Sample Category Title

Brexit Fears Pull Down the Pound

The euro is growing on the back of strong macro data from the flash manufacturing PMI in Germany. According to preliminary data, there was an increase by 59.4 in August vs expected 57.7. The same indicator but for the entire Eurozone increased to 57.4, which is a 0.8 uplift compared to July. The support for the common currency came from the US where President Donald Trump stated that he is willing to close down the government to build the Mexico wall. The market already got used to unexpected statements of Mr. Trump and the influence of his words is likely to be short-lived. The greenback was also negatively affected by data from the new home sales in America which revealed a decline to 571,000 vs 611,000 forecasted. Investors remain nervous ahead of the speech of the Fed's Chairwoman Janet Yellen on Friday in Jackson Hole.

The lack of confidence regarding Brexit talks is a serious obstacle for the British economy and the GBP/USD remains under the pressure of fears about negative economic implications. One of the signs pointing to the worsening of the situation is the price fall of VIP housing in London. Traders are waiting for the preliminary report on the British GDP for the second quarter that will be released tomorrow.

The New Zealand dollar today was under the pressure of worsening GDP expansion forecast in the country for 2017/2018 to 3.5% vs 3.7% previously estimated. Another volatility spike is possible ahead of the publication of the trade balance report in New Zealand at 22:45 GMT.

EUR/USD

The EUR/USD price is trying to gain a foothold above the important level of 1.1800. In case of success we are likely to see continued increase up to 1.1900 and 1.2000. In the coming days the volatility will probably remain high due to expectation of important news from the Jackson Hole symposium. In order to resume negative dynamics, the price has to break through the support at 1.1750 that may become a signal to sell with potential targets at 1.1620 and 1.1550.

GBP/USD

The GBP/USD rate is consolidating near 1.2800 and fixing below this support will open the way for the further drop with potential objectives at 1.2635 and 1.2590. The upward correction is limited by the upper limit of the descending channel and the resistance range 1.2880 - 1.2900. Most likely scenario will be the weakening of the pound against the US dollar.

NZD/USD

The New Zealand dollar is approaching to the important support of 0.7200. Breaking through this line may become a trigger for massive selling, with the fall potentially reaching to 0.7000 - 0.7040. On the other hand, we do not exclude a slight upward correction in the near future to SMA100 on 15-minute chart. The amplitude of price fluctuations may increase after the country's trade balance report release tonight.

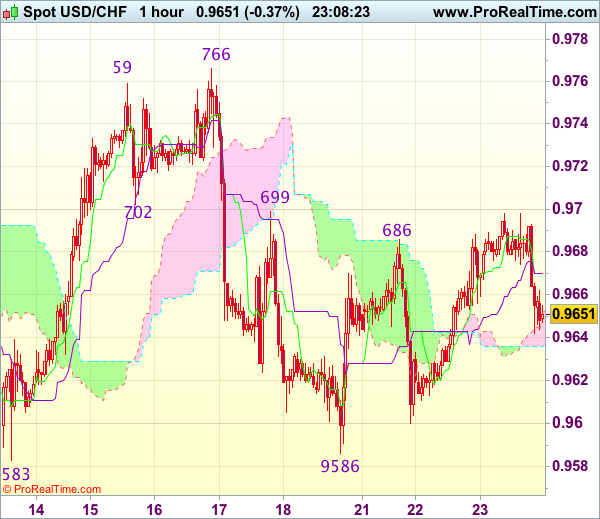

Trade Idea Wrap-up: USD/CHF – Buy at 0.9620

USD/CHF - 0.9658

Most recent candlesticks pattern : N/A

Trend : Sideways

Tenkan-Sen level : 0.9670

Kijun-Sen level : 0.9670

Ichimoku cloud top : 0.9652

Ichimoku cloud bottom : 0.9636

Original strategy :

Buy at 0.9620, Target: 0.9720, Stop: 0.9585

Position : -

Target : -

Stop : -

New strategy :

Buy at 0.9620, Target: 0.9720, Stop: 0.9585

Position : -

Target : -

Stop : -

As the greenback has retreated after faltering below resistance at 0.9699, suggesting initial downside risk remains for weakness to 0.9620-30, however, as long as support at 0.9586 holds, prospect of another rebound remains, above said resistance at 0.9699 would signal the retreat from 0.9766 has ended at 0.9586 last week and mild upside bias is seen for gain to 0.9720, then 0.9740, having said that, reckon resistance at 0.9766-73 would cap upside and bring further consolidation. Only a break of 0.9773 would retain bullishness and signal early rise from 0.9438 has resumed and extend gain to 0.9800.

In view of this, we are looking to buy dollar on further pullback as 0.9620-30 should limit downside. Below 0.9600 would risk test of strong support at 0.9583-86 but only break there would signal a downside break of recent broad range has occurred, bring subsequent fall to 0.9550.

Trade Idea Wrap-up: GBP/USD – Stand aside

GBP/USD - 1.2800

Most recent candlesticks pattern : N/A

Trend : Near term down

Tenkan-Sen level : 1.2810

Kijun-Sen level : 1.2816

Ichimoku cloud top : 1.2864

Ichimoku cloud bottom : 1.2858

New strategy :

Stand aside

Position : -

Target : -

Stop : -

Although cable has remained under pressure after resuming recent decline and near term downside risk remains for weakness to 1.2775-80 (38.2% Fibonacci retracement of 1.1986-1.3269), loss of downward momentum should prevent sharp fall below 1.2750 and reckon 1.2725-30 would limit downside, price should stay above 1.2700-05 (100% projection of 1.3269-1.2940 measuring from 1.3032) and risk from there is seen for a rebound to take place later.

In view of this, would not chase this fall here and would be prudent to stand aside for now. Above 1.2840-45 would suggest a temporary low is possibly formed, bring rebound to 1.2870-75 and then 1.2890 but reckon resistance at 1.2917-18 would hold from here, bring another decline.

Trade Idea Wrap-up: EUR/USD – Hold long entered at 1.1765

EUR/USD - 1.1812

Most recent candlesticks pattern : N/A

Trend : Sideways

Tenkan-Sen level : 1.1780

Kijun-Sen level : 1.1780

Ichimoku cloud top : 1.1781

Ichimoku cloud bottom : 1.1779

Original strategy :

Bought at 1.1765, Target: 1.1865, Stop: 1.1740

Position : - Long at 1.1765

Target : - 1.1865

Stop : - 1.1740

New strategy :

Hold long entered at 1.1765, Target: 1.1865, Stop: 1.1770

Position : - Long at 1.1765

Target : - 1.1865

Stop : - 1.1770

Although the single currency slipped in European morning, as euro found support at 1.1740 and has rebounded, retaining our view that the pullback from 1.1828 has ended there and bring retest of said resistance, break there would extend the rise from 1.1662 low to resistance at 1.1847, above there would provide confirmation that the pullback from 1.1910 has ended and encourage for headway to 1.1870-80 but reckon said resistance at 1.1910 would hold from here.

In view of this, we are holding on to our long position entered at 1.1765. Only below 1.1725-30 would abort and suggest the rebound from 1.1662 has ended instead, risk weakness to 1.1695-00 first.

Euro Gains on PMI, Hits Fresh 10½-Month High Vs Sterling; Dollar Hurt by Trump, Data Misses

During today's European session, forex market participants pushed the euro higher on the overall positive picture given by the PMI figures released earlier in the day. In the meantime, the dollar index was down with the US currency being on a negative footing in today's trading after some comments made by the US President yesterday in Phoenix. Data releases falling short of forecasts also weighed on the US currency.

Eurozone flash PMI figures for the month of August were released during morning European trading hours. The figure for manufacturing activity edged higher to 57.4 from July's 56.6, outstripping forecasts for a reading of 56.3 and rising to its highest in six-and-a-half years. The services PMI though, was released at its lowest since January of the current year at 54.9, failing to beat expectations for a reading of 55.4 and coming in below July's 55.4. Finally, the composite PMI, which blends the two (manufacturing and services PMIs) and which is considered a good proxy for overall growth, came in slightly above July's 55.7 at 55.8 – analysts anticipated the measure to stand at 55.5. It is encouraging for the euro area that the manufacturing sector has not been negatively affected despite the strong euro rally thus far in 2017.

Eurozone's common currency fell within the first few minutes of data release relative to the greenback after initially jumping higher. Shortly after though, it more than made up for the decline. It should also be noted that euro/dollar posted sizable gains earlier in the day upon the release of August flash manufacturing and services PMI data for Germany, eurozone's (and Europe's) largest economy – both readings positively surprised while coming in above July's respective figures.

Later in the session, preliminary figures for the month of August showed eurozone consumer confidence rising to -1.5 from July's -1.7. Expectations were for a fall to -1.8. The euro gained on the news relative to the US currency. Euro/dollar last traded above the 1.18 handle, 0.4% up on the day.

Moving to euro/pound, the pair acted similarly to euro/dollar upon the release of the data above. In addition, euro/pound today rose to a fresh 10½-month high of 0.9236 (this constitutes an eight-year high if one were to exclude sterling's flash crash during October of last year). It is of notice that some analysts are warning that euro strength in recent months is overstretched.

In other news pertaining to the eurozone, European Central Bank President Mario Draghi appeared in Germany today. His comments were not market moving though, as he avoided to offer anything new in terms of monetary policy. On Friday, he's scheduled to give a speech at the Jackson Hall symposium. Federal Reserve Chair Janet Yellen will also be speaking at the same event on Friday. Market participants do not expect either of them to make market-sensitive remarks.

Out of the US, the August flash manufacturing PMI was released at 52.5, below expectations and July's 53.3. Dollar/yen didn't react much to the news. New home sales for July released later in the day stood at 571k, their lowest in seven months. This negatively compares to projections for a reading of 612k. June's respective figure was upwardly revised to 630k from 610k before, putting the month-on-month drop to stand at 9.4% – the largest since August of last year. The US currency declined versus the yen as the data went public, though not by much.

The dollar index, a broader gauge of the US currency's strength, was last down 0.3% on the day, trading at 93.2. Meanwhile, dollar/yen was 0.4% down and close to 109 level. US President Donald Trump's comments at a rally in Phoenix yesterday where he said he'd be willing to shut down the government in order to follow through his campaign pledge to build a wall alongside the US-Mexican border, acted as a drag for the currency during today's trading.

Gold benefitted from dollar weakness to last trade 0.3% up on the day at $1,288.24 an ounce.

Finally, during afternoon European trading hours, the Energy Information Administration (EIA) released its weekly report on US crude inventories. The report showed stockpiles declining by 3.33 million barrels in the week ending August 18, less than the 3.45m that was expected and the 8.95 reduction reported the previous week. In contrast to yesterday's report by the American Petroleum Institute (API), gasoline stocks fell more than expected. WTI experienced added volatility after the data release. It last traded 0.1% down at $47.77 a barrel. Brent was up by less than 0.1% at $51.90 per barrel. The oil-linked Canadian dollar was slightly down versus it's US counterpart with dollar/loonie at 1.2566.

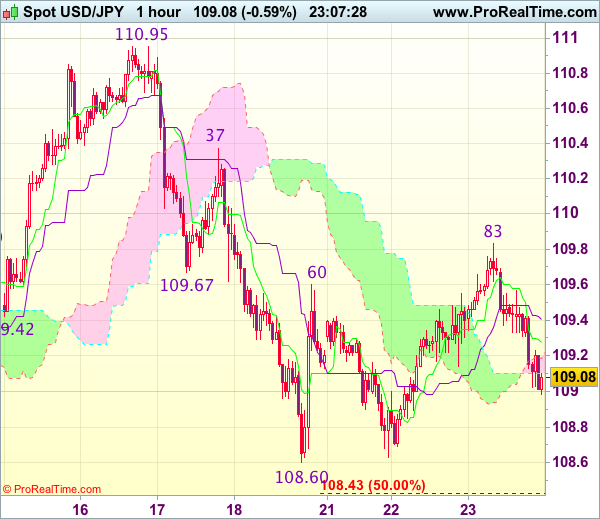

Trade Idea Wrap-up: USD/JPY – Stand aside

USD/JPY - 109.10

Most recent candlesticks pattern : N/A

Trend : Near term down

Tenkan-Sen level : 109.28

Kijun-Sen level : 109.41

Ichimoku cloud top : 109.18

Ichimoku cloud bottom : 109.10

New strategy :

Stand aside

Position : -

Target : -

Stop : -

Despite intra-day initial brief rise to 109.83, lack of follow through buying on break of resistance at 109.60-67 and the subsequent retreat suggest consolidation below this level would be seen and pullback to 109.00 cannot be ruled out, however, break there is needed to signal the rebound from 108.60 has ended there, bring further fall to 108.80, then test of said support. A break of this support would confirm recent decline has resumed and may extend further weakness to 108.30 (1.618 times projection of 110.95-109.67 measuring from 110.37), then towards 108.00.

On the upside, above 109.60 would bring test of said resistance at 109.83, break there would signal low has been formed at 108.60 and bring a stronger rebound to 110.00 and later towards resistance at 110.37 which is likely to hold from here. As near term outlook is still mixed, would be prudent to stand aside in the meantime.

US Debts Approach Limit. How Will It Affect Fed’s Policy?

Recent comments from US Treasury Secretary Steven Mnuchin and Senate Majority Leader Mitch McConnell appeared to have lifted market confidence that the government will eventually be able to raise the debt ceiling and avoid default. While our base case is that a debt ceiling would be suspended or raised, and the government would avoid a shutdown, we do not expect things to go smoothly and it would likely be a last-minute deal. US' politics has been under the spotlight since Donald Trump has become the president. At over 200 days in office, Trump's Russia scandal probably caught most attention, followed by the war of words with North Korean leader Kim Jongun. More recently, Trump dissolved several business advisory councils after resignations of a number of CEOs. On economic achievement, Trump has failed to pass the healthcare reform bill and was unable to kick start any pro-growth or tax policy. The government's debt issue is close watched and volatility of the stock markets could increase as we approach the deadline.

The Congress suspended the debt ceiling in November 2015 until mid-March 2017. Since then, the Treasury has been using "extraordinary measures" to raise capital. In a June report, the Treasury revealed that the extraordinary measures include (1) suspending sales of State and Local Government Series Treasury securities; (2) redeeming existing, and suspending new, investments of the Civil Service Retirement and Disability Fund and the Postal Service Retiree Health Benefits Fund; (3) suspending reinvestment of the Government Securities Investment Fund; and (4) suspending reinvestment of the Exchange Stabilization Fund. However, these measures will run out in early September and the Treasury would resort to incoming tax receipt for financing until September 29. Therefore, it would be critical to raise the debt ceiling by that day. Mnuchin has suggested that he strongly prefer to have "a clean raise of the debt limit", while McConnell added that there is "zero chance - no chance - we won't raise the debt ceiling. No chance".

Freedom Caucus Links Vote to Borrowing and Spending Restrictions

The confidence might come from the fact that, together with a Republican president, the GOP is also control of both the House and the Senate. During the debt ceiling crisis in 2011 and 2013, the Congress was split under a Democrat President, while the Congress was controlled by Republicans under a Democrat President in 2015. Failure to pass the healthcare reform bill has already reflected that a full control by one party does not necessarily be more efficient. The vote amongst Republicans is not unanimous. The House Freedom Caucus, consisting of conservative and libertarian Republican members of the United States House of Representatives, is split on whether they would link a spending cut with the debt-ceiling vote.

60 Votes Needed in Senate

In the Senate where Republicans take 52 seats, 60 votes are needed to pass debt ceiling legislation. So far, Democrats' position regarding a "clean" raise has been ambiguous. Democrat leaders Schumer and Pelosi threatened in June they might not vote for the raise in debt ceiling if the tax cut for the very wealthy might result in huge increases the deficit. Yet, they later changed mind and noted that they would support a "clean" bill, free of conditions. There is no recent update on Democrats' view.

Will Fed Postpone Announcement of Balance Sheet Reduction?

2013

Bearing a resemblance to the situation in 2013, one may worry about Fed's move in light of possible government shutdown. Back in 2013, the FOMC, led by the then Chair Ben Bernanke, noted at the July meeting minutes that "if economic conditions improved broadly as expected, the Committee would moderate the pace of its securities purchases later this year. And if economic conditions continued to develop broadly as anticipated, the Committee would reduce the pace of purchases in measured steps and conclude the purchase program around the middle of 2014". This had spurred strong expectations that the announcement would be made in September. Yet, haunted by threats of not raising debt ceilings by Republicans at the time, Bernanke refrained from making related announcement at the meeting on September 17-18. As noted in the minutes, the Fed acknowledged that "a number of significant risks remained, including those related to the potential economic effects of the sizable increases in interest rates since the spring, ongoing fiscal drag, and the possible fallout from near-term fiscal debates". Thus, it decided to "await more evidence that progress will be sustained before adjusting the pace of its purchases". US dollar slumped with the DXY index sinking over -1% on the day of this dovish announcement.

The FOMC meeting was followed by a 16-day government shutdown from October 1. The shutdown delayed the releases of key economic data including the September employment report, CPI and PPI data, as well as GDP growth estimates. Undoubtedly, the accuracy of the delayed data was questionable as there was data collection in the first half of October was suspended due to the shutdown.

2017

The July minutes noted that "participants generally agreed that, in light of their current assessment of economic conditions and the outlook, it was appropriate to signal that implementation of the program likely would begin relatively soon, absent significant adverse developments in the economy or in financial markets". The market has almost fully priced in an announcement at the meeting on September 20, 9 days before the deadline of raising the debt ceiling so as to avoid additional payment delays and a default. We do not expect the Fed would postpone the announcement this time. The chance that a debt ceiling can be raised on time is much higher this time so that the likelihoods of a default and a government shutdown are lower. Moreover, economic developments are more upbeat and financial conditions more accommodative today than in 2013. On the economic developments, the unemployment rate this year has fallen about three percentage points from four years ago, while GDP growth is also less volatile. Therefore, we expect the Fed would ignore the noise of a potential shutdown and make formal announcement of balance sheet reduction in September.

Trump Comments Weigh on US Dollar

- US stocks opened lower after President Trump injected fresh uncertainty into markets by threatening to shut down the government if Congress did not pay for his proposed border and to pull out of the North American Free Trade Agreement.

- Economic activity in the eurozone has picked up in August after a disappointing July, with a strong performance in the manufacturing sector (57.4 from 56.6 vs 55.4 expected) offsetting a slight decline in the services industry (54.9 from 55.4 vs 55.4 expected), according to August PMI's.

- US PMI's printed in the opposite direction of EMU ones. The manufacturing gauge unexpectedly declined from 53.3 to 52.5 (vs 53.5 expected) while the services PMI rose from 54.7 to 56.9 (vs 55.0 forecast).

- Mario Draghi didn't give any specific clues on the future of the ECB's asset-purchase program in his speech to Nobel laureates and young economists, saying instead that central banks need to be open-minded when preparing for new challenges. Focus turns to his Jackson Hole address on Friday.

- US oil inventories fell 3.6 million barrels last week, according to API data. EIA figures today are expected to confirm a similar drop. However, increasing gasoline and diesel supplies offset the withdrawal, balancing the effect on prices.

Rates

Core bonds go higher on Trump inspired risk-off

Core bonds move modestly higher despite strong EMU business confidence, as comments of president Trump on NAFTA and on a possible government shutdown spook markets. Riskier assets like equities, peripheral bonds and even the dollar lose ground. Core bonds, gold and the yen benefit. Trump comments caused some risk-off jitters during the Asian overnight session, slumbered during the European morning session, but re-appeared with a vengeance as the US session gets going.

President Trump threatened to end the NAFTA deal and would eventually prefer to close the government in case Congress doesn't foresee money for his pet project (" the Wall"). Trump often threatens in negotiations and all his comments shouldn't be taken for granted, but this time they send some shivers through the markets. Intrinsically, one would expect that US Treasuries be hit most, but investors consider them as a safe haven refuge. T-bills on the contrary reflect the fear for a failure to raise the debt ceiling on time. The spread between the 28 sept/T-bill and the Oct 5 T-bill rose today to 17 bps. End September, the ceiling should be reached.

The Bund opened a tad lower, but immediately gained some ground. However, stronger than expected EMU PMI business confidence pushed the Bund slightly lower again. European equities opened somewhat higher catching up with US equities which finished strongly yesterday. However, equity opening gains vanished soon and sideways trading kicked in. Similarly the Bund went nowhere till noon. The German Bund auction was only just covered, but didn't impact dealings. When US traders entered the fray, Trump's comments were prominently discussed. The US Treasuries went up in a move duplicated by German Bunds. The Bund future currently tests the August high at 164.64, which if broken opens the path to the June and April highs at 165.55/93.

At the time of writing, German yields drop 1.4 (2-yr) to 2 (10-yr) bps, while US Treasury yields decline between 1.2 (2-yr) and 3.1 (10-yr) bps. Peripheral spread widening continued today with the 10-yr yield spread up by 3 (Spain) to 5 bps (Italy/Portugal).

Currencies

Trump comments weigh on US dollar

A new wave of unconventional comments of US president Trump on NAFTA and on a government shutdown aborted yesterday's USD rebound. At the same time, the euro was supported by very strong EMU PMI's. EUR/USD returned to the 1.18 area. USD/JPY is drifting back to the 109 barrier.

Overnight, Asian equities opened strong after the WS rally. USD/JPY filled offers in the 109.83 area, but risk sentiment deteriorated after Donald Trump said he may end NAFTA at some point. He also threatened to shut down the US government if he wouldn't get the funding to build a wall along the Mexican border. Equities ceded part of the early gains. USD/JPY returned to the mid 109 area. EUR/USD was little affected by Trump's comments.

They nevertheless prevented European equities to profit from the late session WS up-leg. However, there was initially little additional negative impact on the dollar. The focus for (currency) trading turned to the EMU data. EMU PMI's (especially the German manufacturing PMI) were very strong. EUR/USD jumped to high 1.17 area and found a short-term equilibrium in the 1.1780 area. LT interest rate differentials narrowed marginally in favour of the euro. Risk sentiment remained fragile, preventing USD/JPY to profit from the slight post-PMI rise in core yields. EUR/JPY mirrored the EUR/USD uptick.

US equity futures continued to trade with a negative bias at the start in the US as the overnight Trump headlines returned to the forefront. The dollar continued to fight an uphill battle. EUR/USD (temporary?) regained the 1.18 barrier. USD/JPY dropped to the low 109 area. Yesterday's USD rebound obviously wasn't anything more than a technical move. Dollar sentiment remains fragile. The focus stays on the CB Jackson Hole speeches. However, we wouldn't be surprised if Draghi and Yellen stay muted on any changes in their respective policy approach.

EUR/GBP jumps north of 0.92 barrier

There were plenty of press articles on the role of the ECJ and on how the UK and the EMU will handle juridical disputes in the post-Brexit era. Some comments considered the British language that it will accept no 'DIRECT' jurisdiction of the court as a potential opening/moving back on earlier tough separation rhetoric. At least for now, this potential softer approach didn't help sterling much. EUR/GBP even jumped north of 0,92, admittedly in the first place due to the strong EMU PMI's. However, cable also dropped temporary below 1.28. Sterling clearly needs concrete signs of progress in the run-up to the next round of formal talks that will take place next week. Cable trades near 1.28. EUR/GBP has settled in the 0.9215 area.

Japan 225 Stock Index Turns Bearish after Breaking Out of Consolidation Phase

The Japan 225 stock index consolidated for six weeks after it touched a two-year high of 20322 on June 20. Then, on August 8 the index followed a bearish path, crossing below the Ichimoku cloud and the 50-day exponential moving average (EMA).

According to the technical indicators, the picture in the short term is bearish. The RSI has continued trending below its neutral zone even after emerging from oversold area on August 11, while the MACD has been moving in a negative territory since August 8. The negative alignment between the Kijun-sen and the Tenkan-sen which is still intact since July 20 also gives an additional bearish evidence.

If the index extends its current downtrend, the 50% Fibonacci level at 19257 of the upleg from 18199 to 20322 (April – June) would provide an immediate support. Any violation of this point would likely push prices further down and shift focus to the point of 19005, which is also the 61.8% Fibonacci, while the 78.6% Fibonacci at 18650 could act as an additional barrier to downside movements.

On the other hand, a market action to the upside would first touch the 38.2% Fibonacci of 19510, which was tested recently, before it meets resistance at the 23.6% Fibonacci of 19818. The latter is considered a strong area as the 50-day EMA and the bottom of the Ichimoku cloud are also located in this zone. From here, the index would target June's two-year high of 20322 as a resistance.

Regarding the medium-term outlook, the index looks neutral as long as it ranges between 19261 and 20322.

Trade Idea: EUR/GBP – Buy at 0.9115

EUR/GBP - 0.9216

Original strategy :

Buy at 0.9070, Target: 0.9190, Stop: 0.9030

Position : -

Target : -

Stop : -

New strategy :

Buy at 0.9115, Target: 0.9215, Stop: 0.9075

Position : -

Target : -

Stop : -

As the single currency has surged again after brief pullback, adding credence to our bullish view that recent upmove is still in progress and may extend further gain to 0.9245-50, however, weakening of near term upward momentum should prevent sharp move beyond 0.9270-75 and price should falter below 0.9300-05, risk from there has increased for a retreat to take place later.

In view of this, would not chase this rise here and would be prudent to buy euro on subsequent pullback as 0.9110-15 would limit downside. Below 0.09090 would defer and suggest a temporary top is possibly formed, risk test of support at 0.9063, however, break there is needed to add credence to this view, bring retracement of recent upmove towards 0.9005-10.

Our preferred count is that, after forming a major top at 0.9805 (wave V), (A)-(B)-(C) correction is unfolding with (A) leg ended at 0.8400 (A: 0.8637, B: 0.9491 and 5-waver C ended at 0.8400. Wave (B) has ended at 0.9413 and impulsive wave (C) has either ended at 0.8067 or may extend one more fall to 0.8000 before prospect of another rally. Current breach of indicated resistance at 0.9043 confirms our view that the (C) leg has ended and bring stronger rebound towards 0.9150/54, then towards 0.9240/50.