federal Reserve Beige Book |

USD/CAD Daily Outlook

Daily Pivots: (S1) 1.2333; (P) 1.2375; (R1) 1.2415; More....

USD/CAD is losing some downside momentum as seen in 4 hour MACD. But still, with 1.2490 minor resistance intact, intraday bias stays on the downside. Current decline from 1.3793 (and 1.4689) is expected to continue and target next long term fibonacci level at 1.2048. On the upside, above 1.2490 will turn focus back to 1.2662. Break there will be the first sign of near term reversal.

In the bigger picture, price actions from 1.4689 medium term top are seen as a correction pattern. Such corrective fall is expected to extend to 50% retracement of 0.9406 to 1.4869 at 1.2048. At this point, we'd look for strong support from there to contain downside and bring rebound. Break of 1.2777 resistance will indicate reversal and turn outlook bullish for 1.3793 key resistance. However, sustained break of 1.2048 will carry larger bearish implications and bring deeper decline.

Market Morning Briefing: Strength In The Yen

STOCKS

Dow (21753.31, -1.07%) fell sharply, in line with our doubts as mentioned yesterday. The effort to rise towards 22000 in the last 4-sessions has been invalidated in a single session yesterday, the most important issue being the geopolitical tensions with North Korea. However, the index may not break below 21675 just now and could see some recovery in the coming sessions. A break below 21675 would be an indication of a fresh fall for the medium term.

Dax (12123.71, +0.18%) tested 12200 on the upside but came off from there to close at 12123. Note that 12200-12300 region could be a decent resistance that could push the price back towards 12000 or lower in the near term.

Nikkei (19312.25, -0.38%) is trading at lower levels. There is a fair chance of eventually moving down towards 19100-19000 levels in the next few sessions. Near term looks bearish while the US-Japan 10YR differential (2.05%) is headed lower towards 1.9%. Dollar Yen could also continue to ove down if Nikkei and the yield spread falls sharply.

Shanghai (3366.17, -0.54%) could be trading within 3385-3350 levels for a few sessions, continuing to consolidate sideways.

Nifty (9952.20, +0.40%) was almost stable yesterday and as mentioned yesterday, could be trading within 9850-10050 region in the near term. Unless we see a break below 9800-9750, we remain bullish for the medium term.

COMMODITIES

Gold (1344) moved marginally higher as Dollar index failed to hold 92.50 levels and came down at 92.29 regions. Immediate trading range for Gold is 1280-1350 with an interim support at 1335. Gold is overbought in near term thus we are doubtful on the sustainability beyond 1350-55 regions . Similarly Silver (18.00) has also broken its resistance of 17.95 and heading towards 18.25 and 18.50 regions respectively, but it might face some rejection at 18.25 due to overbought condition. In the medium term, both Gold and Silver are out of their short term bearish channel but the supports of 1280 and 16.90 should hold to keep the bullish momentum intact.

Copper (3.138) moved marginally lower but it is still trading above its immediate support of 3.11-12 levels . The only concern in the short term overbought condition which could be resulted short term profit taking anywhere between 3.12-3.26 levels. But we will remain bullish on copper while it is trading above 2.88 levels in the medium term time frame.

Oil Price moved higher but both Brent (53.14) November contract at ICE and WTI (48.56) October contract at COMEX are trading within the ranges of 50-53.47 and 45.60-50.40 respectively. We will be bullish on the energy pack while Brent and WTI are trading above 52 and 48 regions respectively. We have U.S. Weekly oil inventory tomorrow which may add some more clarity into the price action.

FOREX

Dollar Index (92.31) is a stones's throw away from our target of 92.00. But, watch Resistance at 92.67 and 93.00 now. The downtrend since December could start unraveling if these are broken.

Although the chances of the Euro (1.1913) rising to 1.20 are still valid, the strength of the upmove could be waning. We have to keep an eye on Support at 1.1870-50 now. Need some carefulness here. Dovishness from Draghi tomorrow could lead to some Euro weakness.

The Euro-Yen (129.50) has come down to our target of 129.45. Now we need to see if the medium-term Support at 129.00 cited yesterday holds good or not. If it holds, we may see a fresh rise towards 131+ going into next week. But, there will be trouble if this Support breaks.

Strength in the Yen (108.70) emanates from the ongoing North Korean issue, which is also reflected in Gold rising to 1344. At the same time, there can be a hope of a rebound in Dollar-Yen if and while the horizontal Support region of 108.25-15 holds. Break thereof, however could be quite bearishness. Need to be very careful here also.

Sharp rise in the Pound (1.3035), breaking out of the indecisive range it has been in over the last few days. This could be significant. A Week Close above 1.30 could lead to a rise to 1.33.

Satisfying rise in the Aussie (0.7994), which saw a high of 0.8028 yesterday. Chances of eventual rise to 0.81 remain valid while above Support at 0.7950 now.

A bit of consolidation coming in on the Chinese Yuan (USDCNY = 6.5321) which bounced a bit from a low of 6.5150 yesterday. Dollar-Rupee (64.1225) may trade between 64.10-20 for some more time, but weakness in Equities could pull it abover 64.20. Be careful.

INTEREST RATES

Contrary to our yesterday's view, US T Bond yields moved lower along with the benchmark US 10Yr yield (2.06%) yesterday. the 10Yr yield might touch 1.97% as it is trading below 2.08 regions.

EUR/USD is hovering around 1.1900 levels as the German yields has been dipped along with U.S, keeping The German-US 2 Yr Spread (-2.10%)is stable at current levels.We have ECB press conference tomorrow at 6.00 pm IST, which may add some clarity towards the future price action in Euro.

Although not much movement has happened on the German-US 2Yr (-2.08%), the German-Us 10Yr (-1.73%) has risen sharply from channel support and looks strongly bullish just now. In case the spread continues to rise towards -1.70% or higher, it could pull Euro along to higher levels too. Watch the 10Yr spread closely.

Japan 10Yr yield (0.02%) has risen sharply by 2bps while the 30Yr (0.80%) and the 5Yr (-0.14%) are almost stable ust now with no directional clarity.

The US-Japan 10Yr differential (2.05%) has fallen sharply from interim resistance levels, in line with our expectation mainly due to fall in the US 10Yr yield. The spread could head towards 1.9% in the coming sessions indicating a fall in Dollar Yen and Nikkei too in the next few sessions.

The UK 5Yr and 30Yr Gilt Yields (5Yr 0.46% and 30Yr 1.62%) are maintaing their bullish momentum sice last few days.The UK 10Yr (1.07%) is also hovering around its crucial resistance of 1.07-08% levels and a close above that could open up 1.25 levels in medium term time frame.

USD/JPY Too Heavy To Be Stopped

Price drops like a rock after the failure to stabilize above the warning line (wl1). The next downside target is at the 108.12 horizontal obstacle, but most likely will take this out as the Nikkei is under immense selling pressure. Should approach and reach the 61.8% retracement level and the long term 38.2% retracement level.

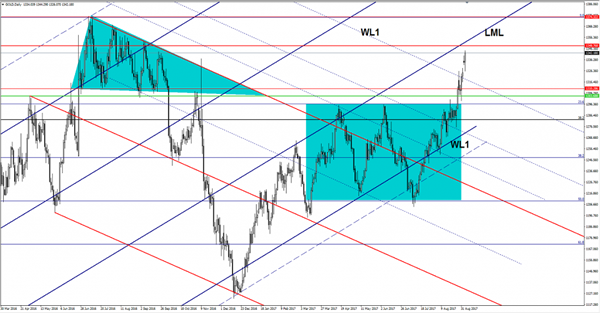

Gold Surges Thanks To Weaker Dollar

The yellow metal rallied in the US session and climbed much above the 1339 Monday’s high. You can see on the Daily chart that has failed to close the former gap up, signaling that the bulls are very strong. Should reach the $1348 per ounce and the lower median line (LML) of the major ascending pitchfork.

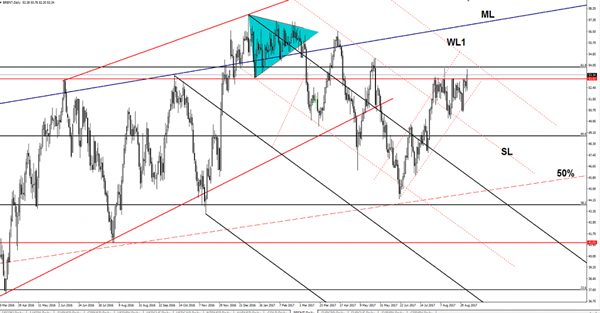

Brent Oil Crucial Breakout Underway

Brent Oil rallied and erased the last two day's losses. Is strong bullish on the daily chart also because the USD/CAD has touched fresh new lows on Tuesday. Technically should climb much higher on the short term after a false breakdown.

Brent has taken advantage of a weaker USD, as you already know, a weaker greenback makes the oil much cheaper for the international customers from outside the United States. The USD/CAD drop helped the oil to climb much higher, but we still need a confirmation that will resume this upside momentum.

You should be careful in the afternoon during the Canadian data release, the Trade Balance could drop further to -3.8B, while the Labor Productivity could increase by 0.9%. The main event will be the release of the Overnight Rate, the BOC is expected to leave the monetary policy unchanged, only a surprise could shake the price.

Price rallied and has managed to climb above the 53.03 major horizontal resistance, but failed once again to reach and retest the 61.8% retracement level. Now has retreated a little and could retest the broken static resistance before will climb much higher. Only a false breakout will signal a reversal on the short term.

Brent continues to move higher within the ascending channel, so it should climb towards new peaks in the upcoming period. However, only a valid breakout above the warning line (wl1) and above the 61.8% retracement level will confirm an increase towards the major upside target from the median line (ML).

Bank Of Canada Expected To Hold Steady

USD struggling with geopolitical, political and natural storms

The USD is lower against most majors after disappointing economic data, political turmoil at home and abroad and dovish rhetoric from Fed members. Markets are now pricing in close to 100 percent chance of the interest rate staying at 100–125 basis points in September and 31.3 percent of a rate hike December, in early August that probability was 42.81 percent.

The Canadian dollar touched a 26 month high versus the US dollar ahead of the Bank of Canada (BoC) meeting. The Bank of Canada (BoC) will be publishing a rate statement on Wednesday, September 6 at 10:00 am EDT. While no rate change is expected, a hawkish statement could be present as Canadian economic indicators have been stronger than forecasted. Canadian GDP for the second quarter destroyed expectations with a 4.5 percent quarterly growth. The strength of the economy has put a second rate hike to the Canadian benchmark rate firmly on the table but with timing issues that would make the October meeting more suitable for that type of announcement.

Central banks will feature prominently this week with the Reserve Bank of Australia (RBA) already keeping rates on hold on earlier today. In what has been an overriding theme for all major central banks the RBA mentioned weak wage growth and low inflation, but with growth still on target for this year. After the BoC on Wednesday, the next major central bank to hold court will be the European Central Bank (ECB) on Thursday.

The USD/CAD fell 0.21 percent in the last 24 hours. The currency pair is trading at 1.2387 ahead of the interest rate decision on Wednesday by the Bank of Canada (BoC). The Canadian central bank is not expected to raise rates at this meeting, but there is growing probability that they will do so before the end of the year, most likely in October.

The timing of the monetary policy decision is down to uncertainty on what other central banks will do in September. This month could prove crucial for the Fed if it announces the start date of its balance sheet reduction plan. Despite the internal debates about rate increases, all Fed members seem to agree on lowering the size of the balance sheet. The only delay could come if policy makers see no chance of a rate hike in December and instead leave the start of reducing the bond repurchases until the end of the year.

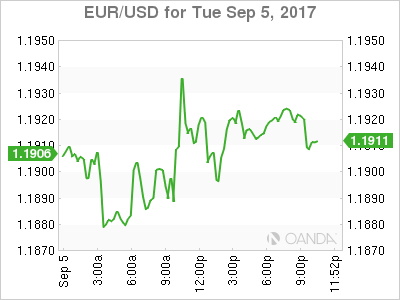

EUR/USD rose 0.088 on Tuesday. The single currency is trading at 1.1912 after North American markets restarted after the labor day holiday. The USD lost ground versus the EUR after political turmoil, soft data and dovish comments from Fed members took a toll on the currency.

Safe haven flows saw the USD back to an oversold position as traders are weighing all the factors in the market and for now the resulting picture is not a positive one for the greenback. A weak US jobs report on Friday and comments from known doves Brainard and Kashkari has put a giant question mark around another rate hike form the Fed this year.

The European Central Bank (ECB) will be front and center this week as it could announce the schedule for its quantitative easing program tapering. Sources from within the central bank came out right after the release of the U.S. non farm payrolls (NFP) stopped the rise of the currency pair above 1.20 by saying the tapering could happen until the end of the year.

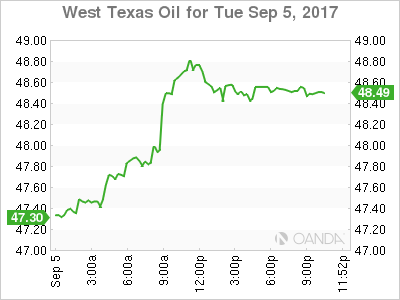

West Texas Intermediate rose 2.586 percent in the last 24 hours. The price of WTI crude is trading at 48.55 after refineries that were hit by Hurricane Harvey are slowly coming back online. With higher refinery capacity available crude prices recovered and gasoline prices have come down. The tropical storm at one point closed down about a quarter of the US refining capacity.

Next on the storm watch is Hurricane Irma which could hit Gulf platforms near Florida, which could hurt US supply of crude acting as a catalyst for higher prices if its a substantial disruption.

Market events to watch this week:

Wednesday, September 6

8:30 am CAD Trade Balance

10:00 am CAD BOC Rate Statement

10:00 am CAD Overnight Rate

10:00 am USD ISM Non-Manufacturing PMI

9:30 pm AUD Retail Sales m/m

9:30 pm AUD Trade Balance

Thursday, September 7

7:45 am EUR Minimum Bid Rate

8:30 am EUR ECB Press Conference

8:30 am USD Unemployment Claims

11:00 am USD Crude Oil Inventories

Tentative CNY Trade Balance

Friday, September 8

4:30 am GBP Manufacturing Production m/m

8:30 am CAD Employment Change