Sample Category Title

Technical Outlook: WTI Oil – Bullish N/T Outlook But 20SMA Caps For Now

WTI oil is trading in consolidation mode on Thursday following strong rally on Wednesday after US crude stocks report showed further fall in inventories by 3.3 million barrels. Oil price rallied over 1% on Wednesday and hit high at $48.48. South-turning 20SMA limited action and acting as initial resistance at $48.56, marking pivotal resistance zone with former highs and double-rejection at $48.72 and Fibo 61.8% of $50.41/$46.44 downleg at $48.89. Daily studies are bullishly aligned and keep focus at the upside for eventual attack at $48.56/89 zone. Meantime, corrective easing should stay above $48.74 (converged 10/100 SMA's) to keep near-term bulls in play. Increased downside risk could be expected on break here that would re-expose strong support $47.01 (daily cloud top).

Res: 48.56, 48.72, 48.89, 49.14

Sup: 48.00, 47.52, 47.35, 47.01

Euro And Dollar Seek Guidance From Jackson Hole

Thursday August 24: Five things the markets are talking about

The majority expect ECB's Draghi to refrain from talking about the timing of exit from ultra-loose monetary policy at the Kansas City Fed's Jackson Hole symposium, which starts today, however, it is still worthwhile watching out for news as the three day annual meet of G10 central bankers is always good for a surprise or two.

The ‘mighty' U.S dollar is finding it difficult to gain meaningful traction over the past couple of sessions as investors digest U.S political uncertainty ahead of important speeches from central bankers – both the Fed's Yellen and ECB's Draghi take center stage tomorrow – President Trump threatened on Tuesday night to shut down the government to secure funding for a wall on the Mexican border and even raised doubts about a new NAFTA deal being reached.

Ms. Yellen is scheduled to speak about financial stability at 10 am EDT Friday, while ECB's Draghi is set to give a speech at 3 pm EDT.

1. Stocks mixed results

In Japan, the Nikkei (-0.4%) share average fell to a four-month low overnight, dragged down by stateside losses and a stronger yen. The broader Topix index fell -0.5%.

In South Korea, the Kospi index increased +0.4%, while down-under, Australia's S&P/ASX 200 Index added +0.1%.

In Hong Kong, the Hang Seng Index rallied +0.5% as the market reopened after being shut on Wednesday, supported by robust gains in financial and property stocks.

In China, stocks fell the most in nearly two-weeks on Thursday, as China Unicom tumbled after rallying earlier in the week as excitement over state enterprise reforms cooled. The blue-chip CSI300 index fell -0.6%, while the Shanghai Composite Index lost -0.5%.

In Europe, indices are trading a tad higher in light summer trade with cyclicals' helping many European names rise.

U.S stocks are set to open in the black (+0.1%).

Indices: Stoxx600 +0.4% at 375.5, FTSE +0.3% at 7407, DAX +0.3% at 12211, CAC-40 +0.4% at 5133, IBEX-35 +0.5% at 10391, FTSE MIB +0.8% at 21800, SMI +0.1% at 8964, S&P 500 Futures +0.1%

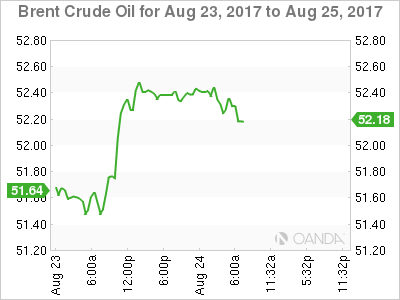

2. Oil steady as storm heads into Gulf of Mexico

Ahead of the U.S open, oil prices are steady, holding on to most of their recent gains after another fall in U.S crude inventories yesterday indicated a tighter market. Also supporting prices is the threat of a tropical storm heading towards oil producing facilities in the Gulf of Mexico.

Brent crude is down -5c at +$52.52, while U.S light crude (WTI) is also -5c lower at +$48.36 a barrel.

Note: Both contracts had rallied more than +1% yesterday, supported by potential output disruptions from the Gulf of Mexico storm Tropical Depression Harvey. Operators in the area are already closing down platforms for precautionary measures.

U.S crude oil production hit +9.53m barrels bpd last week; it's highest since July 2015 and is up over +13% from their most recent low in mid-2016.

Despite elevated production levels, EIA data yesterday showed that U.S crude stocks fell last week and that gas stocks were also down – crude inventories fell by -3.3m barrels in the week ending Aug. 18 to +463.17m barrels, down -13.5% from March's record levels.

Note: OPEC is to hold a joint OPEC, non-OPEC Joint Ministerial Monitoring Committee (JMMC) meeting on Sept 22 – All options will be on the table including production cuts and extension of current agreement. Planning to invite Nigeria and Libya to meeting.

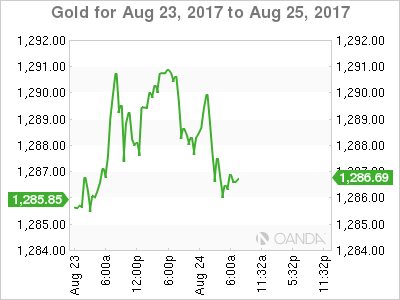

Gold prices have nudged lower overnight, giving up some of its gains made after President Trump's threat of a government shutdown. Spot gold is down -0.2% at +$1,287.21 an ounce. The market is focused on Jackson Hole rhetoric.

3. Yields trade a tight range ahead of central bank meet

Yesterday, Canadian bonds ended a recent losing streak as fixed-income prices rose amid growing uncertainty on the future of Nafta following comments made by Trump.

The yield for Canada's two-year bonds fell -2 bps to +1.259%, while 10-year product was -4 bps lower at +1.883%. Canadian fixed-income continues to underperform U.S Treasury's amid ongoing muted summer trading conditions on the broader market.

U.S debt prices also rallied Wednesday, as combative rhetoric from President Trump this week pressured equities while fuelling demand for assets seen as a safe haven. The yield on U.S 10-year notes is at +2.185%, down from Tuesday's pre speech levels of +2.215%.

Elsewhere, Germany's 10-year Bund yield rallied +1 bps to +0.38%, the first advance in more than a week, while the U.K's 10-year Gilt yield increased +2 bps to +1.074%.

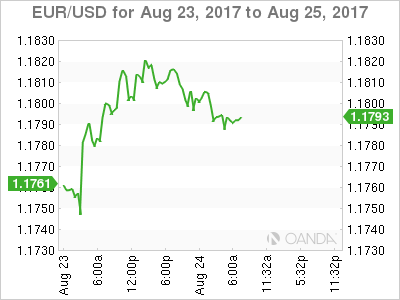

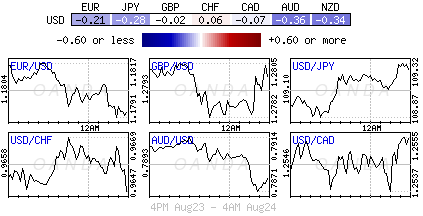

4. Dollar flounder ahead of Yellen's speech Friday

The EUR (€1.1790) has extended its gains outright, helped yesterday by data showing that U.S new-home sales fell sharply in July and by a provisional eurozone PMI survey on manufacturing activity that beat expectations.

Improvements in the eurozone economy, combined with heightened political uncertainty in both the U.S and the U.K will continue to support the single unit on pull backs – EUR/GBP continues to trade north of the psychological €0.92 handle.

Draghi's Jackson Hole speech is being seen as a potential mover as it will have more impact as it relates directly towards monetary policy. Consensus believes ‘no' changes are expected in the QE measures, however attention will be paid to any remarks on the EUR's strength.

Sterling (£1.2800) remains under persistent pressure, driven by concerns about Brexit, while USD/JPY (¥109.32) trades within a tight 120-pip range over the week heading into Jackson Hole conference. Any USD strength has been countered by geopolitical risk as U.S/South Korea continues their war exercises.

Bullish bets on the Chinese yuan are maintained at three-year highs. The currency has gained about +4.1% outright this year, supported by the People's Bank of China (PBoC) guidance of the daily trading band and controls on capital outflows.

5. U.K business investment slows as Brexit fuels uncertainty

Data this morning showed that U.K business investment slowed and posted no growth in Q2 – a sign that uncertainty linked to Brexit negotiations and June's general election may have weighed on firms' long-term plans.

Capital spending by businesses was unchanged compared with the preceding quarter, as well as the corresponding quarter of 2016, standing at +£43.8B.

U.K Ministers have suggested the U.K will seek a “transition agreement' to give businesses time to adapt, but mixed signals on the shape of such a deal have kept companies on edge.

Other data showed that U.K GDP data for Q2 expanded by +0.3% on the quarter, a slight improvement on the +0.2% seen in Q1. It was in line with expectations and on an annualized basis; the U.K economy grew by +1.2%. Household expenditure and government spending drove Q2 expansion.

Equities Pare Losses as Jackson Hole Gets Underway

- Equities recover from Trump-related declines;

- Jackson Hole gets underway but key speeches don’t come until Friday;

- UK growth softens as consumer and business spending slows.

US equity markets are poised to open higher on Thursday, paring Wednesday’s losses which came on the back of Donald Trump’s NAFTA and government shutdown warnings.

The short-term nature of the declines is probably a good reflection of how seriously people are taking Trump’s latest threats. We often see a knee jerk reaction to such negative remarks but the fact that we’re already pushing higher a day later suggests people don’t expect either to happen. Of course, should it become apparent that he will follow through on them then it will likely be a different story altogether.

Barring any political or geopolitical distractions, focus will likely now shift to the week’s main event, Jackson Hole. In what has otherwise been a very slow week for markets – as it typically the case at this time of year – this gathering of central bankers, policy experts and academics was always the standout event that could trigger some market volatility.

Unfortunately, we’ll have to wait until tomorrow for the highlight of the event, appearances from Federal Reserve Chair Janet Yellen and ECB President Mario Draghi. With both central banks on the cusp of making new policy announcements, their views will be poured over for the slightest hints. Markets don’t seem overly concerned about the Fed’s balance sheet plans so interest rate clues is what people will be looking for, whereas with ECB, it’s all about tapering. When will it happen, how much will it be and how long will it last.

On the data side, it’s once again looking a little quiet. We had second quarter GDP data from the UK this morning which painted a rather grim picture of the economy. Consumer spending – a key component of the UK economy – slowed once again as households continue to feel the squeeze of negative real wage growth while business investment stagnated. It’s clear that while the economy has not nose-dived, it is suffering in the aftermath of the Brexit vote. The pound fell initially after the data but quickly recovered to trade off it’s lows just below 1.28 against the dollar. The pair remains under pressure though and should this support break, 1.26 could be on the cards.

There’s a couple more pieces of data still to come from the US today including existing home sales for July, weekly jobless claims and mortgage delinquencies

Technical Outlook: AUDUSD – Bears Found Footstep At Fibo 61.8% Support At 0.7866

The Aussie hit fresh low at 0.7866 on Thursday in extension of pullback from 0.7950, retracing 61.8% of 0.7807/0.7962 upleg.

Fresh weakness on Thursday marks the third straight day in red that broke below daily Tenkan-sen (0.7885).

Subsequent bounce from 0.7866 returned above cracked Tenkan-sen signaling hesitation at pivotal supports. Bears need close below both points to generate fresh signal for further easing.

Mixed signals on daily chart (conflicting MA’s / RSI / slow stoch in neutrality zone and negative momentum studies) do not provide clear direction signal, but bearishly aligned near-term tech keep focus at the downside.

Sustained break below 0.7866 to expose key near-term support at 0.7807, while lift above 0.7916 /25 (20SMA / bear-trendline off 0.8065) would shift near-term focus higher.

Res: 0.7916, 0.7925, 0.7950, 0.7962

Sup: 0.7885, 0.7866, 0.7844, 0.7807

CRUDE OIL Holding Below The 200-DMA And Above 50-DMA

Crude oil is trading mixed. Hourly support is given at 46.46 (17/08/2017 high). Strong resistance can be found at 50.41 (31/07/2017). Expected to show continued short-term sideways move.

In the long-term, crude oil has recovered after its sharp decline last year. However, we consider that further weakness are very likely. Strong support lies at 35.24 (05/04/2016) while resistance can now be found at 55.24 (03/01/2017 high).

SILVER Consolidation Before Another Leg Higher

Silver's bullish pressures are on despite ongoing consolidation. Hourly resistance is given at 17.32 (18/08/2017 high) while support can be found at 16.58 (15/08/2017 high). The commodity lies in a short-term uptrend channel. Expected to show another leg higher.

In the long-term, the death cross indicates that further downsides are very likely. Resistance is located at 25.11 (28/08/2013 high). Strong support can be found at 11.75 (20/04/2009).

GOLD Consolidating Below 1300

Gold has broken strong resistance given at 1296 (06/06/2017 high) before bouncing lower. Hourly support is given at 1251 (08/08/2017 low). Stronger support lies at 1204 (10/07/2017 high). Expected to show continued consolidation below $1300.

In the long-term, the technical structure suggests that there is a growing upside momentum. A break of 1392 (17/03/2014) is necessary ton confirm it, A major support can be found at 1045 (05/02/2010 low)

BITCOIN Buying Pressures Increase

Bitcoin is pausing after the massive surge over the past few days. Resistance is at all-time high at 4480 (17/08/2017 high). Hourly support lies very far at 2403 (26/07/2017 low). The road is wide open for another bullish move.

In the long-term, the digital currency has had an exponential growth. There are decent likelihood that the asset will consolidate above $1500. Long-term support is given at $1464 (04/05/2017 low).

EUR/CHF Buying Pressures Are Up

EUR/CHF's volatility is important. Hourly support is located at 1.1260 (04/08/2017 low). Expected to show further consolidation.

In the longer term, the technical structure has reversed. Strong resistance at 1.1200 (04/02/2015 high) has been broken. Yet,the ECB's QE programme is likely to cause persistent selling pressures on the euro, which should weigh on EUR/CHF. Supports can be found at 1.0184 (28/01/2015 low) and 1.0082 (27/01/2015 low).

EUR/GBP Continued Increase

EUR/GBP is trading around its highest levels of the year. Hourly resistance at 0.9415 (07/10/2017 high) has been broken. Hourly support is given at 0.9160 (16/06/2017 low). Downside risks are nonetheless important.

In the long-term, the pair has largely recovered from recent lows in 2015. The technical structure suggests a growing upside momentum. The pair is trading above from its 200 DMA. Strong resistance can be found at 0.9500 psychological level.