Sample Category Title

ECB In Getting Inflation Higher

Market movers today

Today is the day we've waiting for all week with both ECB President Mario Draghi and Fed President Janet Yellen speaking at the Jackson Hole Symposium. Yellen will speak at 16: 00 CET on the subject of financial stability. It will be interesting to hear her thought s on the how monetary policy plays a role in this. While full employment and inflation at 2% are the Fed's main objectives, financial stability can play a role too. If she gives any policy signals, we expect her to mirror Fed vice President Bill Dudley's comments last week that another rate hike is warranted this year if the economy holds up. If so, it could be interpreted a bit on the hawkish side given the market is pricing in only a third of a likelihood of a hike by end-year.

Tonight focus will turn to Mario Draghi, due to speak at 21:00 CET. We expect him to lean on the dovish side as the euro strength has challenged the ECB in getting inflation higher and is causing some concern within the ECB, according to the minutes from the previous meeting. He may refrain from giving any signals on tapering as signalled by a recent Reuters' story that quoted two ECB sources saying he would not be giving any new policy signals but await the tapering discussion in the ECB Council in the autumn. See also Euro Area: Draghi returns to Jackson Hole with a dovish message 18 August 2017.

On the data front , we have the German ifo index and US durable goods orders today. These will be in the background though, as attention today will be on Jackson Hole.

In Sweden, PPI and household lending data are due to be published. See Scandi Markets on page 2 for more details.

Selected market news

Concerns about the US debt ceiling negotiations increased further yesterday after President Trump last night , in a series of tweets, blamed top Republican leaders for ignoring his advice on raising the debt ceiling and creating a ‘mess'. Earlier this week, Trump threatened to veto any deal and thereby force a government shutdown if Congress did not pay for his proposed border wall to Mexico. Yields on US treasury bills maturing on 12 October spiked 5bp yesterday – the largest intraday move since March – on rising concerns that the government might miss the payment . Congress needs to agree on a spending plan no later than 30 September to avoid a government shutdown and the Congressional Budget Office (CBO) estimates that the Treasury will run out of money sometime in October.

Japanese consumer prices inched slightly higher to 0.5% y/y in July from 0.4% in June. The weak inflation development in Japan, despite solid GDP growth and the fact that the output gap is closed, underscores that the Bank of Japan (BoJ) is still struggling to push up inflation. Given the BoJ's inflation overshooting commitment, where it has promised to continue ease monetary policy until inflation and inflation expectations are above 2% in a stable manner, we expect the BoJ to maintain its current accommodative monetary policy at least throughout our 12-month forecast horizon, support ing the case for a higher EUR/JPY, driven by widening real interest rate spread and continued port folio out flows out of Japan. We target EUR/JPY at 142 in 12 months.

Aussie Dollar Trading A Tad Lower This Morning

For the 24 hours to 23:00 GMT, the AUD declined 0.09% against the USD and closed at 0.7901.

LME Copper prices rose 0.3% or $22.0/MT to $6577.0/MT. Aluminium prices rose 1.1% or $22.5/MT to $2105.0/MT.

In the Asian session, at GMT0300, the pair is trading at 0.79, with the AUD trading marginally lower against the USD from yesterday's close.

The pair is expected to find support at 0.7875, and a fall through could take it to the next support level of 0.7849. The pair is expected to find its first resistance at 0.7918, and a rise through could take it to the next resistance level of 0.7935.

Next week, traders will closely monitor Australia's building approvals and HIA new home sales data.

The currency pair is showing convergence with its 20 Hr and 50 Hr moving averages.

Euro Trading Flat, Ahead Of German Ifo Survey Data

For the 24 hours to 23:00 GMT, the EUR declined 0.12% against the USD and closed at 1.1800.

Macroeconomic data released in the US indicated that existing home sales unexpectedly eased by 1.3% on monthly basis to a level of 5.44 million in July, dipping to an eleven-month low level and offering signs of a slowdown in the nation’s housing sector. Market participants had envisaged existing home sales to rise to a level of 5.55 million, after recording a revised level of 5.51 million in the prior month. Meanwhile, the nation’s initial jobless claims rose less-than-anticipated to a level of 234.0K in the week ended 19 August, compared to market consensus for a rise to a level of 238.0K. Initial jobless claims had recorded a level of 232.0K in the previous week.

In the Asian session, at GMT0300, the pair is trading at 1.1800, with the EUR trading flat against the USD from yesterday’s close, as investors look forward to remarks from key central bankers at a meeting in Jackson Hole, to get cues on the path of monetary policy.

The pair is expected to find support at 1.1784, and a fall through could take it to the next support level of 1.1769. The pair is expected to find its first resistance at 1.1815, and a rise through could take it to the next resistance level of 1.1831.

Going ahead, investors will look forward to Germany’s Ifo expectations and business climate indices for August along with the final 2Q GDP report, scheduled to release in a few hours. Moreover, the US flash durable goods orders for July, set to release later in the day, will be eyed by traders.

The currency pair is showing convergence with its 20 Hr and 50 Hr moving averages.

UK’s Economic Growth Confirmed At 0.3% In 2Q 2017

For the 24 hours to 23:00 GMT, the GBP marginally declined against the USD and closed at 1.2802.

On the macro front, second estimate of gross domestic product (GDP) rose 0.3% on a quarterly basis in the second quarter of 2017, confirming the flash estimate. In the prior quarter, the nation's GDP had advanced 0.2%. Additionally, the nation's BBA mortgage approvals surged to a five-month high level of 41.59K in July. In the prior month, BBA mortgage approvals had recorded a revised reading of 40.39K.

On the other hand, the nation's preliminary total business investment remained flat on a quarterly basis in the three months to June, meeting market expectations. In the prior quarter, total business investment had climbed 0.6%.

In the Asian session, at GMT0300, the pair is trading at 1.2809, with the GBP trading slightly higher against the USD from yesterday's close.

The pair is expected to find support at 1.2776, and a fall through could take it to the next support level of 1.2744. The pair is expected to find its first resistance at 1.2839, and a rise through could take it to the next resistance level of 1.2870.

Amid a lack of any macroeconomic releases in Britain today, investors will focus on UK's Markit manufacturing PMI, consumer credit and GfK consumer confidence data, all due to release next week.

The currency pair is showing convergence with its 20 Hr and 50 Hr moving averages.

Japan’s Annual Inflation Advanced As Expected In July

For the 24 hours to 23:00 GMT, the USD rose 0.63% against the JPY and closed at 109.57.

In the Asian session, at GMT0300, the pair is trading at 109.64, with the USD trading 0.06% higher against the JPY from yesterday's close.

Overnight data showed that Japan's national consumer price index (CPI) climbed 0.4% YoY in July, meeting market expectations. The CPI had registered a similar rise in the prior month.

The pair is expected to find support at 109.22, and a fall through could take it to the next support level of 108.79. The pair is expected to find its first resistance at 109.92, and a rise through could take it to the next resistance level of 110.19.

Moving ahead, Japan's jobless rate, industrial production, retail trade, small business confidence and consumer confidence data, all slated to release next week, will pique significant amount of investor attention.

The currency pair is trading above its 20 Hr and 50 Hr moving averages.

Switzerland’s Industrial Production Rebounded In The Three Months To June

For the 24 hours to 23:00 GMT, the USD marginally rose against the CHF and closed at 0.9653.

In economic news, Switzerland's industrial production rebounded 2.9% on an annual basis in 2Q 2017. In the previous quarter, industrial production had registered a revised drop of 1.0%.

In the Asian session, at GMT0300, the pair is trading at 0.9647, with the USD trading 0.06% lower against the CHF from yesterday's close.

The pair is expected to find support at 0.9622, and a fall through could take it to the next support level of 0.9596. The pair is expected to find its first resistance at 0.9671, and a rise through could take it to the next resistance level of 0.9694.

Going forward, investors will keep a close watch on Switzerland's ZEW expectations survey, retail sales, UBS consumption indicator and KOF leading indicator data, all slated to release next week.

The currency pair is showing convergence with its 20 Hr moving average and trading below its 50 Hr moving average.

Loonie Extends Its Gains In The Morning Session

For the 24 hours to 23:00 GMT, the USD declined 0.24% against the CAD and closed at 1.2517.

In the Asian session, at GMT0300, the pair is trading at 1.2509, with the USD trading 0.06% lower against the CAD from yesterday’s close.

The pair is expected to find support at 1.2490, and a fall through could take it to the next support level of 1.2470. The pair is expected to find its first resistance at 1.2545, and a rise through could take it to the next resistance level of 1.2580.

Going ahead, market participants will eye Canada’s GDP report, slated to release next week, to gauge strength in the Canadian economy.

The currency pair is trading below its 20 Hr and 50 Hr moving averages.

European Open Briefing: Asian Stock Markets Gained Slightly On Friday

Global Markets:

- Asian stock markets: Nikkei rose 0.53 %, Shanghai Composite up 1.22 %, Hang Seng climbed 0.81 %, ASX 200 down 0.01 %

- Commodities: Gold at $1292.33 (+0.03 %), Silver at $16.94 (+0.01 %), WTI Oil at $47.77 (+0.72 %), Brent Oil at $52.44 (+0.75 %)

- Rates: US 10-year yield at 2.18, UK 10-year yield at 1.05, German 10-year yield at 0.38

News & Data:

- GBP Second Estimate GDP q/q 0.3 % vs 0.3 % expected

- GBP Prelim Business Investment q/q 0.0 % vs 0.2 % expected

- USD Unemployment Claims 234 K vs 237 K expected

- USD Existing Home Sales 5.44 M vs 5.55 M expected

- USD Mortgage Delinquencies 4.24 % vs 4.71 % previous

- Asia stocks resilient, dollar up before Yellen, Draghi speeches

- Oil prices rise as Hurricane Harvey heads for U.S. Gulf coast- RTRS

Markets Update:

Asian stock markets gained slightly on Friday but continued to be more subdued than usual as global investors remain on the sidelines ahead of key comments at a central-banking conclave in Jackson Hole.

USDJPY is currently seen trading at 109.62 as the dollar bulls seem to have a slight edge this morning. USD continued to be slightly stronger on Friday, extending Thursday’s 0.5 percent gain, and heading for an overall weekly rise of 0.4 percent.

EURUSD was seen trading slightly lower at 1.1795. Overall we can see that the price took on more of a Sober approach ahead of the Jackson hole conclave. The dollar index (DXY), which tracks the greenback against a basket of six major peers, was seen trading slightly higher at 93.32 after gaining 0.2 percent, targeting its first monthly rise in six months.

AUDUSD slid to lows of 0.7885 early in the session before retracing back to approach 0.7900 and is barely net changed for the day. Continuing the trend from Thursday. Aussie continues to seesaw around the 0.79 handle.

Upcoming Events:

- 08:00 GMT – (EUR) German Ifo Business Climate

- 12:30 GMT – (USD) Core Durable Goods Orders m/m

- 12:30 GMT – (USD) Durable Goods Orders m/m

- 16:00 GMT – (USD) Fed Chair Yellen Speaks

- 19:00 GMT – (USD) ECB President Draghi Speaks

Will Draghi And Yellen Deliver A Summer Bombshell?

The Jackson Hole Symposium is this week's most anticipated event, in part due to a severe lack of other newsworthy market stories but also because two very important central bankers are scheduled to appear.

The Federal Reserve and the European Central Bank are not only two of the most important central banks in the world, they're expected to be among the more active over the next year, with the former having already begun raising interest rates and the latter in the process of winding down its quantitative easing program.

With announcements expected from both in the coming months, investors will be looking to their speeches at Jackson Hole – a platform used to prepare markets for policy changes by previous Fed Chairs Alan Greenspan and Ben Bernanke – for similar policy signals.

Janet Yellen – Federal Reserve Chair

Yellen's remarks will be poured over by investors, primarily for clues on the future path of interest rates, with the prolonged period of low inflation now starting to unsettle some policy makers. The Fed had previously indicated that it plans to raise interest rates one more time this year but investors have been unconvinced for some time and recently, the scepticism has started to spill over into commentary from some policy makers.

Swing voters within the FOMC, such as Jerome Powell and Robert Kaplan, appear to be among those that still need convincing, while others just appear to lack the belief they once had. Should nothing change then I expect the Fed will likely hold off until next year to raise interest rates further but with the committee appearing so split, it's very difficult to call. This is perfectly reflected in current market implied rate hike expectations.

It's also worth noting that the Fed will soon effectively be tightening on two fronts, with the central bank set to announce in September that it plans to start reducing the size of its balance sheet which was built up in the aftermath of the financial crisis through quantitative easing. The balance sheet currently stands close to $4.5 trillion, a level many believe is far too high.

If the Fed starts the process of balance sheet reduction next month, it may buy them a little more time on interest rates and allow them to wait for inflation to pick up before hiking again.

Whatever they decide, traders will be keenly following Yellen's comments for any suggestion that the pace of rate hikes will be slower than previously expected. Should this happen, we could see further weakness in the dollar and yields could fall.

Mario Draghi – ECB President

While getting policy clues out of Janet Yellen may be difficult, in the case of Draghi it's like trying to draw blood from a stone, at least recently anyway.

The ECB has become obsessed, it seems, with the euro rate and bond yields, and the unintentional tightening in financial conditions that these could trigger. At the end of June, Draghi suggested that recent progress could allow the central bank to pull back on unconventional measures – a clear reference to tapering of asset purchases – and markets were quick to respond.

Despite the market's reaction being far from extraordinary, officials at the ECB were quick to clarify his remarks and effectively reverse the moves that followed it. Clearly they're far more concerned about what are relatively minor moves than they would have us believe.

After this mishap, it seems likely that Draghi will very much keep to the script during his appearance at Jackson Hole and, unfortunately for us, I expect this script will be rather uneventful. Not only will the next ECB meeting in September come with new macroeconomic projections that will shape their decision on QE after December, but his speech also falls at a relatively illiquid time of the day and month. The ECB will want to avoid any sharp appreciation in the currency and a similar rise in bond yields at all costs.

If anything, Draghi may deliver a rather dovish message that still leaves the door open to tapering at the end of the year while carefully managing the euro lower.

Of course, there is the potential that a warning of a policy shift comes from the event – and we should be prepared for significant volatility in case it happens – I just don't expect it to come from Draghi this time around. And Yellen may remain tight lipped as well given the uncertain outlook on inflation.

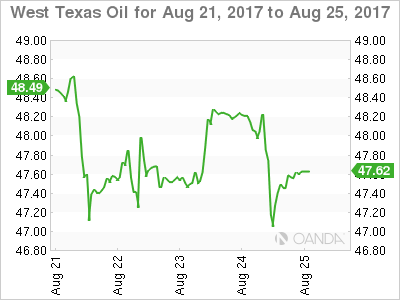

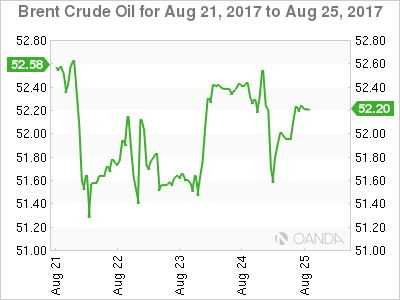

Hurricane Harvey Hits Oil As Gold Relaxes In Jackson Hole

Hurricane Harvey's landfall tonight in Texas promises severe disruption in the oil sector while gold continues to chill ahead of the Jackon Hole Symposium.

Oil prices moved lower overnight with WTI by far the worst performer, falling 1.60% in New York trading despite Hurricane Harvey bearing down on the Texas coast, promising extensive disruption to both refining and extraction operations. The answer may well lie with gasoline futures, which moved the opposite way and rose 2 percent on the day. We suspect that a stronger U.S. dollar overnight and position squaring ahead of Janet Yellen's keynote speech at Jackson Hole were the underlying drivers as Brent also fell, but only by 0.70%.

If Hurricane Harvey's potential to cause disruption and damage in Texas is what the experts are predicting, we expect that the sell-off in WTI may only be transitory. Damage and flooding to refineries and shale fields disrupted production in the Gulf of Mexico and infrastructure damage is unlikely to be bearish for WTI.

WTI spot trades at 47.60 this morning, at its 100-day moving average. Overnight it broke its trend line support of the last week with this line now resistance just above at 47.80. Overnight support lies at 46.90 followed by 46.45. The picture is not positive from a technical perspective, however, given the event risks mentioned we will take it with a grain of salt for now.

Brent spot continues to trade at a healthy premium to WTI, moving slightly higher from its close to 52.40 this morning. It tested but closed above its 200-day average at 51.85 and support remains untested at 51.20. Resistance at 52.70 continues to be the center of attention. Otherwise, the contract seems content to range trade at the upper end of its monthly range into the weekend.

Gold

The summer doldrums continued overnight as gold produced a sideways day ahead of the start of the Jackson Hole Symposium. The trend line support, today at 1282.50, remained untested overnight with gold trading in a 1284.50/1291.50 range.

Ms. Yellen's speech will decide the near term fate of the U.S. dollar, so patience will be required until her keynote address this evening.

Gold's price action continues to be constructive as it consolidates the gains of the last ten days. Resistance remains at 1296.00 followed by the Friday high at 1301.00 with support at 1279.00 and 1267.00.