Sample Category Title

European Open Briefing: Asian Equity Markets Steadied On Wednesday

Global Markets:

- Asian stock markets: Nikkei up 0.32 %, Shanghai Composite lost 0.21 %, Hang Seng up 0.42 %, ASX 200 down 0.10 %

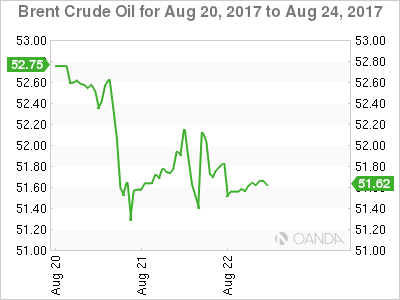

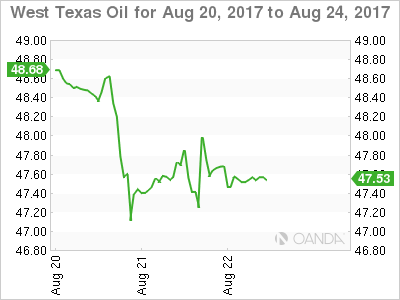

- Commodities: Gold at $1290.87 (-0.02 %), Silver at $16.97 (-0.02 %), WTI Oil at $47.73 (-0.21 %), Brent Oil at $51.75 (-0.23 %)

- Rates: US 10-year yield at 2.21, UK 10-year yield at 1.09, German 10-year yield at 0.40

News & Data:

- JPY Flash manufacturing PMI 52.8 vs 52.3 expected

- GBP Public Sector Net Borrowing -0.8 B vs 5.7 B previous

- EUR German ZEW Economic Sentiment 10.0 vs 14.8 expected

- CAD Core Retail Sales m/m 0.7 % vs 0.0 % expected

- CAD Retail Sales m/m 0.1 % vs 0.2 % expected

- North Korea's Kim orders production of more rocket engines, warhead tips- RTRS

- US president Trump threatens government shutdown over wall funding- FXL

Markets Update:

Asian equity markets steadied on Wednesday as investors continued to add risk positions despite uncertainties about what could emerge from a central banking conclave in Jackson Hole, which begins Thursday.

USDJPY carrying on its rally from US session managed to pop above highs of 109.80. However, it sold of almost immediately losing over 40 points and is currently seen trading around 109.40 handle as the US President Trump spoke at a rally for his supporters in Arizona threatening a government shutdown over the border wall with Mexico

AUDUSD continuing its decline and lost around 0.2 percent, The Aussie is currently seen trading at 78.90 against the US Dollar following the government’s announcement a month before a general election.

EURUSD is seen narrowing as we approach Jackson hole. Euro regained its Asia session earlier highs and is currently trading at 1.1760 against the US Dollar. On the other side, the dollar index against a basket of six major currencies continues to be little changed at 93.522 after rising 0.5 percent the previous day.

Upcoming Events:

- 07:00 GMT – (EUR) ECB President Draghi Speaks

- 07:00 GMT – (EUR) French Flash Manufacturing PMI

- 07:00 GMT – (EUR) French Flash Services PMI

- 07:30 GMT – (EUR) German Flash Manufacturing PMI

- 07:30 GMT – (EUR) German Flash Services PMI

- 08:00 GMT – (EUR) Flash Manufacturing PMI

- 08:00 GMT – (EUR) Flash Services PMI

- 13:05 GMT – (USD) FOMC Member Kaplan Speaks

- 14:00 GMT – (USD) New Home Sales

- 14:30 GMT – (USD) Crude Oil Inventories

Oil And Gold Feel The Cold

Oil and Gold’s price action was underwhelming overnight ahead of the Jackson Hole Symposium. Oil will look for salvation from tonight’s inventory data.

OIL

Crude oil contracts closed flat at the end of New York trading after a nascent rally was cut short by the American Petroleum Institute’s (API) Crude Inventory data. Although crude inventories fell by a pleasing 3.6 million barrels, gasoline inventories rose by a surprising 1.4 million barrels, not a good sign during the U.S. summer driving season.

Attention now turns to this evenings official Energy Information Administration’s (EIA) inventory data, with the street looking for drawdowns in crude and gasoline stocks of -3.1 million and -0.5 million barrels respectively. The data will more than likely decide the fate of crude prices this week with a lower than expected drawdown leading to deeper corrections in both Brent and WTI.

Brent spot trades unchanged this morning at 51.55 in directionless trading. Brent’s pricing remains the more constructive of the two contracts due to the backwardation in the front end of the futures curve. But overall, it continues to range trade in a broad 49.70 to 52.70 band, albeit with choppy intra-day price action.

WTI spot also trades unchanged at 47.50 hovering just below its 100-day average at 47.70. Key support comes in at 46.40 with the double top at 48.70 formidable resistance for now.

GOLD

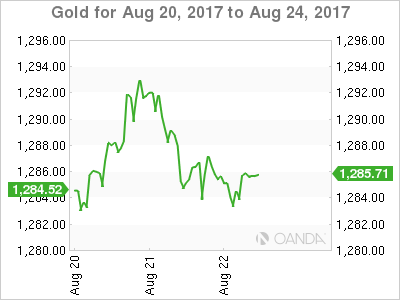

Gold gave up all its previous day’s gains, closing at 1285.00 overnight, as the U.S. dollar and stocks strengthened overnight. This marks the 4th successive failure of gold to close above 1290.00 in a row and the price action will be disappointing to gold bulls, with the street appearing to be in position squaring mode ahead of the Jackson Hole Symposium.

A deeper correction in the short term cannot be ruled out although in the bigger picture gold’s price action remains constructive.

Gold is trading slightly lower in Asia at 1283.50. Initial support will be found at 1280.00 but it is the 1278.00 level that traders will be watching. This is trend line support dating back to early July. A break of this level could imply a deeper technical correction is on the cards to the 1267.00 region.

After the spike on Friday to 1301.00, gold has marked out three consecutive lower daily highs. From a technical perspective gold now needs to see a daily close above 1301.00 to reinvigorate its upward trend.

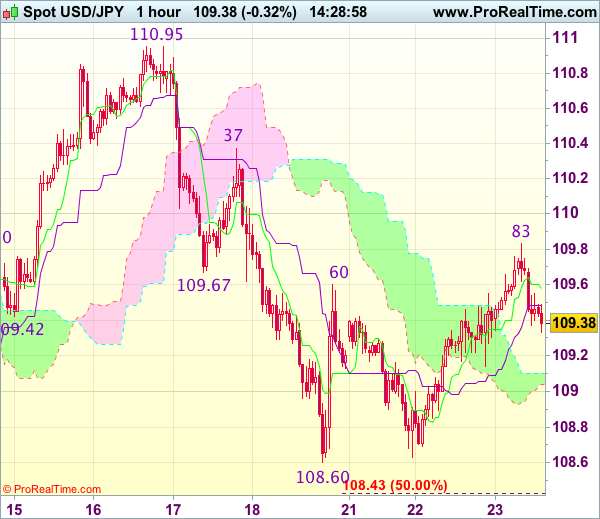

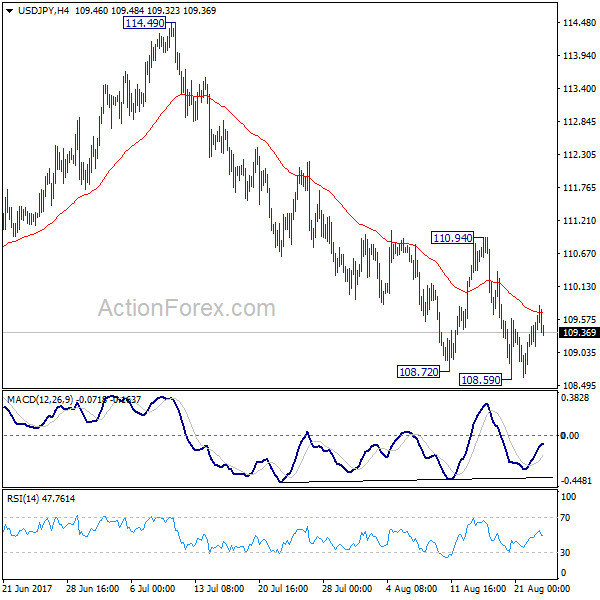

Trade Idea : USD/JPY – Stand aside

USD/JPY - 109.37

Most recent candlesticks pattern : N/A

Trend : Near term down

Tenkan-Sen level : 109.58

Kijun-Sen level : 109.49

Ichimoku cloud top : 109.10

Ichimoku cloud bottom : 109.04

New strategy :

Stand aside

Position : -

Target : -

Stop : -

Despite intra-day initial brief rise to 109.83, lack of follow through buying on break of resistance at 109.60-67 and the subsequent retreat suggest consolidation below this level would be seen and pullback to 109.00-10 cannot be ruled out, however, break there is needed to signal the rebound from 108.60 has ended there, bring further fall to 108.80, then test of said support. A break of this support would confirm recent decline has resumed and may extend further weakness to 108.30 (1.618 times projection of 110.95-109.67 measuring from 110.37), then towards 108.00.

On the upside, above said resistance at 109.83 would signal low has been formed at 108.60 and bring a stronger rebound to 110.00 and later towards resistance at 110.37 which is likely to hold from here. As near term outlook is still mixed, would be prudent to stand aside in the meantime.

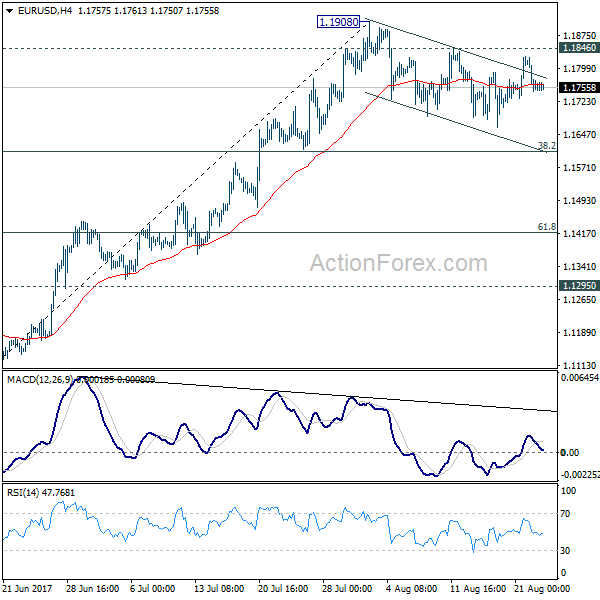

EUR/USD Daily Outlook

Daily Pivots: (S1) 1.1729; (P) 1.1776 (R1) 1.1809; More...

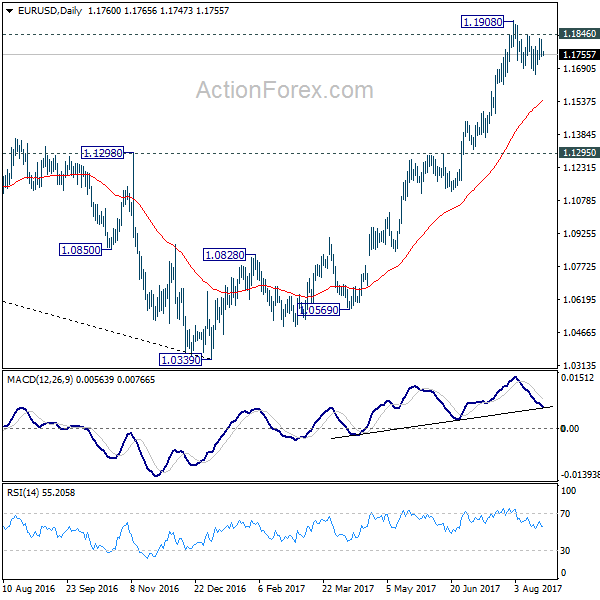

EUR/USD's consolidation from 1.1908 is extending and intraday bias stays neutral. In case of deeper fall, downside should be contained by 38.2% retracement of 1.1119 to 1.1908 at 1.1606 to bring up trend resumption. Break of 1.1846 minor resistance will argue that larger rise from 1.0339 is resuming for 1.2042 long term support turned resistance next.

In the bigger picture, an important bottom was formed at 1.0339 on bullish convergence condition in weekly MACD. Sustained trading above 55 month EMA (now at 1.1768) will pave the way to key fibonacci level at 38.2% retracement of 1.6039 (2008 high) to 1.0339 (2017 low) at 1.2516. While rise from 1.0339 is strong, there is no confirmation that it's developing into a long term up trend yet. Hence, we'll be cautious on strong resistance from 1.2516 to limit upside. But for now, medium term outlook will remain bullish as long as 1.1295 support holds, in case of pull back.

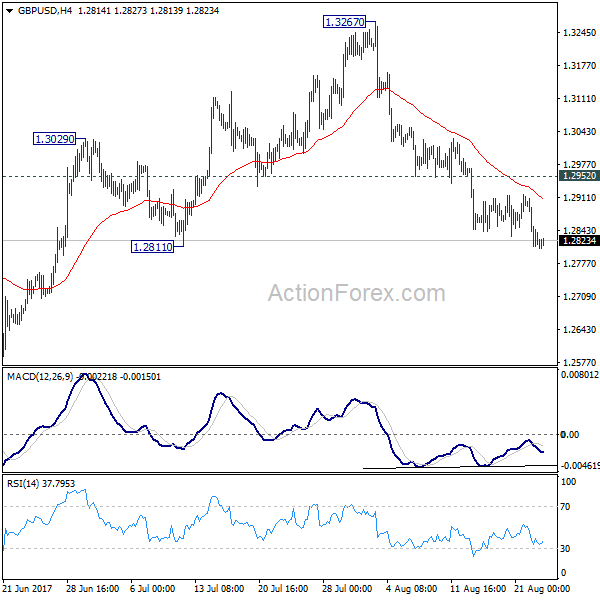

GBP/USD Daily Outlook

Daily Pivots: (S1) 1.2785; (P) 1.2847; (R1) 1.2883; More...

Intraday bias in GBP/USD remains on the downside as fall from 1.3267 is in progress for 1.2588 key near term support. As noted before, we're favoring the case that correction from 1.1946 is completed at 1.3267. Decisive break of 1.2588 will confirm our view and target a test on 1.1946 low. On the upside, break of 1.2952 resistance is needed to indicate completion of the fall from 1.3267. Otherwise, outlook will stay cautiously bearish in case of recovery.

In the bigger picture, overall, price actions from 1.1946 medium term low are seen as a corrective pattern. While further rise cannot be ruled out, larger outlook remains bearish as long as 1.3444 key resistance holds. Down trend from 1.7190 (2014 high) is expected to resume later after the correction completes. And break of 1.2588 will indicate that such down trend is resuming.

The Market Will Probably Go Into A Holding Pattern Ahead Of The Jackson Hole Symposium

Dollar Stays Firm After Bouncing On Position-Squaring. The dollar edged higher against a basket of currencies on Wednesday, after getting a boost the previous day as investors started to reduce their short dollar positions ahead of a global central bankers’ conference later this week and as the euro was weighed down by a weaker-than-expected reading on German investor confidence.

Gold Meets A Tough Resistance Level Of $1300. After trading to above $1300, resulting in gold prices reaching a three-month high, the stronger dollar and resumed market confidence led to a sell-off in precious metals. The gold price fell from a two-month high and is going to form a ‘triple top’ chart pattern if it continues to head south. It seems $1300 an ounce is a tough price point for gold to trade and close above. It is a matter of when, not if, when it comes to the question of whether gold prices will effectively breach the $1300 ceiling and close above it. Obviously, though, that will not occur in today’s trading session. If not for the strong U.S. dollar, gold prices would be unchanged on the day.

Mixed Retail Sales Data Supports The Loonie. The Canadian dollar was marginally weaker against U.S. dollar on Tuesday despite firmer oil prices, as the greenback rallied ahead of the annual Jackson Hole conference. Earlier in the session, the loonie had touched its strongest level in three weeks after robust domestic retail sales data for June bolstered expectations the Bank of Canada could raise interest rates again in October. The strength of the economy this year helped the central bank last month to raise rates for the first time in nearly seven years.

Oil Prices Slip After API Reports. The API reported a major drawdown on U.S. crude oil inventories of 3.595 million barrels – one-third of last week’s API-reported draw of 9.2 million. Also weighing in on oil prices this week so far has been news that OPEC’s November meeting would discuss the fate of the current agreement – whether it would extend the cuts further or decide to terminate it.

Watch Out This Week For:

WED., 10:00 am GMT: GBP Inflation Report Hearings

THURS., FRI., 24h: USD Jackson Hole Symposium

Market Update – Asian Session: Trump Expects To Pull Out Of NAFTA

Asia Summary

Asian equity markets opened mixed. Trading in HIBOR and the Hang Seng was suspended with a level 10 typhoon in Hong Kong. China markets remain under pressure, mostly related to commodity price (Dalian iron ore -5%) and China’s largest banks earnings reports starting tomorrow. At a rally President Trump commented on NAFTA, saying “Personally I dont think we can make a deal” and will probably end up terminating it at some point. He also alluded to allowing the government to shutdown if a deal if not reached on Mexico wall.

NZD fell 0.4% to 0.7250 after New Zealand Treasury released its pre-election economic and fiscal update that cuts 2018 GDP to 3.5% from prior view of 3.7%, it also cut expected surpluses for the coming years. In Indonesia the central bank decision to cuts rates sent shares of property developer, banks and automotive stocks and sends the benchmark stock index to a near record high. PBOC drained funds through OMO for the 3rd consecutive session.

Key economic data

(AU) AUSTRALIA JUL SKILLED VACANCIES M/M: 0.8% V 0.9% PRIOR

(JP) JAPAN AUG PRELIM PMI MANUFACTURING: 52.8 V 52.1 PRIOR FINAL

Speakers and Press

China/Hong Kong

(CN) China State Council Development Research Center deputy director Yiming: Economic growth in 2017 may exceed target set at the beginning of this year as major indicators in 1H were better than expected

(CN) China Finance Ministry confirms plan to roll over CNY600B ($90B) in special bonds issued 10 years ago to launch the country's sovereign wealth fund - US financial press

(CN) China Rare Earth Association has suggested releasing state stockpiles

Korea

(KR) US Sec of State Tillerson: North Korea is demonstrating some level of restraint; hopes there can be dialogue with North Korea - comments in DC

Australia/New Zealand

(NZ) New Zealand Treasury (DMO) affirms Govt bond program NZ$7B in year to June 2018; adjusts surplus and GDP outlooks

Other

(US) President Trump comments on NAFTA: Personally I dont think we can make a deal, will probably end up terminating it at some point

Asian Equity Indices/Futures (00:30ET)

Nikkei +0.3%, Hang Seng closed; Shanghai Composite -0.2%, ASX200 -0.2%, Kospi -0.03%

Equity Futures: S&P500 -0.2%; Nasdaq100 -0.1%, Dax -0.2%, FTSE100 -0.3%

FX ranges/Commodities/Fixed Income (00:30ET)

EUR 1.1766-1.1748; JPY 109.83-109.37; AUD 0.7918-0.7883; NZD 0.7283-0.7232

Dec Gold -0.0% at $1,290/oz; Oct Crude Oil -0.2% at $47.73/brl; Sept Copper -0.4% at $2.98/lb

(CN) China PBOC OMO injects CNY180B v CNY60B in 7 and 14-day reverse reports prior: net drains CNY40B v drains CNY10B prior

USD/CNY *(CN) PBOC SETS YUAN REFERENCE RATE AT 6.6633 V 6.6597 PRIOR

(NZ) New Zealand Local Government Funding Agency sells combined NZ$50M v NZ$50M indicated in 2023 and 2027 bonds

(CN) China MoF sells 3-yr bonds; avg yield 3.4865%; bid-to-cover 2.25x

Equities notable movers

Hong Kong/China

728.HK Reports H1 (CNY) Net 12.6B v 11.7B y/y; EBITDA 52.4B, +3.7% y/y; Op Rev 184.1B v 176.8B y/y

Australia/New Zealand

WOR.AU Reports FY17 (A$) underlying net 123.3M v 128Me, underlying EBIT 257.8M v 257Me; Rev 5.22B v 7.79B y/y; -0.3%

IAG.AU Reports FY17 (A$) Net profit 929M v 927Me, Gross Written Premiums 11.8B v 11.4B y/y; -7%

TGR.AU Reports FY17 (A$) Net 58.1M v 48.5M y/y, Op EBITDA 114.6M v 90Me; Rev 451M v 431M y/y; +5.3%

HSO.AU Reports FY17 (A$) Net 180M v 184Me; EBITDA 411.4M v 429Me; Rev 2.32B v 2.4Be; -13%

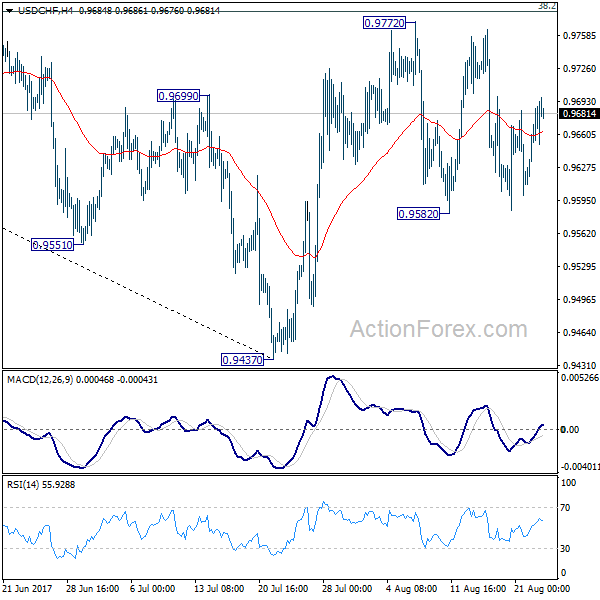

USD/CHF Daily Outlook

Daily Pivots: (S1) 0.9630; (P) 0.9659; (R1) 0.9711; More....

USD/CHF is still staying in sideway trading in range of 0.9582/9772. Intraday bias remains neutral for the moment. On the upside, decisive break of 0.9772 resistance will revive the bullish case of reversal. That is, whole decline from 1.0342 has completed at 0.9437 after defending 0.9443 support. USD/CHF should then target channel resistance (now at 0.9862) next. Meanwhile, the pair is bounded inside medium term falling channel and limited below 38.2% retracement of 1.0342 to 0.9437 at 0.9783 for the moment. Break of 0.9582 will turn bias back to the downside for 0.9437. This could also extend the fall from 1.0342 through 0.9437/43 key support level.

In the bigger picture, we're slightly favoring the case that USD/CHF has successfully defended 0.9443 key support level. And long term range trading in 0.9443/1.0342 is extending with another rise. At this point, there is no sign of an up trend yet. Hence, while further rise is expected in USD/CHF, we'll start to be cautious on loss of momentum above 61.8% retracement of 1.0342 to 0.9437 at 0.9996. However, firm break of 0.9443 will carry larger bearish implication and would target next key support at 0.9072.

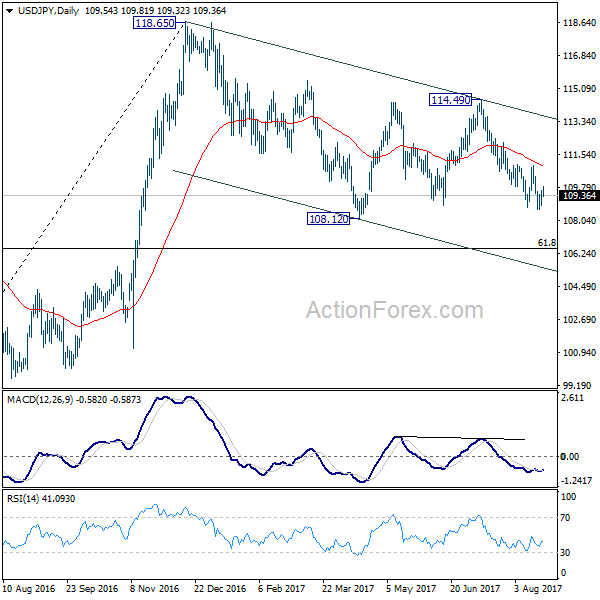

USD/JPY Daily Outlook

Daily Pivots: (S1) 109.04; (P) 109.35; (R1) 109.85; More...

USD/JPY is staying in consolidation above 108.59 temporary low and intraday bias remains neutral. Near term outlook stays bearish with 110.94 resistance intact and deeper decline is expected. Break of 108.59 will target a test on 108.12 low. Whole corrective decline from 118.65 is possibly resuming and break of 108.12 will target 61.8% retracement of 98.97 to 118.65 at 106.48. Nonetheless, firm break of 110.94 will indicate short term bottoming and turn bias back to the upside.

In the bigger picture, the corrective structure of the fall from 118.65 suggests that rise from 98.97 is not completed yet. Break of 118.65 will target a test on 125.85 high. At this point, it's uncertain whether rise from 98.97 is resuming the long term up trend from 75.56, or it's a leg in the consolidation from 125.85. Hence, we'll be cautious on topping as it approaches 125.85. If fall from 118.65 extends lower, downside should be contained by 61.8% retracement of 98.97 to 118.65 at 106.48 and bring rebound.

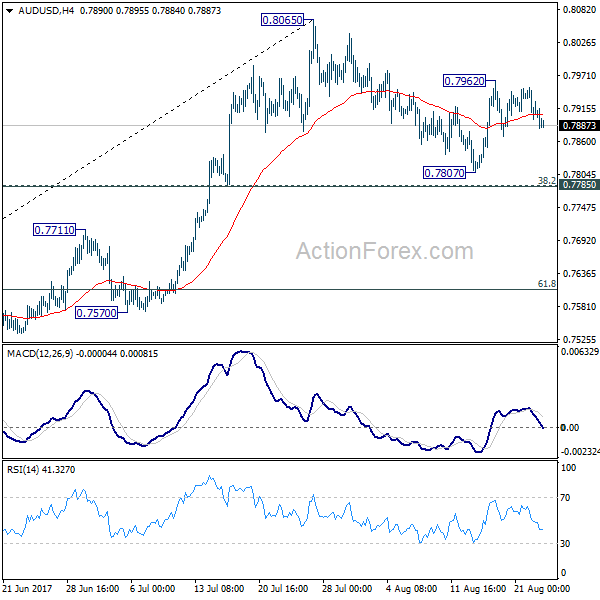

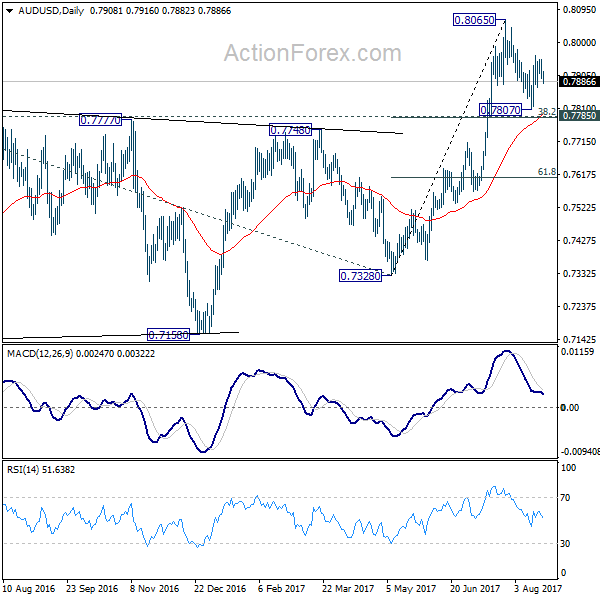

AUD/USD Daily Outlook

Daily Pivots: (S1) 0.7887; (P) 0.7919; (R1) 0.7940; More...

Intraday bias in AUD/USD is turned neutral again as the pair lost upside moment. Correction from 0.8065 might extend. But downside should be contained by 0.7785 cluster support (38.2% retracement of 0.7328 to 0.8065 at 0.7783) to bring rebound. Above 0.7962 will target a test on 0.8065 resistance first. Firm break of 0.8065 will resume the medium term rise and target 100% projection of 0.6826 to 0.7833 from 0.7328 at 0.8335.

In the bigger picture, rise from 0.6826 medium term bottom is still in progress. At this point, there is no confirmation of trend reversal yet and we'll continue to treat such rebound as a corrective pattern. But in any case, break of 55 month EMA (now at 0.8097) will target 38.2% retracement of 1.1079 to 0.6826 at 0.8451. Break of 0.7328 support is needed to confirm completion of the rebound. Otherwise, further rise is now in favor.