Sample Category Title

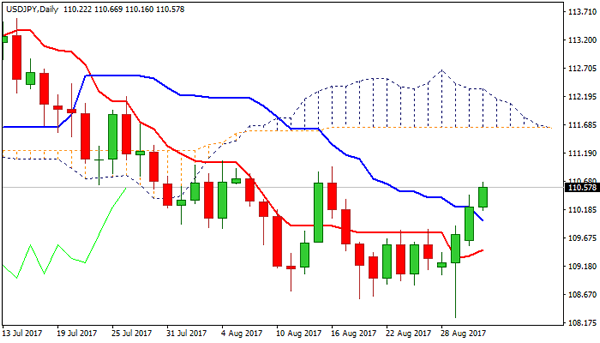

Technical Outlook: USDJPY – Strong Bulls Eye Key Barriers At 111.00 Zone

Strong rally extends into third consecutive day and hits fresh two-week highs on Thursday, approaching key near-term barriers at 111.00 zone, as daily cloud twist continues to attract. Firmly bullish studies on lower timeframes and improving daily technicals are supportive for final push towards a cluster of barriers at 111.00 zone (former tops of 04/16 Aug/converged 100/55SMA's) above which a number of stops is parked that may trigger further acceleration higher on firm break. Meanwhile, bulls may show signs of hesitation at 111.00 barriers as slow stochastic is overbought on daily chart and suggests easing, but without firmer signals so far. Broken 30SMA offers initial support at 110.13, ahead of 20SMA at 109.77.

Res: 110.66, 110.94, 111.18, 111.65

Sup: 110.13, 109.77, 109.53, 109.18

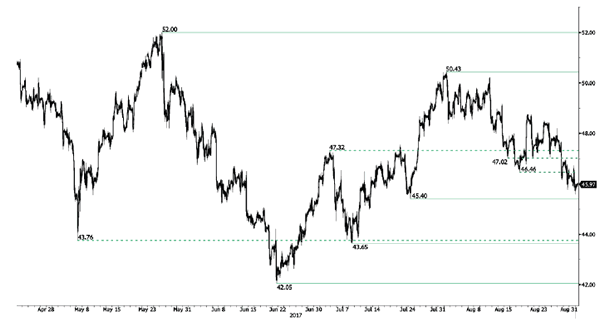

CRUDE OIL Testing Support At 45.40

Crude Oil is trading lower. Hourly support is given at 45.40 (17/08/2017 high). Strong resistance can be found at 50.41 (31/07/2017). Expected to show continued short-term bearish move.

In the long-term, crude oil has recovered after its sharp decline last year. However, we consider that further weakness are very likely. Strong support lies at 35.24 (05/04/2016) while resistance can now be found at 55.24 (03/01/2017 high).

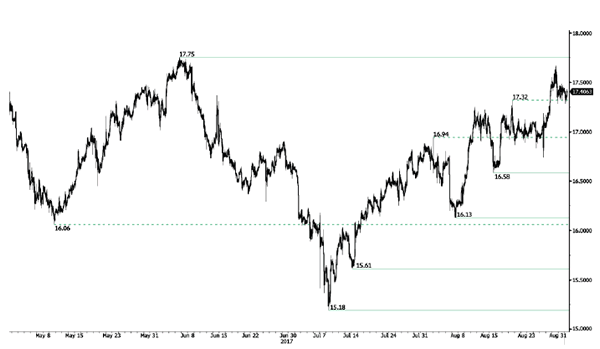

SILVER Short-Term Consolidation

Silver's bullish pressures are strong. Hourly resistance is given at 17.32 (18/08/2017 high) while support can be found at 16.58 (15/08/2017 high). The commodity lies in an uptrend channel. Expected to show another leg higher.

In the long-term, the death cross indicates that further downsides are very likely. Resistance is located at 25.11 (28/08/2013 high). Strong support can be found at 11.75 (20/04/2009).

GOLD Ready To Hit New Highs

Gold is surging. Hourly support is given at a distance 1251 (08/08/2017 low). Stronger support lies at 1204 (10/07/2017 high). Expected to show continued increase.

In the long-term, the technical structure suggests that there is a growing upside momentum. A break of 1392 (17/03/2014) is necessary ton confirm it, A major support can be found at 1045 (05/02/2010 low)

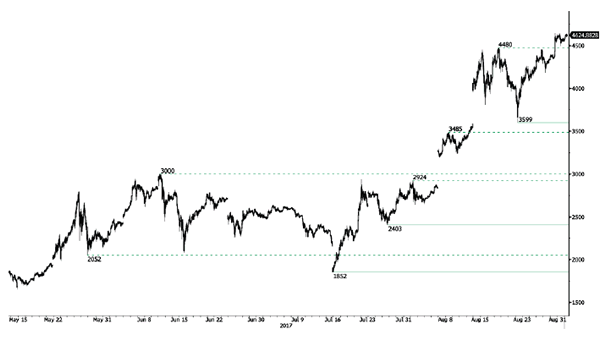

BITCOIN Strong Bullish Momentum

Bitcoin has set a new all-time high. Hourly support lies very far at 3599 (22/08/2017 low). The road is wide open for another bullish move.

In the long-term, the digital currency has had an exponential growth. There are decent likelihood that the asset will consolidate above $1500. Long-term support is given at $1464 (04/05/2017 low).

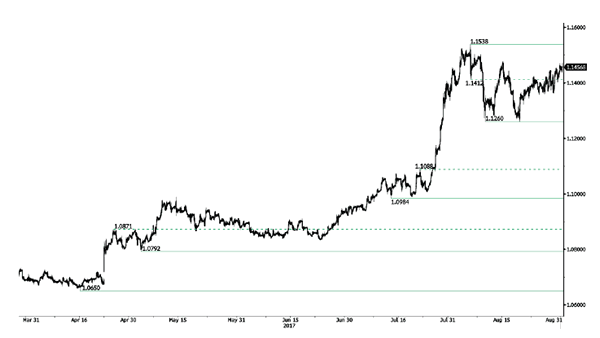

EUR/CHF Edging Higher

EUR/CHF recovery bounce has stalled below downtrend resistance located at 1.1407. Hourly support is located at 1.1260 (04/08/2017 low). Expected to show further consolidation.

In the longer term, the technical structure has reversed. Strong resistance at 1.1200 (04/02/2015 high) has been broken. Yet,the ECB's QE programme is likely to cause persistent selling pressures on the euro, which should weigh on EUR/CHF. Supports can be found at 1.0184 (28/01/2015 low) and 1.0082 (27/01/2015 low).

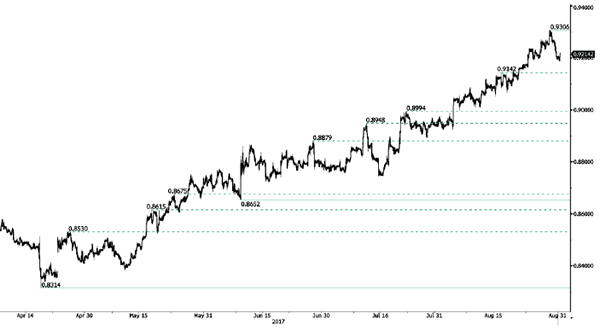

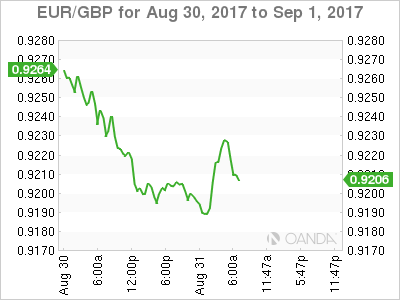

EUR/GBP Buying Pressures Continue

EUR/GBP's buying pressures continues. Hourly resistance lies at 0.9306 (29/07/2017 high). Hourly support is given at 0.9189 (24/08/2017 low). Downside risks are nonetheless important.

In the long-term, the pair has largely recovered from recent lows in 2015. The technical structure suggests a growing upside momentum. The pair is trading above from its 200 DMA. Strong resistance can be found at 0.9500 psychological level.

US Inflation Data Key Ahead Of Friday’s Jobs Report

US futures are pointing to a higher open on Thursday, as we await a batch of data that will be of interest to Fed policy makers ahead of next month's meeting.

Of course, Friday's jobs report is widely regarding as the most important data release each month due to the insight it offers on hiring, wages and therefore potential future inflation pressures. Today's data though is arguably equally important, if not more so at the moment, as it contains the latest inflation numbers – as per the Fed's preferred measure – as well as income and spending figures.

While the Fed has arguably achieved its target on the unemployment side, it still remains well short on inflation so today's data could be seen as the more important when it comes to determining when and how fast the Fed will raise interest rates going forward. Expectations are for inflation to remain at 1.4%, with core falling slightly, also to 1.4%, leaving the Fed once again trailing well behind its 2% target.

With earnings remaining subdued – albeit on a slightly positive trajectory this year – I'm not sure we're seeing enough to convince already uncertain policy makers that the current pace of tightening is appropriate. The December meeting – the most likely timing for the final rate hike this year – is fast approaching and without an improvement in the inflation and income data soon, it may well pass with rates unchanged and expectations going forward much lower.

Initial jobless claims and pending home sales data is also due today, although in all likelihood, focus will likely shift to tomorrow's jobs report after the inflation, income and spending numbers are released. It should therefore be a very interesting end to the week in the markets, even if political and geopolitical events don't rear their ugly head once again. Of course, we can't bank on this given their tendency to do so throughout August, which has helped the likes of Gold hit 2017 highs and remain near these levels. Risk appetite may be returning but traders are still clearly very cautious.

Appetite For U.S Dollar Surges, EUR Pounded

Thursday August 31: Five things the markets are talking about

Capital markets have temporarily rediscovered an appetite for the 'big' dollar and commodities overnight as upbeat Chinese and U.S economic news has increased the demand for riskier assets globally, despite anxieties over North Korea bubbling in the background.

Data Thursday showed that China's manufacturing PMI (51.7 vs. 51.3) further strengthened this month, defying the markets forecasts for a decline. That came after a report yesterday showing U.S Q2 GDP growth reached its fastest pace in two-years on stronger household spending and gains in business investment.

Also stateside, Wednesday's ADP private payrolls indicated robust hiring in August, ahead of tomorrow's U.S non-farm payroll (NFP) report, which could give the market a clue or two on the timing of the Fed's next rate move.

This morning, the U.S releases a key personal consumption expenditure report that the Fed looks at (08:30 am EDT) ahead of tomorrow's granddaddy of economic indicators – U.S non-farm payrolls (NFP – 08:30 am EDT).

1. Stocks get the green light

In Japan, the 'big' dollars strength has taken some of the pressure off the yen (¥110.51) sending Japan equities higher. Overnight, the Nikkei share average (+0.7%) rallied to two-week highs as a weaker yen lifted cyclical stocks such as automakers and financial companies. For the month, the index has slipped -1.4%. The broader Topix gained +0.6%.

Note: Globally, investors remain nervous about the prospect of a U.S government shutdown, and a potential debt default if lawmakers don't raise the U.S debt ceiling by the end of next month, and then there is North Korea.

Down-under, Australia's S&P/ASX 500 Index added +0.8%, while South Korea's Kospi retreated -0.4%.

In Hong Kong, stocks eased overnight, but posted an eighth consecutive month of gains as China's economic recovery and continuous money inflows from the mainland sustained the bullish momentum. The Hang Seng index fell -0.4%, while the China Enterprises Index lost -0.7%. But for the month, the Hang Seng gained +2.4%.

In China, Shanghai stocks ease, but capped their third month of gains on solid earnings. The blue-chip CSI300 index fell -0.3%, while the Shanghai Composite Index shed -0.1%. For the month, CSI300 rose +2.3%, while the SSEC advanced +2.7%.

In Europe, indices continue to recover, trading modestly higher across the board, with grains ranging from +0.4% to +0.7%. Mining and construction stocks lead the decliners on the FTSE, while on the CAC, the retail sector weighs.

U.S stocks are set to open in the black (+0.3%).

Indices: Stoxx600 +0.5% at 373, FTSE +0.6% at 7412, DAX +0.5% at 12061, CAC-40 +0.5% at 5081, IBEX-35 +0.7% at 10315, FTSE MIB +0.6% at 21630, SMI +0.5% at 8897, S&P 500 Futures +0.3%

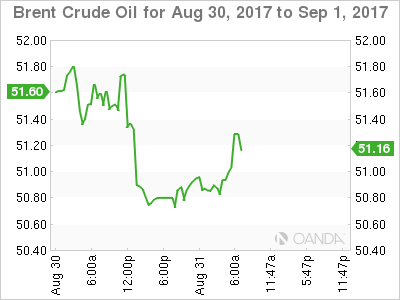

2. U.S gas hits $2 a gallon as Harvey impedes refiners, crude and gold weak

U.S gas prices have hit +$2 a gallon for the first time in two years this morning as flooding from storm Harvey knocked out almost a quarter of U.S refineries, while crude prices remain weak as demand has dropped following the outages.

Note: Due to Harvey, at least +4.4m bpd of refining capacity remains offline. The closure of so many U.S refineries has resulted in a slump in demand for crude oil for the petroleum industry.

The temporary closure of refineries is a major dent to U.S crude demand and is weighing on both Brent and WTI prices. Brent crude is trading at +$50.74 a barrel, down -12c from Wednesday, when the contract fell by more than -2%. U.S West Texas Intermediate (WTI) crude futures are trading at +$46 per barrel, slightly above yesterday's close, when prices fell by -0.8% intraday.

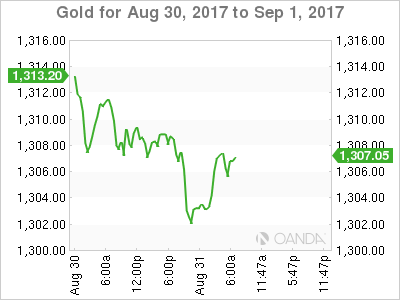

Ahead of the U.S open, gold has slipped a tad as the dollar finds some traction on positive economic data from China and the U.S over the last 24-hours, but continues to hold above the key psychological +$1,300-an-ounce level as safe haven demand due to North Korean tensions cap losses. Spot gold is down -0.4% at +$1,303.11 per ounce and remains on track for a near +3% monthly gain.

3. Sovereign yields fall on the month due to geopolitical concerns

European and U.S bond markets have been caught this week between a stronger tone to economic data globally, putting upward pressure on yields, and concern about rising tensions with North Korea which have boosted demand for safe-haven debt.

The flows back into safe-haven eurozone debt product this month came after a sharp selloff in July on concerns about a scaling back of ECB monetary stimulus.

German Bunds yields are down about -17 bps in August – the biggest fall since February. Currently, 10-year Bund yield is up just +1 bps at +0.37%, edging away from two-month lows hit earlier this week at +0.32%.

In Japan, the Bank of Japan (BoJ) plans to purchase ¥300-500B JGB's this month which mature in 5-10 years. That's -¥50B less than August's stated range.

The announcement could be seen as the BoJ tapering by stealth amid concerns it may soon hit the limit of JGB's it can buy from the market.

Elsewhere, the Bank of Korea (BoK) left its Repo Rate unchanged at +1.25% overnight (as expected), for its 14th straight pause in the current easing cycle. S. Korean policy makers reiterated to maintain the current stance of policy accommodation.

Ahead of the U.S open, the yield on U.S 10-year Treasuries have backed up +2 bps to +2.15%.

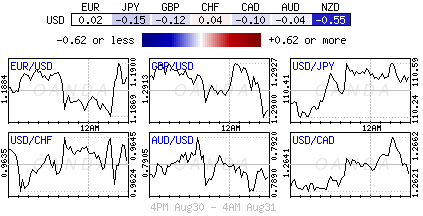

4. Dollar finds support

The USD continues its recent recovery with many attributing the need to pass a disaster relief package for Hurricane Harvey might make it easier for Congress to raise the debt ceiling next month and stronger data in the last two sessions is supporting the greenback.

The EUR/USD (€1.1885) is trading under pressure and has backed off two-big figures from its 2 ½ high (€1.2069). The rapid rise is certainly a concern for the ECB, as it would impede the improvement on EU inflation front.

Note: The ECB meeting is coming up next week and there are rising risks of verbal intervention from Draghi on the EUR's appreciation. Already, France Finance Minister Le Mairea did some verbal intervention noting that a stronger EUR was a 'concern for their domestic economy.'

USD/JPY (¥110.63) is back at its two-week high as geopolitical worries over the Korean Peninsula situation have eased a tad. The US/South Korean military drills are nearing its scheduled end.

GBP (£1.2876) is lower and has ignored commentary by BoE 'hawk' Saunders that the U.K could handle raising interest rates and warned of getting 'behind the curve.'

5. Euro Zone Aug CPI edges higher but still distant from ECB target

Data this morning showed that inflation in the eurozone picked up markedly this month and that the jobless rate remained at its lowest level for over eight years, supporting expectations that the ECB will soon announce a gradual withdrawal from its massive stimulus programs.

The E.U's statistics agency said the region's annual inflation rate rose to +1.5% from +1.3% in July, propelled by energy prices.

Note: Despite the outcome being higher than the +1.4% expected, eurozone inflation continues to undershoot the ECB's target of 'below, but close to' 2%.

The ECB has come under pressure to wind down its stimulus programs from Germany and the market is preparing itself for next week's ECB monetary policy meeting where Draghi could potentially announce something re tapering (Sept. 7).

Other data showed that the eurozone's unemployment rate was stable at +9.1% in July, which marks the lowest level since February 2009.

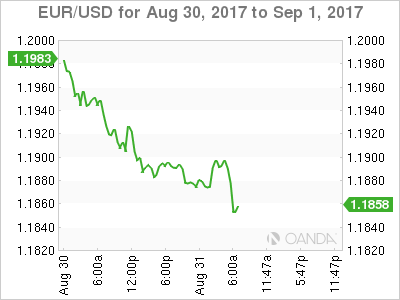

EUR/USD Slips As German Retail Sales Falters

EUR/USD has posted slight gains in the Thursday session. Currently the pair is trading at 1.1860, down 0.21% on the day. On the release front, German Retail Sales declined 1.2%, weaker than the estimate of -0.5%. Euro zone CPI Flash Estimate accelerated to 1.5%, edging above the forecast of 1.4%. In the US, unemployment claims are expected to rise slightly to 237 thousand. As well, Personal Spending is expected to improve to 0.4%. On Friday, the US releases key employment data. Average Hourly Earnings is expected to edge lower to 0.2%, and the markets are braced for Nonfarm Employment Change to drop to 180 thousand.

US numbers looked sharp on Wednesday, and the dollar responded with considerable gains against the euro. Preliminary GDP (second estimate) for the second quarter was revised to 3.0%, a marked improvement from the first estimate of 2.6%. Consumer confidence and spending remain strong and helped contribute to the strong GDP report, as the economy posted its strongest gain since the first quarter of 2015. However, solid consumer spending has failed to boost inflation, which continues to hover at low levels. The lack of inflation could hamper the Federal Reserve's plans to raise interest rates, with the likelihood of a rate hike in December standing at just 35%. On the employment front, ADP Nonfarm Payrolls jumped to 237 thousand, marking a 3-month high. The official Nonfarm Payrolls report will be released on Friday, and if this indicator also beats the forecast, it would be a strong signal that the economic momentum has continued into the third quarter.

The euro has enjoyed a strong run against in the dollar in recent months, jumping 12.0% since April 1. On Tuesday, the currency pushed above the 1.20 level for the first time since January 2015. The euro has benefited from stronger growth in the eurozone in 2017, led by robust growth in Germany. As well, investors are anticipating that the ECB will provide some guidance on plans regarding its asset purchase program (QE), which is scheduled to terminate in December. The ECB is widely expected to taper its QE program early next year, but so far has been mum about its plans. ECB President Mario Draghi opted not to discuss monetary policy at last week's meeting of central bankers at Jackson Hole, which has increased speculation that the issue will be addressed at the bank's policy meeting on September 7.