Sample Category Title

Markets Holding Their Breath as Fed Yellen and ECB Draghi Awaited

The financial markets are generally holding their breath as speeches of Fed Chair Janet Yellen and ECB President Mario Draghi at the Jackson Hole Symposiums are awaited. The occasion is seen in recent years as a platform to launch monetary policy shifts. But this time, neither Yellen nor Draghi is expected to deliver anything drastic regarding monetary policy in near term. At the same time, this could also be Yellen's last address at Jackson Hole since it's uncertain whether she will be granted another term by US President Donald Trump, after the current one expires in February. Yellen might make use of the speech on financial stability to lay down from ground work for the future and leave some legacy.

Fed George and Kaplan differ on rate

Esther George, President of Kansas City Fed which holds the symposium, sounded unbothered with the slowdown in inflation and maintained her push for another rate hike later this year. George told reporters that "while we haven't hit 2 percent, I'm reminded that 2 percent is a target over the long term, and in the context of a growing economy, of jobs being added, I don't think it's an issue that we should be particularly concerned about unless we see something change." And based on what she's seeing, "there's still opportunity" for another rate hike this year.

On the other hand, Dallas Fed President Rob Kaplan sounded more cautious. He noted that "I'm not saying we won't act by the end of the year, but we have the ability to be patient." And, according to Kaplan, the peak of interest rate at this tightening cycle is probably lower than the others. He said that "if you ask me today, I would say it's closer to 2 than to 3". Meanwhile, 10 years ago, he could have said in range of 4-5%.

Japan CPI improved but still way below target

Japan national CPI core ticked up to 0.5% yoy in July, up fro 0.4% yoy and met expectation. Tokyo CPI core rose to 0.4% mom in August, up from 0.2% yoy and beat expectation of 0.3% yoy. Corporate service price slowed to 0.6% yoy in July, down from 0.7% yoy and missed expectation of 0.8% yoy. The inflation reading is still nowhere near to BoJ's 2% target even though growth outlook improved. And the central bank just slashed its annual inflation forecast last month. BoJ expects that inflation won't hit target before 2020.

On the data front, German Q2 GDP final and Ifo business climate are the main features in European session. US will release durable goods orders.

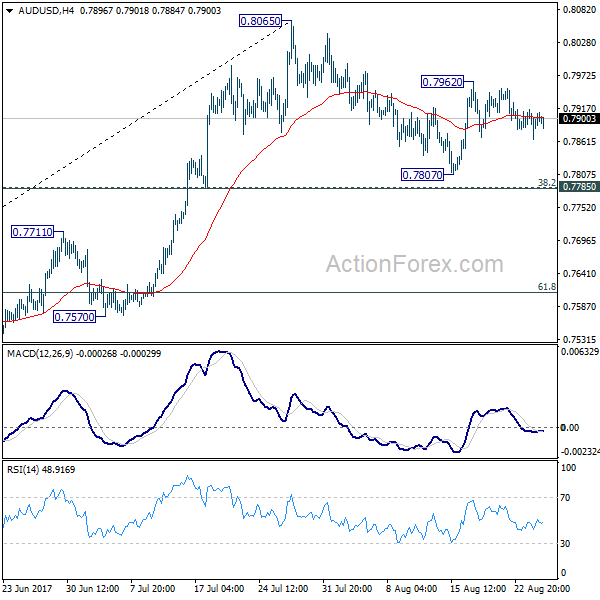

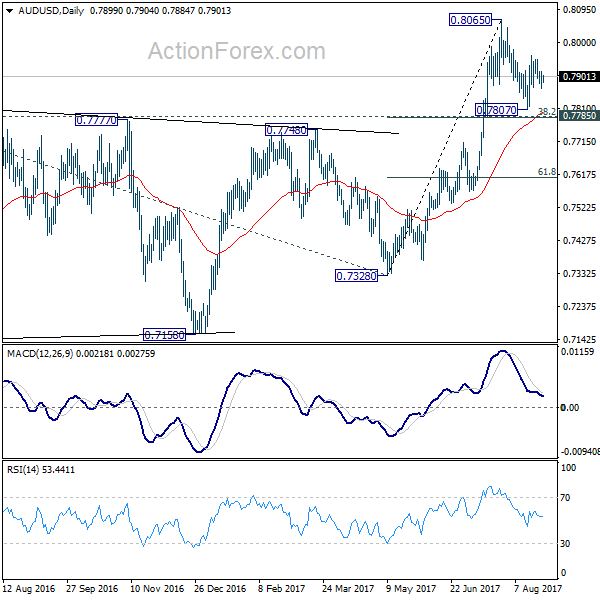

AUD/USD Daily Outlook

Daily Pivots: (S1) 0.7872; (P) 0.7894; (R1) 0.7922; More...

AUD/USD is staying in consolidation and intraday bias remains neutral for the moment. Correction from 0.8065 might extend and another fall cannot be ruled out. But downside should be contained by 0.7785 cluster support (38.2% retracement of 0.7328 to 0.8065 at 0.7783) to bring rebound. Above 0.7962 will target a test on 0.8065 resistance first. Firm break of 0.8065 will resume the medium term rise and target 100% projection of 0.6826 to 0.7833 from 0.7328 at 0.8335.

In the bigger picture, rise from 0.6826 medium term bottom is still in progress. At this point, there is no confirmation of trend reversal yet and we'll continue to treat such rebound as a corrective pattern. But in any case, break of 55 month EMA (now at 0.8097) will target 38.2% retracement of 1.1079 to 0.6826 at 0.8451. Break of 0.7328 support is needed to confirm completion of the rebound. Otherwise, further rise is now in favor.

Economic Indicators Update

| GMT | Ccy | Events | Actual | Forecast | Previous | Revised |

|---|---|---|---|---|---|---|

| 23:30 | JPY | National CPI Core Y/Y Jul | 0.50% | 0.50% | 0.40% | |

| 23:30 | JPY | Tokyo CPI Core Y/Y Aug | 0.40% | 0.30% | 0.20% | |

| 23:50 | JPY | Corporate Service Price Y/Y Jul | 0.60% | 0.80% | 0.80% | 0.70% |

| 6:00 | EUR | German GDP Q/Q Q2 F | 0.60% | 0.60% | ||

| 8:00 | EUR | German IFO - Business Climate Aug | 115.5 | 116 | ||

| 8:00 | EUR | German IFO - Expectations Aug | 106.8 | 107.3 | ||

| 8:00 | EUR | German IFO - Current Assessment Aug | 125 | 125.4 | ||

| 12:30 | USD | Durable Goods Orders Jul P | -5.80% | 6.40% | ||

| 12:30 | USD | Durables Ex Transportation Jul P | 0.40% | 0.10% | ||

| Jackson Hole Symposium |

Unpredictable Jackson Hole

Low expectations for the annual central banker gathering in Jackson Hole in the days ahead set the stage for a surprise. The Canadian dollar was the top performer on Thursday while the yen lagged. Japanese CPI data is due up next. The video for Premium members, focusing on the existing 5 trades and upcoming ideas is below.

Market moves were minimal on Thursday and EUR/USD was locked into a 35-pip range as the market braces for speeches from Yellen and Draghi at Jackson Hole. Other central bankers will be added to the agenda at the annual symposium.

Most of the commentary this week has been dismissive of the speeches from Yellen and Draghi. The topic of Yellen's 10 am ET Friday speech is financial stability, which is sometimes a code word for regulation. Lately, however, the Fed has started to debate whether it's worth raising rates to curb financial risk, even if inflation isn't forecast. If that's the thrust of Yellen's speech, and especially if she argues that it would be prudent to hike in order to curb some excesses in markets, then she could catch the market by surprise.

A week ago, the stakes for Draghi were higher because he was expected to announce, or at least hint, that an ECB taper was coming soon. That plan was scrapped because the ECB has grown increasingly concerned about euro strength, especially with supposed global coordinated tightening failing before it ever got started. However, in the past few months even the smallest hints of tightening have led to major market moves. He could avoi monetary policy, but at least mention the obvious --the growth upswing in the Eurozone.

If the euro sells off, the dip may be short-lived because many market participants are absolutely convinced that it's only a matter of time until the taper announcement comes. So even if Draghi manages to hold the euro down, it's like holding a ball underwater, it's only a matter of time until it pops. AshrafLaidi.com's last 7 trades in EURUSD have each attained a gain of 130-280 pips. The current trade is also in the green.

The yen is likely to be a passenger as it's whipped around by the risk trade on Friday. But before the meetings begin it will briefly have the spotlight with July CPI data due at 2350 GMT. The consensus is for a modest 0.4% y/y rise in the national CPI and just a 0.1% y/y rise in the CPI ex food and energy.

Sterling Hovers Near New Lows as Britain Makes First Step on Brexit Legislation and Growth Stagnates

Today marks a year how the UK Prime Minister gave a speech about Brexit in a Conservative conference and said that "We are not leaving only to return to the jurisdiction of the European Court of Justice - that's not going to happen". Yesterday, though, while May reiterated her view on Britain's own legal path, a Brexit paper on "enforcement and dispute resolution" submitted by the state's secretary David Davis expressed a different opinion. Following the report, which revealed that contradictions between May and her team remain, and today's disappointing evidence on migration, the pound touched new lows against its major counterparts.

The UK's legal positions were put on paper on Wednesday for the first time since the divorce vote in 2016. A few hours later after May reiterated that only the UK and not the ECJ would have the right to decide on the country's legal matters after Brexit. In contrast to May's remarks, the paper which was characterized as "constructive" stated several ways in which the ECJ's permissions would be needed even after the "direct jurisdiction" transitory period (probably three years after divorce) would end. Papers were also published on security and citizen's rights, as well as on a future customs agreement, which is the most important to businesses. The UK government is proposing a "freest and most frictionless possible trade in goods between the UK and the EU". The paper admitted that if the UK refuses to accept EU legal judgment, it will face difficulties to reach a trade agreement with the block. Although the paper did not mention which trade model the UK is heading towards, countries such as Iceland, Liechtenstein, and Norway which operate under ECJ's independent European Free Trade Association court (EFTA), follow ECJ's rules on the single market. The justice minister, Dominic Raab, also argued that the country has to keep "half an eye" on EU legislations as future trade disputes could emerge.

Meanwhile, second estimates of GDP growth figures for the second quarter, published during early European trading hours, showed that the UK economic environment remains fragile. Despite GDP growth rate remaining unrevised at 0.3% q/q and at 1.7% y/y, consumer spending and business investments did not contribute to the country's economic expansion. Household spending rose by 0.1% y/y, the weakest rate posted since 2014, while business spending recorded a 0% growth. Exports and imports increased by 0.7%, while government spending improved by the same amount.

Another report out of the UK showed that net migration has dropped to the lowest level in three years. The Migration Minister, Brandon Lewis, considered this fall as "encouraging", though the head of employment at the CBI, Mathew Percival, claimed that the increasing number of EU departures might lead to skill shortages in the labor market. Based on the statistics, more than half of the fall in net migration was attributed to a decrease of 51,000 EU citizens, the lowest reduction since December 2013.

With political risks heightening and Brexit talks weighing significantly on domestic economic performance, the odds for a rate hike anytime soon are diminishing.

Looking at the reaction in the forex markets, the pound reached a 2-month low of $1.2777 yesterday, while on Thursday cable was trading higher at 1.2810. Euro/pound jumped to a 10 ½ -month high at 0.9235 on Wednesday and pulled back to 0.9207 today. Pound/yen dropped to more than 2-month low of 139.29. Against a trade-weighted basket of currencies, the pound index tumbled to 74.60, its lowest level since November 2016.

Dollar Firmer as Risk Appetite Improves ahead of Jackson Hole; Pound Perks Up on Euro Weakness

Risk appetite improved notably on Wednesday as investors shrugged off the threat of a government shutdown in the United States to focus on the three-day Jackson Hole gathering of central bankers in Wyoming, which starts today. The US dollar extended its Asian session gains to climb towards 109.50 yen, but the euro floundered ahead of an extended speech by ECB head Mario Draghi tomorrow in Jackson Hole.

GDP data dominated the early European session as growth figures were released in Norway and the United Kingdom. British growth was unrevised at 0.3% quarter-on-quarter for the second quarter as expected, but the component breakdowns painted a bleak picture for the UK economy. Business investment was flat in the three months to June, missing forecasts of a 0.4% quarterly gain, while household spending rose by a meagre 0.1%. Other UK data included the CBI's retail sales survey, with the balance of reported sales falling unexpectedly to -10 from +22. Forecasts were for a reading of +15.

The pound initially spiked down after the data, only to quickly resume its uptrend that began in late Asian trading on euro/pound selling. Sterling touched a session-high of $1.2836 before settling around $1.2810 in late European session. The euro slipped against the pound as traders took profit from the pair's sharp gains yesterday. Euro/pound hit a low of 0.9189 from yesterday's 10-month lows before attempting to reclaim the 0.92 level. The single currency also lost ground versus the dollar, easing to around the $1.18 handle.

The Norwegian krone firmed against both the dollar and the euro after growth in Norway jumped to 1.1% q/q in the second quarter. This is up sharply from the growth of just 0.2% in the prior quarter. The dollar was down by about 0.3% at 7.84 kr, with the euro falling a similar amount to 9.25 kr.

The greenback made a steady advance to 109.45 yen but the uptrend lost some of its shine after the release of worse-than-expected housing data. Existing home sales fell by 1.3% in July to an annual figure of 5.44 million. This compares with expectations of 5.57 million and a downwardly revised 5.51 million in June. The dollar slid to around 109.20 after the data, erasing some of the gains from stronger-than-expected weekly jobless claims. Initial claims for unemployment benefits rose by 2k to 234k last week, though this was better than forecasts of an increase to 238k.

The Australian and New Zealand dollars both bounced off support levels to recoup some of their earlier losses. The aussie was flat on the day at around the $0.79 level, while the kiwi fell marginally to $0.7216. The antipodean currencies have been dogged by political concerns in recent days with elections looming in New Zealand in what is turning out to be a tight race, and controversy surrounding senior Australian politicians over dual citizenship.

In commodities, gold was weaker on the back of risk-on and a stronger dollar. The precious metal was slightly lower at $1287 an ounce. Crude oil was also down, despite yesterday's dip in US inventories and the threat of a hurricane hitting Texas, which could cause disruption to supply. WTI oil was 1.3% weaker at $47.79 a barrel and Brent crude was down by a lesser 0.8% at $52.16.

Existing Home Sales Disappoint Again, Pull Back in July

Existing home sales fell 1.3% m/m to 5.44 million (annualized) in July, after sliding by a downwardly revised 2% to 5.51 million in the prior month. The headline print disappointed market expectations which called for a moderate uptick of 0.5%.

Activity pulled back in both the single-family and condo/co-op segments, with transactions falling by 0.8% to 4.84 million in the former and 4.8% to 600 thousand in the latter.

Regional performances were more nuanced, with activity pulling back swiftly in the Northeast (-14.5%, marking the second consecutive decline) and Midwest (-5.3%), while improving in the West (+5%) and South (+2.2%).

The number of homes available for sale fell 1% in July and remained low by historical standards at seasonally unadjusted 1.92 million. This is down 9% from year-ago and accounts for just 4.2 months' worth of sales at the current pace, compared to 4.8 at the same time last year.

The tight inventory is keeping upward pressure on prices, with the median price advancing by 6.2% y/y - roughly in line with the 6.3% pace in the month prior. Properties typically stayed on the market for 30 days - up from 28 days in June but down from 36 days a year ago. Additionally, first-time homebuyers accounted for 33% of sales, up slightly from 32% in the month prior and a year ago.

Key Implications

It's hard to find encouraging details in today's report, given the size and breadth of the decline and the fact that it marks the second consecutive monthly pullback. Existing home sales, while still holding near the 5.5 million mark, have generally trended down since March.

The low inventory of homes available for sale has been one of the main culprits holding back activity in recent months, but we expect to see some improvement on this front. Robust home price growth, while making it harder for some prospective homeowners to enter the market, should help boost inventories as existing homeowners continue to warm up to the idea of listing their properties. This theme is corroborated by results of a recent NAR survey which found that 71% of homeowners believed that now is a good time to sell, compared to 61% for the same period last year.

Moreover, robust demand for homes, owing to an improving labor market, should encourage more homebuilding. The increase in the supply of new homes, particularly in the larger single-family segment, should facilitate a transition away from renovations and into new properties, and help ease gridlock in the resale market. However, this process will be very gradual.

Overall, a recent pullback in mortgage rates, the gradual unlocking of inventories and continued job gains should help support sales activity going forward. In fact, some improvement was already visible in pending home sales which rose robustly in June, breaking a three month streak of declines, with more good news likely on the horizon.

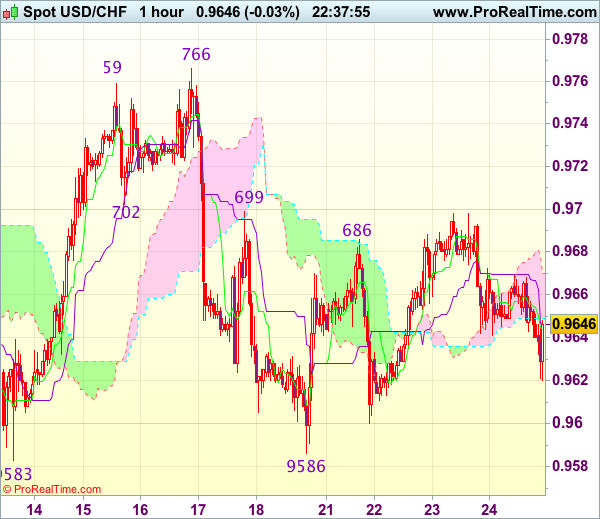

Trade Idea Wrap-up: USD/CHF – Hold long entered at 0.9620

USD/CHF - 0.9630

Most recent candlesticks pattern : N/A

Trend : Sideways

Tenkan-Sen level : 0.9644

Kijun-Sen level : 0.9646

Ichimoku cloud top : 0.9670

Ichimoku cloud bottom : 0.9649

Original strategy :

Bought at 0.9620, Target: 0.9720, Stop: 0.9585

Position : - Long at 0.9620

Target : - 0.9720

Stop : - 0.9585

New strategy :

Hold long entered at 0.9620, Target: 0.9720, Stop: 0.9585

Position : - Long at 0.9620

Target : - 0.9720

Stop : - 0.9585

Dollar’s retreat after faltering below resistance at 0.9699 suggests initial downside risk remains for marginal weakness, however, as long as support at 0.9586 holds, prospect of another rebound remains, above indicated resistance at 0.9699 would signal the retreat from 0.9766 has ended at 0.9586 last week and mild upside bias is seen for gain to 0.9720, then 0.9740, having said that, reckon resistance at 0.9766-73 would cap upside and bring further consolidation. Only a break of 0.9773 would retain bullishness and signal early rise from 0.9438 has resumed and extend gain to 0.9800.

In view of this, we are holding on to our long position entered at 0.9620. Below 0.9600 would risk test of strong support at 0.9583-86 but only break there would signal a downside break of recent broad range has occurred, bring subsequent fall to 0.9550.

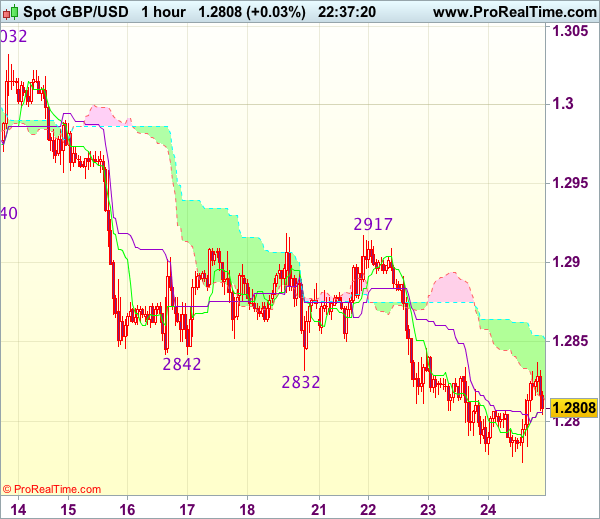

Trade Idea Wrap-up: GBP/USD – Buy at 1.2760

GBP/USD - 1.2805

Most recent candlesticks pattern : N/A

Trend : Near term down

Tenkan-Sen level : 1.2806

Kijun-Sen level : 1.2806

Ichimoku cloud top : 1.2854

Ichimoku cloud bottom : 1.2816

Original strategy :

Buy at 1.2770, Target: 1.2870, Stop: 1.2735

Position : -

Target : -

Stop : -

New strategy :

Buy at 1.2760, Target: 1.2860, Stop: 1.2725

Position : -

Target : -

Stop : -

Although cable has remained under pressure and near term downside risk remains for recent selloff to extend one more fall, loss of downward momentum should prevent sharp fall below 1.2750-55, risk from there has increased for a rebound to take place soon, above 1.2845-50 would suggest a temporary low is possibly formed, bring a stronger rebound to 1.2870, break there would add credence to this view, then retracement of recent decline would commence for further gain to 1.2900.

In view of this, we are inclined to turn long on next decline. Below 1.2740-50 would risk weakness to 1.2720-25, however, still reckon downside would be limited to 1.2700-05 (100% projection of 1.3269-1.2940 measuring from 1.3032) and risk from there remains for another rebound to take place later.

Trade Idea Wrap-up: EUR/USD – Hold long entered at 1.1765

EUR/USD - 1.1796

Most recent candlesticks pattern : N/A

Trend : Sideways

Tenkan-Sen level : 1.1797

Kijun-Sen level : 1.1804

Ichimoku cloud top : 1.1782

Ichimoku cloud bottom : 1.1774

Original strategy :

Bought at 1.1765, Target: 1.1865, Stop: 1.1770

Position : - Long at 1.1765

Target : - 1.1865

Stop : - 1.1770

New strategy :

Hold long entered at 1.1765, Target: 1.1865, Stop: 1.1770

Position : - Long at 1.1765

Target : - 1.1865

Stop : - 1.1770

As the single currency has retreated after faltering below resistance at 1.1828, suggesting minor consolidation would be seen, however, as long as 1.1765-70 holds, mild upside bias remains for another rebound, above said resistance at 1.1828 would extend the rise from 1.1662 low to resistance at 1.1847, break there would provide confirmation that the pullback from 1.1910 has ended and encourage for headway to 1.1870-80 but reckon said resistance at 1.1910 would hold from here.

In view of this, we are holding on to our long position entered at 1.1765. Only below 1.1740 support would abort and suggest the rebound from 1.1662 has ended instead, risk weakness to 1.1695-00 first.

The Confluence of Factors that Makes a Fragile Kiwi

After breaking several technical levels, New Zealand dollar looks vulnerable to further fall against both Australian dollar and US dollar. We believe the selloff over the past few days is driven by several factors, including weakness in soft commodity prices, unwinding of net speculative long positions, government's GDP growth downgrade and uncertainty in the upcoming parliamentary election.

Commodity Prices Retreated after Reaching Peaks

Recent rally in base metal prices has lifted Aussie. However, it does not offer the same advantage to its counterpart, New Zealand, where most exports are soft commodities such as dairy (around 40% of NZ exports), meat and wood. Prices weaknesses in these categories are weighing on New Zealand dollar. For instance, global dairy price in aggregate dropped -2% in the first two weeks in August. According to ANZ's estimates, meat price fell for the first time this year in July, losing -3.38% m/m as lamb prices fell more almost -7%. The overall commodity price index also dropped -0.77% last month.

Unwinding of Net Speculative Long Positions

Net speculative long positions have accelerated since mid-June, eventually rising to a record high of 35 981 contract on the week ending July 19. NZDUSD also peaked a week later that speculators unwound their positions. The latest report shows that net long positions plunged -8 646 contracts to 24 835 in the week ending August 15. This biggest weekly decline in 11 months exacerbated kiwi's decline. We believe unwinding has more to come as the current level of net long positions stays at the highest level since 2013. As such, further decline in kiwi is likely.

GDP Growth Downgrade

As suggested in the Pre-election Economic and Fiscal Update (PREFU) released on Wednesday, the government revised lower New Zealand's GDP growth forecast to +2.6% for the year to June, from May's projection of +3.2%. It also lowered GDP growth to +3.5% for the next year from +3.7% previously. This overshadowed the upward revision on the budget surplus forecast to NZ$3.706B in the year to June, from the previous NZ$1.62B. The increase was driven by strong corporate tax revenue which was only a one-off factor. Meanwhile, lower growth outlook implies less potential tax revenue. This might affect future budget.

Upcoming Election is a Tight Race

Like many of the elections over the year, the upcoming New Zealand general election is highly uncertain. Recent polls have been suggesting that no political party would be able to get at least 61 seats out of 120 and form a majority government at the general election to be held on September 23. Back in 2014 the National Party missed a majority by one seat. Poll of polls showed that the support for the National Party has been slipping gradually while that for the Labour Party, the major opposition, is increasing. Support for Nationals fell to 43-44% as of August 18, from 47-48% a week ago. During the period, support for Labors jumped to around 34%, from below 30%. If we consider the Labour- Green alliance, the support remains shy of 50% and even below that of Nationals'. It is widely believed that the kingmaker would be the populist NZ First party. We find some of NZ First's agenda NZD-negative. For instance, it proposes to reform the RBNZ to create an exporter friendly "sensible exchange rate regime", review all existing free trade agreements (FTAs) and limit foreign investment by adopting "national interest test". Meanwhile, its proposal to cap net migration at 10K per year might dampen New Zealand's growth outlook in the longer term. Certainly, NZ First's proposal of the most expensive fiscal policy- NZ$22.5B in new spending over the next three years- might be NZD-positive. Since it is likely a neck-and-neck race between Nationals and Labours, no one would say in confidence which party would get the most seats and which party(ies) would be able to form a government before the election. We believe the kiwi's volatility would increase as Election Day approaches.

Key Dates:

| Tuesday 29 August | Nominations close for individual electorate candidates |

| Monday 11 September | Advance Voting starts |

| Saturday 23 September | Election Day |

| Preliminary results released progressively from 7.00pm on | |

| Saturday 7 October | Official results for general election declared |

| Wednesday 11 October | Deadline for applications for Judicial Recount |

| Thursday 12 October | Return of Writ showing successful electorate candidates |

Source: http://www.elections.org.nz

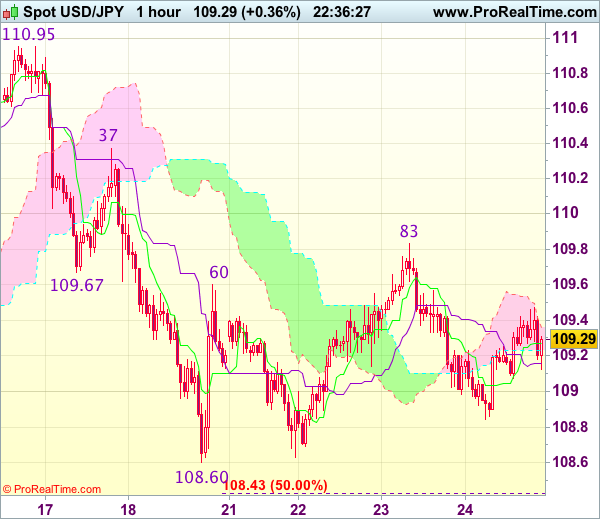

Trade Idea Wrap-up: USD/JPY – Stand aside

USD/JPY - 109.32

Most recent candlesticks pattern : N/A

Trend : Near term down

Tenkan-Sen level : 109.27

Kijun-Sen level : 109.16

Ichimoku cloud top : 109.36

Ichimoku cloud bottom : 109.23

New strategy :

Stand aside

Position : -

Target : -

Stop : -

Despite falling initially to 108.84 earlier today, the subsequent rebound suggests decline is not ready to resume yet and further consolidation is in store, hence risk of another bounce to 109.55-60 is seen, however, reckon resistance at 109.83 (yesterday’s high) would hold and bring retreat later. Only a break of 109.83 would signal low has been formed at 108.60 earlier, bring further gain to 110.00 and later towards previous resistance at 110.37.

On the downside, below 109.00 would bring test of 108.84 but only break of said support at 108.60 would revive bearishness and confirm recent decline has resumed for further weakness to 108.30 (1.618 times projection of 110.95-109.67 measuring from 110.37), then towards 108.00. As near term outlook is still mixed, would be prudent to stand aside in the meantime.