Sample Category Title

Trade Idea: EUR/GBP – Buy at 0.9115

EUR/GBP - 0.9213

Original strategy :

Buy at 0.9115, Target: 0.9215, Stop: 0.9075

Position : -

Target : -

Stop : -

New strategy :

Buy at 0.9115, Target: 0.9215, Stop: 0.9075

Position : -

Target : -

Stop : -

As the single currency has eased after faltering below yesterday’s high at 0.9237, suggesting minor consolidation below this level would be seen and pullback to 0.9150-55 cannot be ruled out, however, reckon support at 0.9111 would contain downside and bring another rise later, above said resistance at 0.9237 would add credence to our bullish view that recent upmove is still in progress and may extend further gain to 0.9250 but weakening of near term upward momentum should prevent sharp move beyond 0.9270-75 and price should falter below 0.9300-05, risk from there has increased for a retreat to take place later.

In view of this, would not chase this rise here and would be prudent to buy euro on subsequent pullback as 0.9110-15 would limit downside. Below 0.09090 would defer and suggest a temporary top is possibly formed, risk test of support at 0.9063, however, break there is needed to add credence to this view, bring retracement of recent upmove towards 0.9005-10.

Our preferred count is that, after forming a major top at 0.9805 (wave V), (A)-(B)-(C) correction is unfolding with (A) leg ended at 0.8400 (A: 0.8637, B: 0.9491 and 5-waver C ended at 0.8400. Wave (B) has ended at 0.9413 and impulsive wave (C) has either ended at 0.8067 or may extend one more fall to 0.8000 before prospect of another rally. Current breach of indicated resistance at 0.9043 confirms our view that the (C) leg has ended and bring stronger rebound towards 0.9150/54, then towards 0.9240/50.

USD Paralyzed ahead of Jackson Hole

- EMU equities are modestly higher, with Italian and Spanish bourses outperforming, as investors take comfort from yesterday's price action on WS. US equities open little changed.

- UK Q2 GDP growth was confirmed at 0.3% Q/Q and 1.7% Y/Y. However, the details painted a poorer picture. Indeed, consumption barely grew (0.1% Q/Q) as high inflation limits the spending capacity of households. It was partly offset by strong government and capital spending. However, the former is untenable given budget constraints. The latter was due to government and housing investment, as business investment was flat.

- UK retailers this month reported their worst month of growth since the Brexit vote, according to a CBI survey, a negative sign for the economy. CBI retailing reported sales index fell to -10 in August from 22 in July. It compares to expectations for a more modest decline to 14.

- INSEE reported that French business confidence continued to improve in August to reach its highest level since April 2011, underscoring recent upbeat data in the eurozone's second largest economy.

- Norway's "mainland" economy, which excludes oil, gas and transport, expanded by 0.7 Q/Q in Q2, while Q1 figures were also revised upwards from 0.6 % Q/Q to 0.7% Q/Q. Statistics Norway said it represents a "moderate economic upturn" after two and a half years of "weak growth". NOK surged, pushing EUR/NOK to the key 9.2521 support.

- European markets traded quiet ahead of the start of Jackson Hole with bond investors making their positions more neutral from dovish. That resulted in modestly higher yields. The dollar was slightly stronger versus yen and euro.

- Kansas Fed George said if U.S. data hold up, there will be an opportunity to raise interest rates again in 2017. She admitted that eco models of how inflation responds to low unemployment may have broken down, but "whether we hit 2 percent on the nose is less important to me than understanding how the economy is doing more generally."

- Hungary's central bank doubled down on its pledge to consider more unconventional easing, moving closer to further action to stem a currency rally. The forint retreated from a two-year high. EUR/HUF rose to 304.55 from 302.

- Dallas Fed Kaplan repeated that he wants to be patient on a rate hike and prefers to wait for more information amongst other about how inflation evolves. He also repeated that the balance sheet tapering should start soon.

Rates

Core bonds lose marginal ground ahead of JH

Core bonds traded with a slight negative bias as the risk sentiment improved, following Trump-related market upheaval on Wednesday. Some more neutral positioning ahead of the Jackson Hole jamboree of the world's top central bankers may have played a role too. However, German bonds are little changed, while US Treasuries are modestly lower. At the time of writing, US yields are up 1.7 to 2.4 bps, the belly of the curve underperforming. Yield changes in the German curve were minimal (less than 1 bp lower).

French business confidence (INSEE survey) confirmed the upbeat mood of corporates, while Belgian business confidence disappointed and US initial claims in line with expectations. All releases were ignored and thus disregarded.

Calmness on the intra-EMU market returned after a widening of the peripheral yield spreads in the past two days. Yield spreads were nearly unchanged. The better risk sentiment played a role, which is also documented by the outperformance of the Milan and Madrid bourses.

Currencies

USD paralyzed ahead of Jackson Hole

The dollar was little changed against the euro and regained marginally ground against the yen as the negative impact from Tuesday's comments of president Trump faded. Even so, price moves remained limited. It was all marking time ahead of tomorrow's Jackson Hole speeches. EUR/USD holds near the 1.18 pivot. USD/JPY is trading a touch higher around 109.30/40.

Overnight, Asian equities mostly showed modest gains with Japan and China being the exception. ECB's Hansen, a hawk, wasn't overly worried about recent euro strength, but his comments didn't cause any further euro gains. EUR/USD stabilized in the 1.18 area. USD/JPY held in the low 109 area. So, the 108.60 ST correction low 'survived' the unconventional Trump comments.

European markets enjoyed a cautious risk-on environment. The comments from US president Trump on Nafta and on a government shutdown moved gradually to the background. There were only second tier eco data in Europe. Core bond yields rose marginally, equities rebounded and the dollar was slightly better bid. EUR/USD drifted (temporary) below 1.18. USD/JPY rebounded a bit further from the 109 barrier. However, all moves developed within recent tight ranges. Changes in interest rate differentials were too small to guide for FX trading.

No change of script for global trading in the US session. EUR/USD reversed the morning 'gain' and returned to the 1.18 area. We didn't seen a specific reason.US weekly jobless claims were in line with expectations and evidently couldn't affect the dollar ahead of tomorrow's Jackson Hole speeches. EUR/USD is trading just below 1.18. USD/JPY is changing hands around 109.30/40.

Sterling decline takes a breather despite poor data

Today, the longstanding decline of sterling (against the euro) finally took a breather. EUR/GBP came slightly off the recent top around 0.9235. Cable returned north of 1.28. The UK data couldn't explain the pause in the sterling decline, as the UK data disappointed (see headlines for details). There was no high profile news from the Brexit negotiations. Immigration data indicated that net migration to the UK fell significantly in the year to March. Whatever, the market apparently found itself a bit too much sterling short and needed some corrective action. EUR/GBP trades currently in the 0.92 area. Cable is changing hands in the 1.2820 area. Today's move didn't change the global technical picture for the UK currency though.

The Contenders: Prospects for the Next Fed Chair

Executive Summary

Trying to guess the next Fed Chair is something between a parlor game and a fire drill. Both involve conjecture and speculation but only one is a useful exercise and even then, only marginally so. In the roughly five months between now and the end of Chair Yellen's term on February 1, 2018, much can change, but we would be remiss not to keep you up to speed on the contenders for the job and the difference the potential change in leadership could bring. If we do get a new Fed Chair, it would be only the third changing-of-the-guard since 1987.

The current Fed Chair, Janet Yellen, could still be at the wheel, but her grip has been loosening in recent weeks. A poll conducted by the National Association for Business Economics puts Yellen's odds of re-nomination at less than one in five.1 President Trump economic adviser Gary Cohn is at the top of the alternate list.

The most important consideration we stress to clients when asked about who will be the next Fed Chair and what it will mean is this: the Fed is an institution. There are more than 300 Ph.D. economists employed by the Federal Reserve Board and each brings their own analysis and viewpoint regardless of who holds the title of Chair. The 12-member Federal Open Market Committee (FOMC) comes to its decisions by consensus, not by edict.

This special report offers an introduction to the various contenders for the top job at the Fed. Any credible Fed Chair candidate would not meaningfully alter the market outlook or our baseline forecasts for GDP growth, interest rates or the dollar in an immediate way. That said, the Fed Chair can often come to symbolize the institution he or she represents and in that capacity command a degree of power and influence over time. On that basis, we offer these thoughts on who might hold the job come February 2, 2018.

The Current Fed Chair in Context

While the Chair of the Federal Reserve is appointed to a four-year term by the President of the United States, a Chair can be appointed to several consecutive terms. When Alan Greenspan finished his final term in 2006, a whole generation had started a career in finance knowing no other Fed Chair than the Maestro. Though Mr. Greenspan served at the pleasure of four presidents, he was not the longest serving. That distinction goes to William McChesney Martin Jr., a veteran of the Second World War whose formal degree was in Latin and English rather than finance or economics, who served from 1951 to 1970.

Chair Yellen's term is due to expire in just over five months on February 1, 2018. She may be appointed to another term, but, at that point, her four years on the job would place her years of service about average in terms of duration compared to past Fed Chairs (that is, if we exclude the longer terms of service of Mr. Martin and Mr. Greenspan from the calculation).

Judging by the numbers, the first female head of the world's largest central bank has made significant progress in meeting the Fed's dual mandate. From the start of Chair Yellen's term in February 2014, PCE inflation has averaged 1.1 percent, core PCE averaged 1.6 percent, the unemployment rate has averaged 5.2 percent and the average quarterly pace of GDP growth has been 2.4 percent.

Admittedly the pace of inflation was well-below the Fed's 2.0 percent target, but throughout her tenure, the United States has sidestepped outright deflation for the most part. The Fed's preferred measure of inflation, the PCE deflator, never went negative on a year-over-year basis; headline CPI did briefly dip below zero.

The same cannot be said for many of the world's other large developed economies that did grapple with outright declines in consumer prices during the same period. The European Central Bank, the Bank of England and the Bank of Japan all experienced outright deflation in the form of negative year-over-year rates of CPI inflation in those economies.

Do You Think It Matters Who Sits on the Iron Throne?

As we noted in the introduction to this report, there is a lot that can change in the roughly five months between now and the end of Chair Yellen's term and this will certainly not be the last thing that passes your desk on the subject of who will be next to lead the Fed.

As a preamble to the discussion of possible Fed replacements, we would underscore the point that the most important consideration in the context of this topic is that the Fed is an institution. The rate-setting and policy-making FOMC has 12 members, seven from the Board of Governors (which includes the Chair) and five presidents of the Regional Banks (four of those seats rotate, the president of the New York Fed has a permanent seat). The most significant observation we can offer about the new Fed Chair, whoever that may be, is that person will preside over a group that is consensus-driven with a very specific dual mandate to promote price stability and maximum employment. On that basis, any credible Fed candidate would not meaningfully alter the market outlook for our baseline forecasts for GDP growth, interest rates or the dollar.

Top Contenders

That said, the selection itself may not have an immediate influence on financial markets but the Fed Chair can often come to symbolize the institution he or she represents and, in that capacity, command a degree of power and influence over time. On that basis, we offer these thoughts on who might hold the job come February 2, 2018.

The Incumbent: "Not Toast"

Although her term is due to expire in just over five months, the notion that Chair Yellen may yet be appointed to another term should not be dismissed out of hand. Although the president has been hot and cold on the current Fed Chair, there are few examples of subjects on which his public statement do not contradict. After acknowledging his respect for her in an April interview, the president, offering his assessment of Chair Yellen's long-term prospects at the Fed, said that she was "not toast."

As we have already demonstrated, Chair Yellen is a known entity in the role. We are not offering an endorsement, but it has not been uncommon for a sitting president to re-nominate a Fed Chair appointed by a prior president, even when the prior president was from the other party. Fed Chair Bernanke was first appointed by President Bush, a Republican, but stayed on at the request of President Obama, a Democrat. Still the prospects are not overwhelming for the sitting Chair. A National Association of Business Economics (NABE) poll of economists put the odds of another Yellen term at the Fed at 17 percent.

The Odds-on Favorite: I Scream Cohn

In another Wall Street Journal interview near the end of July, the president affirmed that Yellen remained in contention to hold the job even as he acknowledged that his economic adviser, Gary Cohn, was also a top-contender along with "two or three" others he chose not to name.2 The same NABE poll mentioned above put Cohn at the top of the short list with 49 percent of respondents selecting him as the next to lead the Fed if Yellen were not the nominee.

At an Institute of International Finance conference in March 2016, then Goldman Sachs President and COO Cohn downplayed the importance of central bank guidance, saying, "In some respects, if central banks would go back to being central banks, and really worry about what's going on in the economy and do what they think they need to do, instead of spending all their time talking about what they're going to do, we'd probably all be in a lot better position."3 Cohn later added that if all the world's central banks "raised interest rates by 300 basis points, the world would be a better place."

Gary Cohn embraces a more market oriented approach to economic policy, rather than the current academic approach in place by Chair Yellen. Although Cohn doesn't fit the traditional mold of a Fed Chair, his lack of formal economics training might not be as disconcerting as it would be in another candidate due to his extensive experience on Wall Street and more than 25 years working in finance. On that basis, as Chair of the Federal Reserve, Cohn's approach would be less academic and more market-focused.

The Best Longshot: Mr. Conventional

The best "longshot" pick may be Kevin Warsh, who picked up 9 percent of the votes in the NABE poll of most likely nominees other than Yellen. If Gary Cohn is the unconventional choice, Warsh is Mr. Conventional. After four years of working in various economic roles in the George W. Bush administration, then President Bush appointed Warsh to fill a vacancy on the Fed's Board of Governors where he served from 2006 until 2011. A Republican, Mr. Warsh now serves as a visiting fellow at Stanford's Hoover Institution. President Trump's well-known affinity for low rates could be seen as being at odds with Warsh's somewhat hawkish tendencies for which he was known in his time at the Fed, but he would otherwise fit the bill for a candidate that checks all the boxes for the president.

Other Possibilities

Another potential, but less likely candidate, is Stanford Economics Professor John Taylor, whose eponymous "Taylor Rule" presents a formulaic approach to economic policy, implying with each one-percent increase in inflation, a central bank should raise the nominal interest rate by more than one percentage point. Coincidentally, Mr. Taylor and Mr. Warsh are both fellows at the Hoover Institution.

Glenn Hubbard is the current Dean at Columbia's Business School and a professor of economics there. He previously served as Deputy Assistant at the Treasury in the 1990s. In another example of the small world of economics, Mr. Hubbard and Mr. Warsh worked together for a stretch in the early 2000s when Mr. Warsh was Special Assistant to the President for Economic Policy and Mr. Hubbard was the Chairman of the President's Council of Economic Advisers.

With Monetary Policy, Fed Chair Will Have to Keep an Eye on Fiscal Policy

In addition to managing the fed funds rate, the next Chair of the Federal Reserve will also need to oversee the unwinding of the Fed's roughly $4.5 trillion balance sheet. There are a number of Republican members of Congress who would like to see the Fed get out of the housing market and unwind some or all of its $1.8 trillion portfolio of MBS and agencies. In many instances, these are members of Congress who also place a high value on balancing the federal budget.

Without making a value judgement about whether or not the Fed "should" maintain a large balance sheet, the Fed's large holdings currently help reduce the budget deficit. In an environment of rising deficits and policy proposals for which finding the funding is often a major challenge, reduced remittances to the Treasury cannot be ignored. As illustrated in Figure 5, Fed earnings remitted to the Treasury over the past 12 months add up to roughly $85 billion. Without those remittances, last year's fiscal budget deficit would have been 16 percent larger.

Furthermore, despite a debt-to-GDP ratio that has doubled since the Great Recession began, net interest costs as a share of GDP have remained historically low (Figure 6). With monetary policy tightening likely driving interest rates higher, this represents yet another way in which monetary policy can influence the fiscal side of the economic policy equation.

In a May interview on Bloomberg, Mr. Warsh weighed in on precisely this dynamic, saying, "The sooner they (Fed policy-makers) come out with principles, the easier markets can adjust and, importantly, the easier the Treasury can know what their issuance calendar should be. We are all part of one government."

Conclusion

To reiterate our view, any credible Fed Chair candidate would not meaningfully alter the market outlook or our baseline forecasts for the economy, the path of interest rates or the value of the dollar. That said, the Chair of the Fed can often come to symbolize the institution he or she represents and in that capacity, command a degree of power and influence over time.

Ms. Yellen would signal convention and continuity. Mr. Cohn would be a somewhat unconventional pick inasmuch as he is not a formally trained economist, but then neither was the longest-serving Fed Chair, William M. Martin Jr. Additionally, Mr. Cohn's extensive experience in finance deflects the criticism of his academic credentials. Mr. Warsh is the most likely of the "longshots" and would also represent a conventional pick with his experience at the White House, at the Fed and more traditional academic credentials.

The Fed has lowered its estimates of what it considers the appropriate level for the fed funds rate in the longer-run from 4.25 percent in 2012 to 3.0 percent today.5 The ultimate terminal fed funds rate will likely be lower when the current cycle comes to an end than it has been in prior economic cycles. With limited scope for the Fed to cut rates when the next recession comes along, whenever that may be, the Fed may have to go back to the well of quantitative easing. This could entail resuming reinvestments or even returning to asset purchases, depending on what economic conditions warrant.

Normalization of the Fed's balance sheet is an important consideration for the next Fed Chair as well. Monetary policymakers will be challenged to find a balanced path that begins the process of unwinding years of unconventional monetary policy while simultaneously keeping the economic expansion chugging along. The various scenarios considered in this report are offered to help decision-makers frame their thinking and make informed decisions as this process unfolds.

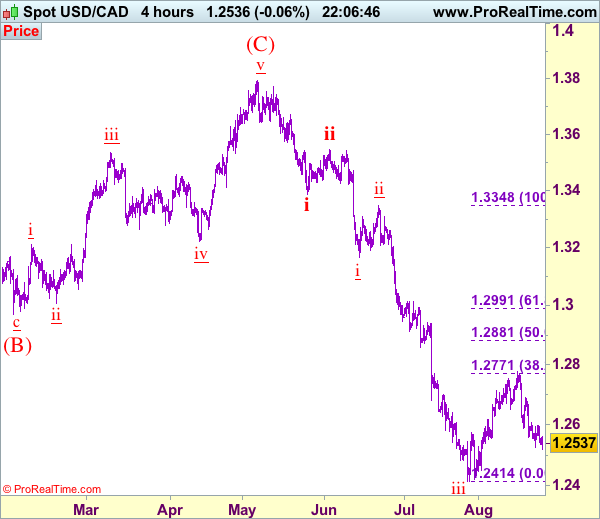

Trade Idea: USD/CAD – Hold short entered at 1.2690

USD/CAD - 1.2539

Trend: Down

Original strategy :

Sold at 1.2690, Target: 1.2490, Stop: 1.2610

Position: - Short at 1.2690

Target: - 1.2490

Stop: - 1.2610

New strategy :

Hold short entered at 1.2690, Target: 1.2490, Stop: 1.2610

Position: - Short at 1.2690

Target: - 1.2490

Stop:- 1.2610

As the greenback has slipped again after faltering below indicated resistance at 1.2607, retaining our bearishness for the fall from 1.2778 top to extend weakness to 1.2490-00 but a sustained breach below there is needed to signal the wave iv correction from 1.2414 (wave iii trough) has ended at 1.2778, bring further fall towards support at 1.2451 which is likely to hold on first testing. We are keeping our count that wave v as well as wave (C) ended at 1.3794 and impulsive wave (i ii, i ii) is now unfolding with minor wave iii possibly ended at 1.2414, hence wave iv correction is underway.

In view of this, we are holding on to our short position entered at 1.2690. Only above said resistance at 1.2607 would defer and prolong consolidation, risk rebound to 1.2660 but resistance at 1.2691 should hold from here, bring further consolidation. Above 1.2691 resistance would risk a stronger rebound to 1.2740-50, however, said resistance at 1.2778 should hold. In the event the pair breaks said resistance at 1.2778, this would abort and signal the rebound from 1.2414 is still in progress for retracement of recent decline to 1.2825-30 but still reckon upside would be limited to 1.2880-85 (50% Fibonacci retracement of wave iii) and price should falter well below 1.2990-95 (61.8% Fibonacci retracement), bring retreat later.

To recap, wave B from 1.3066 is unfolding as an a-b-c and is sub-divided as a: 1.2192, b: 1.2716 and wave c is a 5-waver with i: 1.1983, ii: 1.2506, extended wave iii with minor iii at 1.0206, wave iv ended at 1.0781 and wave v as well as wave iii has ended at 0.9931, hence the subsequent choppy trading is the wave iv which is unfolding as (a)-(b)-(c) with (a) leg of iv ended at 1.0854, followed by (b) leg at 1.0108 and (c) leg as well as the wave iv ended at 1.0674. The wave v is sub-divided by minor wave (i): 0.9980, (ii): 1.0374, (iii): 0.9446, (iv): 0.9913 and (v) as well as v has possibly ended at 0.9407, therefore, consolidation with upside bias is seen for major correction, indicated target at 1.3700 and 1.4000 had been met and further gain to 1.4700 would be seen later.

Capitol Hill Update: Fall Legislative Preview

Executive Summary

Congress returns from its August recess Tuesday, September 5 with a long to-do list of legislative deadlines, including lifting the debt ceiling, funding the government beyond the end of September, reauthorizing a number of federal programs and passing a budget resolution to serve as the vehicle for changes to tax law. For the House of Representatives, there are just 12 scheduled legislative days in September to accomplish the to-do list. In this slightly longer edition of the Capitol Hill Update, we outline the legislative calendar and provide our views on how we believe federal fiscal policy will unfold in the month ahead.

Our expectation is that the debt ceiling will be lifted before the projected September 29 deadline. Given the need for a bipartisan vote in the Senate to lift the borrowing limit, we expect the debt ceiling will be suspended for a period of time without being tied to budget cuts or other policy changes. The federal funding bill will also require bipartisan support and thus we expect Congress will enact a continuing resolution that maintains this fiscal year's funding levels through the beginning/middle of December, buying policymakers more time to work toward a solution for the remainder of the fiscal year. While tax reform discussions will be ongoing, we do not expect any major developments until late October or early November due to the numerous other pressing legislative priorities and the need to first pass a budget resolution.

Debt Ceiling: Will There Be Strings Attached?

One of the biggest concerns among market participants is the need to lift the nation's borrowing limit. Back in 2011, a down-to-the-wire vote resulted in volatile financial markets and a credit rating downgrade of U.S. sovereign debt. During this round of the debt ceiling debate, there have been demands by some fiscally conservative members of the House of Representatives to cut nondefense spending in exchange for lifting the debt ceiling. Other members of Congress have balked at this approach, preferring to pass a "clean" debt ceiling bill that does not tie the borrowing limit to other legislative items.

Given the fact that at least eight Democrats will need to join with Republicans in the Senate to advance the bill, it will require a bipartisan effort to raise the debt ceiling. A key question surrounding the debt ceiling debate is whether Democrats will demand concessions from Republicans to gain their votes. If fiscally conservative members begin to abandon ship in droves and Republican leadership must lean heavily on Democratic votes to pass a debt ceiling increase, it may empower the minority party to try to extract a hefty price from the party in power. If this was to occur, it would put Republican leadership in an awkward place; short of the necessary votes, and stuck between two sides both demanding concessions for their critical block of votes. The probability of a major market moving event in this case would likely increase, and we will be watching closely in the weeks ahead for signs that events are unfolding along this path.

Our view is that a "clean" debt ceiling bill with no other policy changes or budget cuts attached will be passed. There are just 12 legislative days scheduled in the House of Representatives before the September 29 deadline, suggesting that both the House and Senate must move quickly toward passage, limiting the ability to have a long, drawn out debate over other policy changes.1 This "clean" debt ceiling bill is likely to suspend the borrowing limit as has been done frequently in the recent past as opposed to increasing the borrowing limit to a specific dollar amount.

Federal Funding: Expect the Can to Be Kicked

The next major issue to tackle is funding the federal government beyond September 30. Should Congress fail to pass a funding bill, the result would be a partial federal government shutdown. In the case of a partial shutdown, the President's Office of Management and Budget would develop a plan to determine which federal employees would be affected through furlough. The most likely outcome given the very short timeline entails passing a continuing resolution (CR) that funds the government through the first or second week in December. Once again, the CR will require at least eight Democrats to join with Republicans to keep the government functioning. This CR will likely carry over funding from the current 2017 fiscal year to keep the bill bipartisan and hopefully noncontroversial. We believe policymakers will likely turn to a shortterm patch because the regular appropriations process has been delayed as policymakers have grappled with other legislative items and difficult questions remained unresolved. Thus far, Republicans have pursued an aggressive expansion of defense spending while keeping nondefense spending more or less flat. Budget agreements over the past few years have often led a more bipartisan approach that provides bumps in funding to both defense and nondefense discretionary spending. If Democrats refuse to play ball in the Senate on a budget that abandons this balanced framework, or if a fight erupts over controversial budget items such as funding for a border wall, the appropriations process would likely continue to face major roadblocks throughout the fall.

Kicking the can to December will buy more time for a longer-term funding bill to be worked out in the remaining months of the year and allow Congress to turn to the other legislative deadlines it is facing in September, including the need to reauthorize the Federal Aviation Administration, the National Flood Insurance Program and the Children's Health Insurance Program. Historically, reauthorizing these programs has at times been controversial and time consuming, requiring several weeks of debate to find solutions. This time around, we would not be surprised if these programs' authorizations are also extended for a short period to buy time for continued negotiations and more comprehensive legislation.

What about Tax Reform?

Given the multiple legislative deadlines facing Congress in September, as well as the fact that Republicans still need to pass a budget resolution before moving on to tax reform, we do not expect much progress on tax legislation until October or November. As we have described in previous pieces, the FY 2018 budget resolution is needed to proceed with the reconciliation process that will allow tax legislation to clear both chambers with a simple majority vote.2 Early signs are that the debate over a budget resolution could take some time. Fiscal conservatives in the House want more nondefense budget cuts, while more moderate members have resisted sharp cuts to nondefense discretionary and/or mandatory spending. Disagreements over balancing the budget/deficit size over the next decade have also plagued the budget resolution. For now, despite the optimistic rhetoric coming from Washington D.C. on taxes, we expect tax legislation will take a backseat in September to other more pressing federal fiscal policy items, such as the debt ceiling and government funding.

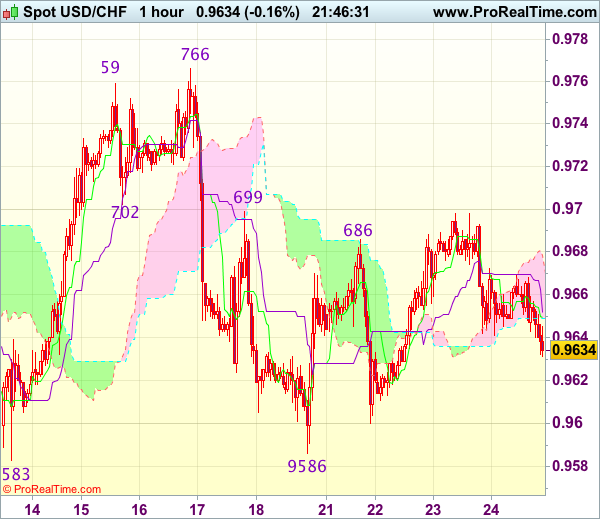

Trade Idea Update: USD/CHF – Hold long entered at 0.9620

USD/CHF - 0.962

Original strategy :

Bought at 0.9620, Target: 0.9720, Stop: 0.9585

Position : - Long at 0.9620

Target : - 0.9720

Stop : - 0.9585

New strategy :

Hold long entered at 0.9620, Target: 0.9720, Stop: 0.9585

Position : - Long at 0.9620

Target : - 0.9720

Stop : - 0.9585

Dollar’s retreat after faltering below resistance at 0.9699 suggests initial downside risk remains for marginal weakness, however, as long as support at 0.9586 holds, prospect of another rebound remains, above indicated resistance at 0.9699 would signal the retreat from 0.9766 has ended at 0.9586 last week and mild upside bias is seen for gain to 0.9720, then 0.9740, having said that, reckon resistance at 0.9766-73 would cap upside and bring further consolidation. Only a break of 0.9773 would retain bullishness and signal early rise from 0.9438 has resumed and extend gain to 0.9800.

In view of this, we are holding on to our long position entered at 0.9620. Below 0.9600 would risk test of strong support at 0.9583-86 but only break there would signal a downside break of recent broad range has occurred, bring subsequent fall to 0.9550.

As Dollar Reaches Bottom of Range Again, Investors Await Direction from Fed and White House

Despite a series of significant uptrends and downtrends since March, the US dollar has largely been bound within a trading range of between 115 and 108 against the Japanese yen for much of the year.

Growing doubts about the Fed's ambitious projections of one more rate increases in 2017 and three hikes in 2018 have weighed on the yield of 10-year Treasury notes, which peaked at 2.629% in March and currently stand around 2.185%. However, another factor in putting an end to the dollar's post-election rally has been the never-ending saga of political upheaval in the White House and in turn, fading hopes of a fiscal stimulus anytime soon. Ongoing troubles in the White House have been capping any advances the dollar has been able to muster from positive economic data.

The dollar's decline has been even steeper against other currencies, particularly against the euro, which is up 12% in the year-to-date. Even the Brexit-battered pound has gained versus the dollar so far this year. Against the safe-haven yen, the greenback is currently down by almost 7% since the start of 2017 as it hovers near the bottom of its range that's been in place since mid-January. It's worth noting though that when the dollar is trading near the top of its present range, those losses are limited to just under 2%.

The troubles in the Trump administration started on January 30 soon after the President took office and he fired the acting Attorney General, Sally Yates, after she refused to defend Trump's ban on immigrants from several Muslim-majority countries. They escalated on February 13 when Michael Flynn, the national security advisor was forced to resign over revelations of potentially illegal contacts with the Russian ambassador to the US. The next major departure came on May 9 when Trump fired the FBI director, James Comey. This was followed by the exit of Trump's first communication director on May 30. But the scale of the turmoil in the West Wing only became apparent in July when Tump's second communications director, Anthony Scaramucci, his press secretary, Sean Spicer, and chief of staff, Reince Priebus, all departed within days of each other.

There was some positive news for the markets in August when the President's chief strategist, Stephen Bannon, a known economic nationalist, was fired by Trump on the advice of his new chief of staff, John Kelly. Bannon was widely credited for driving much of Trump's anti-immigration and anti-trade policies and his departure gave some hope to market participants that Trump would tone down his rhetoric on trade and immigration. It's also a sign that the newly appointed chief of staff and retired general John Kelly is able to get a tighter grip on the White House, bringing discipline to the disorder.

While the series of resignations and sackings in July exasperated the dollar's decline from its July peak of 114.49 yen, the downtrend was triggered by an apparent shift in the Fed's stance to a less hawkish one. Federal Reserve Chair Janet Yellen voiced some concern about the softening in US inflation at her semi-annual testimony before Congress on July 12. Interestingly, the March downtrend was also sparked by the Fed, following the not-as-hawkish-as-expected FOMC projections from the March policy meeting, while the May downtrend came about from disappointing economic indicators.

This suggests Fed policy remains the main driver for the greenback despite the growing volatility and uncertainty being generated by White House developments. The next big move by the Fed is expected to come at the September policy meeting where they will likely initiate their well-telegraphed balance sheet reduction plan. Concerns about a possible government shutdown are unlikely to derail the Fed's plans unless it was to lead to a market panic.

President Trump this week threatened to shut down the government if Congress did not provide funding for his election pledge to build a wall across the Mexican border, adding to the unease in the markets. However, the dollar remains off its four-month low of 108.60 touched last week and could be on the verge of a new uptrend if it bounces off its support level of the bottom of the range, as it has done after the previous downtrends reached this area.

As sentiment for the dollar turns increasingly negative, with a bearish crossover of the 50- and 200-day moving averages in July underlining this view, it might not take much to trigger an upside correction. However, the odds for a breach of the range bottom is as likely, if not greater, given the downside risks. As dollar/yen wavers near this support level, direction could come either way from the Fed and Washington.

While Trump's record in the White House leaves much to be desired, progress on the tax front is not inconceivable as the reforms have broad-based support within the Republican party. Traders are unlikely to push the dollar substantially higher however, unless there was evidence that the tax reform plans were moving significantly forward as there's always going to be the risk of the President creating unnecessary distraction and antagonising his own party. Trump's response to the recent events in Charlottesville, Virginia may have lost him some key support from not just the Republicans but also from the business community.

Meanwhile, as the Fed appears to be taking a more cautious approach to inflation, markets may be underestimating the likelihood of another rate hike this year. Although various measures of inflation have weakened over the past few months, the labour market continues to tighten and consumer spending has rebounded from a soft patch earlier in the year. More importantly for the Fed, market volatility is at a record low, the dollar has depreciated substantially this year and financial conditions remain loose. Therefore, it could only require a minor reassuring uptick in price pressures to prompt Fed policymakers to resume their rate hiking cycle.

Alternatively, signs of further delays in Trump's economic agenda would only increase the bearish bets already placed against the dollar. A deepening turmoil in the White House as well as a possible escalation of tensions with North Korea could overshadow strong economic data. However, an increasing number of analysts are taking the view that low inflation is here to say and are not forecasting interest rates to peak much higher from their current levels. The next FOMC projections due on September 20 will be especially interesting to watch for any change in committee members outlook on inflation, as well as the updated dot plot chart.

Ceilings and Budgets and Shutdowns. Oh My!

Highlights

- Congress has two critical to-dos in September: raise the debt ceiling and pass a resolution to fund the government beyond Sept. 30th. In recent years, these issues often are not settled until the 11th hour, resulting in market volatility.

- With Republicans dominating Washington, agreements on both items should seemingly be reached more easily. However, the need for Democratic cooperation in the Senate raises the probability of a government shutdown in particular. A brief government shutdown would dent, but not derail, economic growth in the fourth quarter.

- The risk is a standoff could damage market confidence in Washington Republicans enacting pro-growth policies they expect. We had a sneak preview of the volatility that could result from this last week. While not our base case, a worst case scenario of a bad standoff and severe market turmoil could lead to the Fed delaying the start of normalizing its balance sheet in September.

When Congress resumes sitting on September 5th it has two pressing matters to address: the debt ceiling and funding the government beyond the end of September. In theory, the stakes are high on both fronts. If the debt ceiling is not raised or suspended, the government can no longer borrow to fund its deficit. This would be equivalent to an individual who has maxed out their credit cards, used all the cash hidden in cookie jars, and whose next paycheck isn't going to cover their expenses – something has to give. This raises the risk the government would either default on its debt payments, or leave other bills unpaid. And, if legislation is not passed to fund government programs beyond September 30th, many government functions and services would shut down, as we saw most recently in 2013.

Both of these items have proved contentious in the past, as various factions in Congress use them as leverage to achieve other policy priorities. With Republicans (GOP) controlling the Senate, the House and the White House, it would seem that a standoff is less likely this time around. Financial markets' are currently making the same bet. On a trend basis, volatility (as measured by the VIX) had been hovering near all-time lows, or reacting to geopolitical events such as North Korea and rumors about turmoil in the White House's economic leadership (Chart 1). Last week's experience shows how sensitive markets are to perceived turmoil in Washington. Markets currently assume the lion waiting for them in September is cowardly, just like in Oz. But, they will likely be spooked if it turns out to be the Wicked Witch.

However, the diversity of views within the GOP, and a narrow majority in the Senate doesn't eliminate the risk of a standoff. If a game of fiscal chicken erupts on either front, as we have seen in the past, market sentiment is likely to sour quickly.

The Debt Ceiling – the more you ignore me, the closer I get

For starters, the debt limit or "ceiling" caps the government's authority to borrow money (issue Treasury securities) to pay for spending already authorized by Congress. The U.S. government hit this ceiling back in mid-March, and the Treasury has since been using "extraordinary" measures to fund the government. The Treasury estimates the money in cookie jar and under mattresses will run out by September 29th, and has formally requested Congress to raise or suspend the debt ceiling, which it did not do before going on its August recess.

So far, the GOP leadership has not conveyed an interest in engaging in a public, confidence-damaging fight on the decision to raise or suspend the debt ceiling. GOP leadership, including Freedom Caucus leader Mark Meadows, recently reassured markets that they will raise or suspend the debt ceiling with no strings attached. No doubt, the 2011 experience of a disastrous debt ceiling standoff remains fresh in the minds of Republicans. Historically, Congress routinely raised the debt ceiling without much fuss. But in 2011, Republicans, having recently taken control of the House, demanded the President negotiate over deficit reduction in exchange for an increase in the debt ceiling. Two days before Treasury's stated deadline, Republicans agreed to raise the ceiling in exchange for future spending cuts embodied in the Budget Control Act of 2011. In reaction to the standoff, S&P downgraded the sovereign credit rating of the U.S. government for the first time ever. This resulted in the worst financial market volatility since the financial crisis, with the S&P 500 dropping about 12% over the course of the 2011 debt ceiling debacle.

There's some comfort today that the 2011 experience was under a Democratic President, and this time around, members are likely more confident that government spending restraint is more achievable with a Republican President. But it's not totally free and clear, as legislation to raise the debt ceiling will need 60 votes to pass the Senate, and Democrats could choose to be obstructive in getting a bill passed in a timely manner. It is unclear at this time what the Congressional leadership's strategy will be.

If an agreement does prove difficult when Congress returns in September, financial market reaction is likely to be more muted than the 2011 experience. At that time, S&P already had the U.S. rating on a negative watch. That is not the case this time around. S&P recently reaffirmed (Aug. 2, 2017) the US AA+ rating as stable. With the U.S. government's fiscal situation markedly improved since then (Chart 2), a downgrade is not in the offing.

Absent the credit rating experience, more recent debt ceiling showdowns in 2013 and 2015 were less damaging to markets. In 2013, the S&P 500 dipped slightly as the clocked ticked down to the deadline, but rebounded quickly afterwards, and in 2015 equity markets rose steadily. These more muted responses may reflect the fact that they expect an 11th hour deal, as was the case in 2011. Moreover, markets have greater confidence that default is not really on the table. According to transcripts (made public in 2016) of a Conference call with then Fed Chair Ben Bernanke in 2011, the Federal Reserve and Treasury had developed procedures that would have insured principal and interest on Treasury securities would continue to be made on time. "Other" payments may be delayed. We don't know specifics, but these payments could include salaries, payments on contracts or even delay Social Security or Medicare payments.

Even if the debt ceiling isn't raised and the U.S. avoids a technical default, there would still be a price to pay for the standoff apart from losses on equity markets. Reduced market confidence in the U.S. government's ability to keep its fiscal house in order has a real cost. The U.S. Government Accountability Office estimated that delays in raising the debt ceiling in 2011 led to an increase in government borrowing costs of $1.3 billion in 2011. 2011 likely represents a worst-case scenario, but the short-term measures Secretary Mnuchin has had to take since the debt limit was reached in March have cost at least $2.5 billion, not including any increased borrowing costs. (Ultimately, this is a drop in the bucket for a $4 trillion budget.)

Government shutdown more likely, but less damaging

The second pressing issue facing the GOP relates to funding government services for the next fiscal year, which starts on October 1st. On this front, consensus is less clear. In the tangled web of U.S. budgeting process, the appropriations process for the 2018 fiscal year is underway without a Budget resolution. The House has passed four of 12 appropriation bills, but these would likely need Democratic support in the Senate. So funding decisions for FY2018 are far from assured, and Congressional leadership has not outlined their plan publically for September.

Congress must either pass a budget resolution or a continuing resolution stop gap to fund the government beyond September 30th. To pass tax reform through reconciliation, Congress ultimately needs to pass a budget resolution with reconciliation instructions. But, in the interim, a continuing resolution to fund government for a given period of time may be more achievable given the House is only sitting for 12 days in September. However, a continuing resolution could be filibustered in the Senate, and therefore would need Democratic support to pass. Add to this the fact that Trump had threatened a government shutdown in the fall earlier this year, and the risks that an agreement will not be reached cannot be ignored.

This is not uncharted territory. The U.S. government has gone through 18 government shutdowns in the modern budgeting era (since 1976), and the economic impact would be small provided the shutdown is not prolonged. The Bureau of Economic Analysis (BEA) estimated that the 16-day shutdown in 2013 lowered real GDP in Q4 2013 by 0.3 percentage points (annualized), but growth was still very strong in that quarter as a whole. If the shutdown were to drag on, for example, for four weeks, it is estimated it would lower real GDP growth by 1.5 percentage points (annualized) in the fourth quarter.

On average, government shutdowns have lasted seven days. However, the two most recent shutdowns were far longer. During the 2013 shutdown, about 40% of government workers were furloughed, equivalent to 850 000 people. However, one of the reasons that the impact isn't greater on economic activity is because essential roles remain in place, like air-traffic controllers, armed forces, and food safety inspectors. The Federal Reserve is not funded by Congress, so it too would remain open for business. But, tax refunds and economic data releases would be delayed, among other things, causing significant disruption in the lives of many Americans.

Worst case scenarios could stay the Fed's hand

Facing midterm elections next year the GOP likely wants to demonstrate their ability to govern, and a damaging game of fiscal chicken is not in their interest. That said, raising the debt ceiling and passing a continuing resolution to fund government beyond Sept. 30th will require cooperation with Democrats in the Senate. That is a wide ideological expanse to bridge with right-wing factions in the GOP. Therefore, a down-to-the wire debate on either matter cannot be ruled out. If market volatility spikes significantly, the Fed could delay normalizing its balance sheet, which is expected to be detailed at the September 20th meeting. Back in May, Fed Governor Brainard had flagged the debt limit as a possible pitfall for her outlook.

This scenario is not our base case, but financial markets have until recently been complacent about domestic risks. There is a tendency for agreements to not be reached until the 11th hour, and it would not take much in this environment to see volatility return in September. This was born out in last week's experience where mere rumors that moderate White House economic advisor Gary Cohn might resign, sent volatility back as nearly as high as it was during heightened worries about North Korea. As such, investors would do well to brace themselves for a potential twister of volatility in September.

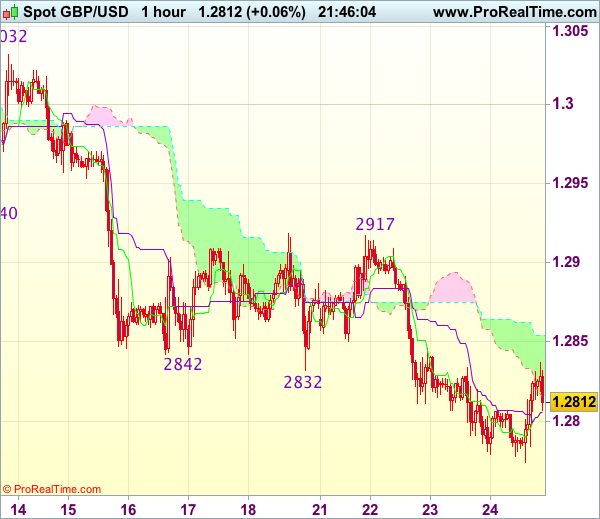

Trade Idea Update: GBP/USD – Buy at 1.2770

GBP/USD - 1.2815

Original strategy :

Buy at 1.2770, Target: 1.2870, Stop: 1.2735

Position : -

Target : -

Stop : -

New strategy :

Buy at 1.2770, Target: 1.2870, Stop: 1.2735

Position : -

Target : -

Stop : -

Although cable has remained under pressure and near term downside risk remains for recent selloff to extend one more fall, loss of downward momentum should prevent sharp fall below 1.2750-55, risk from there has increased for a rebound to take place soon, above 1.2845-50 would suggest a temporary low is possibly formed, bring a stronger rebound to 1.2870, break there would add credence to this view, then retracement of recent decline would commence for further gain to 1.2900.

In view of this, we are inclined to turn long on next decline. Below 1.2740-50 would risk weakness to 1.2720-25, however, still reckon downside would be limited to 1.2700-05 (100% projection of 1.3269-1.2940 measuring from 1.3032) and risk from there remains for another rebound to take place later.

Trade Idea Update: EUR/USD – Hold long entered at 1.1765

EUR/USD - 1.1801

Original strategy :

Bought at 1.1765, Target: 1.1865, Stop: 1.1770

Position : - Long at 1.1765

Target : - 1.1865

Stop : - 1.1770

New strategy :

Hold long entered at 1.1765, Target: 1.1865, Stop: 1.1770

Position : - Long at 1.1765

Target : - 1.1865

Stop : - 1.1770

As the single currency has retreated after faltering below resistance at 1.1828, suggesting minor consolidation would be seen, however, as long as 1.1765-70 holds, mild upside bias remains for another rebound, above said resistance at 1.1828 would extend the rise from 1.1662 low to resistance at 1.1847, break there would provide confirmation that the pullback from 1.1910 has ended and encourage for headway to 1.1870-80 but reckon said resistance at 1.1910 would hold from here.

In view of this, we are holding on to our long position entered at 1.1765. Only below 1.1740 support would abort and suggest the rebound from 1.1662 has ended instead, risk weakness to 1.1695-00 first.