Sample Category Title

Market Update – European Session: Draghi Speech Largely Academic

Notes/Observations

Major European Aug Preliminary PMI Manufacturing data better-than-expected (Beats: France, Germany and Euro Zone)

Draghi speech in Germany mostly centered on academic observations but noted to be prepared for new challenges

President Trump raised the specter of a government shutdown to fulfil a campaign pledge of building the Mexican border wall

Overnight

Asia:

Japan Aug Preliminary PMI Manufacturing: 52.8 v 52.1 prior

Europe:

PM May said to drop pledge to cut ties with European Court of Justice (ECJ) after Brexit and sought only to ensure that the ECJ did not have direct jurisdiction over the UK

Americas:

President Trump commented on NAFTA during his from Arizona rally and personally believed that the US could not make a deal, will probably end up terminating it at some point

Mexico Foreign Min Videgaray: Mexico will continue with NAFTA talks

Energy:

Weekly API Oil Inventories: Crude: -3.6M v -9.2M prior

Economic data

(FR) France Aug Preliminary Manufacturing PMI: 55.8 v 54.5e (10th month of expansion), Services PMI: 55.5 v 55.8e, Composite PMI: 55.6 v 55.4e

(DK) Denmark Aug Consumer Confidence Index: 7.6 v 9.5e

(TR) Turkey Aug Consumer Confidence : 71.1 v 71.3 prior

(DE) Germany Aug Preliminary Manufacturing PMI: 59.4 v 57.6e (33rd month of expansion), Services PMI: 53.4 v 53.3e, Composite PMI: 55.7 v 54.7e

(EU) Euro Zone Aug Preliminary Manufacturing PMI: 57.4 v 56.3e (49th month of expansion), Services PMI: 54.9 v 55.4e, Composite PMI: 55.8 v 55.5e

(ZA) South Africa July CPI M/M: 0.3% v 0.3%e; Y/Y: 4.6% v 4.6%e (4th straight reading within the SARB target range of 3.0-6.0%)

(ZA) South Africa July CPI Core M/M: 0.5% v 0.5%e; Y/Y: 4.7% v 4.7%e

(TW) Taiwan July Industrial Production Y/Y: 2.4% v 3.3%e

(IS) Iceland Central Bank (Sedabanki) left its 7-Day Term Deposit Rate currently stands at 4.50% for its 1st pause in three meetings since removing capital controls

Fixed Income Issuance:

(IN) India sold total INR170B vs. INR170B indicated in 3-month and 6-month Bills (INR100B and 70B respectively)

(DK) Denmark sold total DKK1.45B in 2020 and 2027 Bonds

(EU) ECB allotted $35M in 7-day USD Liquidity Tender at fixed 1.64% vs $35M prior

(SE) Sweden sold total SEK2.5B vs. SEK2.5B indicated in 2023 and 2026 bonds

SPEAKERS/FIXED INCOME/FX/COMMODITIES/ERRATUM

Equities

Indices [Stoxx600 -0.3% at 374.8, FTSE +0.1% at 7388, DAX -0.1% at 12219, CAC-40 flat at 5133, IBEX-35 -0.1% at 10397, FTSE MIB -0.1% at 21698, SMI -0.3% at 8941, S&P 500 Futures -0.2%]

Market Focal Points/Key Themes:

European Indices trade lower across the board tracking US futures lower, despite stronger than expected Manufacturing PMI readings out of Europe. Advertising giant WPP set the tone following its results trading lower by over 10% after cutting its full year outlook following pressure on client spending particularly in the fast moving consumer goods sector. Elsewhere K+S shares trade higher after vague rumours regarding a potential stake acquisition by Elliot. Elsewhere Bayer shares trade little changed after the EU initiates a phase II probe on competition concerns.

Looking ahead to the US morning, retailers continue to dominate earnings with notable names including Express and American Eagle set to report alongside earnings from Lowes.

Equities

Consumer discretionary [WPP [WPP.UK] -11% (Earnings, cuts outlook), Publicis [PUB.FR] -2.9% (In sympathy with WPP], Emmi [EMMN.CH] -9.5% (Earnings) , Rockwool [ROCKB.DK] +4.9% (Earnings)]

Materials: [K+S [SDF.DE] +3.6% (Reportedly Elliot looking to take stake) ]

Industrials: [Vedanta [VED.UK] +1.9% (Earnings) , Costain [COST.UK] +2.1% (Earnings)]

Healthcare: [Ambu [AMBUB.DK] +6.7% (Earnings), NMC Health [NMC.UK] +4.9% (Earnings)]

Speakers

ECB's Draghi noted that research helped us decide whether a change in facts deserves a policy response or look through it. Research showed that QE and forward guidance are a success> Monetary policy must always prepare for new challenges

German Fin Min Schaeuble said to want more influence on region's budgets and working on a proposal that would allow southern euro zone countries to tap into the single currency bloc's bailout fund to boost investments during recessions (**Insight: Plan would mark a major change of policy for Schaeuble)

Norway PM Solberg: Growth is improving and employment is gaining

Currencies

EUR/USD reverse earlier loses following better Manufacturing PMI. Also Draghi’s speech ahead of his Jackson Hole conference focused only on academic observations and did not address any concern on the recent EUR currency appreciation or hints on QE exit.

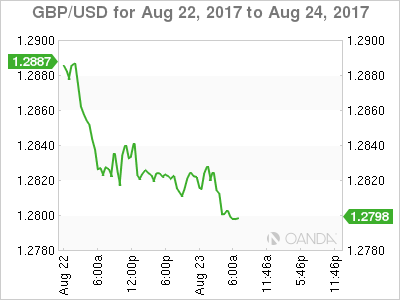

GBP/USD tested 2-month lows below the 1.28 level despite talk that the UK was softening its stance on Brexit. PM May said to drop pledge to cut ties with European Court of Justice (ECJ) after BrexiT viewed as a sign of a new willingness to compromise

Fixed Income

Bund futures trades at 164.24 down 12 ticks following strong German PMI readings, with IHS Markit noting input inflation continued to rise, with manufacturing posting a steeper rate of price increases. Downside targets 163.50 followed by 162.56. To the upside the 164.50 to 165.20 remains key resistance.

Gilt futures trades at 127.55 down 10 ticks little changed along with Bunds. A resumption to the upside could eye 128.25 then 128.75. A move back below 126.51 targets 125.97

Wednesday's liquidity report showed Tuesday’s excess liquidity rose to €1.715T from €1.711T and use of the marginal lending facility rose to €202M from €171M prior

Corporateissuance saw no deals priced in high-grade primary

Looking Ahead

05:30 (DE) Germany to sell €3.0B in 0.5% Aug 2027 Bunds

05:30 (UK) DMO to sell £2.7B in 0.75% 2023 Gilts

06:30 (DE) Chancellor Merkel discusses the West's Future at Event in Berlin

06:45 (US) Daily Libor Fixing

07:00 (RU) Russia to sell combined RUB40B in 2024 and 2033 OFZ Bonds

07:00 (US) MBA Mortgage Applications w/e Aug 8th: No est v +0.1% prior

07:30 (CL) Chile Central Bank's Traders Survey

08:00 (BR) Brazil Aug IBGE Inflation IPCA-15 M/M: +0.4%e v -0.2% prior; Y/Y: 2.7%e v 2.8% prior

08:00 (PL) Poland July M3 Money Supply M/M: +0.3%e v -0.2% prior; Y/Y: 5.0%e v 5.0% prior

08:05 (UK) Baltic Dry Bulk Index

09:00 (MX) Mexico Jun Retail Sales M/M: +0.2%e v -0.1% prior; Y/Y: 2.8%e v 4.1% prior

09:05 (US) Fed's Kaplan speaks to Oil Group in Midland, Texas

09:30 (BR) Brazil July Current Account: -$3.4Be v +$1.3B prior; Foreign Direct Investment (FDI): $5.0Be v 4.0B prior

09:45 (US) Aug Markit Preliminary Manufacturing PMI: 53.5e v 53.3 prior, Services PMI: 55.0e v 54.7 prior, Composite PMI: No est v 54.6 prior

10:00 (US) July New Home Sales: 610Ke v 610K prior

10:00 (EU) Euro Zone Aug Advance Consumer Confidence: -1.8e v -1.7 prior

10:30 (US) Weekly DOE Crude Oil Inventories

11:00 (IT) Italy Debt Agency (Tesoro) announces upcoming CTZ auction for Aug 28th

11:30 (US) Treasury to sell $13B in 2-Year Floating Rate Notes Reopening

12:00 (CA) Canada to sell 5-Year Bonds

Dollar Flounders On Trump Comments

Wednesday August 23: Five things the markets are talking about

The EUR (€1.1781) is the standout currency in another low volume trading session, supported by better than expected flash manufacturing and service PMI's (see below) that continues to encourage investor confidence in the region's growth.

Elsewhere, comments from President Trump at a rally in Arizona yesterday evening again have provoked another bout of investor caution with gold and yen benefitting.

The President said he 'might terminate' the NAFTA trade treaty with Mexico and Canada after three-way talks failed to bridge deep differences and he would build a border wall with Mexico even if he has to shut down the U.S government to secure enough funding.

Geopolitical events continue to hover in the background. Investors are also keeping an eye on tensions between the U.S and North Korea, after the U.S and South Korea began joint military exercises on Monday.

Oil prices are under pressure after U.S gasoline inventories rose.

1. Global stocks mixed results

In Japan, the Nikkei share average posted modest gains overnight (+0.3%), snapping a five session losing that marked its longest losing streak in 12-months. Presidents Trumps overnight comments pared some of those gains. The broader Topix rallied +0.3%, but turnover remains subdued, with more than -10% below the recent average.

In South Korea, the Kospi index added +0.1%, while down-under, Australia's S&P/ASX 200 Index declined -0.2%.

In Hong Kong, trading was halted on Wednesday as a strong typhoon bared down on the financial centre and other parts of southern China.

In China, the main stock indexes ended little changed overnight, with profit taking in steel firms offsetting a rise in financials ahead of earnings reports. The CSI300 index rose +0.1%, while the Shanghai Composite Index fell -0.1%.

In Europe, Indices trade lower across the board tracking U.S futures, despite stronger than expected Manufacturing PMI readings out of Europe.

U.S stocks are set to open in the red (-0.2%).

Indices: Stoxx600 -0.3% at 374.8, FTSE +0.1% at 7388, DAX -0.1% at 12219, CAC-40 flat at 5133, IBEX-35 -0.1% at 10397, FTSE MIB -0.1% at 21698, SMI -0.3% at 8941, S&P 500 Futures -0.2%

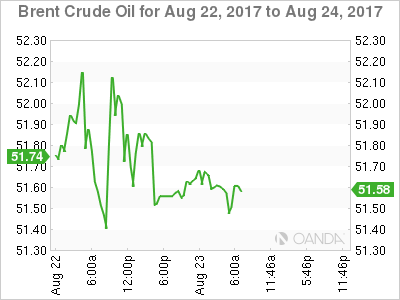

2. Oil prices fall on concerns of oversupply, gold higher

Ahead of the U.S open, oil prices trade under pressure, weighed down by concerns of oversupply as Libyan output improves and as U.S gasoline inventories rise.

Brent crude futures are at +$51.64 per barrel at 0721 GMT, down -23c, or -0.4% from Tuesday's close. U.S West Texas Intermediate (WTI) crude futures are at +$47.59 a barrel, down -24c, or -0.5%.

Libya's Sharara oil field was back on line Tuesday, although regional instability suggests that output could be volatile.

Note: Sharara recently reached output of +280k bpd, but closed earlier this week due to a pipeline blockade.

Libya's rising output is a headache for the OPEC, which together with non-OPEC producers have pledged to hold back around -1.8m bpd of supplies between January 2017 and March 2018 to tighten supplies.

The next meeting of OPEC and non-OPEC states to discuss their production pact has been proposed for Sept. 22.

Stateside yesterday, API crude inventories fell by -3.6m barrels in the week to Aug. 18 to +465.6m. However, gasoline stocks rose by +1.4m barrels, compared with expectations for a -643k decline.

Investors will take their cue from today's EIA report (10:30 am EDT).

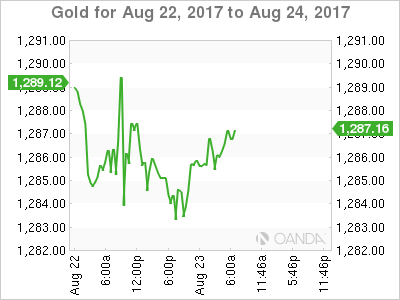

Gold prices inched up on Wednesday (+0.1% to +$1,285.30) as the dollar slipped after remarks by President Trump raised fears of a government shutdown. Expect investors to wait for further direction from this week's Jackson Hole symposium.

3. Yields back up a tad

In the absence of major economic data, bonds have been strongly influenced by market sentiment in recent sessions, a pattern that is expected to hold for much of this week until the Jackson Hole conference on Friday, which kicks off with a speech from Fed Chairwoman Janet Yellen on financial stability. A key question is whether Yellen will suggest the need for tighter monetary policy to address high asset prices.

While a trimming of expectations for a tighter ECB policy have helped push down yields across the eurozone, investors now seem reluctant to go any further without fresh policy cues.

With market speculation mounting about when the ECB will signal an exit from its ultra-loose monetary policy, Draghi's speech Friday remains a key focus for markets.

This morning, Eurozone government bond yields have backed up a tad ahead of the U.S open after a plethora of surveys showed the bloc's manufacturing businesses reported their best month of growth in nearly seven-years.

Germany's 10-year Bund yield gained +1 bps to +0.41%, while Britain's 10-year Gilt yield advanced +1 bps to +1.097%.

The yield on 10-year Treasuries increased less than +1 bps to +2.22%.

4. Pound struggles on Brexit investment woes

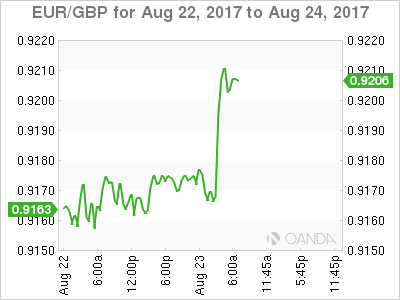

Sterling has fallen further, reaching its lowest reading in two months outright while the EUR/GBP breaks above the psychological €0.92 handle, as investors continue to shun the pound due to Brexit uncertainty.

GBP/USD falls -0.2% to a low of £1.2792, while EUR/GBP rises +0.4% to a high of €0.9215, as the U.K.'s release of policy papers on Brexit this week fails to reassure investors.

Above-forecast Eurozone manufacturing PMI's have benefitted the 'single unit' – the EUR/USD up +0.2% at €1.1787.

USD/JPY (¥109.35) is little changed.

5. Eurozone maintains solid growth in August

Data in Europe this morning showed that eurozone economy maintained its solid growth momentum this month, supported by a rise in manufacturing activity and strong exports, according to the regions PMI reports.

The composite PMI for the eurozone increased marginally to 55.8 from 55.7 in July, which marks a two-month high. The market had been expecting a decline to 55.4.

According to IHS Markit, the outcome signals 'strong growth' in the private sector, and the rate of expansion remained broadly 'the best seen over the past six years.'

Manufacturing activity picked up in July, boosted by 'the fastest rise in exports,' but services-sector activity hit a seven-month low, according to the survey.

Trump Warns Of Government Shutdown Over Wall

Speaking at a rally in Arizona overnight, US President Trump said that: 'if we have to close down our government, we are building that wall'. Even though this may be just rhetoric aimed at his supporters, given that building a border wall was a core theme of his campaign, his comments still suggest that the government may continue to seek funding for a wall in the upcoming budget. The deadline for Congress to reach a deal on the budget is September 30th, which is when the fiscal year ends.

This is a key issue because in case the new budget does not include funds for a wall, the President could veto it. At the same time, if it does include such funding, Congress is highly unlikely to vote for it. The Democrats have been very vocal in their opposition for such a project, and the Republicans have shown little willingness to fight for this issue. Therefore, if the President insists about keeping wall funds in the budget, then the prospect of a government shutdown could quickly become realistic.

In our view, a potential shutdown could dampen expectations for tax reform even further. It could highlight once again the division between the White House and Congress and send the signal that if the two sides cannot agree on a budget, then a complex tax overhaul is far less likely to materialize. As such, once Jackson Hole is out of the way and investors begin to focus more on this subject, speculation for a potential shutdown could begin to weigh on the assets that rallied after the election, namely the dollar and US equities.

USD/JPY traded higher yesterday after it hit the key support barrier of 108.70 (S1) on Monday. Nevertheless, the rate found resistance at 109.75 (R1) and retreated following Trump’s comments over a government shutdown. The pair has been oscillating between 108.70 (S1) and 111.00 (R3) since the 28th of July and therefore, we consider the short-term path to be sideways for now. Having said that, given that the latest recovery started after testing the lower bound of the aforementioned range, we would expect the bulls to take advantage of the overnight Trump pullback, or any extensions of it, and perhaps drive the rate above 109.75 (R1). If they manage to do so, we believe that they may target our next resistance of 110.35 (R2).

As for the bigger picture, on the daily chart we see that USD/JPY is trading within a broader range between 108.70 (S1) and 114.40 since mid-March. This keeps the medium-term outlook flat as well and enhances the case for a further recovery within the range. Nevertheless, if speculation over a potential government shutdown begins to heighten over the next weeks, this could bring the pair under renewed selling interest. In our view, a clear close below the key support zone of 108.70 (S1) is needed to turn the medium-term picture back negative.

Kiwi tumbles as government trims growth forecasts

NZD came under renewed selling interest overnight, after New Zealand’s government trimmed its GDP forecasts for the current year and the next. It also noted that it will not consider any tax cuts until 2020, unless economic conditions turn out better than currently expected. These reinforce our view that the outlook for NZD remains cautiously negative, amid lackluster economic data and an RBNZ worried about the high exchange rate.

NZD/USD tumbled on the news, fell below the support (now turned into resistance) of 0.7275 (R1), and now appears ready to challenge the 0.7225 (S1) barrier. Given that the rate is trading below the prior uptrend line drawn from the low of the 11th of May, and also below the short-term downtrend line taken from the peak of the 27th of July, we consider the near-term outlook to be negative. A break below 0.7225 (S1) would confirm a forthcoming lower low on the 4-hour chart and is possible to initially aim for our next support of 0.7200 (S2). Nonetheless, bearing in mind that the latest tumble appears overextended, we would stay mindful of a minor corrective rebound before the bears decide to take the reins again.

Today’s highlights:

During the European morning, Eurozone’s preliminary manufacturing and services PMIs for August will take center stage. The forecast is for the manufacturing index to slip somewhat, while the services print is expected to hold steady. Even though a decline in the manufacturing print could weigh on the euro somewhat, as long as these figures remain at healthy levels, we do not expect them to derail the ECB’s policy plans. We get preliminary Markit manufacturing and services PMI data for the month from the US as well.

We have two speakers on the schedule: ECB President Mario Draghi and Dallas Fed President Robert Kaplan. Considering all the recent speculation regarding some fresh policy signals on ECB policy, we expect market focus to be primarily on Draghi. Should he reiterate the risk of exchange rate overshooting, as the latest ECB minutes highlighted, then the common currency could correct lower.

USD/JPY

Support: 108.70 (S1), 108.00 (S2), 107.40 (S3)

Resistance: 109.75 (R1), 110.35 (R2), 111.00 (R3)

NZD/USD

Support: 0.7225 (S1), 0.7200 (S2), 0.7170 (S3)

Resistance: 0.7275 (R1), 0.7300 (R2), 0.7335 (R3

Euro Climbs After PMIs And Draghi Jackson Hole Warm Up Speech

- Draghi steers clear of monetary policy decisions ahead of Jackson Hole;

- EUR pops higher on strong manufacturing data;

- EIA seen reporting eighth consecutive drawdown in oil inventories.

It's been a slow start to trading on Wednesday, much in keeping with the rest of the week so far, as traders wait in anticipation of the Jackson Hole Symposium which takes place over the next few days.

The event will see both Federal Reserve Chair Janet Yellen and ECB President Mario Draghi speak on Friday, which will be of keen interest to traders. Both central banks are expected to be very active between now and year-end and Jackson Hole is the perfect platform to lay the foundation for upcoming policy moves. Whether they will or not remains to be seen.

If Draghi's comments today are anything to go by we should not get our hopes up. Draghi steered well clear of upcoming monetary policy decisions and if reports last week are to be believed, he may well do so again on Friday. The ECB is clearly very concerned about the recent appreciation in the euro – despite an insistence that it does not concern itself with such matters – and recent “misinterpretations” by traders to Draghi's comments will likely mean he steers clear once again.

The euro is trading a little higher this morning after some more strong survey data from the region. Manufacturing and services PMIs from the eurozone, Germany and France were all very strong and well above the level that separates growth from contraction, suggesting that the recovery is continuing to gain traction. Manufacturing was a particular strong point in all three cases, despite the fact that the currency moves this year represent a potential headwind for exporters.

Oil is coming under a little pressure this morning after API on Tuesday reports another drawdown in inventories last week. Should EIA confirm a decline of around 3.59 million today, it would fall in line with expectations and be the eighth consecutive weekly drop which suggests the output cut is taking its toll. The fact that oil rigs in the US have stabilised and last week actually fell slightly would also suggest the worst of the glut may be behind us.

Other US data being released throughout the session today includes manufacturing and services PMIs for August and new home sales data. We'll also get consumer confidence data from the eurozone, which is expected to remain below 0 – indicating pessimism – but it has improved dramatically over the last year and looks on the cusp of moving into positive territory for the first time since 2001. We'll also hear from Robert Kaplan today who is one of the policy makers that has become increasingly concerned about a lack of inflation and recently suggested he may be willing to wait before raising interest rates again.

Currencies: Dollar Rebound Remains Unconvincing

Sunrise Market Commentary

- Rates: Sentiment-driven trading, but Draghi's speech wildcard

Today's eco calendar contains EMU PMI's and consumer confidence. We don't expect large deviations from consensus. A speech by ECB President Draghi is the wildcard. Will he revive speculation on an APP tapering announcement or keep his cards close to his chest? We forecast trading to remain sentiment-driven ahead of speeches in Jackson Hole on Friday. - Currencies: Dollar rebound remains unconvincing

Yesterday, the dollar was in better shape supported by higher US yields and a positive risk sentiment. Overnight, Trump comments on NAFTA broke the positive USD momentum. Today's US eco data might be ok, but USD traders remain in waitand- see modus ahead of the CB speeches at Jackson Hole.

The Sunrise Headlines

- US equities put last week's political troubles behind and rallied to a 1% gain. Asian equity markets are less enthused this morning, trading mixed. Hong Kong is closed, bracing for Typhoon Hato. Iron ore takes a hit, weighing on AUD.

- US trade officials are putting together a proposal to let the US withdraw from a corporate arbitration system at the heart of NAFTA, upsetting big American companies that say the system protects their investments overseas.

- EU law will influence the UK long after Brexit, Theresa May conceded. It's a marked change of tone from seven months ago when she vowed to end the ECJ's jurisdiction. The compromise is an attempt to speed up divorce talks.

- German FM Schaeuble is working on a proposal that would allow southern euro zone countries to tap into the single currency bloc's bailout fund (ESM) to boost investments during recessions, according to Bild.

- The Nikkei-Markit Japan flash manufacturing PMI came in at 52.8 in August, up from 52.1 in July. Growth in output, new orders and employment all accelerated in the first three weeks of the month. NZD/USD loses some ground.

- New Zealand's government trimmed economic growth and budget surplus forecasts a month before a general election, limiting the ability of political parties to ramp up spending promises. NZD/USD loses some ground.

- Today's EMU eco calendar heats up with August Manufacturing & Services PMI's, consumer confidence and a speech by ECB president Draghi. Germany holds this week's only scheduled bond auction (2027).

Currencies: Dollar Rebound Remains Unconvincing

Dollar rebound remains unconvincing

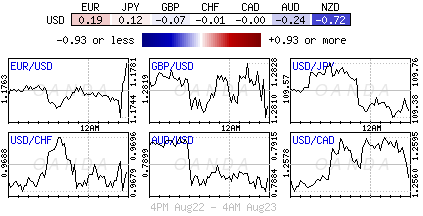

Yesterday, the dollar profited from a modest rise in US yields and a positive equity sentiment. Still, EUR/USD and USD/JPY held within the established ranges. Currency investors are looking forward to the CB speeches at Jackson Hole later this week. EUR/USD finished the session at 1.1762 (from 1.1815). USD/JPY was propelled by a nice US equity rebound end finished the day at 109.57 (from 108.98)

Overnight, Asian equities opened strong after the WS rally. USD/JPY filled offers in the 109.83 area but risk sentiment deteriorated after Donald Trump said he may end NAFTA at some point. He also threatened to shut down the US government if he wouldn't get the funding to build a wall along the Mexican border. Equities ceded part of the early gains. USD/JPY (currently 109.45) is off the intraday top (109.83). The Kiwi dollar (USD/NZD 0.7235) declined after the government cut its growth forecasts. A setback in Iron ore weighed on the Aussie dollar. AUD/USD dropped below 0.79. EUR/USD was little affected by the Trump comments.

This morning ECB-s Draghi will give a speech in Germany before leaving for Jackson Hole. Will he give any hints/details on the exit of the APP bond buying programme or will he abstain from doing so due to fear about a further strengthening of the euro. Most likely he won't dwell on these questions today but it's a wildcard. Regarding the data, ,the focus is on the EMU PMI's. The indices are slightly off the May highs, but stay on levels that suggest ongoing strong growth. Similarly, August consumer confidence is expected marginally lower(-1.8 from -1.7). US August PMI confidence is expected to have risen marginally to 53.5 (manufacturing) and 54.9 (services). We see a risk for an above consensus outcome, based on weaker dollar and signs retail sales are improving. The EMU data should be neutral for the euro. US data might in theory be USD supportive. However, this positive impact might be counterbalanced by the fall-out of the Trump comments on ending NAFTA. So, we expect yesterday's USD rebound to halt. A modest USD setback going into the Jackson Hole speeches is possible. However, we expect the established ranges to remain in place.

Broader context and technical picture. Late June, EUR/USD started a new upleg as investors anticipated a reduction of ECB bond buying to be announced in autumn. The Fed was expected to remove policy stimulation only in a very gradual way as US inflation remained soft. Uncertainty on the policy of the Trump administration was an secondary negative factor for the dollar. EUR/USD set a new correction top north of 1.19 before consolidating in a narrow 1.1662/1.1910 trading range. We expect this range will hold going into the Jackson Hole symposium. If US data remain ok (as most were this month) and if Draghi gives little information on next ECB steps, there might be room for a modest USD comeback. A return of EUR/USD to the 1.15/16 area is possible. Pockets of US political risk are a (negative) wildcard for the dollar. A downward correction in core (US and European) yields supported the yen in August. USD/JPY declined from the mid 114 area mid-July to 108.60. The April correction low (108.13) remains the line in the sand. For now, this level won't be easy to break as quite some USD bad news is discounted after the recent protracted setback. A cautious buy-on-dips approach (with stop-loss protection below 108) may be considered.

EUR/US: awaiting clearer CB guidance

EUR/GBP

EUR/GBP sets new highs

Sterling continued trading with a negative bias yesterday. Cable drifted from the high 1.28 area early in Europe to close the session at 1.2824. Most of this move was due to a rebound of the dollar, but sterling also set a minor new low against the euro. The UK data were not to blame. The UK August public budget showed an unexpected surplus and the CBI orders were better than expected. However, good eco/activity data don't help sterling these days as long as inflation remain modest and as there is little progress in the EU-UK Brexit talks. EUR/GBP closed the session at 0.9172.

Today, without UK eco data, the global risk sentiment and the headlines on the Brexit negotiations will set the tone for sterling trading. A cautious sentiment on risk is sterling negative. We also don't expect high profile positive Brexit news. So, despite the extensive sterling correction (especially against the euro) and the overbought EUR/GBP conditions, we don't see a trigger for a change in sentiment

From a technical point of view, EUR/GBP cleared the 0.8854/80 resistance (top end June), opening the way for further gains The move was the result of euro strength (ongoing strong EMU growth and expectations of the ECB reducing policy stimulus later this year). At the same time, UK price data remain soft enough for the BoE to keep a wait-and-see modus as the Brexit negotiations continue. MT, we maintain a buy EUR/GBP on dips approach as we expect the constellation of relative euro strength and sterling softness to continue. The 0.9415 flash-crash spike is the next MT target on the charts. However, we don't jump on the trend anymore after recent protracted EUR/GBP rally and wait for a correction, e.g to the technical support in the 0.88/89 area.

EUR/GBP: uptrend continues unabatedly

CRUDE OIL Holding Below The 200-DMA And Above 50-DMA

Crude oil is trading mixed. Hourly support is given at 46.46 (17/08/2017 high). Strong resistance can be found at 50.41 (31/07/2017). Expected to show continued short-term sideways move.

In the long-term, crude oil has recovered after its sharp decline last year. However, we consider that further weakness are very likely. Strong support lies at 35.24 (05/04/2016) while resistance can now be found at 55.24 (03/01/2017 high).

SILVER Consolidation Before Another Leg Higher

Silver's bullish pressures are on despite ongoing consolidation. Hourly resistance is given at 17.32 (18/08/2017 high) while support can be found at 16.58 (15/08/2017 high). The commodity lies in a short-term uptrend channel. Expected to show another leg higher.

In the long-term, the death cross indicates that further downsides are very likely. Resistance is located at 25.11 (28/08/2013 high). Strong support can be found at 11.75 (20/04/2009).

GOLD Consolidating Below 1300

Gold has broken strong resistance given at 1296 (06/06/2017 high) before bouncing lower. Hourly support is given at 1251 (08/08/2017 low). Stronger support lies at 1204 (10/07/2017 high). Expected to show continued consolidation below $1300.

In the long-term, the technical structure suggests that there is a growing upside momentum. A break of 1392 (17/03/2014) is necessary ton confirm it, A major support can be found at 1045 (05/02/2010 low)

BITCOIN Strong Bearish Retracement

Bitcoin is pausing after the massive surge over the past few days. Resistance is at all-time high at 4480 (17/08/2017 high). Hourly support lies very far at 2403 (26/07/2017 low). The road is wide open for another bullish move.

In the long-term, the digital currency has had an exponential growth. There are decent likelihood that the asset will consolidate above $1500. Long-term support is given at $1464 (04/05/2017 low).

EUR/CHF Bearish Flag Pattern

EUR/CHF's volatility is important. Hourly support is located at 1.1260 (04/08/2017 low). Expected to show further consolidation.

In the longer term, the technical structure has reversed. Strong resistance at 1.1200 (04/02/2015 high) has been broken. Yet,the ECB's QE programme is likely to cause persistent selling pressures on the euro, which should weigh on EUR/CHF. Supports can be found at 1.0184 (28/01/2015 low) and 1.0082 (27/01/2015 low).